|

市场调查报告书

商品编码

1643014

资料转换器 -市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Data Converter - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

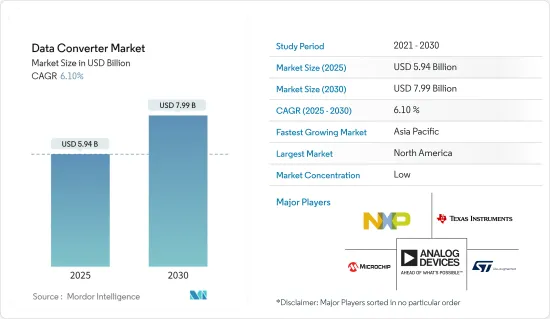

资料转换器市场规模预计在 2025 年为 59.4 亿美元,预计到 2030 年将达到 79.9 亿美元,预测期内(2025-2030 年)的复合年增长率为 6.1%。

高效能电子系统正在使用越来越多的高效能资料转换器来改进和塑造其架构并开拓新的应用领域。最先进调变前沿的新电路和系统技术正在推动效能的进步,创造出新一代资料转换器。此外,当前和未来的趋势受到全球经济、技术进步和行销等新旧因素的驱动。

关键亮点

- 技术先进的资料收集系统的采用正在推动市场的发展。多种讯号中编码的高资讯率迫使资料撷取 (DAQ) 系统从实验室任务发展成为现代工程流程。产业正朝着模组化硬体与灵活软体结合的趋势发展,这些新的模组化系统具有适当的讯号调节和类比数位转换(ADC),可以与各种感测器接口,支援多种资料收集要求。

- 考虑到当今的要求,执行某些 DAQ 任务的传统方法根本不可行。因此,市场趋向于采用软体定义的 DAQ 方法,并出现支援高速 USB 的 DAQ。

- 此外,科学和医学应用对高解析度影像的需求不断增长,推动了市场研究。资料转换器代表了医学影像在所需的动态范围、解析度、准确性、线性度和杂讯方面提出的最具挑战性的电子设计挑战。 ADC(类比数位转换)需要具有至少 24 位元的高解析度才能获得更好的影像清晰度,并且需要快速的取样率才能将检测器读数数位化,在 CT(电脑断层扫描)解决方案中,该取样率可以短至 100 μs。 ADC 取样率还必须允许多路復用,这样就可以使用更少的转换器并减少整体系统尺寸和功率。

- 像 ADI 公司这样的公司提供关键讯号链功能块的高度整合的解决方案来满足这些要求并实现一流的临床成像设备。该公司的ADAS1256(用于X光应用)、ADAS1135和ADAS1134(用于CT应用)等产品引领医疗应用市场。

- 此外,低功耗资料转换器的开发对于市场成长来说是一个挑战。功耗是当今积体电路的主要设计限制之一。低频生物电讯号的转换不需要很高的速度,但需要超低功耗操作。这一点,加上所需的转换精度,使得这种 ADC 的设计成为一项巨大的挑战。

- 此外,新冠疫情对半导体产业的国际供需产生了重大影响。开发资料转换器需要 IC、电阻器、电容器等。分销管道的中断正在减缓资料感测器市场的成长。然而,许多中央和地方政府认识到半导体产业的战略重要性,并在强制关闭企业的情况下优先考虑国内公司和供应商的不间断营运。

资料转换器市场趋势

通讯占很大市场占有率

- 随着4G和通讯的出现,通讯基础设施正在刺激市场成长。无线基础设施製造商,尤其是 4G 和 5G 製造商,正在不断缩小新无线基础设施安装的规模和成本,同时保持高标准的性能、功能和服务品质。资料转换模组是无线基础架构设计中的关键功能。类比数位转换器 (ADC) 是将输入的中频 (IF) 讯号数位化并将数位资料传递到数位下变频器的基本模组。

- 透过将频率转换和滤波从类比域转移到数位域,可以满足 5G 解决方案的高频宽要求。两款 RF 转换器,即 AD9081/AD9082 混合讯号 RF 转换器,就是 ADI 公司推出的这数位化浪潮的一部分。这些射频转换器旨在允许多频段无线电安装在与单频段无线电相同的空间内,有助于将通话容量提高到目前 4G LTE基地台的三倍。

