|

市场调查报告书

商品编码

1645099

建筑用可携式发电机:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)Construction Portable Generators - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

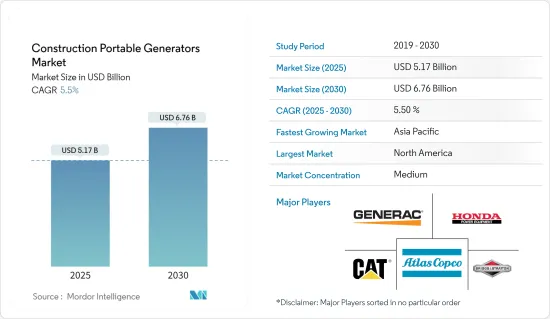

预计 2025 年建筑可携式发电机市场规模为 51.7 亿美元,预计到 2030 年将达到 67.6 亿美元,预测期内(2025-2030 年)的复合年增长率为 5.5%。

从中期来看,不断增长的电力需求、缺乏可靠的电网基础设施、对紧急备用电源解决方案的需求以及对建筑工地稳定电源的需求等因素正在推动可携式发电机市场的发展。

另一方面,可携式发电机面临来自电池储存系统的激烈竞争。此外,其他更干净的电力源预计也会阻碍可携式发电机市场的发展。

预计新兴经济体商业和工业领域的新建筑以及住宅领域的新建筑将在不久的将来为市场参与企业提供重大商机。

预计北美将占据主要市场占有率,大部分需求来自美国和印度等国家。

建筑可携式发电机的市场趋势

10KW以上将成为重要细分市场

- 可携式发电机对于建筑业来说至关重要。承包商经常会遇到施工现场缺乏电力服务或停电的情况,这意味着他们必须使用可携式照明设备。由于多种因素,预计未来几年建筑业可携式发电机市场将大幅成长。首先,市场受到全球对基础设施开发和建设活动日益增长的需求的推动。

- 工地使用10kVA以上的柴油发电机来持续供电。建筑工地需要它为起重机和挖掘机等重型机械提供动力,并运行必要的工具。

- 此外,停电变得越来越频繁,特别是在新兴国家,从而推动了对可携式发电机的需求。电网电力不稳定,需要使用可携式发电机来防止工作中断。

- 2023年2月,卡特彼勒宣布推出搭载Cat C9.3B柴油引擎的XQ330可携式柴油发电机。它还具有几个适合租赁的功能,包括电池充电器、引擎加热器、可切换电压输出、永磁发电机 (PMG) 和拖车安装选项。

- 此外,近年来美国的建筑支出一直稳定成长。 2023年,住宅和住宅建筑支出也在增加。环保建筑实践趋势也促进了市场的成长。建设公司越来越多地转向运作生物柴油和天然气等替代燃料的可携式发电机,以减少排放气体和环境影响。

- 由于这些因素,预计未来几年该领域将占据相当大的市场占有率。

北美占据主要市场占有率

- 2023年,美国的电力消耗量约为4,000兆瓦时。儘管电网基础设施复杂,全国电力供应充足,但停电和备用电源需求增加等问题预计将推动该国备用发电市场的需求。停电每年平均给该国造成约 180 亿至 330 亿美元的损失。因此,备用发电机或UPS被认为是保持业务运作不间断的最可行选择。

- 此外,由于激进的货币紧缩政策导致房屋抵押贷款利率上升,且高通膨持续影响住宅承受能力,预计住宅建筑业将出现最大萎缩。不过,由于政府的奖励策略,非住宅建筑仍保持强劲。 《基础设施投资与就业促进法案》旨在对老化的基础设施(道路、高速公路、桥樑、铁路、宽频开发等)进行全面投资,预计将在今年刺激建设。随着住宅领域建设的增加,建筑用可携式发电机的市场利用率预计也将增加。

- 截至 2024 年,美国等国家已计划在非住宅领域实施多个建设计划。例如,戈迪豪国际大桥、Brightline West高速铁路和加州高速铁路等计划是即将实施的一些重大计划,这些项目可能会在建筑工地产生对可携式发电机的需求。

- 截至2023年,美国是世界上最大的资料中心建设国家之一。主要市场包括纽约和芝加哥的金融中心,湾区(旧金山)、西雅图和波特兰的科技中心,达拉斯和洛杉矶的人口中心,以及华盛顿特区/维吉尼亚的政府中心。美国的资料中心总数是距离最近的市场(英国)的5倍多,美国也是无可争议的「网路之乡」。随着资料中心建设的不断增加,市场成长预计将在不久的将来达到顶峰。

- 鑑于上述情况,由于美国、加拿大和墨西哥的住宅和工业建设不断增加,预计北美将占据市场主导地位。

可携式建筑发电机行业概况

建筑可携式发电机市场较为分散。市场的主要企业包括 Generac Holdings Inc.、Caterpillar Inc.、Honda Siel Power Products Ltd.、Briggs & Stratton Corporation 和 Atlas Copco AB。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究范围

