|

市场调查报告书

商品编码

1643129

软体定义边界:全球市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Global Software-Defined Perimeter - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

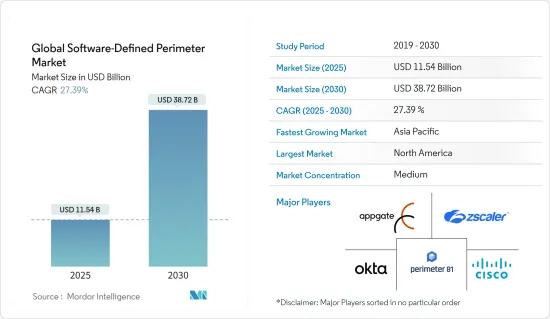

预计 2025 年全球软体定义边界市场规模为 115.4 亿美元,预计到 2030 年将达到 387.2 亿美元,预测期内(2025-2030 年)的复合年增长率为 27.39%。

主要亮点

- 云端服务是数位转型的关键驱动力,正被各行各业广泛采用。这为企业带来了各种安全挑战,也是预测期内推动全球软体定义边界市场成长的关键原因。

- 由于大多数企业处于混合 IT 采用的不同阶段以支援数位业务转型,因此企业在未来一段时间内可能会同时依赖虚拟私人网路 (VPN) 和软体定义的边界技术。许多企业会根据业务需求、部门或地理位置选择采用 SDP 来支援其使用者和应用程式。这增加了管理两个或多个独立安全存取系统的复杂性,从而抵消了 IT 整合带来的好处和经济性。最终,公司应该投资并致力于安全存取。

- 传统的内部部署 VPN 成本昂贵,且难以操作和维护。因此,许多面临维持或过渡到远端劳动力挑战的组织正在考虑其他网路安全选项。例如,有些人强调软体定义边界是 VPN 的可行替代方案。例如,Palo Alto Networks 和 Zscaler 提供的软体定义边界服务可以简化大规模远端访问,儘管这需要一些财务和营运投资。

- 云端服务透过快速的可扩展性和资源利用的灵活性为加速您的业务提供了绝佳的机会。云端处理还能以合理的成本实现无缝扩展,降低营运成本并避免因重大升级而产生的财务支出。

- 此外,越来越多的公司正在采用企业行动解决方案,以便员工可以在任何地方、使用任何设备工作。这实现了工作与生活的平衡,并提高了员工与消费者之间的互动以及业务效率 34%。预计约有 67% 的员工将采用自带设备 (BYOD) 政策来业务,这进一步凸显了行动和远端设备网路安全的必要性。报告称,到2023年,30%的IT组织将扩大其BYOD政策,将员工穿戴装置纳入其中,这将进一步推动市场发展。

- 然而,对软体定义边界解决方案的显着优势缺乏认识以及对免费和开放原始码安全标准日益增长的需求可能会阻碍市场成长。

- 儘管许多组织已将「采用零信任」列入其「待办事项」清单,但 COVID-19 疫情加速了零信任的采用。此外,云端运算的兴起导致软体定义广域网路 (SD-WAN) 的使用增加,呼吁新的趋势来适应未来的安全模型,其中包括检测和阻止漏洞、网路钓鱼、勒索软体和其他现代恶意软体的方法。

软体定义边界市场趋势

BFSI 产业将大幅成长

- 数位化在各领域的广泛应用也延伸到了金融领域。大多数银行正在将资料、流程和基础设施转移到混合云,希望获得内部和外部部署云端实施带来的好处。

- 电子设备的快速普及和互联网的高普及率推动了数位服务的成长,并提高了客户对便利付款、全天候执行时间、安全储存和互通性的期望。云端处理创造了以显着降低的成本维持与客户多通路关係的机会。云端处理也缩短了新产品的开发週期,帮助企业更快、更有效地回应客户需求。

