|

市场调查报告书

商品编码

1642963

发电机租赁:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)Power Generator Rental - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

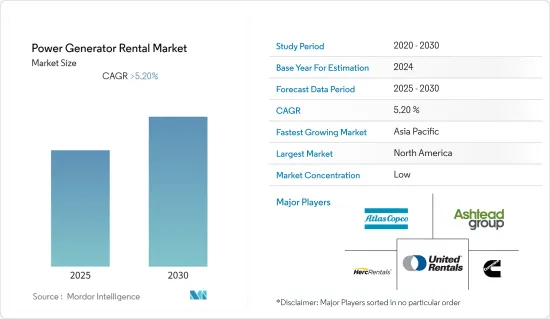

预测期内,发电机租赁市场预计将以超过 5.2% 的复合年增长率成长。

市场受到了 COVID-19 的不利影响。目前市场已恢復至疫情前的水准。

关键亮点

- 推动发电机租赁市场发展的因素包括购买新发电机的成本以及石油和天然气以及建筑等各个领域的重大发展。

- 然而,配电网的扩张和可再生能源计划的市场不断开发预计将抑制市场的成长。

- 随着人口的成长,预计各领域的计划将会增加以满足日常生活的需求,包括能源、商业和居住空间、製造设备等。例如,预计到 2030 年世界人口将达到近 85 亿,这可能会使全球建筑支出增加到 175 亿美元。建筑业的成长意味着全球发电机租赁市场可能会成长。

- 北美是发电机租赁市场的关键地区。预计定期停电、各行业新计画安装、自然灾害以及季节性电力需求高峰将主要推动该地区的发电机租赁市场的发展。

发电机租赁市场趋势

石油和天然气行业发电机组实现巨大成长

- 石油和天然气产业在发电机租赁市场占有重要份额。大多数计划地处偏远,油井的预期深度各不相同,因此需要能够在恶劣环境下运作的大容量发电机。

- 发电机将作为钻井/挖掘和电力备用活动的电源。在钻孔或挖掘时,需要大量电力来运作设备。发电机在紧急情况和灾难期间为石油和天然气设施提供电源备用。

- 根据国际能源总署预测,2021年上游油气投资将达3,840亿美元。上游投资的年增长率为 8.8%,预计在预测期内将增加,这可能会推动石油和天然气行业的发电机市场,因为钻井和钻探需要大量电力。

- 对于油田组装来说,石油和天然气工业通常最倾向于使用两个轴承的 1,200 rpm、6 极交流发电机。此外,发电机的交流发电机必须承受马达启动时所引起的25-30%的电压降。

- 在预测期内,预计石油和天然气行业将因探勘和生产 (E&P) 活动支出的增加而推动发电机租赁市场的发展。预计到 2025 年,石油和天然气产业的投资将达到近 7,000 亿美元,这可能会推动发电机租赁市场的发展。

北美可望成为重要市场

- 北美发电机租赁市场预计将大幅成长,主要得益于柴油发电机。然而,随着减少二氧化碳排放的环境措施加强,替代燃料发电机也越来越受到关注。

- 石油和天然气产业需要大量电力来支援其上游和下游製程。北美的石油消费量与前一年同期比较增加,从而产生了对石油生产的需求,预计这将在预测期内推动发电机租赁市场的发展。 2021年,北美石油消费量总量为2,226.4万桶/日,年增率为7.6%。

- 美国是使用天然气发电机来创造清洁环境的着名国家之一。由于天然气发电机在运作过程中故障较少,因此其依赖性很高。天然气发电机在运作过程中通常每千瓦时可节省 1,000 至 3,000 美元。

- 不断增长的能源需求、基础设施计划和联繫电力需求是推动北美发电机租赁市场发展的一些主要因素。预计美国石油和天然气产业将获得约 2.5 亿美元的投资,预计这将在预测期内推动市场发展。

- 预计预测期内该地区建筑业将吸引超过 1 兆美元的投资。该行业以及石油和天然气行业的成长预计将进一步推动租赁发电机市场的发展。

发电机租赁业概况

发电机租赁市场是细分的。市场的主要企业(不分先后顺序)包括阿特拉斯·科普柯(印度)有限公司、康明斯公司、阿什特德集团有限公司、现代招聘服务公司、联合租赁公司、Herc Rentals Inc.、Generac Power Systems、瓦克诺森集团和瓦锡兰公司。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究范围

