|

市场调查报告书

商品编码

1644926

欧洲浮体式海上风电 -市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)Europe Floating Offshore Wind Power - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

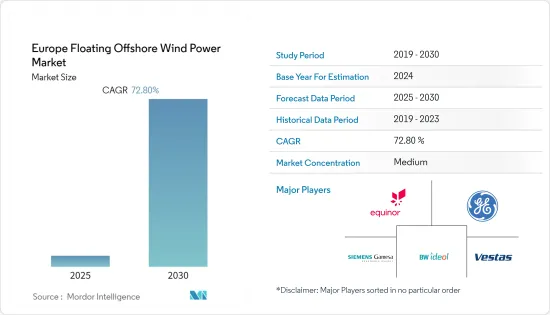

预计预测期内欧洲浮体式海上风电市场复合年增长率将达到 72.8%。

2020 年,市场受到了 COVID-19 的不利影响。目前市场已经恢復到疫情前的水准。

从长远来看,离岸风力发电需求的增加预计将刺激欧洲浮体式海上风电市场的成长。此外,离岸风力发电计划的深水域被认为是利用深水域丰富风能潜力的突破性技术,预计将推动市场成长。

同时,人们越来越多地采用替代清洁发电能源,主要是天然气和太阳能。由于太阳能和燃气发电是更清洁的能源生产方式,它们的普及预计会削弱对风电的需求。

新兴市场和尚未开发市场对离岸风力发电的兴趣日益浓厚,预计将在预测期内为欧洲浮体式海上风电市场带来有利的成长机会。

预计英国将主导市场。预计在预测期内,其复合年增长率也将达到最高。这一增长归因于投资的增加以及政府政策的实施。

欧洲浮体式海上风力发电市场趋势

浮体式海上风电的政府政策与私人投资

浮体式海上风电被视为挪威石油和天然气产业转型为可再生能源的关键新兴产业。 2020年12月,挪威石油和能源部长宣布将在挪威建立一个新的风电研究中心。诺斯风研究中心将专注于技术创新,离岸风力发电研究是其主要重点之一。

然而,由于担心对景观和生态系统的影响,挪威面临当地对陆上风电发电工程的反对。因此,2022年5月,挪威宣布计画在2040年大幅扩大离岸风力发电,旨在将这个依靠石油和天然气累积财富的国家变成再生能源的出口国。该国政府因继续支持石油和天然气产业而受到环保人士的批评,并设定了到 2040 年开发 30 吉瓦(GW)离岸风力发电容量的目标。

目前已有多家公司报名加入挪威的行动,希望扩大其离岸风力发电项目,并利用其在石油和天然气探勘行业的经验展示新技术。

例如,壳牌和英国石油公司以及埃尼、Equinor和Orsted等公司都对挪威设施感兴趣。 Vattenfall和挪威的Seagust公司也宣布,双方已成立合资企业参与竞标。 EDF Renewables表示,它将与挪威独立电力生产商Deep Wind Offshore合作,并于2021年12月加入该进程。

法国浮体式海上风电市场是世界上最大的市场之一。该国还表示有兴趣在 2050 年安装 50 个离岸风力发电,总合40 吉瓦,这将减缓陆上风电的发展。作为增加离岸风力发电的一部分,法国政府于 2022 年 3 月启动了竞争性竞标程序,以开发地中海两个 250 兆瓦的浮体式海上风电场。第一个风电场将建在纳博讷海岸,距离海岸 22 多公里,第二个风电场将建在滨海福斯海岸 22 公里处。

根据爱尔兰风能协会 (WEI) 在 2021 年第一季进行的最新开发商调查,凯尔特海拥有约 3GW 的浮体式海上风电发电工程处于开发初期。大西洋地区也提案另外 5GW浮体式海上风电发电工程。例如,2022 年 6 月,基利贝格斯渔民组织和辛巴达海洋服务公司提案在爱尔兰多尼戈尔海岸建造一个浮体式海上风电场。他们与瑞典浮动式风力发电开发技术供应商Hexicon签署了谅解备忘录。

截至 2021 年,欧洲已安装新的风电容量 17.4 GW,其中陆上 14 GW,海上 3.4 GW。 2021年将成为风电装置容量创纪录的一年(超过2017年的17.1吉瓦),欧盟27国每年需要安装32吉瓦的风电容量才能达到40%的可再生目标。

