|

市场调查报告书

商品编码

1643177

欧洲柴油发电机组:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Europe Diesel Generator - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

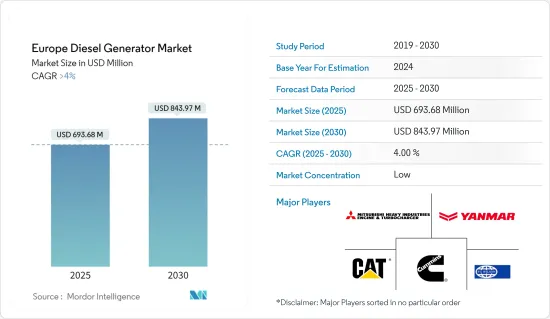

预计 2025 年欧洲柴油发电机市场规模为 6.9368 亿美元,到 2030 年将达到 8.4397 亿美元,预测期内(2025-2030 年)的复合年增长率将超过 4%。

关键亮点

- 从中期来看,备用柴油发电机的需求预计将推动市场发展。这些发电机适用于许多领域,包括工业、建筑、医疗和离网应用。

- 由于可再生能源作为替代电源(无论是在併网还是离网)的使用越来越多,未来几年市场成长可能会放缓。

- 随着向再生能源来源的转变不断进行,欧洲消费者正在寻找高效、环保的选择,例如结合了太阳能等再生能源来源的混合柴油发电机。预计这将在不久的将来为市场参与企业创造巨大的商机。

欧洲柴油发电机市场趋势

工业领域预计将主导市场

- 包括采矿业、製造业、农业和建设业在内的工业领域将在未来几年消耗一半以上的能源。

- 最大的能源使用者是工业部门,包括采矿业、製造业、农业和建设业。这可能会推动对柴油发电机的需求,因为这些产业,尤其是医疗、製药和製造设施,越来越需要运作、可靠的电力。

- 因此,製药和製造设施等行业对持续可靠电力供应的需求不断增加,预计将推动对柴油发电机的需求。在停电期间(以避免停机)以及电网接入有限的地区,工业运作主要依赖柴油发电机产生的电力。

- 截至 2023 年,欧洲是仅次于亚太地区的世界第二大钢铁生产国。根据世界钢铁协会预测,2023年欧盟钢铁产量将达1.263亿吨。钢铁业是电力消耗大户,钢铁生产需要大量可靠的能源。德国等许多国家仍在其钢铁业使用柴油发电机,以支持该国的发展工作。

- 预计未来几年英国和俄罗斯的工业部门都将成长。这是由于这两个国家的製造业蓬勃发展,这可能会刺激工业领域对柴油发电机的需求。

- 此外,预计在预测期内,政府(尤其是英国和土耳其)扩大工业部门的措施将推动对柴油发电机的需求。

英国可望主导市场

- 英国是世界上最发达的国家之一,也是欧洲工业化程度最高的国家之一。随着能源需求的不断成长,经济的各个领域也需要不间断的电力供应。

- 英国电网在尖峰时段需要备用电源。为了满足这一峰值需求,国家电网输电公司(NGET)一直使用柴油发电机(DG)组为变电站的冷却风扇、泵浦和照明等关键活动提供备用电源。

- 英格兰和威尔斯的 250 多个 NGET 站点均使用备用发电机,其中大多数由柴油发电。这些系统为 NGET 在停电时提供恢復能力。

- 生活水准的提高推动了对电力备用设备的需求,国家也从柴油发电机的成本和效益中受益。在英国,发电机广泛用于农业、通讯和建筑等各个领域。

- 近几个月来,该国的建设活动一直在增加。英国政府预计,2023年新建住宅存量订单量将达175.5亿,较2018年持续增加。预计预测期内建设活动的增加将产生对柴油发电机的需求。

- 英国农业规模庞大,农业覆盖了英国国土面积的60%以上。随着国家电网越来越依赖可再生能源,农业产业热衷于开发备用电源系统。对柴油发电系统的依赖日益增加正在推动市场的发展。

- 超过40%的欧洲资料中心位于英国,消耗大量电力。资料中心使用柴油发电机来满足停电期间的电力需求。截至 2023 年,英国共有 513 个资料中心运作。

- 预计未来几年该国将建立更多的资料中心,从而增加对柴油发电机的需求。

欧洲柴油发电机产业概况

欧洲柴油发电机市场适度细分。市场的主要参与企业包括卡特彼勒、三菱重工引擎与涡轮增压器有限公司、FG Wilson Engineering(都柏林)有限公司、康明斯公司和洋马控股。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究范围

