|

市场调查报告书

商品编码

1643038

微型逆变器:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Micro Inverter - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

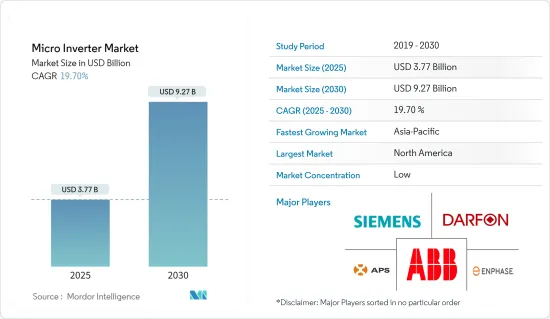

微型逆变器市场规模在 2025 年预计为 37.7 亿美元,预计到 2030 年将达到 92.7 亿美元,预测期内(2025-2030 年)的复合年增长率为 19.7%。

与传统逆变器相比,监控模组层级的能力、安装的简易性、增强的设计灵活性、消除直流开关点和更高的安全性正在推动微型逆变器市场的成长。

主要亮点

- 微型逆变器的持续研发活动和成本的大幅降低正在推动微型逆变器市场的发展。此外,其紧凑的尺寸和多功能性也为其在市场上提供了巨大的推动力。此外,基于模组化、安全性和最大能量产出的消费者需求不断增长,可能会在预测期内推动市场大幅成长。

- 对超紧凑型逆变器的需求使得该公司能够开发额外的电池储存装置。 2022 年 4 月,能源储存提供商 Yotta Energy(德克萨斯州)宣布已赢得一份价值 197 万美元的合同,在拉斯维加斯内利斯空军基地安装太阳能加储能微电网。

- 微型逆变器由于其应用范围广泛而在世界各地广泛采用。其优点包括设计灵活性和透过最大功率点追踪 (MPPT) 技术从太阳能电池板产生最大功率的能力。这些因素使得微型逆变器市场在住宅和商业应用中比其他逆变器更具优势。

- 对微型逆变器的需求使得该公司能够开发额外的电池储存系统。 2022 年 4 月,位于德克萨斯州奥斯汀的 Yotta Energy 获得了一份价值 197 万美元的合同,将在拉斯维加斯内利斯空军基地安装太阳能加储能微电网。该公司相信电池产业正朝着同一方向发展。模组级微储存。该公司在安定器的相同太阳能模组支架中部署了重达 52 磅、1 千瓦时的磷酸锂铁锂电池。

- 根据政府间组织国际能源总署预测,全球可再生能源发电量将比2020年增加60%以上,到2026年达到4,800多万千瓦,相当于全球石化燃料和核能量的总和。

微型逆变器市场趋势

住宅领域推动市场成长

- 美国、加拿大和其他地区的住宅领域越来越多地采用太阳能,这主要是为了节省电费、需要替代电力源以及减轻气候变迁的风险。这推动了微型逆变器市场的成长机会。

- 由于太阳能成本下降、政府对住宅太阳能的支持政策、FIT 计划和奖励以及各国政府设定的太阳能目标成为推动微型逆变器市场发展的关键因素,因此预测期内屋顶太阳能的份额预计会增加。

- 全球微型逆变器业务大部分提供单相设备。此外,由于单相电力传输非常适合住宅应用,因此全球需求量很大,这也使其成为微型逆变器的主要市场之一。例如,在美国和欧洲,住宅领域依赖单相输电。

- 不断的技术改进,例如提高太阳能发电模组的效率,有助于降低成本。这种高度模组化技术的工业化带来了令人瞩目的优势,从规模经济和竞争加剧到改进的製造流程和供应链,进一步加速了微型逆变器市场的成长。

亚太地区市场成长最高

- 预计预测期内亚太地区将成为微型逆变器成长最快的市场。包括中国、日本、印度和澳洲在内的许多国家都在努力透过先进的太阳能光电系统来提高太阳能发电装置容量,从而提高电力安全。

