|

市场调查报告书

商品编码

1645120

非洲食品低温运输物流 -市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Africa Food Cold Chain Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

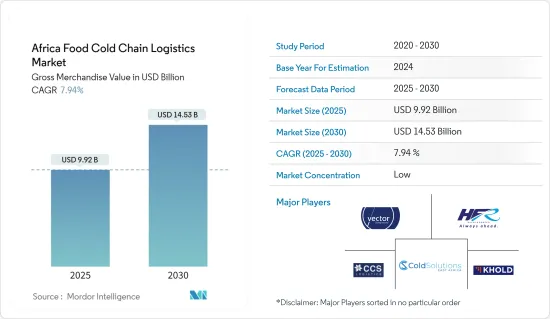

基于商品总价值,非洲食品低温运输物流市场规模预计将从 2025 年的 99.2 亿美元成长到 2030 年的 145.3 亿美元,预测期内(2025-2030 年)的复合年增长率为 7.94%。

生活方式的改变和都市化促进了该国加工食品消费量的增加,同时,随着人们的健康意识增强、需要解决食物浪费问题和确保粮食安全,消费模式的改变(包括新鲜水果消费量的增加)也是支持市场成长的因素。

气候危机是造成非洲严重粮食不安全和粮食浪费的主要原因。据估计,非洲生产的三分之一以上的食物因变质或浪费而损失。联合国粮食及农业组织估计,撒哈拉以南非洲地区超过 40% 的食物在到达消费者手中之前就被浪费了。撒哈拉以南非洲的生鲜食品的比例上升至 60%。

食物浪费的主要原因是腐败,尤其是由于缺乏仓储设施来延长对温度敏感的食物的保质期。非洲农民和农业承包商依赖临时冷却器和过时的通用冷藏室。这些系统不可靠、维护不善且运作成本高。

冷藏仓库和冷藏供应链产品有助于减少损失并维持产品的品质和效力,但它们需要足够的电力才能有效运作。根据非洲开发银行(AfDB)统计,非洲有超过 6.4 亿人无法用电,维持持续低温也是一项挑战。非洲迫切需要建立一个有弹性、可靠和永续的低温运输,以解决食品和药品损失问题。

一些非洲新兴企业正在创新数位解决方案以应对新的挑战。这些新兴企业提供节能且符合出口要求的冷藏产品和解决方案。它们价格合理,并配有全面的温度和性能监控系统。

根据低温运输储存产业报告,东非的低温运输基础设施更发达,而南部非洲的低温运输基础设施更发达,并迎合出口商的需求。

非洲食品低温运输物流市场趋势

电力危机对南非食品低温运输物流市场造成负面影响

南非目前拥有非洲大陆大部分的冷藏容量,并拥有多种正冷藏(新鲜水果、蔬菜)和负冷藏(鱼、肉)选择。许多在非洲营运的低温运输物流供应商的总部都设在南非。但该国电力短缺现象严重,各地区普遍停电,每天停电时间长达10小时。根据矿产资源和能源部的数据,南非国内总发电量为 58,095 兆瓦(MW)。煤炭仍是主要能源来源,占该国能源结构的80%左右。然而,一些燃煤电厂老化、状况恶化,导致实际发电量严重短缺,缺口达4,000-6,000兆瓦。

这种短缺导致了严重的停电,也称为「负载削减」。可靠、稳定的能源供应对于维持低温运输至关重要。在电力不稳定或不可靠的地区,温控环境受到干扰的风险会增加。这些中断对农业领域的低温运输产生了不利影响,尤其是影响了生鲜食品的储存和运输。据报道,由于运输延迟和低温运输中断,一些零售商拒绝生鲜食品,而这种情况在天气炎热时会更加严重。此次能源危机对南非食品低温运输物流市场提出了重大挑战。

新鲜水果出口促进市场成长

埃及是该地区最大的水果和蔬菜出口国。埃及每年透过出口各种新鲜、干燥和冷冻水果和蔬菜产品赚取约 30 亿美元。出口到国际市场的主要产品包括柳橙、马铃薯、冷冻草莓、鲜食葡萄和新鲜洋葱。南非在出口市场也扮演着重要角色。南非的农业部门明显以出口为导向,约有一半的产量以金额为准出口。南非水果产业在该国农业出口中占据主导地位,新鲜水果约占南非农业出口的35%。数十年来针对种植者和行业协会的研发和能力建设倡议帮助生产出能够在全球有效竞争的高品质水果。

