|

市场调查报告书

商品编码

1644979

德国太阳能逆变器:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)Germany Solar Inverter - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

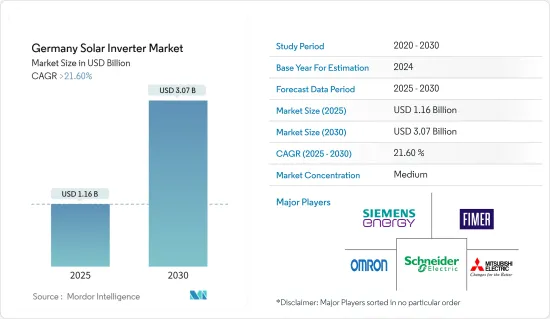

预计 2025 年德国太阳能逆变器市场规模为 11.6 亿美元,到 2030 年将达到 30.7 亿美元,预测期内(2025-2030 年)的复合年增长率将超过 21.6%。

主要亮点

- 从中期来看,商业和工业领域越来越多地采用太阳能以及对太阳能计划的投资增加等因素预计将推动市场的发展。

- 另一方面,欧洲地区政府最近削减了太阳能电池板的补贴,预计将在研究期间阻碍市场的成长。

- 话虽如此,许多逆变器製造商正在努力创新和采用由太阳能动力来源的最新技术。预计这一因素将在不久的将来为德国太阳能逆变器市场创造巨大的机会。

德国太阳能逆变器市场趋势

集中式逆变器市场预计将占据市场主导地位

- 集中逆变器是大电网供电设备。它常用于额定输出功率超过100kWp的太阳能发电系统。落地式或地面安装的逆变器将从太阳能电池阵列收集的直流电转换为交流电以用于并联型。这些设备的容量范围从大约 50kW 到 1MW,可在室内和室外使用。

- 中央逆变器用于公共事业规模的应用,因此必须与其所使用的电网的电压和频率相符。由于世界各地的电网标准差异很大,製造商可以自订这些参数以满足他们的特定要求,例如相数。

- 根据国际可再生能源机构(IRENA)预测,到2022年12月底,日本太阳能发电装置容量将达到5,872.6万千瓦。

- 此外,还有多家公司联合起来推动集中式逆变器的使用。例如,2022年5月,Gamesa Electric与西门子股份公司签署了一项策略伙伴关係协议,针对光伏和能源储存计划采用中央逆变器Proteus。根据该协议,西门子将能够在其光伏和BESS计划中使用Gamesa Electric的Proteus逆变器。这些中央逆变器具有高达 4700kVA 的高功率和 99.45% 的创纪录效率,为太阳能和储能计划提供了整合解决方案。

- 2022年1月,阳光电源推出全新「1+X」集中模组化逆变器,输出容量为1.1MW。本款1+X模组化逆变器可组合成8台单元,达到8.8MW的输出功率,并配备DC/ESS接口,可连接能源储存系统(ESS)。

- 因此,由于上述电力需求增加等因素,预计中央逆变器领域将占据市场主导地位。

太阳能计划投资增加推动市场

- 以装置容量容量计算,德国是欧洲最大的太阳能光电市场,确立了其作为全球能源和气候安全领跑者之一的地位。该国太阳能发电市场正在快速发展。由于上网电价和自用电相结合的吸引力,这一趋势可能会持续下去,特别是对于 40kW 至 750kW 的大中型商业系统而言。

- 德国光伏累积设置容量正在大幅成长。 2022年太阳能发电装置容量达6,650万千瓦,2021年达5,870万千瓦。 2022年与前一年同期比较增长13.2%。

- 在太阳能领域,人们正在进行大量投资来建立新的太阳能计划。例如,2022年3月,德国表示打算在可再生能源领域投资2,160亿美元,减少对易受乌克兰衝突影响的俄罗斯天然气的依赖。

- 此外,2022 年 4 月,德国联邦网路局宣布,在太阳能光电竞标中已授予 201 份提案,总合容量为 108.4 吉瓦,高于 2021 年 7 月的 510.34 兆瓦。竞标价格范围为每千瓦时 0.040 欧元至 0.055 欧元。数量加权平均价格为每千瓦时 0.0519 欧元(0.057 美元),高于先前的 0.050 欧元。

- 此外,2022年7月,德国同意政府提出的设立专案「气候变迁和转型基金」的建议,该基金将在未来四年内投资1,800亿美元,用于推动向不依赖俄罗斯能源来源的清洁经济的能源提案。

