|

市场调查报告书

商品编码

1644462

美国数位借贷:市场占有率分析、行业趋势和成长预测(2025-2030 年)United States Digital Lending - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

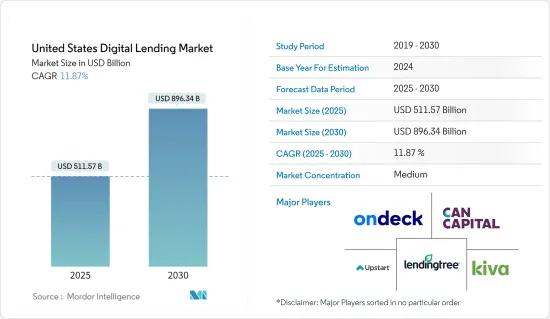

2025年美国数位借贷市场规模预估为5,115.7亿美元,预估至2030年将达8,963.4亿美元,预测期间(2025-2030年)复合年增长率为11.87%。

预计市场扩张将受到数位借贷平台带来的好处的推动,例如改进贷款优化贷款流程、加快决策速度、遵守法规和规范以及提高业务效率。传统借贷平台要求每一步都进行身体接触和人机交互,从而延长了处理时间并增加了人为错误的可能性。然而,数位借贷平台使银行能够实现贷款流程自动化并提高消费者满意度。

关键亮点

- 美国是全球最大、最先进的数位借贷市场之一,也是各领域数位化的早期采用者。此外,蓬勃发展的经济、知名解决方案提供商的强大影响力以及政府和私人组织对开发和发展研发活动的大力投资等因素都将推动该地区对数位借贷的需求。

- 资金筹措是数位借贷经营模式的关键组成部分。数位贷款机构采用的资金筹措模式主要有三种:市场贷款人、资产负债表贷款人和银行通路贷款人。一些数位贷款机构在发展过程中采用多种资金筹措模式。

- 此外,银行具有根本的竞争优势。最重要的是,他们可以获得保险存款,从而获得低成本资本。儘管监管问题似乎阻碍了银行采用新技术,但它们正越来越多地寻找进入金融科技领域的切入点。预计将有许多银行与现有的金融科技公司合作,将他们的技术力与自身的成本优势结合。

- 将银行的低资本成本与技术专长结合,可以使银行以更低的费用提供更有效率的客户体验,从而开拓以前尚未开发的客户群。此外,在美国,从事信用发放的平台可能需要遵守国家许可要求。为此,许多平台与银行合作,执行网路约定的贷款。

- 新冠疫情导致该地区的小型企业在危机期间面临继续营运的资金筹措挑战。预计数位借贷将迎来许多成长和应用机会,尤其是在中小型企业中。此外,在 COVID-19 疫情期间,政府致力于支持其公民。此外,鑑于大规模失业、工资削减和严重的流动性短缺,随着新冠肺炎疫情对贷款行业的影响不断显现,银行和金融机构(FI)的信贷成本和不良资产率预计将上升。贷款人可以透过使用科技受益匪浅,以帮助他们适应新常态。

美国数位借贷市场趋势

越来越多潜在的贷款购买者正在采用数位化行为

- 根据美国小型企业管理局统计,美国未偿还的100万美元以下小型企业贷款余额为4,100亿美元,未偿还的小型企业消费贷款余额为4兆美元。美国联邦储备银行估计,由于银行不愿发放小额贷款,约有 1,000 亿美元的信贷需求未得到满足。为了满足这一未满足的需求,利用科技与银行合作的数位贷款机构正在受到关注。

- 此外,信贷平台鼓励投资者分散风险。投资者可以选择在各种贷款中进行多元化投资,通常会根据他们选择的风险类别和条款自动获得贷款组合的投资机会。美国超过 95% 的点对点消费者平台使用自动选择流程。在信用便利方面,金融科技平台可以提供与银行等传统信贷提供者类似的监控和定序能力。

- 大多数消费者使用金融科技提供者来再融资或合併现有债务,但有些消费者也使用它们来为更大的购买资金筹措资金(例如汽车或房地产)。在美国,学生借贷来资助高等教育的现象十分突出。