南非在全球水果生产中占有重要地位,是世界第二大柑橘出口国、第六大梨生产国、第七大葡萄出口国、第八大苹果出口国和第九大酪梨出口国。在出口市场方面,南非水果产业的目标是维持并扩大在欧盟、英国和美国的传统市场。此外,公司的策略重点是进入东亚和中东的新市场。非洲是南非多种水果的重要潜在出口市场。目前,苹果和梨在西非和东非的销售情况良好。这些水果在非洲国内外的出口是低温运输物流的重要需求驱动力,凸显了持续发展低温运输基础设施的重要性。

非洲食品低温运输物流产业概况

鑑于非洲大陆的多样性,当地和区域物流供应商发挥关键作用。区域参与者是非洲食品低温运输物流市场的主要参与企业。这些公司对当地市场动态、法规和基础设施挑战有更好的了解。低温运输物流业务集中在非洲大陆南部地区。提供运输、仓储和配送等综合低温运输服务的公司具有竞争优势。这些服务的无缝协调对于保持温度敏感食品的完整性至关重要。 CCS Logistics、Khold、Cold Solutions East Africa、Vector Logistics、HFR Transport 等是市场的主要企业。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概况

- 价值链/供应链分析

- 政府对产业的监管和倡议

- 市场技术开发

- 深入了解市场上的创新新兴企业(Solar Freeze、InspiraFarms、Coldbox Store、ColdHubs、Freezelink)

- 新冠肺炎疫情对市场的影响

第五章 市场动态

- 驱动程式

- 水果出口增加

- 限制因素

- 电力危机

- 机会

- 缺乏冷藏设施导致食物浪费

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买家的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

第六章 市场细分

- 按服务

- 贮存

- 运输

- 附加价值服务(冷冻、标籤、库存管理等)

- 按温度

- 冷藏

- 冷冻

- 常温

- 按产品类型

- 园艺(新鲜水果和蔬菜)

- 乳製品(牛奶、冰淇淋、奶油等)

- 肉类、家禽、鱼贝类

- 加工食品

- 其他的

- 按国家

- 埃及

- 奈及利亚

- 南非

- 其他国家

第七章 竞争格局

- 市场集中度

- 公司简介

- CCS Logistics

- Khold

- Cold Solutions East Africa

- Vector Logistics

- HFR Transport

- Africa Cold Chain Limited

- African Perishable Logistics

- Unitrans

- Africa Global Logistics (AGL)

- Go Global

- Lieben Logistics

- BigCold Kenya Ltd

- Southern Shipping Services Ltd (SSSL)*

- 其他公司

第 8 章:市场的未来

第 9 章 附录

The Africa Food Cold Chain Logistics Market size in terms of gross merchandise value is expected to grow from USD 9.92 billion in 2025 to USD 14.53 billion by 2030, at a CAGR of 7.94% during the forecast period (2025-2030).

Changes in lifestyle and urbanization contributing to increased domestic consumption of processed foods and a shift in consumption patterns, including increased consumption of fresh fruits, as people become more health concerned, need to address food wastage and ensure food security, are the factors assisting the market's growth.

The climate change crisis has significantly contributed to the dire food insecurity and food wastage in Africa. Over one-third of food produced in Africa is estimated to be lost to spoilage or waste. The United Nations Food and Agriculture Organization estimates that over 40% of food in Sub-Saharan Africa perishes before it reaches a consumer. This can be as high as 60% for fresh produce in Sub-Saharan Africa.

The leading cause of food wastage is spoilage due to the lack of cold storage facilities to extend the shelf life, especially temperature-sensitive food items. Farmers and agri-traders in Africa rely on makeshift coolers or outdated, generic cold rooms. These systems are unreliable, poorly maintained, and have high operational costs.

Cold storage or cold supply chain products can help reduce spoilage and maintain quality and efficacy, but they require sufficient electricity to work effectively. In Africa, according to the African Development Bank (AfDB), electricity is out of reach for more than 640 million people, and the ability to sustainably maintain constant cold temperatures remains a challenge. There is an urgent need to deploy resilient, reliable, and sustainable cold chains to tackle food and medicine losses in Africa.