- 亚太地区已在住宅、商业和太阳能发电厂安装了多台微型逆变器。日本和澳洲是微型逆变器技术的领先采用者。此外,随着製造商寻求满足印度和日本潜在客户的需求,住宅屋顶太阳能装置正在增加。

- 在印度、中国和日本等国家,政府正在製定法规、改革和倡议来实现电力部门的现代化。

- 在印度,住宅太阳能安装成本估计为每千瓦 1,000 美元,而商业太阳能安装成本为每千瓦 692 美元。然而,印度的安装成本低于全球平均水平,无论是住宅(每千瓦 1,638 美元)还是商业安装成本(每千瓦 1,379 美元)。这些因素正在推动该地区的市场成长。

- 印度也计划在2021年对进口太阳能电池和逆变器征收20%的课税,取代目前的保障税。这项课税是由印度电力部长在与行业代表的电话交谈中提案的,总理在电话中确认了他打算对进口产品征收 20% 的基本关税 (BCD)。

微型逆变器产业概况

微型逆变器市场高度分散,主要参与者包括 Enphase Energy Inc.、Altenergy Power Systems Inc.、DARFON、ABB Ltd 和西门子股份公司。这些市场参与者正在采用新产品发布、业务扩展、合作和收购等策略来扩大其在该市场的影响力。

- 2022 年 4 月-Yotta Energy 宣布已筹集 350 万美元新资本,使其 A 轮资金筹措总额达到 1,650 万美元。此轮资金筹措及奖励使 Yotta 的总资金筹措达到 2,550 万美元以上。

- 2021 年 10 月-Enphase Energy, Inc. 是一家基于微型逆变器的太阳能和电池系统的全球製造商,它为北美客户推出了采用 IQ8TM 太阳能微型逆变器的 Enphase 能源系统。 IQ8 是 Enphase 最先进的微型逆变器。与其他产品不同的是,IQ8 可以利用太阳能创建微电网,并在停电期间提供备用能源,而无需使用电池。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场动态

- 市场概况

- 市场驱动因素

- 提高对可再生能源的认识和采用

- 这些产品的成本效益和发展

- 市场限制

- 安装和维护成本高

- 产业价值链分析

- 产业吸引力-波特五力分析

- 新进入者的威胁

- 买家的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争强度

- COVID-19 对微型逆变器市场的影响评估

第五章 市场区隔

- 按类型

- 单相

- 三相

- 透过通讯技术

- 有线

- 无线的

- 按销售管道

- 直接的

- 间接销售

- 按应用

- 住宅

- 商业的

- 太阳能发电厂

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 世界其他地区

第六章 竞争格局

- 公司简介

- Enphase Energy Inc.

- Altenergy Power System Inc.

- DARFON

- ABB Ltd

- Siemens AG

- Zhejiang Envertech Corporation Limited

- Omnik New Energy

- Sunpower Corporation

- ReneSolaPower

- AEconversion GmbH & Co. KG

- SMA Solar Technology AG

- Sparq Systems

- Sensata Technologies Inc.

- EnluxSolar Co. Ltd

- Delta Energy Systems

- SolarEdge Technologies Inc.

第七章投资分析

第八章 市场机会与未来趋势

The Micro Inverter Market size is estimated at USD 3.77 billion in 2025, and is expected to reach USD 9.27 billion by 2030, at a CAGR of 19.7% during the forecast period (2025-2030).

The factors like enabling module-level monitoring, easier installation, enhanced design flexibility, removing the need for DC switching points, and better safety than conventional inverters are some factors that are fueling the growth of the micro inverter market.

Key Highlights

- Constant R&D activities and significant reductions in the costs of microinverters drive the micro inverter market. Furthermore, the market also receives a considerable boost due to its compact size and versatility. Additionally, the increasing requirement of consumers, based on modularity, safety, and maximum energy harvest, will continue to drive the market at a considerable pace in the forecast period.

- The demand for micro inverters has enabled companies to develop increased battery storage. In April 2022, energy storage provider Yotta Energy, Austin, Texas, announced that it had been awarded a USD 1.97 million contract to install a solar + storage microgrid at Nellis Air Force Base in Las Vegas.