- 市场定义

- 调查前提

第 2 章执行摘要

第三章调查方法

第四章 市场概况

- 介绍

- 2028 年发电机租赁市场(百万美元)

- 最新趋势和发展

- 政府法规和政策

- 市场动态

- 驱动程式

- 限制因素

- 工业供应链分析

- 波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争强度

第五章 市场区隔

- 按最终用户

- 石油和天然气

- 建造

- 矿业

- 製造业

- 资料中心

- 其他的

- 按地区

- 北美洲

- 亚太地区

- 欧洲

- 南美洲

- 中东和非洲

第六章 竞争格局

- 併购、合资、合作与协议

- 主要企业策略

- 公司简介

- 阿特拉斯·科普柯(印度)有限公司

- Wartsila Corporation

- Wacker Neuson Group

- Generac Power Systems

- Herc Rentals Inc.

- United Rentals Inc.

- Modern Hiring Service

- Ashtead Group PLC

- Cummins Inc.

- Aggreko Energy Rental India Private Ltd

第七章 市场机会与未来趋势

The Power Generator Rental Market is expected to register a CAGR of greater than 5.2% during the forecast period.

The market was negatively impacted by COVID-19. Presently, the market has reached pre-pandemic levels.

Key Highlights

- The drivers for the power generator rental market include the cost associated with purchasing new generators and tremendous developments in various sectors, such as oil and gas, construction, etc.

- However, the expansion of power distribution networks and rising development in renewable energy projects are expected to act as a restraint for the market's growth.

- With the rising population, projects from different sectors are expected to increase to meet the requirements, like energy, commercial and residential space, and manufacturing units, for daily needs. For instance, the global population is estimated to reach nearly 8.5 billion by 2030, which may boost global construction spending to USD 17.5 billion. Growth in construction implies a high possibility of an increase in the worldwide power generator rental market.

- North America is a significant region for the power generator rental market. It is estimated that scheduled power shutdowns, new projects installations for various industries, and enplanements, such as natural disasters and seasonal peak power demand, may primarily drive the regional power generator rental market.

Power Generator Rental Market Trends

Power Generators in the Oil and Gas Industry to Witness Significant Growth

- The oil and gas industry has a prominent share in the power generator rental market. With most of the projects located in remote areas, with different anticipated oilfield depths, power generators with high capacity that can work in rigorous environments are required.

- Power generators act as a power supply for both drilling and digging and power backup activities. During drilling and digging, huge power is required to operate the equipment. Power generators act as a power backup to the oil and gas facilities during any emergency or disaster.

- According to IEA, in 2021, oil and gas upstream investment accounted for USD 384 billion. With an annual growth rate of 8.8%, upstream is expected to increase during the forecast period, which, in turn, may drive the power generators market in the oil and gas industry as drilling and digging require a large amount of power.

- Typically, six poles of 1,200 rpm alternators, with two bearings for assembling on an oilfield, are most preferable in the oil and gas industry. The generator's alternator should also withstand voltage dips as large as 25-30% that an electric motor can cause while starting.

- During the forecast period, the oil and gas industry is expected to boost the power generator rental market, as expenditure for exploration and production (E&P) activities is increasing. By 2025, the oil and gas industry is expected to have nearly USD 700 billion in investment, which may drive the power generator rental market.

North America is Expected to Become a Significant Market

- North America's power generator rental market is estimated to grow significantly, with diesel generators being the most dominating segment. However, with tightening environmental policies to reduce carbon footprints, the focus on alternate fuel generators is increasing.

- The oil and gas industry requires a huge amount of power for its upstream and downstream processes. Oil consumption in North America is increasing Y-o-Y, thus creating demand for oil production, which, in turn, is expected to drive the power generator rental market during the forecast period. In 2021, total North American oil consumption accounted for 22,264 thousand barrels daily with an annual growth rate of 7.6%.

- The United States is one of the prominent countries that use natural gas power generators to have a cleaner environment. The country highly relies on natural gas generators due to their less failure during operation. Natural gas generators typically save USD 1,000 per kilowatt to USD 3,000 per kilowatt during operation.