Several startups in Africa are innovating digital solutions to respond to emerging challenges. These startups offer cold storage products and solutions that are energy-efficient and compliant with export standards. They are also affordable and well-equipped with temperature and performance monitoring systems.

According to a Cold Chain Storage industry report, the cold chain infrastructure is developing in East Africa, with cold chain infrastructure in Southern Africa being more developed and geared toward exporters.

Africa Food Cold Chain Logistics Market Trends

Electricity Crisis is Negatively Affecting the South African Food Cold Chain Logistics Market

South Africa currently hosts most of the continent's cold storage capacity, encompassing many positive (fresh fruit and vegetables) and negative (fish and meat) cold storage options. Numerous cold chain logistics providers operating in Africa are headquartered in South Africa. However, the country is grappling with significant electricity shortages, resulting in widespread daily power cuts lasting up to 10 hours in various regions. As per the Ministry of Mineral Resources and Energy, South Africa's total domestic electricity generation capacity is 58,095 megawatts (MW). Coal remains the predominant energy source, constituting approximately 80% of the country's energy mix. Nonetheless, due to the aging and deteriorating condition of some coal power stations, actual power generation falls substantially short, creating a deficit ranging between 4000 - 6000 MW.

This shortfall has led to severe power cuts, also known as 'load shedding.' A reliable and consistent energy supply is crucial for maintaining the cold chain. In regions with inconsistent or unreliable power, the risk of disruptions to temperature-controlled environments increases. These power cuts are adversely affecting the cold chains within the agricultural sector, particularly impacting the storage and transport of fresh produce. Reports indicate that some retailers have rejected fresh produce due to delivery delays and disruptions in the cold chain, exacerbating the situation during warmer months. This energy crisis is a significant challenge for the South African food cold chain logistics market.

Fresh Fruit Exports are Contributing to the Growth of the Market

Egypt holds the position of being the largest exporter of fruits and vegetables in the region. Annually, the country generates approximately USD 3 billion in revenue from exporting various fresh, dried, and frozen fruit and vegetable products. Key products exported to international markets include oranges, potatoes, frozen strawberries, table grapes, and fresh onions. South Africa also plays a vital role in the export market. The agricultural sector in South Africa is distinctly export-focused, with approximately half of its produce being exported in value terms. The South African fruit industry is a predominant force in the country's agricultural exports, with fresh fruit accounting for around 35% of South African agricultural exports. Decades of research and development and capacity-building initiatives for growers and industry associations have been instrumental in producing high-quality fruit that can compete effectively globally.

South Africa boasts significant rankings in global fruit production, including being the world's 2nd largest citrus exporter, 6th largest pear producer, 7th largest grape exporter, 8th largest apple exporter, and 9th largest avocado exporter. Regarding export markets, the South African fruit industry aims to retain and maximize its traditional markets within the European Union, the United Kingdom, and the United States. Additionally, there is a strategic focus on gaining access to new markets in East Asia and the Middle East. Africa represents a substantial potential export market for various types of fruit from South Africa. Presently, apples and pears are performing well in West and East Africa. The export of these fruits within and outside Africa is a significant demand driver for cold chain logistics, emphasizing the importance of ongoing development in cold chain infrastructure.

Africa Food Cold Chain Logistics Industry Overview

Given the diversity of the African continent, local and regional logistics providers play a crucial role. Regional players are the major players in the African food cold chain logistics market. They have a better understanding of local market dynamics, regulations, and infrastructure challenges. Cold Chain logistics operations are concentrated in the Southern region of the continent. Companies that offer integrated cold chain services, including transportation, warehousing, and distribution, have a competitive advantage. Seamless coordination of these services is essential for maintaining the integrity of temperature-sensitive food products. CCS Logistics, Khold, Cold Solutions East Africa, Vector Logistics, and HFR Transport are some of the key players in the market.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Value Chain/Supply Chain Analysis

- 4.3 Government Regulations and Initiatives in the Industry

- 4.4 Technological Developments in the Market

- 4.5 Insights on Innovative Startups in the Market (Solar Freeze, InspiraFarms, Coldbox Store, ColdHubs, and Freezelink)