- Due to the varying use of micro inverters, they are widely adopted worldwide. They provide various benefits such as design flexibility and capabilities like producing the maximum power from solar panels through maximum power point tracking (MPPT) technology. These factors have helped the micro-inverter market gain an advantage over other inverters in residential and commercial applications.

- The demand for micro inverters has enabled companies to develop increased battery storage. In April 2022, Yotta Energy of Austin, Texas, was awarded a USD 1.97 million contract to install a solar + storage microgrid at Nellis Air Force Base in Las Vegas. The company believes batteries are headed in the same direction: module-level microstorage. The business is deploying a 52lb, 1kWh lithium-iron-phosphate battery on the same solar module racking gear, which holds the ballast.

- Worldwide renewable electricity capacity is predicted to expand by more than 60% from 2020 to over 4,800 (GW) by 2026, equaling the total global power capacity of fossil fuels and nuclear power combined, according to the International Energy Agency (an intergovernmental agency).

Micro Inverter Market Trends

Residential Segment to Drive the Market Growth

- The increasing adoption of solar photovoltaics in the residential sector in countries such as the United States and Canada is primarily driven by expected savings in electricity costs, the need for an alternative source of electricity, and the desire to mitigate climate change risk. Therefore, boosting the growth opportunities for the micro inverter market.

- During the forecast period, the share of the rooftop solar PV is expected to increase, on account of decreasing solar PV costs, supportive government policies for residential solar PV, FIT programs and incentives, and targets set by various governments for solar energy are some of the critical factors that are driving the micro inverter market.

- The majority of micro-inverter businesses throughout the world provide single-phase devices. Furthermore, considerable demand is observed globally because single-phase power transmission is best adapted for domestic applications, which is likewise among the primary marketplaces for micro-inverters. For example, the residential sector relies on single-phase power transmission in the United States and Europe.

- Continuous technological improvements, including higher solar PV module efficiencies, drive cost reductions. The industrialization of these highly modular technologies has yielded impressive benefits, from economies of scale and greater competition to improved manufacturing processes and supply chains, further accelerating the micro-inverter market growth.

Asia-Pacific to Register Highest Market Growth

- Asia-Pacific is expected to be the fastest-growing market for micro-inverters over the study period. Several countries, such as China, Japan, India, and Australia, are striving to boost their solar PV installation capacity through advanced solar PV systems that could, in turn, enhance electric stability.

- Asia-Pacific has several micro-inverter installations for residential, commercial, and PV power plant applications. Japan and Australia have been the major adopters of micro-inverter technology. Additionally, the growth in residential rooftop solar PV installations in India and Japan encourages manufacturers to cater to the needs of potential customers in this region.

- In countries such as India, China, and Japan, respective governments have laid regulations, reforms, and initiatives for modernizing the power sector.

- In India, the residential PV installation cost is estimated to be USD 1000 per KW, which is higher when compared to its commercial counterpart (USD 692 per KW). However, the Indian installation costs are cheaper than the global average for both residential (USD 1638 per KW) and commercial (USD 1379 per KW). These factors fuel the market growth in the region.

- India is also set to impose a 20% levy on imported solar module cells and inverters in 2021, replacing the current safeguard duty. The levy was proposed by the Indian power minister during a call with industry representatives, confirming that the Prime Minister of India intended to impose a Basic Custom Duty (BCD) of 20% on imports.

Micro Inverter Industry Overview

The micro-inverter market is highly fragmented, and the major players such as Enphase Energy Inc., Altenergy Power System Inc., DARFON, ABB Ltd, and Siemens AG, among others. These market players are using strategies such as new product launches, expansions, partnerships, acquisitions, and others to increase their footprints in this market.

- April 2022 - Yotta Energy announced obtaining USD 3.5 million in new capital, bringing its total Series A funding to USD 16.5 Million. Yotta's total funding is now over USD 25.5 million due to the current funding round and award.

