|

市场调查报告书

商品编码

1644457

义大利低温运输物流:市场占有率分析、产业趋势与成长预测(2025-2030 年)Italy Cold Chain Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

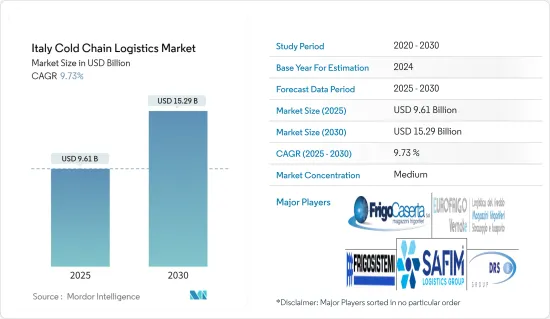

义大利低温运输物流市场规模预计在2025年为96.1亿美元,预计到2030年将达到152.9亿美元,预测期内(2025-2030年)的复合年增长率为9.73%。

关键亮点

- 义大利已成为货运和低温运输物流的全球领跑者。义大利的国内铁路运输市场总量位居德国之后,位居欧洲第二。每年,义大利的铁路和公路网络管理着约 160 万个 20 英尺当量单位 (TEU) 和 1,230 万公吨的货物。

- 义大利蓬勃发展的电子商务正在推动网路购物的成长。最近的一项分析显示,2024 年义大利食品和杂货市场的规模将达到 755 亿欧元(795.7 亿美元),其中线上销售额占总销售额的 6%,相当于 46 亿欧元(48.5 亿美元)。网路销售额较去年同期成长 6.2%,超过实体店面销售额 1.5% 的增幅。消息人士强调,食品采购在义大利网路购物趋势中处于领先地位。主要的消费驱动因素包括便利性,例如实惠的送货、高效的运输和无缝的购物体验。

- 义大利线上杂货店购物者表现出非凡的忠诚度,重复购买率超过 70%。个人护理和美容占义大利数位零售市场的 9%,而食品和饮料占 6%。包括家居和卫生产品在内的「近食品」物品的线上渗透率为 3%,这与欧洲的整体模式一致。 2024年,27.1%的义大利消费者将使用线上平台购买食品,比前一年成长8.8%。此外,21% 的义大利人打算在 2024 年在食物上花费更多,凸显了他们更喜欢更健康的选择。

- 总之,在交通运输进步、转向线上购物以及低温运输物流市场的推动下,义大利的物流和电子商务产业正在经历显着成长。

义大利低温运输物流市场趋势

乳製品消费量增加推动市场

义大利在全球乳製品产业中发挥着至关重要的作用,其生产的乳製品将品质、生产和传统完美地结合在一起。最先进的牛奶加工技术使得新鲜牛奶、超高温牛奶和低脂牛奶等各种形式的牛奶得以广泛供应,以满足有特殊饮食和不耐症人群的需求。

37 种 PDO 起司和众多的区域品种彰显了义大利丰富的起司製作传统。在这里,传统方法已经演变成工业流程,并与使用现代技术製作的乳酪共存。最终的成果是生产出种类繁多的乳酪,以满足国内外消费者的挑剔偏好。

优格和发酵乳製品的口味、尺寸和特性种类繁多,适合各种消费场景。除了传统产品外,益生菌发酵乳还迎合了现代注重健康的市场。乳製品产业在义大利食品市场占据主导地位,销售额达 142 亿欧元(149.6 亿美元)。值得注意的是,义大利75%的原乳产量来自北部。伦巴第大区、艾米利亚-罗马涅大区、威尼託大区和皮埃蒙特大区。