- 此外,为了使 5G 解决方案支援小型天线的部署,无线电架构核心必须紧密整合。一种解决方案是采用传统方法,将多千兆取样 ADC 和 DAC 与系统晶片(SoC) 结合。这种方法证明了嵌入式系统设计能够满足日益增长的操作频宽需求。有些资料转换器使用 JESD204B 实作介面。

- 此外,在过去十年中,Xilinx 等 FPGA 製造商透过缩小硅製造结构的尺寸改进了其技术,从而降低了其设备的尺寸、重量和功率 (SWaP) 值。 Xilinx 最新的系统晶片单晶片(SoC) 装置 RFSoC 在同一晶片上整合了 FPGA 结构、ARM 处理器、类比数位转换器 (ADC) 和数位类比转换器 (DAC)。

- 16nm 技术的特点是每个设备有 4.2K DSP 切片、四个 1.5GHz A53 Arm 处理器、两个 600MHz R5 ARM 处理器、八个 4GHz、12 位元 ADC 和八个 6.4GHz、14 位元 DAC。商用现货 (COTS) 製造商可以使用这项突破性技术,为开发 5G 无线产品的工程师提供多通道 SDR 收发器。

北美占有最大市场占有率

- 由于通讯领域的成长和 FPGA(现场可程式闸阵列)的使用,北美贡献了最高的份额。在家用电子电器中,对于获取高解析度影像的 A2D 转换器的需求不断增加是推动市场发展的关键因素。

- 此外,需要资料转换器的汽车感测器应用范围包括识别不同引擎状况的温度感测器以及支援汽车驾驶辅助系统 (ADAS) 的雷达/雷射雷达。其他资料转换器应用包括用于与其他车辆或固定网路通讯的无线收发器。每辆车 7,500 美元的税额扣抵(该政策推动了美国电动车的销售)即将取消,但奖励上限不会提高。

- 关税风险也迫使外国公司到北美购物。福斯汽车宣布将投资 8 亿美元在田纳西州查塔努加建造一座製造工厂。此外,丰田和马自达将在阿拉巴马州亨茨维尔联合建造一家组装厂。该工厂投资约16亿美元,年产能30万辆。预计此类案例将推动该地区汽车领域资料转换器市场的成长。

- 此外,预计 IT 和通讯应用占据美国资料转换器市场的最大份额。这一成长是由 4G 网路的发展所推动的,4G 网路采用更好的调变和天线格式来改善语音和资讯服务,从而增加了对 AMS 模组的需求。

- 此外,根据 GSMA 的数据,未来三年美国行动连线的 5G 普及率预计将分别成长 33%、40% 和 46%。这将进一步推动5G资料转换器应用的成长。

资料转换器行业概况

由于全球参与企业将讯号整合到家用电子电器和汽车等各种应用中,资料转换器市场呈现细分化,导致竞争对手之间的竞争异常激烈。主要企业包括 Analog Devices Inc. 和 Microchip Technology Inc.。

- 2022 年 5 月:Analog Devices Inc. 推出了新一代 16 至 24 位元超精度 SAR ADC 产品组合,简化了仪器、工业和医疗领域复杂的 ADC 设计流程。 ADI 的取得专利的Easy Drive 技术和自适应 Flexi-SPI 序列週边介面 (SPI) 是新型高效能 SAR ADC 系列的两个方面,可解决系统设计难题并扩大直接相容伴同性产品的范围。

- 2022 年 9 月:MaxLinear Inc. 和 RFHIC 宣布合作开发用于 5G大型基地台无线电的可投入生产的 400 MHz 功率放大器 (PA) 解决方案。此解决方案采用MaxLinear MaxLIN数位预失真(DPD)和波峰因子降低(CFR)技术来增强RFHIC最新ID-400W系列GaN RF电晶体的效能。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 市场定义和范围

- 调查前提

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概况

- 产业相关人员分析

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场动态

- 市场驱动因素

- 越来越多地采用技术先进的资料收集系统

- 科学和医学应用对高解析度影像的需求日益增加

- 市场问题

- 开发低功耗资料转换器的挑战

- 新冠疫情对全球半导体供应链分布的影响

第六章 重大技术投入

- 云端技术

- 人工智慧

- 网路安全

- 数位服务

第七章 市场区隔

- 按类型

- 类比数位转换器

- 数位类比转换器

- 按最终用户

- 车

- 通讯

- 家用电子电器

- 工业的

- 医疗

- 其他的

- 地区

- 北美洲

- 美国

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 欧洲其他地区

- 亚太地区

- 印度

- 中国

- 日本

- 其他亚太地区

- 其他的

- 北美洲

第八章 竞争格局

- 公司简介

- Analog Devices Inc.