- 市场定义

- 调查前提

第二章调查方法

第三章执行摘要

第四章 市场概况

- 介绍

- 2029 年市场规模与需求预测(十亿美元)

- 最新趋势和发展

- 政府法规和政策

- 市场动态

- 驱动程式

- 备用应用中需要柴油发电机

- 在多个终端用户行业中的使用日益广泛

- 限制因素

- 增加使用可再生能源作为替代电力来源

- 驱动程式

- 供应链分析

- 波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争强度

第五章 市场区隔

- 容量

- 75kVA以下

- 75 至 350 kVA 或更低

- 350kVA以上

- 最终用户

- 住宅

- 商业的

- 工业的

- 地区

- 德国

- 俄罗斯

- 英国

- 挪威

- 北欧的

- 法国

- 义大利

- 欧洲其他地区

第六章 竞争格局

- 併购、合资、合作与协议

- 主要企业策略

- 公司简介

- Caterpillar Inc.

- Mitsubishi Heavy Industries Engine & Turbocharger Ltd

- FG Wilson

- Cummins Inc.

- Yanmar Holdings Co. Ltd

- Generac Power Systems

- Kohler Co.

- Doosan Corporation

- 其他知名公司名单

- 市场排名分析

第七章 市场机会与未来趋势

- 混合柴油发电机的需求不断增加

简介目录

Product Code: 70158

The Europe Diesel Generator Market size is estimated at USD 693.68 million in 2025, and is expected to reach USD 843.97 million by 2030, at a CAGR of greater than 4% during the forecast period (2025-2030).

Key Highlights

- In the medium period, the market is expected to be driven by the need for diesel generators in standby applications. These generators are needed in many fields, including industrial, construction, medical, and off-grid applications.

- The growing use of renewables as an alternative power source, both on-grid and off-grid, is likely to slow the market's growth over the next few years.

- Nevertheless, with the increasing shift toward renewable energy sources, European consumers are looking for efficient and environmentally safe options, such as hybrid diesel generators that incorporate renewable sources like solar. This, in turn, is expected to create significant opportunities for the market players in the near future.

Europe Diesel Generator Market Trends

The Industrial Segment is Expected to Dominate the Market

- The industrial segment, which includes mining, manufacturing, agriculture, and construction, uses more than half of the energy that will be used over the next few years.

- The largest amount of energy is used by the industrial sector, which includes mining, manufacturing, agriculture, and construction. Because of this, the demand for diesel generators is likely to go up as these industries, especially healthcare, pharmaceutical, and manufacturing facilities, need more and more power that is always on and reliable.

- Therefore, the increasing demand for continuous and reliable power supply in industries like pharmaceuticals and manufacturing facilities is expected to escalate the demand for diesel generators. Industrial operations mainly depend on electricity generated from diesel generators during power outages (to avoid operation downtime) and in regions with limited grid access.

- As of 2023, Europe was the second-largest producer of steel in the world after Asia-Pacific. According to the World Steel Association, in 2023, the European Union produced 126.3 million tonnes of steel. The steel industry is a major consumer of power and requires a large amount of reliable energy for steel manufacturing. Many countries like Germany still use diesel generators for the steel industry, which are the backbone of the country's development work.

- In the next few years, both the United Kingdom and Russia are likely to see growth in their industrial sectors. This is because the manufacturing sectors in both countries are growing quickly, which is likely to increase the demand for diesel generators in the industrial sector.

- Furthermore, government initiatives to expand the industrial sector, especially in the United Kingdom and Turkey, are expected to propel the demand for diesel generators during the forecast period.

The United Kingdom is Expected to Dominate the Market

- The United Kingdom is one of the most developed countries in the world and one of the most industrialized countries in Europe. With an ever-increasing demand for energy, various sectors of the economy also need an uninterrupted power supply.

- The United Kingdom's national grid requires a backup power source when there is a peak demand. The National Grid Electricity Transmission (NGET) has been using diesel generators (DG) sets to accommodate this peak demand and provide backup power to substations for key activities such as cooling fans, pumps, and lighting, enabling it to continue to perform its crucial role in the electricity transmission system.