- 市场定义

- 调查前提

第二章调查方法

第三章执行摘要

第四章 市场概况

- 介绍

- 2029 年市场规模与需求预测(十亿美元)

- 最新趋势和发展

- 政府法规和政策

- 市场动态

- 驱动程式

- 可携式电源需求不断增长

- 增加全球建筑业的投资

- 限制因素

- 对电池储存系统和其他清洁备用电力源的需求不断增加

- 驱动程式

- 供应链分析

- 波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 投资分析

第五章 市场区隔

- 额定功率

- 小于5KW

- 5~10KW

- 10KW以上

- 燃料类型

- 气体

- 柴油引擎

- 其他燃料

- 地区

- 北美洲

- 美国

- 加拿大

- 北美其他地区

- 欧洲

- 德国

- 法国

- 英国

- 西班牙

- 北欧的

- 土耳其

- 俄罗斯

- 欧洲其他地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 马来西亚

- 泰国

- 印尼

- 越南

- 其他亚太地区

- 南美洲

- 巴西

- 阿根廷

- 哥伦比亚

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 南非

- 埃及

- 奈及利亚

- 卡达

- 其他中东和非洲地区

- 北美洲

第六章 竞争格局

- 併购、合资、合作与协议

- 主要企业策略

- 公司简介

- Generac Holdings Inc.

- Caterpillar Inc.

- Honda Siel Power Products Ltd.

- Briggs & Stratton Corporation

- Kohler Power Systems

- Wacker Neuson SE

- Atlas Copco AB

- Eaton Corporation PLC

- Yamaha Motor Co. Ltd.

- 市场排名/份额(%)分析

- 其他知名公司名单

第七章 市场机会与未来趋势

- 新兴国家不断成长的商业和工业部门

The Construction Portable Generators Market size is estimated at USD 5.17 billion in 2025, and is expected to reach USD 6.76 billion by 2030, at a CAGR of 5.5% during the forecast period (2025-2030).

Over the medium term, factors such as the ever-increasing demand for power, lack of reliable grid infrastructure, the need for emergency backup power solutions, and the demand for steady power supply at construction sites are driving the portable generator market.

On the other hand, Portable generators face tough competition from battery storage systems. Also, other cleaner sources of standby power are expected to hinder the portable generators market.

Nevertheless, the new constructions in the commercial and industrial sectors of emerging economies and the residential sector of developed economies are expected to create significant opportunities for market participants in the near future.

North America is expected to have a significant market share, with the majority of the demand coming from countries such as the United States and India.

Construction Portable Generators Market Trends

Above 10 KW to be a Significant Market Segment

- Portable power generators are an essential part of the construction industry. In many situations, contractors may find themselves at job sites where the lack of electrical service or power failures requires them to utilize portable lighting units. The portable generator market in the construction industry is expected to witness substantial growth in the coming years due to several factors. Firstly, the growing demand for infrastructure development and construction activities across the globe is driving the market.

- The above 10 kVA diesel generators are used at construction sites for continuous power supply. Construction sites are vital for powering heavy machinery, such as cranes and excavators, and for running essential tools.

- Additionally, the increasing frequency of power outages, especially in developing countries, is boosting the demand for portable generators. Unreliable grid power necessitates the use of portable generators to ensure uninterrupted work progress.

- In February 2023, Caterpillar announced the launch of the XQ330 portable diesel generator powered by the Cat C9.3B diesel engine. It is also equipped with several rental-ready features, including a battery charger, block heater, switchable voltage outputs, permanent magnet generator (PMG), and optional mounting on a trailer.

- Furthermore, construction spending has grown steadily in the United States over the last couple of years. Up to 2023, residential building construction spending and non-residential construction also increased. The rising trend of green construction practices also contributes to market growth. Construction companies are increasingly adopting portable generators that run on alternative fuels, such as biodiesel and natural gas, to reduce emissions and environmental impact.

- Thus, owing to such factors, the segment is expected to have a significant market share in the coming years.

North America to Have a Significant Market Share

- In 2023, the electricity consumption in the United States was about 4000 terawatt-hours. Despite the presence of a complex electricity grid infrastructure and 100% electricity access across the country, problems like power outages and increasing demand for standby power sources are expected to drive the demand for the backup power generation market in the country. Power outages cost an average of about USD 18 billion to USD 33 billion per year in the country. Therefore, backup generators and UPS are considered the most viable options for making business operations run continuously without any interruption.

- Moreover, It is expected that the residential building segment will see the largest contraction because aggressive monetary tightening is feeding into higher mortgage rates, and high inflation weighs on the affordability of homeownership. However, non-residential construction remains more resilient due to government stimulus. The Infrastructure Investment and Jobs Act will provide a stimulus for construction this year, aiming at comprehensive investments in aging infrastructure (including roads, highways, bridges, rail, and broadband development). The growing residential sector constructions will, in turn, culminate in the growth in the utilization of construction portable generators in the market.