- October 2021 - Enphase Energy, Inc., the world's premier microinverter-based solar and battery system manufacturer, unveiled the Enphase Energy System with IQ8TM solar microinverters for clients in North America. IQ8 is Enphase's most advanced microinverter to date. Unlike rival gadgets, IQ8 can build a microgrid using sunlight throughout a power outage, delivering backup energy without a battery.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definitions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rise in benefits and awareness about the renewable energy sources along with increased adoption

- 4.2.2 Cost-effectiveness and increased developments of these products

- 4.3 Market Restraints

- 4.3.1 High installation and maintenance costs

- 4.4 Industry Value Chain Analysis

- 4.5 Industry Attractiveness - Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 Assessment of Impact of Covid-19 on the Micro Inverter Market

5 MARKET SEGMENTATION

- 5.1 By Type

- 5.1.1 Single Phase

- 5.1.2 Three Phase

- 5.2 By Communication Technology

- 5.2.1 Wired

- 5.2.2 Wireless

- 5.3 By Sales Channel

- 5.3.1 Direct

- 5.3.2 Indirect

- 5.4 By Application

- 5.4.1 Residential

- 5.4.2 Commercial

- 5.4.3 PV Power Plant

- 5.5 Geography

- 5.5.1 North America

- 5.5.2 Europe

- 5.5.3 Asia-Pacific

- 5.5.4 Rest of the World

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Enphase Energy Inc.

- 6.1.2 Altenergy Power System Inc.

- 6.1.3 DARFON

- 6.1.4 ABB Ltd

- 6.1.5 Siemens AG

- 6.1.6 Zhejiang Envertech Corporation Limited

- 6.1.7 Omnik New Energy

- 6.1.8 Sunpower Corporation

- 6.1.9 ReneSolaPower

- 6.1.10 AEconversion GmbH & Co. KG

- 6.1.11 SMA Solar Technology AG

- 6.1.12 Sparq Systems

- 6.1.13 Sensata Technologies Inc.

- 6.1.14 EnluxSolar Co. Ltd

- 6.1.15 Delta Energy Systems

- 6.1.16 SolarEdge Technologies Inc.

7 INVESTMENT ANALYSIS

8 MARKET OPPORTUNITIES AND FUTURE TRENDS

全球微型逆变器市场规模、份额、趋势和成长分析报告(2026-2034年)

全球微型逆变器市场规模、份额、趋势和成长分析报告(2026-2034年) 2026年全球微型逆变器市场报告

2026年全球微型逆变器市场报告 微型逆变器市场规模、份额和成长分析:按产品、通讯技术、类型、额定功率、连接类型、销售管道、应用、地区划分 - 产业预测(2026-2033 年)

微型逆变器市场规模、份额和成长分析:按产品、通讯技术、类型、额定功率、连接类型、销售管道、应用、地区划分 - 产业预测(2026-2033 年) 微型逆变器市场按最终用途、产品类型、功率输出、安装类型、组件整合和销售管道划分-2025-2032年全球预测

微型逆变器市场按最终用途、产品类型、功率输出、安装类型、组件整合和销售管道划分-2025-2032年全球预测 全球商用三相微型逆变器市场全球商用单相微型逆变器市场

全球商用三相微型逆变器市场全球商用单相微型逆变器市场 住宅微型逆变器市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

住宅微型逆变器市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测 微型逆变器市场规模、份额、趋势分析报告:按类型、应用、地区、细分市场预测,2025-2030 年

微型逆变器市场规模、份额、趋势分析报告:按类型、应用、地区、细分市场预测,2025-2030 年 到 2030 年微型逆变器市场预测:按类型、额定功率、连接性别、销售管道、技术、应用和地区进行全球分析单相户用微型逆变器市场机会、成长动力、产业趋势分析与 2024 年至 2032 年预测

到 2030 年微型逆变器市场预测:按类型、额定功率、连接性别、销售管道、技术、应用和地区进行全球分析单相户用微型逆变器市场机会、成长动力、产业趋势分析与 2024 年至 2032 年预测