- 截至2022年10月,德国拥有超过258万座太阳能发电厂。该数字代表了审查期间记录的站点峰值数量。

- 考虑到以上所有因素,预计该国太阳能市场的投资将会增加,并很快占领德国太阳能逆变器市场。

德国光电逆变器产业概况

德国的光电逆变器市场减少了一半。市场的主要企业(不分先后顺序)包括 FIMER SpA、施耐德电气 SE、西门子能源股份公司、三菱电机株式会社和Omron Corporation。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究范围

- 市场定义

- 调查前提

- 调查结果

第 2 章执行摘要

第三章调查方法

第四章 市场概况

- 介绍

- 2028 年市场规模与需求预测(美元)

- 最新趋势和发展

- 政府法规和政策

- 市场动态

- 驱动程式

- 商业和工业领域越来越多地采用太阳能

- 增加对太阳能计划的投资

- 限制因素

- 欧洲政府近期削减太阳能板补贴

- 驱动程式

- 供应链分析

- PESTLE分析

第五章 市场区隔

- 按逆变器类型

- 集中式逆变器

- 组串式逆变器

- 微型逆变器

- 按应用

- 住宅

- 商业和工业

- 公共事业规模

第六章 竞争格局

- 併购、合资、合作与协议

- 主要企业策略

- 公司简介

- FIMER SpA

- Schneider Electric SE

- Siemens Energy AG

- Mitsubishi Electric Corporation

- General Electric Company

- SMA Solar Technology AG

- Omron Corporation

- Delta Energy Systems Inc.

- Huawei Technologies Co. Ltd.

- KACO New Energy GmbH

第七章 市场机会与未来趋势

- 创新并采用利用太阳能的最新技术

简介目录

Product Code: 5000152

The Germany Solar Inverter Market size is estimated at USD 1.16 billion in 2025, and is expected to reach USD 3.07 billion by 2030, at a CAGR of greater than 21.6% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, factors such as the growing adoption of solar PV in commercial and industrial sectors and increasing investments in solar energy projects are expected to drive the market.

- On the other hand, the recent subsidy cuts on solar panels by governments in the Europe region is expected to hinder the market growth during the study period.

- Nevertheless, Many inverter manufacturers strive for innovation and adoption of the latest technologies powered by solar energy. This factor is expected to create immense opportunities for Germany's solar inverter market in the near future.

Germany Solar Inverter Market Trends

Central Inverters Segment Expected to Dominate the Market

- A central inverter is a large grid feeder. It is often used in solar photovoltaic systems with rated outputs over 100 kWp. Floor or ground-mounted inverters convert DC power collected from a solar array into AC power for grid connection. These devices range in capacity from around 50kW to 1MW and can be used indoors or outdoors.

- As central inverters are used for utility-scale applications, they should produce the same voltage and frequency as that of the electric grid where they are used. As there are a lot of different electric grid standards worldwide, manufacturers are allowed to customize these parameters to match the specific requirements in terms of the number of phases; most central inverters manufactured are three-phase inverters.

- Acoriding to International Renewable Energy Agency (IRENA), by the end of December 2022, the country will have 58.726 GW of solar PV capacity.

- Moreover, to promote the utilization of central inverters, several companies collaborated. For instance, In May 2022, Gamesa Electric and Siemens AG signed a strategic partnership agreement addressing the employment of its Proteus central inverters for PV and Energy Storage projects. Under this agreement, Siemens could use Gamesa Electric Proteus inverters for PV and BESS projects. These central inverters are distinguished by their high-power output of up to 4700kVA and a record efficiency of 99.45%, providing integrated solutions for solar and storage projects.

- In January 2022, Sungrow launched its new '1+X' central modular inverter with an output capacity of 1.1MW. This 1+X modular inverter can be combined into eight units to reach a power of 8.8MW and features a DC/ESS interface for connecting energy storage systems (ESS).

- Therefore, the Central Inverters Segment is expected to dominate the market based on the above factors, like increased power demand.

Increasing Investments in Solar Energy Projects to Drive the Market

- Germany is the largest solar photovoltaic market in Europe in terms of installed capacity, which justifies it being one of the front runners in energy and climate security globally. The country has witnessed significant developments in the solar PV market. It will likely continue to do so due to a combination of self-consumption with attractive feed-in premiums, especially for medium- to large-scale commercial systems ranging from 40 kW to 750 kW.

- The cumulative solar photovoltaic installed capacity in Germany has witnessed significant growth. The solar PV installed capacity will be 66.5 GW in 2022 and 58.7 GW in 2021. There has been 13.2 % year-on-year growth in 2022 compared to the previous year.