义大利生产 1,100 万吨牛奶,加工成 100 万吨乳酪(超过 44 万吨 PDO)、约 300 万吨巴氏杀菌饮用乳和 19 万吨优格和发酵产品。乳酪产量包括 130 万吨巴氏杀菌牛奶和 160 万吨超高温牛奶。义大利起司出口额达14亿欧元,出口量近25万吨。主要出口品种有莫札瑞拉起司起司和其他新鲜起司(36.4%)、格拉娜帕达诺起司(PDO)和帕玛森起司(PDO)(25%)、罗马羊乳酪(PDO)、戈贡佐拉起司(PDO)和波罗伏洛起司(PDO)。为义大利乳品加工业和牲畜饲养者协会 Alleanza Cooperative Agroalimentari 准备的报告预测,未来五年义大利的牛奶产量将成长 +10/+15%,年均波动率为 +2/+3%,持续到 2030 年。

该报告还包括该国牛奶产量的估计值。义大利将在几年内实现原材料理论上的自给自足(目前为80%)。过去五年来,义大利的牛奶产量大幅增加。产量成长主要发生在义大利北部(Lombardia+19%、艾米利亚-罗马涅 +15%、威尼托 +6.0%、Piemonte+15%),但也发生在一些南部地区(普利亚大区 +12%、Sicilia和巴西利卡塔 +11%、Calabria+17%)。国内乳製品使用量的不断增加,推动了低温运输物流市场的发展。

义大利冷藏设施扩建推动市场

冷藏仓储设施对于保存水果、蔬菜和鱼贝类等生鲜产品至关重要。为满足农业需求,气候温和的义大利冷藏设施正在迅速增加。冷藏和物流技术的进步使得这些设施更有效率,有助于促进义大利的农产品出口。例如,2024年9月,全球先进食品物流先驱Nucold在义大利中南部破土动工建造最大的恆温仓库。计划位于弗罗西诺内省费伦蒂诺,投资 7,000 万欧元(7,377 万美元),将创造 150-200 个就业岗位,预计将于 2026 年投入营运。该工厂位置Froneri 的 Ferentino 工厂旁边,地理位置优越,旨在简化冷冻产品的存储,提供显着的环境效益并支持 Froneri 的业务扩展。 Froneri 是全球第二大包装和冰淇淋公司,也是领先的自有品牌冰淇淋製造商。

该设施第一期将高 40 公尺(130 英尺),可容纳 62,000 个托盘。最重要的是,这个最先进的仓库利用可再生能源和自动化技术,比传统仓库节省 50% 的能源。其特点包括用于装卸行李的自动车辆和全自动拣选系统。 NewCold 的 Ferentino 仓库将扩大其在义大利的业务,补充其在皮亚琴察和博尔戈罗斯的现有设施。如果所有阶段都得以实现,Nucold 在义大利的生产能力将飙升至 20 万个托盘。总之,义大利先进冷藏仓库的发展不仅将支持农业部门,也将为经济成长和环境永续性做出重大贡献。

义大利低温运输物流行业概况

义大利低温运输物流市场细分化,研究市场中有许多国内和国际参与者。市场上企业与新进者之间的联盟日益增多,并且正在确立强势地位。低温运输设施需求庞大,导致企业数量众多,规模较小,专业化程度较低,营运成本较高,发展不平衡、不足。现有主要参与者包括 Safim Logistics、Frigocaserta SRL、Eurofrigo Vernate SRL、Frigoscandia SPA 和 DRS Depositi Regionali Surgelati SRL。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 调查结果

- 调查前提

- 研究范围

第二章调查方法

- 分析方法

- 研究阶段

第三章执行摘要

第四章 市场动态与洞察

- 当前市场状况

- 市场动态

- 驱动程式

- 电子商务成长

- 对永续产品的需求不断增加

- 限制因素

- 司机短缺

- 能源燃料成本上涨

- 机会

- 自动化仓库

- 驱动程式

- 产业吸引力-波特五力分析

- 新进入者的威胁

- 购买者/消费者的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

- 技术趋势和自动化

- 政府法规和倡议

- 产业价值链/供应链分析

- 专注于气候和温度控制存储

- 排放标准和法规对低温运输产业的影响

- 地缘政治事件如何影响市场

第五章 市场区隔

- 按服务

- 贮存

- 运输

- 附加价值服务(冷冻、标籤、库存管理等)