- 此外,一些专注于金融的科技新兴企业也纷纷涌现,并且正在颠覆我们的购买方式。例如,在印度,从基于应用程式的钱包和 Aadhaar/UPI 连结的即时交易到单视窗电子商务应用程序,金融科技新兴企业需要注意威胁并为其应用程式投资强大的资料安全框架。这些案例需要软体定义的边界解决方案来控制银行、金融服务和保险 (BFSI) 行业的网路威胁。

- 许多金融机构正在与政府机构合作,提高网路安全意识并保护敏感资料。例如,2022年2月,菲律宾司法部(DoJ)与产业组织菲律宾银行家协会(BAP)签署了一份谅解备忘录(MoU),以提升菲律宾的网路安全意识并打击网路犯罪。此外,金融机构意识的提高可能会推动软体定义的边界解决方案的采用。

北美占据主要市场占有率

- 医疗保健产业正在经历转型,新的工具和技术正在重塑医疗服务的提供方式,以提高效率并为患者照护。行动健康应用程式和穿戴式技术正在被用作监测患者活动的实用健康工具。例如,智慧型手机可以用作心电图电极的适配器,来传输资料以检测无症状心房颤动。

- 根据全球行动通讯系统协会(GSMA)预测,到 2025 年,北美的物联网(IoT)连线数量预计将从 2018 年的 23 亿增加到 59 亿。随着物联网设备数量的增加,对支援采用 SDP(软体定义边界)的高阶网路安全解决方案的需求日益增长,尤其是在中大型企业中。

- 2022年4月,美国政府成立网路空间与数位政策局(CDP),以应对网路安全挑战并加强全国的网路安全。此外,政府还将解决与电脑网路空间、数位科技和数位政策相关的国家安全挑战、经济机会以及对美国价值观的影响。此外,中央民主党局还有三个政策部门:国际网路空间安全、国际资讯和通讯政策以及数位自由。预计这些政府措施将在预测期内进一步促进市场成长。

- 此外,零售巨头正在采用混合云解决方案,一些应用程式在自己的资料中心,其他应用程式在公有公共云端,以利用内部和外部部署混合云端实施的好处并提供卓越的购物体验。例如,AmazonGo 商店结合使用电脑视觉、深度学习和感测器融合技术来自动化付款和结帐流程,让顾客无需排队,只需进入、领取商品然后离开即可。同时,付款透过 Amazon Go 应用程式自动完成。因此,零售业正在走向数位化,未来将需要网路安全,为软体定义边界市场铺平了一条充满希望的道路。

- 最近,由于分散式基础设施的 API 和其他服务的使用增加,COVID-19 疫情导致安全软体的需求短期内增加。然而,预计更多企业将采用数位基础设施,这将推动未来几年需求大幅成长。

软体定义边界产业概览

软体定义边界市场集中度较高,主要由 Perimeter 81、ZScaler、思科系统公司 (Cisco Systems, Inc.)、Okta Inc.、APPGate 和 Check Point 等大型公司主导。这些拥有较大市场占有率的大公司正致力于发展海外基本客群。此外,这些公司正在利用策略联盟和伙伴关係关係来扩大市场占有率并提高盈利。然而,中小企业利用技术进步和创新产品,开拓新市场和赢得新契约,扩大了其市场影响力。

2022 年 6 月,江森自控宣布收购 Temper Networks,为互联建筑带来零信任网路安全。 Tempered Networks 使用软体定义的边界实现安全通讯,实现建筑网路的微分段、细粒度的存取控制和身份验证,以强制执行关键资料和服务。 Tempered Networks 开发了「Airwall」技术,这是一种先进的建筑物自防御系统,可实现不同端点设备、边缘网关、云端平台和服务技术人员之间的安全网路存取。

此外,2022 年 4 月,云端安全联盟 (CSA) 宣布了由 SDP 和零信任工作小组创建的软体定义边界 (SDP) 2.0 规范。 SDP 2.0 规范可协助安全和技术组织了解实现 SDP 的核心组件和原则。它也强调了云端原生架构、服务网格实作和零信任更广泛追求等努力之间的协同效应。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概况

