|

市场调查报告书

商品编码

1644842

二次包装:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Secondary Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

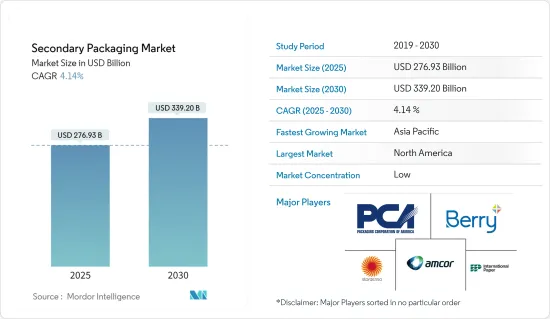

2025 年二次包装市场规模预计为 2,769.3 亿美元,预计到 2030 年将达到 3,392 亿美元,预测期内(2025-2030 年)的复合年增长率为 4.14%。

关键亮点

- 二次包装对于保护产品、保持产品完整以及优化运输过程起着至关重要的作用。纸箱、托盘和薄膜捆包是一些具有多种形式和尺寸的二次包装的例子。二次包装对于品牌行销和产品展示也很重要。

- 食品和饮料、药品、化妆品、个人护理和家用产品等多个终端用户行业中二次包装的部署不断增加,正在推动市场的成长。

- 二次包装公司以循环性和永续性作为成长策略,以增加二次包装应用的回收解决方案的可用性。 2023 年 6 月,利安德巴塞尔与 AFA Nord 建立伙伴关係,回收上市后的柔性二次包装废弃物。合资公司 LMF Nord GmbH 计划建造一座回收工厂,将 LDPE废弃物转化为可用于包装的高品质再生塑胶材料。

- 医疗保健中的二次包装用于为瓶子、管瓶和泡壳等初级包装提供额外的保护和组织。二次包装还可以增加产品的需求,因为它提供有关产品的重要信息,例如剂量说明、有效期和监管信息,并有助于防止假冒和篡改。

- 各类二次包装製造商都受到严格的监管,很难创新新产品。此外,消费者对二次包装的偏好不断变化可能会使製造商更难在市场上竞争。

二次包装市场趋势

折迭式纸盒预计将占据主要市场占有率

- 随着人们的注意力转向环保和永续实践,食品和饮料、医疗保健、个人护理、居家医疗和零售等许多行业对折迭式纸盒的需求正在增加。折迭式纸盒的需求受到消费者对永续包装的偏好、原材料的可用性、纸张的轻质、生物分解性和可回收特性以及减少森林砍伐的推动。

- 各国旅游业的快速成长导致加工食品、碳酸饮料和已调理食品的消费量增加。食品服务业的二次包装要求正在改变并推动对食品药物管理局批准纸箱的需求。用途广泛且引人注目的纸质食品容器的出现推动了该产品的需求。

- 各公司纷纷透过投资併购作为扩大策略,以增加市场占有率。 2023年9月,美国包装公司Graphic Packaging宣布收购美国折迭纸盒公司Bell。此次收购还包括贝尔在美国的三家加工工厂,这可能会提升 Graphic 在食品包装市场的份额。

- 各公司正在製造个人化和创新的折迭纸盒来包装各种美容产品,如化妆品、护肤、护髮产品等,从而推动了需求。公司也致力于透过使用环保材料来製作纸箱,实现永续包装。

- 根据美国林业和农业理事会的数据,2023年全球纸和纸板产能约为258,631,000吨。过去十年来,由于各终端用户产业的需求不断增长,纸和纸板的产量一直保持稳定。这些因素预计将为市场参与企业提供开发新产品以获得市场占有率的机会。

预计北美将占据较大的市场占有率

- 北美二次包装市场受到二次包装中环保材料的使用日益增长的推动。食品和饮料、製药和化妆品行业等最终用户越来越意识到需要使用环保包装材料来满足永续性的可持续性需求。由纸板等可回收和生物分解性材料製成的纸质容器促进了永续性,从而促进了市场成长。

- 顾客支出的增加和网路购物销售额的不断增长正在影响电子商务的扩张。根据美国人口普查局预测,2024年第一季电子商务销售额将占美国零售额的15.6%,超过2023年第一季,推动市场成长。

- 北美的製药业正在蓬勃发展,一系列新药的不断开发推动了对二次包装的需求。 2024 年 5 月,美国合约包装公司Sharp Corporation Services 宣布将扩建製造地,以增加其无菌注射二次包装的生产能力。