由于该地区拥有离岸风电资源并获得政府支持,预计欧洲将在预测期内成为浮体式海上风电最大的市场之一。

英国主导市场成长

英国是全球最大的离岸风力发电市场之一,截至 2021 年,其在 38 个地点的累积设置容量超过 10GW。另有5GW正在前期建设中,另有11GW正在规划中。

根据WindEurope预测,2021年英国海上装置容量将达260万千瓦,占欧洲海上装置容量的88%。海上设施建设主要受 Moray 酵母和 Triton Knoll 风电场的建成推动。英国陆上风电装置容量略有增加,但仍处于2005年以来的第二低水准。

美国绿色工业革命十点计画中提出,2030年安装40吉瓦的离岸风力发电,这个目标推动了美国产业的成长。其中包括采用浮体式技术的1GW。 2022 年 4 月发布的英国能源安全战略 (BESS) 进一步增强了这一目标,该战略旨在到 2030 年实现离岸风力发电达到 50GW,其中浮体式海上风电将贡献 5GW。

作为其净零计画的一部分,苏格兰政府设定了到 2030 年提供高达 11 吉瓦的离岸风力发电容量的目标,以支持苏格兰到 2045 年实现净零排放的承诺。苏格兰是世界上第一个商业浮体式海上风电发电工程的所在地,即 Equinor/Masdar 的 Hywind Scotland 风电场,该项目于 2017 年开始运营,使用五台 SGRE 6 MW 涡轮机。

2022 年 8 月,Cerulean Winds 与英国Ping Petroleum 签署了一项协议,将建造一个主要由离岸风电动力来源的海上油气设施。根据合同,Cerulean Winds 将与层级工业合作伙伴联盟一起提供大型浮体式海上风力发电机,并透过电缆连接到 Ping Petroleum 的浮体式生产和储存船。该计划预计于 2025 年投入运作。此计划得益于 Cerulean Winds 透过浮体式海上风电示范计画获得的津贴。

因此,在英国政府的帮助下及其雄心勃勃的离岸风力发电计画下,英国有望成为全球浮体式海上风电市场的主导国家。

欧洲浮体式海上风电产业概况

欧洲浮体式海上风电市场适度细分。市场的主要企业(不分先后顺序)是 Equinor ASA、通用电气公司、西门子歌美飒可再生能源、BW Ideol SA 和 Vestas Wind Systems AS。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究范围

- 市场定义

- 调查前提

第 2 章执行摘要

第三章调查方法

第四章 市场概况

- 介绍

- 2027年浮体式海上风电潜在装置容量设置容量预测(单位:MW)

- 2021年离岸风力发电产能预测(单位:MW)

- 最新趋势和发展

- 政府法规和政策

- 市场动态

- 驱动程式

- 限制因素

- 供应链分析

- 波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争强度

第五章 市场区隔

- 依深度(仅定性分析)

- 浅水(深度30公尺或以下)

- 过渡深度(30-60公尺)

- 深海(深度60公尺以上)

- 地区

- 英国

- 挪威

- 法国

- 丹麦

- 欧洲其他地区

第六章 竞争格局

- 併购、合资、合作与协议

- 主要企业策略

- 公司简介

- Equinor ASA

- General Electric Company

- Siemens Gamesa Renewable Energy

- BW Ideol SA

- Vestas Wind Systems AS

- Renexia

- Saitec Offshore Technologies

- Orsted A/S

- Repsol SA

- Falck Renewables SpA

第七章 市场机会与未来趋势

The Europe Floating Offshore Wind Power Market is expected to register a CAGR of 72.8% during the forecast period.

The market was negatively impacted by COVID-19 in 2020. Presently, the market has reached pre-pandemic levels.

Over the long term, the growing demand for offshore wind power is expected to stimulate the market growth of the Europe floating offshore wind power market. Furthermore, increasing the water depth of offshore wind power projects is considered a game-changing technology to exploit abundant wind potential in deeper waters and is also expected to drive the growth of the market studied.

On the other hand, the adoption of alternate sources of clean power generation, mainly gas and solar power, is increasing. As power generation from solar and gas resources are cleaner modes of energy production, the growing adoption of the same is expected to hamper the demand for wind power.