- Significant investments in the solar energy sector are being made to set up new solar energy projects. For instance, In March 2022, Germany intends to invest USD 216 billion in renewable energy to reduce its reliance on Russian gas, which has left it susceptible to the effects of the conflict in Ukraine.

- Additionally, in April 2022, Germany's Federal Network Agency announced that the agency had selected 201 proposals with a combined output of 1.084 GW under the solar auction, up from 510.34 MW in July 2021. The bids in the round ranged from EUR 0.040 to EUR 0.055 per kWh. The volume-weighted average price stood at EUR 0.0519 (USD 0.057) per kWh, up from EUR 0.050 per kWh in the previous round.

- Furthermore, in July 2022, Germany agreed on proposals for the government's special "climate and transformation fund" to invest USD 180 billion over the following four years to expedite the energy shift to a cleaner economy and less reliant on Russian energy sources.

- As of October 2022, Germany was home to over 2.58 million energy-generating solar photovoltaic sites. This figure illustrates the peak number of sites recorded in the period of consideration.

- Owing to the above points, increasing investments in the country's solar energy market are expected to dominate the Germany solar inverter market soon.

Germany Solar Inverter Industry Overview

The Germany solar PV inverters market is semi-fragmented. Some of the major players in the market (in no particular order) include FIMER SpA, Schneider Electric SE, Siemens Energy AG, Mitsubishi Electric Corporation, and Omron Corporation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

- 1.4 Study Deliverables

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2028

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Growing Adoption of Solar PV in Commercial and Industrial Sectors

- 4.5.1.2 Increasing Investments in Solar Energy Projects

- 4.5.2 Restraints

- 4.5.2.1 Recent Subsidy Cuts on Solar Panels by Governments in the Europe Region

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 PESTLE Analysis

5 MARKET SEGMENTATION

- 5.1 Inverter Type

- 5.1.1 Central Inverters

- 5.1.2 String Inverters

- 5.1.3 Micro Inverters

- 5.2 Application

- 5.2.1 Residential

- 5.2.2 Commercial and Industrial

- 5.2.3 Utility-Scale

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 FIMER SpA

- 6.3.2 Schneider Electric SE

- 6.3.3 Siemens Energy AG

- 6.3.4 Mitsubishi Electric Corporation

- 6.3.5 General Electric Company

- 6.3.6 SMA Solar Technology AG

- 6.3.7 Omron Corporation

- 6.3.8 Delta Energy Systems Inc.

- 6.3.9 Huawei Technologies Co. Ltd.

- 6.3.10 KACO New Energy GmbH

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Innovation and Adoption of the Latest Technologies Powered by Solar Energy

02-2729-4219

+886-2-2729-4219

太阳能逆变器测试解决方案市场:按应用、逆变器类型、输出额定值和测试类型划分,全球预测(2026-2032年)

太阳能逆变器测试解决方案市场:按应用、逆变器类型、输出额定值和测试类型划分,全球预测(2026-2032年) 太阳能逆变器市场机会、成长要素、产业趋势分析及2026年至2035年预测。

太阳能逆变器市场机会、成长要素、产业趋势分析及2026年至2035年预测。 太阳能逆变器:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

太阳能逆变器:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 2026-2034年全球商用和工业用太阳能逆变器市场规模、份额、趋势和成长分析报告全球太阳能微型逆变器市场规模、份额、趋势和成长分析报告(2026-2034年)

2026-2034年全球商用和工业用太阳能逆变器市场规模、份额、趋势和成长分析报告全球太阳能微型逆变器市场规模、份额、趋势和成长分析报告(2026-2034年) 日本太阳能逆变器市场规模、份额、趋势和预测:按逆变器类型、应用和地区划分,2026-2034年

日本太阳能逆变器市场规模、份额、趋势和预测:按逆变器类型、应用和地区划分,2026-2034年 2026年全球住宅太阳能逆变器市场报告2026年全球太阳能逆变器市场报告2026年全球太阳能逆变器市场报告太阳能逆变器外壳市场:按逆变器类型、外壳材料、冷却方式、安装方式和应用划分 - 全球预测(2026-2032 年)

2026年全球住宅太阳能逆变器市场报告2026年全球太阳能逆变器市场报告2026年全球太阳能逆变器市场报告太阳能逆变器外壳市场:按逆变器类型、外壳材料、冷却方式、安装方式和应用划分 - 全球预测(2026-2032 年)

▼