- As of 2024, countries like the United States have several upcoming construction projects in the non-residential sector. For instance, projects like Gordie Howe International Bridge, Brightline West High-Speed Rail, and California High-Speed Rail are a few significant upcoming projects, which are likely to create demand for portable generators in the construction sites.

- As of 2023, the United States was one of the largest countries in the world for the construction of data centers. Major markets include the financial hubs of New York and Chicago, the tech hubs of the Bay Area (San Francisco), Seattle, and Portland, the population hubs of Dallas and Los Angeles, and the center of Government in Washington DC/Virginia. With the country's total data center numbers outweighing its nearest market (the United Kingdom) by five times, the United States is also the undisputed "home of the internet. The growing construction of data centers will culminate in the market's growth in the near future.

- Owing to the above points, with the increase in residential and industrial construction in the United States, Canada, and Mexico, North America is expected to dominate the market.

Construction Portable Generators Industry Overview

The Construction Portable Generators Market is fragmented. Some of the major companies operating in the market include Generac Holdings Inc., Caterpillar Inc., Honda Siel Power Products Ltd, Briggs & Stratton Corporation, and Atlas Copco AB.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD billion, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increasing Demand for portable power source

- 4.5.1.2 Increasing investments in Construction Sector across the Globe

- 4.5.2 Restraints

- 4.5.2.1 Increasing Demand for Battery Storage Systems and other Cleaner Sources of Standby Power

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Power Rating

- 5.1.1 Below 5 KW

- 5.1.2 5-10 KW

- 5.1.3 Above 10 KW

- 5.2 Fuel Type

- 5.2.1 Gas

- 5.2.2 Diesel

- 5.2.3 Other Fuel Types

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 France

- 5.3.2.3 United Kingdom

- 5.3.2.4 Spain

- 5.3.2.5 NORDIC

- 5.3.2.6 Turkey

- 5.3.2.7 Russia

- 5.3.2.8 Rest of Europe

- 5.3.3 Asia Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Malaysia

- 5.3.3.6 Thailand

- 5.3.3.7 Indonesia

- 5.3.3.8 Vietnam

- 5.3.3.9 Rest of Asia Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 South Africa

- 5.3.5.4 Egypt

- 5.3.5.5 Nigeria

- 5.3.5.6 Qatar

- 5.3.5.7 Rest of Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Generac Holdings Inc.

- 6.3.2 Caterpillar Inc.

- 6.3.3 Honda Siel Power Products Ltd.

- 6.3.4 Briggs & Stratton Corporation

- 6.3.5 Kohler Power Systems

- 6.3.6 Wacker Neuson SE

- 6.3.7 Atlas Copco AB

- 6.3.8 Eaton Corporation PLC

- 6.3.9 Yamaha Motor Co. Ltd.

- 6.4 Market Ranking/Share (%) Analysis

- 6.5 List of Other Prominent Companies

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing Commercial and Industrial Sectors of Emerging Economies

发电机维护服务市场:按服务类型、发电机类型、维护频率、服务提供者和最终用户划分 - 全球预测 2026-2032 年发电机市场:2026年至2032年全球预测(依产品类型、额定输出功率、相数、冷却方式及应用划分)

发电机维护服务市场:按服务类型、发电机类型、维护频率、服务提供者和最终用户划分 - 全球预测 2026-2032 年发电机市场:2026年至2032年全球预测(依产品类型、额定输出功率、相数、冷却方式及应用划分) 发电机市场规模、份额和成长分析:按类型、额定功率、最终用户和地区划分-2026-2033年产业预测

发电机市场规模、份额和成长分析:按类型、额定功率、最终用户和地区划分-2026-2033年产业预测 全球发电机市场规模、份额、趋势和成长分析报告(2026-2034年)全球黑启动发电机市场规模、份额、趋势和成长分析报告(2026-2034年)

全球发电机市场规模、份额、趋势和成长分析报告(2026-2034年)全球黑启动发电机市场规模、份额、趋势和成长分析报告(2026-2034年) 日本发电机市场:规模、份额、趋势和预测:按燃料类型、输出功率、销售管道、设计、应用、最终用户和地区划分(2026-2034 年)

日本发电机市场:规模、份额、趋势和预测:按燃料类型、输出功率、销售管道、设计、应用、最终用户和地区划分(2026-2034 年) 2026年全球军用发电机市场报告2026年全球发电机市场报告2026年全球发电机销售市场报告

2026年全球军用发电机市场报告2026年全球发电机市场报告2026年全球发电机销售市场报告 中速大型发电机市场 - 全球产业规模、份额、趋势、机会及预测(按技术、功率输出、燃料类型、最终用户、地区和竞争格局划分,2021-2031年)

中速大型发电机市场 - 全球产业规模、份额、趋势、机会及预测(按技术、功率输出、燃料类型、最终用户、地区和竞争格局划分,2021-2031年)