- 在商业方面,各类微企业寻求营运资金和投资计划融资的情况很常见。资金也可以透过发票交易的形式筹集,投资者根据公司的发票(应收帐款)购买折价应收帐款。小型企业对大多数地区的经济做出了重大贡献。以下统计数据支持上述说法:根据美国小型企业管理局 (SBA) 的数据,超过 50% 的美国拥有或经营小型企业。

消费者数位借贷预计将大幅成长

- 尤其是专注于消费贷款的GreenSky Inc.的IPO,引发了人们对银行通路贷款的关注。该公司已获得超过110亿美元的银行承诺。小型企业贷款机构 OnDeck 宣布扩展其 OnDeck-as-a-Service 平台,将其技术授权给银行。该公司增加了 PNC 银行作为客户,并推出了新的子公司 ODX,以处理未来基于银行管道的业务。 Avant推出了个人借贷银行合作平台 Amount。

- 为了继续发展,数位贷款机构正在抓住机会扩大其覆盖范围,包括资金筹措和产品供应。例如,SoFi 最初是一家学生贷款再融资公司,现在提供个人贷款和房屋抵押贷款。 Lending Club 专门提供个人贷款,同时也提供商业贷款产品。虽然 Square 和 Paypal 等一些公司已经从相邻的金融科技领域进入数位借贷领域,但其他贷款机构正寻求透过提供贷款以外的服务来朝这个方向发展。 SoFi 在这方面最为活跃,提供资产管理服务并接受其高收益储蓄帐户产品 SoFi Money 的申请。

- 随着该地区继续面临学生贷款债务危机,学生贷款新兴企业正在寻找新的投资和新的客户。美国联邦估计美国学生贷款债务为1.7兆美元。平均而言,学生毕业时背负 29,000 美元的私人和联邦贷款债务,其中 15% 拖欠贷款。

- 该部门提供的产品包括学生贷款再融资、直接学生贷款、个人贷款以及资产管理和房屋抵押贷款产品。

- 云端可以被视为数位借贷领域最重要的趋势之一,因为它能够协助金融机构进行线上服务交付、文件管理、资讯储存、资料处理等。据埃森哲称,目前超过 90% 的银行在云端运行至少相当一部分工作负载。

美国数位借贷产业概况

随着各类全球公司进入美国数位借贷市场,投资和併购活动预计将增加,市场预计将呈现半固定化趋势。供应商正在透过提供一系列优惠来增加支出以吸引消费群。此外,这些投资在我们的竞争策略中发挥强大的作用。获得分销管道、现有的业务关係、更好的供应链知识和自有平台使进入市场的现有科技巨头比新竞争对手更具优势。

2023年10月,美国软体公司Blend Labs与金融机构和消费者研究组织的软体供应商MeridianLink Inc.宣布建立合作伙伴关係。 Blend 表示,使用 MeridianLink 消费者贷款发放软体 (LOS) 的金融机构可以透过利用 Blend 的统一平台和消费者银行发放软体,享受更快的银行、信用卡和贷款产品的入职和申请流程。

2023 年 9 月,富国银行支持的抵押房屋抵押贷款金融科技公司 Maxwell 宣布将收购数位借贷平台 Revvin(前身为 MortgageHippo),以改善其销售点技术。该公司专注于 Revvin 更快的贷款发放流程,并相信 Maxwell 将使房屋抵押贷款市场的贷方受益,该市场继续面临利率上升、贷款量限制和贷款成本增加的挑战。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概况

- 监管状态

- 美国个人贷款借款人的关键指标

- 美国借款人贷款与负债比率

- 超级总理

- 优质加值

- 主要的

- 接近黄金地段

- 次级贷款

- 美国借款人平均余额

- 超级总理

- 优质加值

- 主要的

- 接近黄金地段

- 次级贷款

- 美国借款人拖欠率

- 超级总理

- 优质加值

- 主要的

- 接近黄金地段

- 次级贷款

- 美国借款人贷款与负债比率

- 数位贷款机构发放量分析

- 个人贷款

- 小型企业贷款

- 美国次级抵押贷款分析

- 状态分布

- 年龄结构

- 次级抵押贷款类别整体萎缩

第五章 市场动态

- 市场驱动因素

- 更多具有「数位行为」的潜在贷款购买者

- 可支配所得增加

- 市场限制

- 数字借贷的安全问题

第六章 市场细分

- 按类型

- 商业

- 商业数位借贷市场动态

- 商业数位借贷生态系统(包括新兴企业和成熟企业)