Nevertheless, the growing interest in offshore wind energy from developing and untapped markets is expected to create lucrative growth opportunities for the European floating offshore wind power market in the forecast period.

The United Kingdom is expected to dominate the market. It is also expected to witness the highest CAGR during the forecast period. This growth is attributed to the increasing investments coupled with the adoption of government policies.

Europe Floating Offshore Wind Power Market Trends

Government Policies and Private Investments in Floating Offshore Wind Power

Offshore wind is seen as a key new industry offering a potential transition for Norway's dominant oil and gas sector to a renewable energy future. In December 2020, the Norwegian Minister of Petroleum and Energy announced a new wind power research center in Norway. The NorthWind research center will focus on innovations, and one of its main priorities will be offshore wind power research.

However, Norway has faced local opposition to onshore wind power projects based on the perceived impact on landscapes and ecology. Accordingly, in May 2022, Norway unveiled plans for a major expansion in offshore wind energy by 2040, aiming to turn a country that has built its wealth on oil and gas into an exporter of renewable electricity. The government, which has come under fire from environmentalists for continuing to support the oil and gas industry, set a target to develop 30 gigawatts (GW) of offshore wind capacity by 2040.

Several companies are already lining up to participate in Norway's effort, looking to expand their own offshore wind ambitions and showcase new technology that draws on the experience with the oil and gas exploration industry.

For instance, Shell and BP are among the companies with an interest in Norwegian installations, along with Eni, Equinor, and Orsted. Vattenfall and Norway's Seagust also announced that they had formed a joint venture to bid in the auction. EDF Renewables declared that it had partnered with Deep Wind Offshore, a Norwegian independent power producer, to participate in the process in December 2021.

The floating offshore wind power market in France is one of the largest in the world. The country also showcased its interest to install 50 offshore wind farms by 2050, with a total capacity of 40 GW, and to slow down the development of onshore wind power. As part of the process of increasing the offshore wind capacity, the government of France launched the competitive tendering procedure for the development of two 250 MW floating offshore wind farms in the Mediterranean Seain in March 2022. The first wind farm will be located off Narbonne, more than 22 km from the coast, while the second wind farm is located 22 km off Fos-sur-Mer, subject to the results of ongoing environmental studies.

According to Wind Energy Ireland's (WEI) most recent developer survey carried out in Q1 2021, there are approximately 3 GW of floating offshore wind energy projects in the early stages of development in the Celtic Sea. An additional 5 GW of floating offshore wind energy projects are proposed for the Atlantic. For instance, in June 2022, the Killybegs Fishermen's Organization and Sinbad Marine Services proposed a floating wind farm to be built offshore Donegal, Ireland. They signed a Memorandum of Understanding with Swedish floating wind developer and technology provider, Hexicon.

As of 2021, there were 17.4 GW of new wind installations in Europe, with 14 GW onshore and 3.4 GW offshore. As 2021 marks a record year for wind installations (surpassing 2017's 17.1 GW figure), the EU-27 will need to install 32 GW of wind capacity each year in order to achieve the 40% renewable energy target.

With great access to offshore wind resources in the region and support from the various country governments, Europe is anticipated to be one of the biggest markets for floating offshore wind energy during the forecast period.

United Kingdom to Dominate the Market Growth

The United Kingdom is one of the world's largest markets for offshore wind power, with more than 10 GW of cumulative installed capacity across 38 sites as of 2021. There is a further 5 GW in pre-construction, and there are plans for a further 11 GW.

According to WindEurope, in 2021, the United Kingdom had 2.6 GW of offshore installations, accounting for 88% of Europe's offshore installations. The completion of the Moray East and Triton Knoll wind farms primarily drove offshore installations. Despite a slight increase in onshore installations in the United Kingdom, they remain the second lowest since 2005.

The growth of the sector was encouraged by the United Kingdom's target of 40 GW of offshore wind energy by 2030, as stated in the Ten Point Plan for a Green Industrial Revolution. This includes 1 GW generated by floating technologies. This ambition was increased through the British Energy Security Strategy (BESS), published in April 2022, which aims to achieve up to 50 GW of offshore wind by 2030, of which floating offshore wind would contribute 5 GW.