- 二次饮料包装有多种用途。二次包装用于保护重瓶子免于破损,并透过将多个物品一起运输来降低成本。它还可以用作屏障或保护免受阳光照射和其他外部挑战。二次饮料包装有助于行销产品并提高产品的知名度,从而推动市场成长。

二次包装行业概况

二级包装市场比较分散,主要参与者正在采用各种成长策略,如併购、新产品发布、业务扩张、合资和伙伴关係,以加强其市场地位。市场的主要企业包括 Amcor、国际纸业公司、雷诺包装、斯道拉恩索、WestRock、Ball Corporation 和 Berry Global。

- 2024 年 5 月,Mondi 推出了 TrayWrap,一种新的纸质二次包装解决方案,用于取代用于食品和饮料产品的塑胶收缩膜。 TrayWrap 由 100% 牛皮纸製成,完全可回收。

- 2023年9月,美国WestRock将与爱尔兰Smurfit Kappa合併,成立永续包装解决方案製造商Smurfit WestRock。成立合资公司是两家公司的策略性倡议,旨在拓宽 Smurfit 在瓦楞纸板和箱板纸领域的产品系列,同时拓展各个终端用户市场的地域覆盖范围。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 买家的议价能力

- 供应商的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 地缘政治情势如何影响市场

第五章 市场动态

- 市场驱动因素

- 全球工业和消费者活动的扩张

- 安全交通的需求日益增加

- 市场限制

- 消费者对永续环境的需求和意识不断改变

第六章 市场细分

- 依产品类型

- 折迭式纸盒

- 瓦楞纸箱

- 塑胶盒

- 包装和薄膜

- 按最终用户产业

- 食物

- 饮料

- 医疗

- 家用电子电器

- 个人护理及家居产品

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

第七章 竞争格局

- 公司简介

- Amcor PLC

- Berry Global Inc.

- Packaging Corporation of America

- Stora Enso Oyj

- WestRock Company

- Ball Corporation

- International Paper Company

- Sealed Air Corporation

- Reynolds Group Holdings

- Mondi Group

- Multi-Pack Solutions LLC

第八章投资分析

第九章:市场的未来

The Secondary Packaging Market size is estimated at USD 276.93 billion in 2025, and is expected to reach USD 339.20 billion by 2030, at a CAGR of 4.14% during the forecast period (2025-2030).

Key Highlights

- Secondary packaging plays a pivotal role in product protection by holding them together and optimizing the product for transportation. Cartons, trays, and film bundles are a few examples of secondary packaging available in several shapes and sizes. Secondary packaging is also important for brand marketing and product display.

- The increasing deployment of secondary packaging for multiple end-user industries, including food and beverage, pharmaceuticals, cosmetics, personal care, and household care, is boosting market growth.

- Companies providing secondary packaging aim for circularity and sustainability as a growth strategy to increase the availability of recycled solutions for secondary packaging applications. In June 2023, LyondellBasell and AFA Nord entered a partnership to recycle post-commercial flexible secondary packaging waste. In the joint venture, LMF Nord GmbH planned to build a recycling plant to turn LDPE waste into quality recycled plastic material that can be used in packaging.

- Secondary packaging in healthcare is used to provide an additional level of protection and organization for primary packaging, including bottles, vials, and blisters. Secondary packaging can also provide important information about the product, such as dosage instructions, expiration dates, and regulatory information, and help prevent counterfeiting and tampering, thus boosting product demand.

- Various manufacturers of secondary packaging are subject to stringent regulations, which can make it challenging for them to innovate new products. Also, evolving consumer preferences for secondary packaging can make it difficult for manufacturers to compete in the market.

Secondary Packaging Market Trends

The Folding Cartons Segment is Expected to Hold a Significant Market Share

- Folding carton demand has been increasing across many industries, including food and beverage, healthcare, personal care, homecare, retail, and others, as the focus shifts to eco-friendly and sustainable practices. The need for folding cartons is driven by consumer awareness of sustainable packaging preferences, availability of raw materials, the lightweight, biodegradable, and recyclable nature of paper, and deforestation.

- Rapidly growing tourism in different countries has led to the high consumption of processed food, carbonated beverages, and ready-to-eat foods. The food service industry's requirement for secondary packaging has been reshaped, fueling the demand for folding cartons that are approved by the FDA (Food and Drug Administration). The availability of versatile and eye-catching food folding cartons boosts product demand.