- 市场估计和预测

- 消费者

- 消费者数位借贷市场动态

- 消费者导向的数位借贷模式(发薪日贷款、P2P借贷、个人贷款、汽车贷款、学生贷款)

- 消费者数位借贷生态系统(包括新兴企业和现有企业)

- 市场估计和预测

- 商业

第七章 竞争格局

- 公司简介

- Bizfi, LLC.

- OnDeck Capital Inc.

- Prosper Marketplace Inc.

- LendingClub Corp.

- Social Finance Inc.(SoFi)

- Upstart Network Inc.

- Kiva Microfunds

- Kabbage Inc.

- Lendingtree Inc.

- CAN Capital Inc.

第八章投资分析

第九章 市场机会及未来展望

The United States Digital Lending Market size is estimated at USD 511.57 billion in 2025, and is expected to reach USD 896.34 billion by 2030, at a CAGR of 11.87% during the forecast period (2025-2030).

Market expansion is anticipated to be fueled by the advantages provided by digital lending platforms, such as improved loan optimization loan process, quicker decision-making, compliance with regulations and norms, and improved corporate efficiency. Traditional lending platforms required physical contact and human engagement at every stage, which prolonged processing times and raised the possibility of human error. However, digital lending platforms allow banks to automate the loan process, improving consumer satisfaction.

Key Highlights

- The United States is one of the largest and most advanced markets for digital lending globally due to its early adoption of digitization in various sectors. Also, factors such as the strong economy and robust presence of prominent solution providers, coupled with strong investment by government and private organizations for the development and growth of research & development activities, are poised to drive the demand for digital lending in the region.

- Funding is a crucial element of the digital lending business model. There are three major funding models used by digital lenders: Marketplace lenders, Balance sheet lenders, and bank channel lenders. Several digital lenders have been tapping multiple funding models as they grow.

- Further, banking institutions retain certain fundamental competitive advantages. Arguably the most important is their access to insured deposits, which affords them low-cost capital. Regulatory concerns have likely caused banks to hesitate when adopting new technologies, but banks are increasingly looking for points of entry to the fintech space. It is expected that many banks will partner with existing fintech companies to have their cost advantages with the fintech's technological capabilities.

- By combining their technological expertise with banks' lower cost of capital, these partnerships could enable banks to provide more efficient customer experiences at lower rates and open them up to previously untapped customer segments. Also, in the United States, platforms engaging in credit origination can be subjected to licensing requirements in each state. For this reason, many platforms partner with the banks to originate loans agreed online.

- Owing to the COVID-19 pandemic, SMEs in the region faced challenges in raising funds during the crisis to keep their businesses operating. Digital Lending is expected to find several opportunities, especially among SMEs, for growth and adoption. Further, during the COVID-19 pandemic, the government aimed to support the people. Moreover, given widespread job losses, wage reductions, and a severe liquidity shortage, banks and financial institutions (FIs) anticipates to experience an increase in credit costs and non-performing assets ratio as the effects of COVID-19 on the lending industry develop. Lenders can benefit significantly from the use of technology to assist them in adjusting to the new normal.

United States Digital Lending Market Trends

Increasing Number of Potential Loan Purchasers with Digital Behavior

- According to the U.S. Small Business Administration, there are USD 410 billion in sub-USD 1 million loans to small firms and USD 4 trillion in outstanding consumer loans for small enterprises in the US. In addition, the US Federal Reserve Bank of NY calculates an approximate USD 100 billion unmet credit demand due to banks' resistance to making small-dollar loans. To address the unmet demand, technology-driven digital lenders are attracting attention in their capacity to collaborate with banks.

- Moreover, credit platforms majorly encourage investors to spread the risks. Investors can choose to spread the investments across various multiple loans and often can automatically gain exposure to a portfolio of loans based on the risk category and terms they select. Among P2P (peer-to-peer) consumer platforms, more than 95% of the United States use an auto-selection process. In facilitating credit, fintech platforms can provide monitoring and servicing functions that are similar to those of traditional credit providers such as banks.