- Microchip Technology Inc.

- STMicroelectronics NV

- NXP Semiconductors NV

- Texas Instruments Incorporated

- Mouser Electronics Inc.

- DATEL Inc.

- Synopsys Inc.

- Cirrus Logic Inc.

- Maxim Integrated Products Inc.

第九章投资分析

第十章 市场机会与未来趋势

The Data Converter Market size is estimated at USD 5.94 billion in 2025, and is expected to reach USD 7.99 billion by 2030, at a CAGR of 6.1% during the forecast period (2025-2030).

High-performance electronic systems use more and more high-performance data converters to improve and shape the architecture and open new application perspectives. The emerging circuits and systems techniques at the forefront of state-of-the-art modulators are pushing their performance forward and giving rise to new generations of data converters. Further, the current and future trend depends on old and new factors, including the global economy, technological evolution, and marketing.

Key Highlights

- Increasing adoption of technologically advanced data acquisition systems drives the market. The high rates of encoded information in multiple signals forced data acquisition (DAQ) systems to evolve from research work to modern engineering processes. The industry is evolving toward a trend of having a combination of modular hardware and flexible software, where these newer modular systems have appropriate signal conditioning and analog-to-digital conversion (ADC), with various interfacing sensors that support multiple data acquisition requirements.

- The traditional approach for performing specific DAQ tasks is not feasible, considering today's requirements. Thus, a market tends toward a more software-defined approach to DAQ and the emergence of high-speed USB-enabled DAQs.

- Furthermore, the growing demand for high-resolution images in scientific and medical applications is driving the market studied. Data converters constitute the most demanding challenge medical imaging imposes on the electronics design in terms of required dynamic range, resolution, accuracy, linearity, and noise. The ADC (analog to digital) must have a high resolution of at least 24 bits to achieve better and sharper images and a fast sampling rate to digitize detector readings that can be as short as 100 µs in a CT (computed tomography) solution. The ADC sampling rate must also enable multiplexing, which would allow the use of fewer converters as well as the reduction of the size and power of the entire system.

- A company such as Analog Devices addresses these requirements and offer highly integrated solutions for the key signal chain functional blocks to enable best-in-class clinical imaging equipment. Its products, such as ADAS1256 (X-ray applications), ADAS1135, ADAS1134 (CT applications), and many more, drive the market in medical applications.

- Further, the development of low-power consumption data converters challenges the market's growth. Power consumption is one of the leading design constraints in today's integrated circuits. Conversion of the low-frequency bioelectric signals does not require high speed but requires an ultra-low-power operation. This, combined with the required conversion accuracy, makes designing such ADCs a major challenge.

- Further, due to the impact of the COVID-19 pandemic, there is a high effect internationally on supply-demand in the semiconductor industry. For the development of data converters, there is a need for ICs, resistors, capacitors, etc. The breakage in the distribution channel holds slow growth for the data converter market. However, many central and local governments have recognized the strategic importance of the semiconductor industry and prioritized uninterrupted operations for their domestic companies and suppliers in the midst of mandated business closures.

Data Converter Market Trends

Telecommunication to Account for Significant Market Share

- Telecommunication infrastructure is stimulating market growth owing to the advent of 4G communication and the emerging 5G communication. Manufacturers of wireless infrastructure, especially 4G and 5G, are constantly reducing the size and cost of newly installed wireless infrastructure while holding to high standards of performance, functionality, and quality of service. The data conversion block is a critical function in wireless infrastructure designs. The analog-to-digital converter (ADC) is the fundamental block that digitizes the incoming intermediate frequency (IF) signal and then passes the digital data to the digital downconverter.