- Backup generators are used at over 250 NGET sites across England and Wales, the majority of which are diesel-powered. These systems provide NGET with the resilience to recover from a loss of power supply event.

- The country benefits from the cost and effectiveness of diesel generators, with improved living standards increasing the demand for power backup devices. Various sectors, such as agriculture, telecommunication, and construction, within the United Kingdom regularly utilize generators.

- Construction activity around the country has been increasing in the past few months. According to the government of the United Kingdom, in 2023, 175.5 orders were placed for new housing public, which has been continuously increasing since 2018. The rise in construction activities is expected to create demand for diesel generators during the forecast period.

- The UK agriculture sector is large and covers more than 60% of the country's total land area. Although the country's power grid is increasingly dependent on renewable sources, the agriculture industry is more interested in the power backup system. It is becoming more dependent on diesel generator systems, which is driving the market.

- More than 40% of the data centers in Europe are present in the United Kingdom and consume a significant amount of power. The data center uses a diesel generator to meet the demand for electricity during a power cut. As of 2023, there were 513 data centers active in the United Kingdom.

- The country is expected to witness more data centers in the coming years, increasing the demand for diesel generators.

Europe Diesel Generator Industry Overview

The European diesel generator market is moderately fragmented. Some of the major players in the market are Caterpillar Inc., Mitsubishi Heavy Industries Engine & Turbocharger Ltd, FG Wilson Engineering (Dublin) Ltd, Cummins Inc., and Yanmar Holdings Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD billion, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Need for Diesel Generators in Standby Applications

- 4.5.1.2 Increasing Use in Several End-user Industries

- 4.5.2 Restraints

- 4.5.2.1 Growing Use of Renewables as an Alternative Power Source

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Capacity

- 5.1.1 Below 75 kVA

- 5.1.2 75-350 kVA

- 5.1.3 Above 350 kVA

- 5.2 End User

- 5.2.1 Residential

- 5.2.2 Commercial

- 5.2.3 Industrial

- 5.3 Geography

- 5.3.1 Germany

- 5.3.2 Russia

- 5.3.3 United Kingdom

- 5.3.4 Norway

- 5.3.5 NORDIC

- 5.3.6 France

- 5.3.7 Italy

- 5.3.8 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Caterpillar Inc.

- 6.3.2 Mitsubishi Heavy Industries Engine & Turbocharger Ltd

- 6.3.3 F G Wilson

- 6.3.4 Cummins Inc.

- 6.3.5 Yanmar Holdings Co. Ltd

- 6.3.6 Generac Power Systems

- 6.3.7 Kohler Co.

- 6.3.8 Doosan Corporation

- 6.4 List of Other Prominent Players

- 6.5 Market Ranking Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Demand for Hybrid Diesel Generators

02-2729-4219

+886-2-2729-4219

柴油发电机:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

柴油发电机:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 2026年全球空气冷发电机市场报告2026年全球柴油发电机市场报告

2026年全球空气冷发电机市场报告2026年全球柴油发电机市场报告 柴油发电机监控系统市场 - 全球产业规模、份额、趋势、机会及预测(按类型、应用、组件、地区和竞争格局划分),2021-2031年

柴油发电机监控系统市场 - 全球产业规模、份额、趋势、机会及预测(按类型、应用、组件、地区和竞争格局划分),2021-2031年 日本柴油发电机市场规模、份额、趋势及预测(按容量、应用、移动性、最终用户及地区划分),2026年至2034年

日本柴油发电机市场规模、份额、趋势及预测(按容量、应用、移动性、最终用户及地区划分),2026年至2034年 柴油发电机市场规模、份额和趋势分析报告:按额定输出功率、应用、地区和细分市场预测(2026-2033 年)

柴油发电机市场规模、份额和趋势分析报告:按额定输出功率、应用、地区和细分市场预测(2026-2033 年) 空冷式发电机市场-2025-2030年预测

空冷式发电机市场-2025-2030年预测 2025年全球柴油发电机市场

2025年全球柴油发电机市场 柴油发电机市场按千伏安额定值、最终用途、应用模式、冷却方式、安装方式和销售管道划分 - 全球预测 2025-2032

柴油发电机市场按千伏安额定值、最终用途、应用模式、冷却方式、安装方式和销售管道划分 - 全球预测 2025-2032 全球便携式可携式发电机市场

全球便携式可携式发电机市场

▼