- Most consumers use fintech providers to refinish or consolidate existing debts, but some use them to finance their major purchases (such as vehicles or real estate). Borrowing by students to fund higher education is prominent in the United States.

- On the business side, various small and micro enterprises typically seek funds for working capital or investment projects. Financing can also be in the form of invoice trading, whereby investors purchase discounted claims on a firm's invoices (receivables). SMEs are contributing to the economy significantly for most regions. The following statistics validate the above statement: According to the US Small Business Administration (SBA), more than 50% of Americans either own or work for a small business.

Consumer Digital Lending is Expected to Grow Significantly

- Bank channel-based lending drew particular attention, especially with the IPO of consumer loan-focused GreenSky Inc. The company has secured more than USD 11 billion in bank commitments. Small business-focused lender OnDeck announced an expansion of its OnDeck-as-a-Service platform through which it licenses its technology to banks. The company added PNC Bank as a customer and launched a new subsidiary, ODX, to handle future bank channel-based business. Avant launched a bank partnership platform for personal lending called Amount.

- In order to keep growing, digital lenders are taking advantage of opportunities to expand the scope of their activities, both in terms of funding and product offerings. For example, SoFi, which began as a student loan refinancing company, now offers personal loans and mortgages. Personal loan-focused LendingClub also offers a business loan product. While some the companies, such as Square and PayPal, entered digital lending from adjacent fintech segments, some lenders are moving in the other direction by offering nonlending services. SoFi has been the most aggressive on this front, offering wealth management services and accepting applicants for its high-yield deposit account product, SoFi Money.

- Student-focused lenders remain the most diversified platforms in the digital lending sector as Student loan startups are witnessing new investments and new customers as the region faces a continued student loan debt crisis. The Federal Reserve estimates USD 1.7 trillion in U.S. student loan debt. Students, on average, graduate with USD 29,000 of private and federal loan debt and default on their loans at a rate of 15%.

- Product offerings in this segment include student loan refinance, direct student loans, personal loans, and even wealth management and mortgage products.

- Due to its capacity to assist financial institutions with service delivery, document management, information storage, and data processing online, the cloud can be regarded as one of the most important trends in digital lending. It's understandable why, according to Accenture, more than 90% of banks currently have at least a significant level of workloads operating in the cloud.

United States Digital Lending Industry Overview

The United States digital lending market is expected to be semi-consolidated, observing an increase in the number of investments and M&A activities by various global enterprises to gain access to the market. Vendors are increasingly spending on gaining a consumer base by offering numerous benefits. In addition, such investments are a strong part of their competitive strategy. Access to the distribution channel, already present business relations, better supply chain knowledge, and the self-owned platform give the established tech giants entering the market an advantage over the new competitors.

In October 2023, Blend Labs, a United States-based software company, and MeridianLink Inc., a software provider for financial institutions and consumer reporting agencies, announced a partnership. Blend stated that lenders utilizing MeridianLink Consumer loan origination software (LOS) can use Blend's unified platform and consumer banking origination software for a quick onboarding and application procedure for banking, credit card, and loan products.

In September 2023, the digital lending platform Revvin, formerly MortgageHippo, was announced to be acquired by Maxwell, a mortgage fintech sponsored by Wells Fargo, to improve its point-of-sale technology. The company focuses on Revvin's faster loan origination process, which Maxwell thinks would benefit lenders as the mortgage market continues to be challenged by rising interest rates, limited loan volume, and increasing lending expenses.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Regulatory Landscape