- Growing demand for energy, infrastructure projects, and requirement for contact power are a few primary factors driving the North American power generator rental market. The US oil and gas sector is expected to see an investment of around USD 250 million, which is anticipated to drive the market during the forecast period.

- The region's construction sector is expected to exceed USD 1 trillion in investment during the forecast period. The sector's growth is anticipated to further boost the rental generator market, along with the oil and gas industry.

Power Generator Rental Industry Overview

The power generator rental market is fragmented. Some of the key players in the market (not in a particular order) include Atlas Copco (India) Ltd, Cummins Inc., Ashtead Group PLC, Modern Hiring Service, United Rentals Inc., Herc Rentals Inc., Generac Power Systems, Wacker Neuson Group, and Wartsila Corporation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Power Generator Rental Market in USD million, till 2028

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.2 Restraints

- 4.6 Industry Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By End User

- 5.1.1 Oil and Gas

- 5.1.2 Construction

- 5.1.3 Mining

- 5.1.4 Manufacturing

- 5.1.5 Data Centers

- 5.1.6 Other End Users

- 5.2 By Geography

- 5.2.1 North America

- 5.2.2 Asia-Pacific

- 5.2.3 Europe

- 5.2.4 South America

- 5.2.5 Middle East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Atlas Copco (India) Ltd

- 6.3.2 Wartsila Corporation

- 6.3.3 Wacker Neuson Group

- 6.3.4 Generac Power Systems

- 6.3.5 Herc Rentals Inc.

- 6.3.6 United Rentals Inc.

- 6.3.7 Modern Hiring Service

- 6.3.8 Ashtead Group PLC

- 6.3.9 Cummins Inc.

- 6.3.10 Aggreko Energy Rental India Private Ltd

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

2026-2030年全球电力租赁市场

2026-2030年全球电力租赁市场 发电租赁系统市场规模、份额及成长分析(按电源、燃料、租赁期限、应用、最终用户和地区划分)-2026-2033年产业预测

发电租赁系统市场规模、份额及成长分析(按电源、燃料、租赁期限、应用、最终用户和地区划分)-2026-2033年产业预测 电力租赁市场-全球产业规模、份额、趋势、机会及预测(按燃料类型、功率等级、应用、最终用户产业、地区和竞争格局划分,2020-2030 年预测)

电力租赁市场-全球产业规模、份额、趋势、机会及预测(按燃料类型、功率等级、应用、最终用户产业、地区和竞争格局划分,2020-2030 年预测) 美国电力租赁市场规模、份额和趋势分析报告:按燃料类型、设备和细分市场分類的预测(2025-2033 年)

美国电力租赁市场规模、份额和趋势分析报告:按燃料类型、设备和细分市场分類的预测(2025-2033 年) 发电机租赁市场按燃料类型、输出容量、应用类型、租赁期限、最终用途行业、客户类型和销售管道划分 - 2025-2032 年全球预测按设备类型、最终用户、燃料类型、租赁期限和交付方式分類的电力租赁市场—2025-2032年全球预测

发电机租赁市场按燃料类型、输出容量、应用类型、租赁期限、最终用途行业、客户类型和销售管道划分 - 2025-2032 年全球预测按设备类型、最终用户、燃料类型、租赁期限和交付方式分類的电力租赁市场—2025-2032年全球预测 2025 年至 2033 年电力租赁市场规模、份额、趋势及预测(按燃料类型、设备类型、额定功率、应用、最终用途行业和地区)

2025 年至 2033 年电力租赁市场规模、份额、趋势及预测(按燃料类型、设备类型、额定功率、应用、最终用途行业和地区) 全球行动电源租赁服务市场

全球行动电源租赁服务市场 共享行动电源市场(按容量范围、电池类型和地区划分)

共享行动电源市场(按容量范围、电池类型和地区划分) 电力租赁市场规模、份额及成长分析(按租赁类型、额定功率、燃料类型、设备、最终用户、应用和地区)-2025-2032 年产业预测

电力租赁市场规模、份额及成长分析(按租赁类型、额定功率、燃料类型、设备、最终用户、应用和地区)-2025-2032 年产业预测