- 价值链/供应链分析

- 产业吸引力-波特五力分析

- 新进入者的威胁

- 购买者/消费者的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争强度

- COVID-19 产业影响评估

第五章 市场动态

- 市场概况

- 市场驱动因素

- 持续迁移至云端、采用物联网和 BYOD

- 严格的资料合规性要求和可扩展资料保护策略的需求

- 市场限制

- 对开放原始码安全标准的需求不断增长

第六章 市场细分

- 按类型

- 解决方案

- 服务

- 按部署形式

- 云

- 本地

- 按最终用户产业

- BFSI

- 通讯和 IT

- 卫生保健

- 零售

- 政府

- 其他最终用户产业

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 世界其他地区

第七章 竞争格局

- 公司简介

- Perimeter 81

- ZScaler

- Cisco Systems, Inc

- Okta, Inc

- APPGate

- Check Point

- Broadcom(Symantec)

- Cato Networks Limited

- Unisys Corporation

- Fortinent Corporation

- Palo Alto Networks Inc.

- Safe-T Group Limited

- Akamai Technologies, Inc(Soha Systems)

- Verizon Communications(Vidder)

第八章投资分析

第九章 市场机会与未来趋势

The Global Software-Defined Perimeter Market size is estimated at USD 11.54 billion in 2025, and is expected to reach USD 38.72 billion by 2030, at a CAGR of 27.39% during the forecast period (2025-2030).

Key Highlights

- Cloud services are the primary drivers for digital transformation, with ubiquitous adoption in various industries. It has brought different security challenges for the business, which is the crucial reason for promoting the growth of the global software-defined perimeter market during the projected period.

- As most enterprises are at various stages of their hybrid IT implementation to support their digital business transformation, organizations will likely rely on both virtual private networks (VPN) and software-defined perimeter technology for some time. Many organizations have decided to implement SDP according to a business need, division, or region to support that set of users and applications. This introduces complications in managing two or more separate secure access systems, which contradicts IT consolidation's benefits and economies. Ultimately, organizations should progress their investment and initiatives for highly-secure access.

- Traditional on-premises VPNs can be expensive and difficult to operate and maintain. Thus, many organizations tasked with maintaining or moving to a new remote workforce are considering other network security alternatives. For example, some weigh software-defined perimeter as a vital VPN alternative. For instance, software-defined perimeter services from Palo Alto Networks and Zscaler can simplify remote access at a broad scale, pending some degree of financial and operational investment.

- Cloud services provide significant opportunities to accelerate the business through rapid scalability and the flexibility of resource utilization. It also reduces operational costs and controls financial spending on large-scale upgrades as cloud computing facilitates seamless scaling at reasonable costs.

- In addition, more and more businesses are implementing enterprise mobility solutions that enable and encourage employees to work from anywhere and through a wide range of devices. It has created a work-life balance and increased employee-consumer interaction and operational productivity by 34%. About 67% of the workforce is expected to adopt bring your own devices (BYOD) policy for work; this further emphasizes the need for network security for mobile and remote devices. According to the report, by 2023, 30% of IT organizations will extend their BYOD policy to cater to employees' wearables in the workforce, which will further drive the market.

- However, a lack of awareness of the critical benefits of software-defined perimeter solutions and the rise in demand for free and open-source security standards can hamper the market's growth.

- While many organizations put "deploying zero trust" on their "to-do" list, the COVID-19 pandemic sped up zero-trust adoption. Furthermore, with the rise of the cloud, the increasing use of software-defined wide area networks (SD-WANs) has given a new trend demand as it is a future-proof security model that encompasses the ways to detect and block exploits, phishing, ransomware, and other modern malware.

Software-Defined Perimeter Market Trends

BFSI Sector Will Experience Significant Growth

- Wide-scale adoption of digitalization in every sector has also touched the financial sector. Most banks are migrating their data, process, and infrastructure to hybrid cloud to benefit from both on-premises and off-premise cloud implementation.