- 按温度类型

- 常温

- 冷藏

- 冷冻

- 按应用

- 园艺(新鲜水果和蔬菜)

- 乳製品(牛奶、冰淇淋、奶油等)

- 肉类和鱼类

- 加工食品

- 製药、生命科学、化学

- 其他的

第六章 竞争格局

- 市场集中度概览

- 公司简介

- Safim Logistics

- Frigocaserta SRL

- Eurofrigo Vernate SRL

- Frigoscandia SPA

- DRS Depositi Regionali Surgelati SRL

- Frigogel SRL

- Soluzioni Logistiche Freddo SRL In Breve SL Freddo SRL

- Sodele Magazzini Generali Frigoriferi SRL

- Horigel SRL

- Fridocks General Warehouses and Frigoriferi SRL

- Lineage Logistics

- UPS*

- 其他公司

第七章:未来市场展望

第 8 章 附录

- 宏观经济指标(GDP分布、按活动划分、运输和仓储业对经济的贡献)

- 对外贸易统计 - 出口和进口(按产品划分)

The Italy Cold Chain Logistics Market size is estimated at USD 9.61 billion in 2025, and is expected to reach USD 15.29 billion by 2030, at a CAGR of 9.73% during the forecast period (2025-2030).

Key Highlights

- Italy has established itself as a global frontrunner in freight and cold chain logistics. Following Germany, Italy ranks as Europe's second-largest market for combined domestic rail transport. Each year, Italy's rail and road networks manage around 1.6 million twenty-foot equivalent units (TEU) and 12.3 million metric tons.

- Italy's burgeoning e-commerce landscape is fueling a rise in online grocery shopping. A recent analysis revealed that in 2024, Italy's food and grocery market, valued at EUR 75.5 billion (USD 79.57 billion), saw online sales accounting for 6% of the total, equating to EUR 4.6 billion (USD 4.85 billion). Online sales surged by 6.2% from the previous year, outpacing the 1.5% growth in brick-and-mortar stores. Sources emphasize that food purchases are at the forefront of Italy's online shopping trends. Key consumer drivers include conveniences such as affordable delivery, efficient shipping, and a seamless purchasing experience.

- Italian online grocery shoppers demonstrate notable loyalty, with repeat purchases exceeding 70%. While personal care and beauty account for 9% of Italy's digital retail market, food and beverage hold a 6% share. 'Near Food' items, which include household and hygiene products, show a 3% online penetration, aligning with broader European patterns. In 2024, 27.1% of Italian shoppers utilized online platforms for food purchases, an 8.8% increase from the previous year. Additionally, 21% of Italians intend to boost their food spending in 2024, emphasizing a preference for healthier options.

- In conclusion, Italy's logistics and e-commerce sectors are experiencing significant growth, driven by advancements in transportation and a shift towards online grocery shopping and cold chain logistics market.

Italy Cold Chain Logistics Market Trends

Increasing Usage of Dairy Products in the Country is Driving the Market

Italy stands as a pivotal player in the global dairy industry, seamlessly blending quality, volume, and tradition in its national production. Cutting-edge milk processing technologies have popularized milk in various forms - fresh, UHT, and LSL - catering to special diets and those with intolerances.

Italy's rich cheese-making heritage is underscored by 37 PDO cheeses and a plethora of local varieties. Here, traditional practices have evolved into industrial processes, coexisting with cheeses crafted through modern techniques. This results in a diverse array of cheeses tailored to meet the discerning tastes of both domestic and international consumers.

Yogurt and fermented milk products boast a vast array of flavors, sizes, and characteristics, making them versatile for various consumption occasions. Beyond traditional offerings, probiotic fermented milk caters to the contemporary health-conscious market. Dominating the Italian food landscape, the dairy sector boasts sales of EUR 14.2 billion (USD 14.96 bn). Notably, 75% of Italy's milk production hails from the northern regions: Lombardia, Emilia Romagna, Veneto, and Piemonte.