- Various companies are investing in mergers and acquisitions as an expansion strategy to boost their market share. In September 2023, Graphic Packaging, a US packaging company, announced the acquisition of Bell Inc., a US folding carton company. The acquisition included Bell's three converting facilities in the United States, which is likely to grow Graphic's presence in the food service packaging market.

- Various companies are manufacturing personalized and innovative folding cartons to package different beauty products, including cosmetics, skincare, and haircare, boosting the demand. Companies are also aiming toward sustainable packaging by using eco-friendly materials to make folding cartons.

- According to the Forest and Agriculture Association of the United States, in 2023, the production capacity of paper and paperboard was approximately 258,631 thousand tons globally. The production of paper and paperboard has been stable over the past decade with respect to the growing demand in various end-user industries. Such factors are expected to create an opportunity for the players in the market to develop new products to capture market share.

North America is Expected to Hold a Significant Market Share

- The North American market for secondary packaging is being driven by the increasing usage of environment-friendly materials in secondary packaging. End users, such as the food and beverage, pharmaceutical, and cosmetic industries, are becoming increasingly aware of the need to utilize environment-friendly packaging materials to cater to growing sustainability demand. Folding cartons made from recyclable and biodegradable materials like paperboard promote sustainability, propelling market growth.

- Increasing customer spending and growing online shopping sales influence the expansion of e-commerce. According to the US Census Bureau, e-commerce sales accounted for 15.6% of all US retail sales in the first quarter of 2024, higher than the first quarter of 2023, propelling the market growth.

- The rapidly booming pharmaceutical industry in North America and the growing advancements in developing a variety of new drugs are driving the demand for secondary packaging. In May 2024, Sharp Services, a United States-based contract packaging company, announced the expansion of its Pennsylvania manufacturing site to increase its production capacity for sterile injectables secondary packaging.

- The secondary packaging for beverages serves different purposes. The secondary packaging is used to protect heavy bottles from breaking, and it reduces costs by shipping multiple items together. It may sometimes be used as a barrier or protection against sunlight exposure or other external challenges. The secondary packaging for beverages helps in product marketing and enhances product visibility, thus driving market growth.

Secondary Packaging Industry Overview

The secondary packaging market is fragmented, with major players adopting various growth strategies, such as mergers and acquisitions, new product launches, expansions, joint ventures, partnerships, and others, to strengthen their position in the market. Some of the major players in the market are Amcor, International Paper Company, Reynolds Packaging, Stora Enso, WestRock, Ball Corporation, and Berry Global.

- May 2024: Mondi unveiled a new secondary paper packaging solution, "TrayWrap," to replace plastic shrink film used for food and beverage products. TrayWrap is made from 100% krafted paper, which is fully recyclable.

- September 2023: WestRock, a United States-based company, merged with Smurfit Kappa, an Ireland-based company, to create Smurfit WestRock to manufacture sustainable packaging solutions. The joint venture was a strategic move by the companies to expand Smurfit's product portfolio in corrugated and containerboard, along with regional expansion for various end-user markets.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Buyers

- 4.2.2 Bargaining Power of Suppliers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products and Services

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Impact of the Geo-Political Scenarios on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Industrial and Consumer Activities across the World

- 5.1.2 Increased Need for Safe Transportation

- 5.2 Market Restraints

- 5.2.1 Changing Consumer Needs and Awareness Towards a Sustainable Environment

6 MARKET SEGMENTATION

- 6.1 By Product Type

- 6.1.1 Folding Cartons

- 6.1.2 Corrugated Boxes

- 6.1.3 Plastic Crates

- 6.1.4 Wraps and Films

- 6.2 By End-user Industry

- 6.2.1 Food

- 6.2.2 Beverage

- 6.2.3 Healthcare

- 6.2.4 Consumer Electronics

- 6.2.5 Personal Care and Household Care

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia Pacific

- 6.3.4 Latin America

- 6.3.5 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Amcor PLC

- 7.1.2 Berry Global Inc.

- 7.1.3 Packaging Corporation of America

- 7.1.4 Stora Enso Oyj

- 7.1.5 WestRock Company

- 7.1.6 Ball Corporation

- 7.1.7 International Paper Company

- 7.1.8 Sealed Air Corporation

- 7.1.9 Reynolds Group Holdings

- 7.1.10 Mondi Group

- 7.1.11 Multi-Pack Solutions LLC