As part of the plan to net zero, the Scottish government has set a target to deliver up to 11 GW of offshore wind capacity by 2030 to support Scotland's commitment to net zero emissions by 2045. Scotland is home to the world's first commercial floating offshore wind project, Equinor/Masdar's Hywind Scotland wind farm, which used 5 SGRE 6 MW turbines, commissioned in 2017.

In August 2022, Cerulean Winds and Ping Petroleum UK signed an agreement on offshore oil and gas facilities powered mainly by offshore wind. Under the agreement, Cerulean Winds, with its consortium of Tier 1 industrial partners, will provide a large floating offshore wind turbine that will be connected via a cable to Ping Petroleum's Floating Production & Storage vessel. The project is expected to come online in 2025. The project was enabled by a grant to Cerulean Winds through the Floating Offshore Wind Demonstration Program.

Therefore, with the help of the UK government and its ambitious plans for the offshore wind segment, the United Kingdom is predicted to be a dominant country in the floating offshore wind power market worldwide.

Europe Floating Offshore Wind Power Industry Overview

The European floating offshore wind power market is moderately fragmented. Some of the major players in the market (in no particular order) are Equinor ASA, General Electric Company, Siemens Gamesa Renewable Energy, BW Ideol SA, and Vestas Wind Systems AS.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Floating Offshore Wind Power Potential Installed Capacity Forecast in MW, until 2027

- 4.3 Offshore Wind Energy Installed Capacity in MW, until 2021

- 4.4 Recent Trends and Developments

- 4.5 Government Policies and Regulations

- 4.6 Market Dynamics

- 4.6.1 Drivers

- 4.6.2 Restraints

- 4.7 Supply Chain Analysis

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Consumers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitute Products and Services

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Water Depth (Qualitative Analysis Only)

- 5.1.1 Shallow Water ( less than 30 m Depth)

- 5.1.2 Transitional Water (30 m to 60 m Depth)

- 5.1.3 Deep Water (higher than 60 m Depth)

- 5.2 Geography

- 5.2.1 United Kingdom

- 5.2.2 Norway

- 5.2.3 France

- 5.2.4 Denmark

- 5.2.5 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Equinor ASA

- 6.3.2 General Electric Company

- 6.3.3 Siemens Gamesa Renewable Energy

- 6.3.4 BW Ideol SA

- 6.3.5 Vestas Wind Systems AS

- 6.3.6 Renexia

- 6.3.7 Saitec Offshore Technologies

- 6.3.8 Orsted A/S

- 6.3.9 Repsol SA

- 6.3.10 Falck Renewables SpA

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

2026年全球浮体式海上电市场报告2026年全球浮体式海上风力发电市场报告

2026年全球浮体式海上电市场报告2026年全球浮体式海上风力发电市场报告 浮体式海上风电市场-2026-2031年预测

浮体式海上风电市场-2026-2031年预测 全球浮体式海上风电系统市场:预测至2032年-按组件、平台类型、风扇容量、水深、轴线、应用、最终用户及地区进行分析

全球浮体式海上风电系统市场:预测至2032年-按组件、平台类型、风扇容量、水深、轴线、应用、最终用户及地区进行分析 海上漂浮式风电:全球市场份额和排名、总收入和需求预测(2025-2031年)

海上漂浮式风电:全球市场份额和排名、总收入和需求预测(2025-2031年) 浮体式海上风电市场按组件、涡轮机容量、水深、技术、应用和发展阶段划分-2025-2032年全球预测

浮体式海上风电市场按组件、涡轮机容量、水深、技术、应用和发展阶段划分-2025-2032年全球预测 全球浮体式海上风力发电市场

全球浮体式海上风力发电市场 浮体式海上风电:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年)

浮体式海上风电:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年) 浮动离岸风电市场-全球产业规模、份额、趋势、机会和预测,按水深(浅水、过渡水域和深水)、按涡轮机容量、按地区、按竞争细分,2020-2030 年

浮动离岸风电市场-全球产业规模、份额、趋势、机会和预测,按水深(浅水、过渡水域和深水)、按涡轮机容量、按地区、按竞争细分,2020-2030 年 浮动离岸风能市场机会、成长动力、产业趋势分析及2025-2034年预测

浮动离岸风能市场机会、成长动力、产业趋势分析及2025-2034年预测