- 4.6 Impact of the COVID - 19 Pandemic on the Market

5 MARKET DYNAMICS

- 5.1 Drivers

- 5.1.1 Increasing Fruit Exports

- 5.2 Restraints

- 5.2.1 Electricity Crisis

- 5.3 Opportunities

- 5.3.1 Food Wastage Due to Lack of Cold Storage Facilities

- 5.4 Industry Attractiveness - Porter's Five Forces Analysis

- 5.4.1 Bargaining Power of Suppliers

- 5.4.2 Bargaining Power of Buyers

- 5.4.3 Threat of New Entrants

- 5.4.4 Threat of Substitutes

- 5.4.5 Intensity of Competitive Rivalry

6 MARKET SEGMENTATION

- 6.1 By Service

- 6.1.1 Storage

- 6.1.2 Transportation

- 6.1.3 Value-added Services (Blast Freezing, Labeling, Inventory Management, etc.)

- 6.2 By Temperature

- 6.2.1 Chilled

- 6.2.2 Frozen

- 6.2.3 Ambient

- 6.3 By Product Category

- 6.3.1 Horticulture (Fresh Fruits and Vegetables)

- 6.3.2 Dairy Products (Milk, Ice Cream, Butter, etc.)

- 6.3.3 Meat, Poultry, and Seafood

- 6.3.4 Processed Food Products

- 6.3.5 Other Categories

- 6.4 By Country

- 6.4.1 Egypt

- 6.4.2 Nigeria

- 6.4.3 South Africa

- 6.4.4 Other Countries

7 COMPETITIVE LANDSCAPE

- 7.1 Market Concentration

- 7.2 Company Profiles

- 7.2.1 CCS Logistics

- 7.2.2 Khold

- 7.2.3 Cold Solutions East Africa

- 7.2.4 Vector Logistics

- 7.2.5 HFR Transport

- 7.2.6

Africa Cold Chain Limited

- 7.2.7 African Perishable Logistics

- 7.2.8 Unitrans

- 7.2.9 Africa Global Logistics (AGL)

- 7.2.10 Go Global

- 7.2.11 Lieben Logistics

- 7.2.12 BigCold Kenya Ltd

- 7.2.13 Southern Shipping Services Ltd (SSSL)*

- 7.3 Other Companies

8 FUTURE OF THE MARKET

9 APPENDIX

食品物流市场:依运输方式、温度控制、产品类型、服务类型及最终用户划分-2026-2032年全球市场预测

食品物流市场:依运输方式、温度控制、产品类型、服务类型及最终用户划分-2026-2032年全球市场预测 食品物流市场规模、份额、趋势和预测:按运输方式、产品类型、服务类型、细分市场和地区划分,2026-2034年

食品物流市场规模、份额、趋势和预测:按运输方式、产品类型、服务类型、细分市场和地区划分,2026-2034年 2026年全球食品低温运输市场报告2026年全球智慧食品物流市场报告全球食品冷藏物流服务市场(依运输方式、附加价值服务、仓储配送及运输划分)预测(2026-2032年)食品冷藏和冷冻供应链物流市场:按仓储、包装和标籤、订单履行和运输划分,全球预测,2026-2032年日本食品物流市场规模、份额、趋势及预测(依运输方式、产品类型、服务类型、细分市场及地区划分),2026-2034年

2026年全球食品低温运输市场报告2026年全球智慧食品物流市场报告全球食品冷藏物流服务市场(依运输方式、附加价值服务、仓储配送及运输划分)预测(2026-2032年)食品冷藏和冷冻供应链物流市场:按仓储、包装和标籤、订单履行和运输划分,全球预测,2026-2032年日本食品物流市场规模、份额、趋势及预测(依运输方式、产品类型、服务类型、细分市场及地区划分),2026-2034年 食品物流市场规模、份额及成长分析(依运输方式、服务、产品、仓储设施及地区划分)-2026-2033年产业预测

食品物流市场规模、份额及成长分析(依运输方式、服务、产品、仓储设施及地区划分)-2026-2033年产业预测 食品低温运输:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年)

食品低温运输:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年) 食品低温运输市场规模、份额和趋势分析报告:按类型、建设类型、应用、地区和细分市场预测,2025-2033 年

食品低温运输市场规模、份额和趋势分析报告:按类型、建设类型、应用、地区和细分市场预测,2025-2033 年