Italy produces 11 million tons of milk, converting it into 1 million tons of cheese (with over 440,000 tons being PDO), nearly 3 million tons of pasteurized drinking milk, and 190,000 tons of yogurt and fermented products. The cheese production includes 1.3 million tons of pasteurized milk and 1.6 million tons of UHT milk. Italy's cheese exports, valued at €1.4 billion, amount to nearly 250,000 tons. The leading exported varieties include Mozzarella and other fresh cheeses (36.4%), Grana Padano PDO and Parmigiano Reggiano PDO (25%), followed by Pecorino Romano PDO, Gorgonzola PDO, and Provolone. In a report carried out for the Italian association of farmers and breeders Alleanza Cooperative Agroalimentari, cow's milk production in Italy is expected to increase by +10/+15% in the next five years, with an average annual variation rate of + 2/+3% which is intended to continue until 2030.

The report also includes estimates of the national production of cow's milk: Italy will reach theoretical self-sufficiency in the raw material in a few years (today it is 80%). In the last five years, the production of cow's milk in Italy has increased significantly. Most of the increase in production took place in the northern Italian regions (Lombardy +19%, Emilia Romagna +15%, Veneto +6.0%, Piedmont +15%), but also in some southern regions (Puglia +12%, Sicily and Basilicata) +11%, Calabria +17%). The increasing usage of dairy products in the country is driving the cold chain logistics market.

Expanding Cold Storage Facilities in Italy is Driving the Market

Cold storage facilities are crucial for preserving perishable goods like fruits, vegetables, and seafood. In response to its agricultural industry's needs, Italy, benefiting from a temperate climate, has witnessed a surge in cold storage facilities. Due to advancements in refrigeration and logistics technologies, these facilities have become more efficient, bolstering Italy's agricultural exports. For instance, in September 2024, NewCold, a global frontrunner in advanced food logistics, broke ground on Central and Southern Italy's largest temperature-controlled warehouse. Located in Ferentino, Frosinone, this EUR 70 million (USD 73.77 mn) project is poised to create 150 to 200 jobs and commence operations by 2026. Strategically situated next to Froneri's Ferentino plant, the facility aims to streamline frozen product storage, offering notable environmental advantages and bolstering Froneri's expansion. Froneri stands out as the globe's second-largest packaged ice cream entity and a prominent private-label ice cream manufacturer.

The facility's inaugural phase will see it rise to 40 meters (130 feet) with a capacity of 62,000 pallet spaces. Notably, this state-of-the-art warehouse is engineered to consume 50% less energy than its conventional counterparts, harnessing renewable energy and automation. Features include automated vehicle loading/unloading and a fully automated picking system. Expanding its Italian footprint, NewCold's Ferentino warehouse will complement its existing facilities in Piacenza and Borgorose. Once all phases are realized, NewCold's Italian capacity will soar to 200,000 pallet positions. In conclusion, the development of advanced cold storage facilities in Italy not only supports the agricultural sector but also contributes significantly to the economic growth and environmental sustainability.

Italy Cold Chain Logistics Industry Overview

The Italian cold chain logistics market is fragmented, with several domestic and international companies present in the market studied. The market is experiencing collaborations and new entries of companies to set up their firm foot. The demand for cold chain facilities has led to many small players with a low degree of specialization, leading to problems like high operating costs and unbalanced and insufficient development. Some existing major players in the market include Safim Logistics, Frigocaserta SRL, Eurofrigo Vernate SRL, Frigoscandia SPA, and DRS Depositi Regionali Surgelati SRL.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Analysis Methodology

- 2.2 Research Phases

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS AND INSIGHTS

- 4.1 Current Market Scenario

- 4.2 Market Dynamics

- 4.2.1 Drivers

- 4.2.1.1 Rise in Ecommerce

- 4.2.1.2 Increase in Demand for Persiable Products

- 4.2.2 Restraints

- 4.2.2.1 Shortage of Drivers

- 4.2.2.2 Increasing Energy and Fuel Costs

- 4.2.3 Opportunities

- 4.2.3.1 Automated Warehouses

- 4.2.1 Drivers

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Technological Trends and Automation

- 4.5 Government Regulations and Initiatives

- 4.6 Industry Value Chain/Supply Chain Analysis

- 4.7 Spotlight on Ambient/Temperature-controlled Storage

- 4.8 Impact of Emission Standards and Regulations on Cold Chain Industry

- 4.9 Effect of Geopolitical Events on the Market

5 MARKET SEGMENTATION

- 5.1 By Services

- 5.1.1 Storage

- 5.1.2 Transportation

- 5.1.3 Value-added Services (Blast Freezing, Labeling, Inventory Management, etc.)