- The wide bandwidth demands of the 5G solution can be met by moving frequency translation and filtering from the analog to the digital domain. Two RF converters are part of this digitization wave: the AD9081/AD9082 mixed-signal RF converters, which analog devices introduce. They have been engineered to install multi-band radios in the same footprint as single-band ones, which helps to increase call capacity three-fold, compared to the call capacity available in today's 4G LTE base stations.

- Further, the radio architecture core must be tightly integrated for a 5G solution to support small antenna deployments. One solution is the traditional approach combining multi-Giga sample ADCs and DACs with a System-on-Chip (SoC). This approach provides the ability to perform the embedded system design and to address the increased required operating bandwidths. Several data converters implement interfaces using JESD204B.

- Also, over the past ten years, FPGA manufacturers like Xilinx have been improving technology by reducing the silicon fabrication structure size and, as a result, the device's size, weight, and power (SWaP) values. The latest system-on-chip (SoC) device from Xilinx, the RFSoC, consists of FPGA fabric with arm processors, analog-to-digital converters (ADCs), and digital-to-analog converters (DACs) all on the same chip.

- This 16-nm technology has over 4.2K DSP slices, four 1.5-GHz A53 Arm processors, two 600-MHz R5 ARM processors, eight 4-GHz, 12-bit ADCs, and eight 6.4-GHz, 14-bit DACs per device. COTS (Commercial-off-the-shelf) manufacturers can use this game-changing technology to provide multichannel, SDR transceivers for engineers developing 5G radio products.

North America to Hold the Largest Market Share

- North America holds the highest share due to the growth in the telecom sectors and the use of FPGA (field-programmable gate array). The rising demand for A2D converters in consumer electronics for high-resolution images has become an essential part of driving the market.

- Further, sensor applications in automotive that require data converters range from temperature sensors identifying different engine statuses to radar/LIDAR enabling automotive driver assistance systems (ADAS). Other data converters applications include wireless transceivers for communicating with other vehicles or fixed networks. The USD 7,500 per vehicle tax credit that has boosted EV sales in the United States is drafted to be repealed without any increment in the upper limit of the incentive.

- Also, tariff risk is compelling foreign companies to shop in North America. Volkswagen announced spending USD 800 million to build a manufacturing facility in Chattanooga, Tennessee. Further, Toyota and Mazda are joining forces to construct an assembly plant in Huntsville, Alabama. The factory, which costs about USD 1.6 billion, would have a production capacity of 300,000 units per year. These instances are expected to increase the data converter market's growth in the region's automotive segments.

- Further, IT and telecommunications applications were estimated to have the largest share of the data converter market in the United States. The growth is driven by the development of the 4G network, with superior modulation and antenna methods for improved voice and data services, which enhances the demand for the AMS blocks.

- Further, according to GSMA, in the United States, the 5G adoption rate as a share of mobile connections is expected to increase by 33%, 40%, and 46% in the coming three years, respectively. This further enhances the growth of applications in 5G for data converters.

Data Converter Industry Overview

The data converter market is fragmented as the global players integrate signals in various applications like consumer electronics and automotive, which gives an intense rivalry among the competitors. Key players are Analog Devices, Inc., Microchip Technology Inc., etc.

- May 2022: Analog Devices Inc. introduced a new portfolio of next-generation 16- to 24-bit, ultrahigh-precision SAR ADCs to simplify the complicated process of designing ADCs for instrumentation, industrial, and healthcare applications. The patented Easy Drive technology and the adaptable Flexi-SPI serial peripheral interface (SPI) of ADI are two aspects of the new high-performance SAR ADC series that address system design issues and increase the range of directly compatible companion products.

- September 2022: MaxLinear Inc. and RFHIC announced a collaboration to develop a 400MHz Power Amplifier (PA) solution for 5G Macrocell Radios that is production-ready. This solution will use MaxLinear MaxLIN Digital Predistortion (DPD) and Crest Factor Reduction (CFR) technologies to enhance the performance of RFHIC's newest ID-400W series GaN RF Transistors.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Market Definition and Scope

- 1.2 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Stakeholder Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Adoption of Technologically Advanced Data Acquisition Systems

- 5.1.2 Growing Demand for High-Resolution Images in Scientific and Medical Applications

- 5.2 Market Challenges

- 5.2.1 Challenges in the Development of Low-power Consumption Data Converters

- 5.3 Impact of the COVID-19 Pandemic in Supply Chain Distribution of Semiconductors Globally