- 4.3 Key Indicators for Personal Loan Borrowers in the United States

- 4.3.1 Percentage of Loan Debt in United States Held By Borrowers

- 4.3.1.1 Super Prime

- 4.3.1.2 Prime Plus

- 4.3.1.3 Prime

- 4.3.1.4 Near Prime

- 4.3.1.5 Sub Prime

- 4.3.2 Average Outstanding Balances in United States Held By Borrowers

- 4.3.2.1 Super Prime

- 4.3.2.2 Prime Plus

- 4.3.2.3 Prime

- 4.3.2.4 Near Prime

- 4.3.2.5 Sub Prime

- 4.3.3 Delinquency Rates of Borrowers in United States

- 4.3.3.1 Super Prime

- 4.3.3.2 Prime Plus

- 4.3.3.3 Prime

- 4.3.3.4 Near Prime

- 4.3.3.5 Sub Prime

- 4.3.1 Percentage of Loan Debt in United States Held By Borrowers

- 4.4 Analysis of Origination Volumes of Digital Lenders

- 4.4.1 Personal Loans

- 4.4.2 SME Loans

- 4.5 Analysis of Subprime Borrowers in the United States

- 4.5.1 Distribution by States

- 4.5.2 Demographic Breakdown by Age

- 4.5.3 Overall Shrinking of Subprime Population in the Country

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Uptick of Potential Loan Purchasers with 'Digital Behavior'

- 5.1.2 Increasing Disposable Income

- 5.2 Market Restraints

- 5.2.1 Security Concerns involved in Digital Lending

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Business

- 6.1.1.1 Business Digital Lending Market Dynamics

- 6.1.1.2 Business Digital Lending Ecosystem (including both Startups and Incumbents)

- 6.1.1.3 Market Size Estimates and Forecasts

- 6.1.2 Consumer

- 6.1.2.1 Consumer Digital Lending Market Dynamics

- 6.1.2.2 Consumer Digital Lending Models (Payday Lenders, Peer-to-peer Loans, Personal Loans, Auto Loans, and Student Loans)

- 6.1.2.3 Consumer Digital Lending Ecosystem (including both Startups and Incumbents)

- 6.1.2.4 Market Size Estimates and Forecasts

- 6.1.1 Business

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Bizfi, LLC.

- 7.1.2 OnDeck Capital Inc.

- 7.1.3 Prosper Marketplace Inc.

- 7.1.4 LendingClub Corp.

- 7.1.5 Social Finance Inc. (SoFi)

- 7.1.6 Upstart Network Inc.

- 7.1.7 Kiva Microfunds

- 7.1.8 Kabbage Inc.

- 7.1.9 Lendingtree Inc.

- 7.1.10 CAN Capital Inc.

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

数位借贷:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

数位借贷:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 2026-2030年全球数位借贷市场

2026-2030年全球数位借贷市场 数位借贷平台市场预测至2032年:按组件、部署模式、贷款类型、应用、最终用户和地区分類的全球分析

数位借贷平台市场预测至2032年:按组件、部署模式、贷款类型、应用、最终用户和地区分類的全球分析 2025年借贷技术(LendTech)全球市场报告2025年全球数位借贷平台市场报告

2025年借贷技术(LendTech)全球市场报告2025年全球数位借贷平台市场报告 数位借贷平台市场规模、份额、趋势及预测(按类型、组件、部署模式、产业垂直领域及地区划分),2025 年至 2033 年

数位借贷平台市场规模、份额、趋势及预测(按类型、组件、部署模式、产业垂直领域及地区划分),2025 年至 2033 年 数位借贷平台市场按组件、类型、利率类型、贷款类型、应用、借款人类型和部署模式划分—2025-2030 年全球预测

数位借贷平台市场按组件、类型、利率类型、贷款类型、应用、借款人类型和部署模式划分—2025-2030 年全球预测 数位借贷平台市场规模、份额、趋势分析报告:按组件、部署、最终用途、地区、细分市场预测,2025 年至 2030 年

数位借贷平台市场规模、份额、趋势分析报告:按组件、部署、最终用途、地区、细分市场预测,2025 年至 2030 年 数位借贷平台市场规模、份额、成长分析(按组成部分、按贷款额金额、按部署模式、按订阅类型、按贷款类型、按地区)-2025 年至 2032 年产业预测

数位借贷平台市场规模、份额、成长分析(按组成部分、按贷款额金额、按部署模式、按订阅类型、按贷款类型、按地区)-2025 年至 2032 年产业预测 全球数位借贷平台市场规模(按产品、部署类型、最终用户、地理位置和预测)

全球数位借贷平台市场规模(按产品、部署类型、最终用户、地理位置和预测)