- 5.2 By Temperature Type

- 5.2.1 Ambient

- 5.2.2 Chilled

- 5.2.3 Frozen

- 5.3 By Application

- 5.3.1 Horticulture (Fresh Fruits and Vegetables)

- 5.3.2 Dairy Products (Milk, Ice-cream, Butter, etc.)

- 5.3.3 Meats and Fish

- 5.3.4 Processed Food Products

- 5.3.5 Pharma, Life Sciences, and Chemicals

- 5.3.6 Other Applications

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration Overview

- 6.2 Company Profiles

- 6.2.1 Safim Logistics

- 6.2.2 Frigocaserta SRL

- 6.2.3 Eurofrigo Vernate SRL

- 6.2.4 Frigoscandia SPA

- 6.2.5 DRS Depositi Regionali Surgelati SRL

- 6.2.6 Frigogel SRL

- 6.2.7 Soluzioni Logistiche Freddo SRL In Breve SL Freddo SRL

- 6.2.8 Sodele Magazzini Generali Frigoriferi SRL

- 6.2.9 Horigel SRL

- 6.2.10 Fridocks General Warehouses and Frigoriferi SRL

- 6.2.11 Lineage Logistics

- 6.2.12 UPS*

- 6.3 Other Companies

7 FUTURE OUTLOOK OF THE MARKET

8 APPENDIX

- 8.1 Macroeconomic Indicators (GDP Distribution, by Activity, Contribution of Transport, and Storage Sector to economy)

- 8.2 External Trade Statistics - Exports and Imports, by Product

农产品低温运输物流市场预测至2032年:按组件、温度范围、运输方式、储存基础设施、技术、最终用户和地区分類的全球分析

农产品低温运输物流市场预测至2032年:按组件、温度范围、运输方式、储存基础设施、技术、最终用户和地区分類的全球分析 全球冷链物流市场:依技术、温度类型、解决方案、产业和地区划分-市场规模、产业趋势、机会分析和预测(2025-2033 年)

全球冷链物流市场:依技术、温度类型、解决方案、产业和地区划分-市场规模、产业趋势、机会分析和预测(2025-2033 年) 北美低温运输市场规模、份额和趋势分析报告:按类型、包装、设备、应用、国家和细分市场预测(2025-2033 年)

北美低温运输市场规模、份额和趋势分析报告:按类型、包装、设备、应用、国家和细分市场预测(2025-2033 年) 冷链物流设备市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)

冷链物流设备市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年) 低温运输市场按温度范围、设备类型、服务模式、最终用户和分销管道划分-2025-2032 年全球预测低温运输物流市场(按服务类型、温度范围和最终用途)-全球预测,2025-2032全球低温运输物流自动化市场:2032 年预测 - 按组件、温度范围、应用、最终用户和地区分析

低温运输市场按温度范围、设备类型、服务模式、最终用户和分销管道划分-2025-2032 年全球预测低温运输物流市场(按服务类型、温度范围和最终用途)-全球预测,2025-2032全球低温运输物流自动化市场:2032 年预测 - 按组件、温度范围、应用、最终用户和地区分析 电动车、电气化与冷链运输:机会在哪里?

电动车、电气化与冷链运输:机会在哪里? 2025年低温运输全球市场报告2032 年低温运输物流市场预测:按类型、温度类型、应用和地区进行的全球分析

2025年低温运输全球市场报告2032 年低温运输物流市场预测:按类型、温度类型、应用和地区进行的全球分析