- The rapid adoption of electronic devices and high internet penetration fuelled the growth of digital services and increased the customers' expectations for ease of payment, 24x7 uptime, secure storage, and interoperability. It has created an opportunity to maintain a multi-channel relationship with customers at a much-reduced cost. Cloud computing has also shortened the development cycles for new products and supports a faster and more efficient response to customers' needs.

- Further, several technology start-ups specializing in the financial segment have emerged, disrupting how we make purchases. For instance, in India, from app-based wallets and Aadhaar/UPI-linked instant transactions to single-window e-commerce apps, fintech start-ups need to be mindful of the threats and invest in robust data security frameworks for the apps. Such instances demand software-defined perimeter solutions to control cyber threats in the banking, financial services, and insurance (BFSI) industry.

- Many financial institutions collaborate with government organizations to advance cyber security awareness and protect sensitive data. For instance, in February 2022, the Department of Justice (DoJ) and the industry group Bankers Association of the Philippines (BAP) signed a memorandum of understanding (MoU) to raise cybersecurity awareness and combat cybercrime in the Philippines. In addition, the increased awareness among financial organizations would prompt deploying software-defined perimeter solutions.

North America to Hold a Significant Market Share

- The healthcare industry is experiencing a transformation with new tools and technologies to reconstruct the delivery of health services to improve efficiency with better patient care. Mobile health applications and wearable technologies are leveraged as practical health tools to monitor patients' activities. For instance, smartphones are used as an adapter with electrocardiogram electrodes to transmit data to detect silent atrial fibrillation.

- According to Groupe Speciale Mobile Association (GSMA), by 2025, the number of Internet of Things (IoT) connections in North America is expected to grow to 5.9 billion from 2.3 billion in 2018. With the rising trend of IoT devices, the demand for high network security solutions is increasing, which caters to adopting the software-defined perimeter (SDP), mostly in medium and large enterprises.

- In April 2022, the US government launched the Bureau of Cyberspace and Digital Policy (CDP) to enhance cybersecurity across the nation, aiming to address cybersecurity challenges. In addition, the government would address the national security challenges, economic opportunities, and implications for US values associated with cyberspace, digital technologies, and digital policy. Further, the CDP bureau includes three policy units: International Cyberspace Security, International Information and Communications Policy, and Digital Freedom. Such initiatives taken by the government would further boost the market growth over the forecast period.

- Moreover, major players in the retail sector are embracing hybrid cloud solutions with various applications in their data centers and others in the public cloud to benefit from both on-premise and off-premise cloud implementation and create a great shopping experience. For instance, AmazonGo stores utilize a combination of computer vision, deep learning, and sensor fusion technology to automate the payment and checkout process so that customers can directly enter the store, pick up items and leave without queuing. In contrast, the payment is made automatically through the Amazon Go app. Therefore, the retail sector is shifting to digitalization and requires network security in the future, which paves a promising road for a software-defined perimeter market.

- The recent outbreak of COVID-19 worldwide resulted in a short-term increase in demand for security software owing to the increased usage of API and other services from distributed infrastructure. However, this is expected to influence a significant growth in demand over the next few years as the number of enterprises adopting digital infrastructure is expected to increase.

Software-Defined Perimeter Industry Overview

The software-defined perimeter market is moderately concentrated and dominated by significant players like Perimeter 81, ZScaler, Cisco Systems, Inc, Okta Inc., APPGate, and Check Point. With a significant market share, these major players focus on developing their customer base across foreign countries. In addition, these companies are leveraging strategic collaborations and partnerships to raise their market share and boost their profitability. However, with product innovations using technological advancements, mid-size to smaller firms are growing their market presence by tapping new markets and securing new contracts.

In June 2022, Johnson Controls announced the acquisition of Tempered Networks to bring zero-trust cybersecurity to connected buildings. Tempered Networks use software-defined perimeters to create secure communications enabling micro-segmentation of building networks and granular access control and authentication that fortifies critical data and services. Tempered Networks has created 'Airwall' technology, an advanced self-defense system for buildings that enables secure network access across diverse groups of endpoint devices, edge gateways, cloud platforms, and service technicians.