6 KEY TECHNOLOGY INVESTMENTS

- 6.1 Cloud Technology

- 6.2 Artificial Intelligence

- 6.3 Cyber Security

- 6.4 Digital Services

7 MARKET SEGMENTATION

- 7.1 By Type

- 7.1.1 Analog to Digital Converter

- 7.1.2 Digital to Analog Converter

- 7.2 By End User

- 7.2.1 Automotive

- 7.2.2 Telecommunication

- 7.2.3 Consumer Electronics

- 7.2.4 Industrial

- 7.2.5 Medical

- 7.2.6 Other End Users

- 7.3 Geography

- 7.3.1 North America

- 7.3.1.1 United States

- 7.3.1.2 Canada

- 7.3.2 Europe

- 7.3.2.1 Germany

- 7.3.2.2 United Kingdom

- 7.3.2.3 France

- 7.3.2.4 Italy

- 7.3.2.5 Rest of Europe

- 7.3.3 Asia-Pacific

- 7.3.3.1 India

- 7.3.3.2 China

- 7.3.3.3 Japan

- 7.3.3.4 Rest of Asia-Pacific

- 7.3.4 Rest of the World

- 7.3.1 North America

8 COMPETITIVE LANDSCAPE

- 8.1 Company Profiles

- 8.1.1 Analog Devices Inc.

- 8.1.2 Microchip Technology Inc.

- 8.1.3 STMicroelectronics NV

- 8.1.4 NXP Semiconductors NV

- 8.1.5 Texas Instruments Incorporated

- 8.1.6 Mouser Electronics Inc.

- 8.1.7 DATEL Inc.

- 8.1.8 Synopsys Inc.

- 8.1.9 Cirrus Logic Inc.

- 8.1.10 Maxim Integrated Products Inc.

9 INVESTMENT ANALYSIS

10 MARKET OPPORTUNITIES AND FUTURE TRENDS

资料转换器市场分析及预测(至2035年):按类型、产品类型、服务、技术、组件、应用、最终用户、功能、安装类型、设备划分

资料转换器市场分析及预测(至2035年):按类型、产品类型、服务、技术、组件、应用、最终用户、功能、安装类型、设备划分 全球数据转换器市场规模、份额、趋势和成长分析报告(2026-2034)

全球数据转换器市场规模、份额、趋势和成长分析报告(2026-2034) 高速资料转换器市场 - 全球产业规模、份额、趋势、机会及预测(按产品类型、技术、资料速率、最终用户产业、地区和竞争格局划分,2021-2031年)

高速资料转换器市场 - 全球产业规模、份额、趋势、机会及预测(按产品类型、技术、资料速率、最终用户产业、地区和竞争格局划分,2021-2031年) 全球数据转换器市场,2026-2030年

全球数据转换器市场,2026-2030年 全球直接空气控制(DAC)及建筑、工程及施工(AEC)市场展望、详细分析及至2031年的预测

全球直接空气控制(DAC)及建筑、工程及施工(AEC)市场展望、详细分析及至2031年的预测 资料转换器市场规模、份额和成长分析(按类型、采样率、应用和地区划分)-2026-2033年产业预测

资料转换器市场规模、份额和成长分析(按类型、采样率、应用和地区划分)-2026-2033年产业预测 按类型、解析度、通道数和应用分類的类比数位转换器市场 - 全球预测 2025-2032资料转换器市场按设备类型、作业系统、最终用户和分销管道划分-2025-2032 年全球预测

按类型、解析度、通道数和应用分類的类比数位转换器市场 - 全球预测 2025-2032资料转换器市场按设备类型、作业系统、最终用户和分销管道划分-2025-2032 年全球预测 2032 年数位音讯转换器市场预测:按类型、解析度、输出、技术、应用、最终用户和地区进行的全球分析电阻数位转换器市场(按产品类型、解析度、介面类型、应用和分销管道)-全球预测,2025-2030

2032 年数位音讯转换器市场预测:按类型、解析度、输出、技术、应用、最终用户和地区进行的全球分析电阻数位转换器市场(按产品类型、解析度、介面类型、应用和分销管道)-全球预测,2025-2030