Moreover, in April 2022, The Cloud Security Alliance (CSA) published the software-defined perimeter (SDP) 2.0 specification created by their SDP and zero-trust working groups. SDP 2.0 specification helps security and technology organizations understand the core components and tenets of implementing an SDP. It also highlights the synergies among efforts such as cloud-native architectures, service-mesh implementations, and the broader pursuit of zero trust.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Value Chain / Supply Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Assessment of Impact of COVID-19 on the Industry

5 MARKET DYNAMICS

- 5.1 Market Overview

- 5.2 Market Drivers

- 5.2.1 Ongoing Migration to The Cloud, Adoption of IoT & BYOD

- 5.2.2 Stringent Data Compliance Requirements and Need for Scalable Data Safeguarding Strategies

- 5.3 Market Restraints

- 5.3.1 Growing Demand for Open-Source Security Standards

6 MARKET SEGMENTATION

- 6.1 Type

- 6.1.1 Solutions

- 6.1.2 Services

- 6.2 Deployment Mode

- 6.2.1 Cloud

- 6.2.2 On-Premise

- 6.3 End-User Verticals

- 6.3.1 BFSI

- 6.3.2 Telecom and IT

- 6.3.3 Healthcare

- 6.3.4 Retail

- 6.3.5 Government

- 6.3.6 Other End-user Verticals

- 6.4 Geography

- 6.4.1 North America

- 6.4.2 Europe

- 6.4.3 Asia-Pacific

- 6.4.4 Rest of the World

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Perimeter 81

- 7.1.2 ZScaler

- 7.1.3 Cisco Systems, Inc

- 7.1.4 Okta, Inc

- 7.1.5 APPGate

- 7.1.6 Check Point

- 7.1.7 Broadcom (Symantec)

- 7.1.8 Cato Networks Limited

- 7.1.9 Unisys Corporation

- 7.1.10 Fortinent Corporation

- 7.1.11 Palo Alto Networks Inc.

- 7.1.12 Safe-T Group Limited

- 7.1.13 Akamai Technologies, Inc (Soha Systems)

- 7.1.14 Verizon Communications (Vidder)

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

全球软体定义周界市场规模、份额、趋势和成长分析报告(2026-2034)

全球软体定义周界市场规模、份额、趋势和成长分析报告(2026-2034) 2026-2030年全球软体定义边界(SDP)市场全球软体定义边界(SDP)市场:市场规模、占有率、成长率、行业分析、依类型、应用和地区划分的分析以及未来预测(2026-2034)

2026-2030年全球软体定义边界(SDP)市场全球软体定义边界(SDP)市场:市场规模、占有率、成长率、行业分析、依类型、应用和地区划分的分析以及未来预测(2026-2034) 软体定义边界 (SDP) 市场规模、份额和成长分析(按组件、连接方式、部署方式、组织规模、最终用户和地区划分):产业预测(2026-2033 年)

软体定义边界 (SDP) 市场规模、份额和成长分析(按组件、连接方式、部署方式、组织规模、最终用户和地区划分):产业预测(2026-2033 年) 软体定义边界市场按组件类型、认证类型、部署模型、垂直行业和组织规模划分 - 全球预测 2025-2032

软体定义边界市场按组件类型、认证类型、部署模型、垂直行业和组织规模划分 - 全球预测 2025-2032 软体定义边界市场规模、份额、趋势分析报告:按执行点、部署、组织规模、应用、地区和细分市场进行预测,2025 年至 2030 年

软体定义边界市场规模、份额、趋势分析报告:按执行点、部署、组织规模、应用、地区和细分市场进行预测,2025 年至 2030 年 软体定义外围市场规模- 按组件(解决方案、服务)、按组织规模(中小企业、大型企业)、按部署模式(云端、本地)、按连接性(控制器、网关、端点)、按最终用途和预测,2024 - 2032

软体定义外围市场规模- 按组件(解决方案、服务)、按组织规模(中小企业、大型企业)、按部署模式(云端、本地)、按连接性(控制器、网关、端点)、按最终用途和预测,2024 - 2032