|

市场调查报告书

商品编码

1683119

光电产业市场 -市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Photonics Industry - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

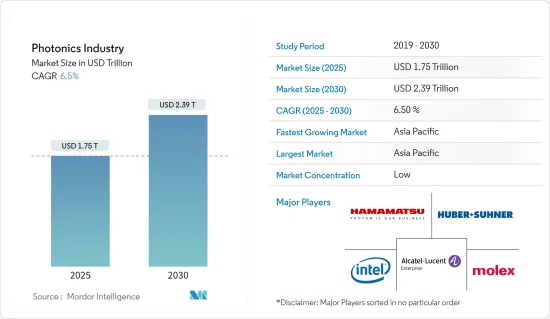

光电产业预计将从 2025 年的 1.75 兆美元成长到 2030 年的 2.39 兆美元,预测期内(2025-2030 年)的复合年增长率为 6.5%。

光电涉及辐射能(如光),其基本元素是光子和波,可以治疗疾病、探勘宇宙甚至破案。光电涉及光和其他电磁辐射的产生、操纵、传输、检测和利用。光电被广泛认为是开发智慧系统的一项必不可少的技术,该系统可以在不牺牲整体系统效率的情况下高效利用能源。医疗、汽车、通讯、製造和零售等许多行业都在利用这项技术来提高效率,从而推动工业成长。这些领域的投资近年来也呈现强劲成长。

关键亮点

- 光电是跨多个行业的核心技术,根据行业展望,该技术的消费正在快速增长,市场正在扩展到新的垂直领域。近年来,光电在雷射雷达和增材製造领域呈现日益增长的趋势。几十年来,光达一直被用来研究大气中气体和污染物的分布。近年来,它已成为自动驾驶必不可少的技术。 LiDAR 测绘系统及其支援技术的进步正在渗透到各个垂直领域,包括航太和国防、走廊测绘和地形测量、汽车、采矿以及石油和天然气,扩大了全球市场的覆盖范围。

- 在美国,Google、微软、Facebook等大公司引领光电市场,它们需要优化每个资料中心的资料传输流程。此外,该国为技术进步和扩张提供了良好的环境。此外,美国硅光电元件产业的重要资金筹措格局正在鼓励组织和新兴企业投资于不断扩大的光电市场。

- 此外,美国电脑协会发表的《深度学习中硅光子的调查》报导指出,深度学习在解决电脑视觉、自然语言处理和一般模式识别等领域的极其困难的问题方面表现出非凡的成功。这些成就是数十年来对更好的学习技术和更深的神经网路模型的研究以及用于训练和执行的深度神经网路硬体平台的开发的成果。近年来,用于深度学习的 ASIC(专用积体电路)硬体加速器备受关注,因为其中许多加速器比标准 CPU 和 GPU 设计具有更高的效能和能源效率。

- 根据产业分析报告,产业需要大量的初始投资来整合这些光电技术以实现自动化目的。自动化系统的高成本与有效、强大的硬体和高效的软体有关。自动化设备需要大量的资本投入才能实现智慧生产(安装、设计和建造自动化系统可能要花费数百万美元)。这导致各行各业依赖现有的低成本技术,从而难以采用。

- 产业分析报告强调,除了对光子解决方案的供应链和生产的直接影响外,疫情的后遗症也在影响市场成长。例如,包括美国在内的各个地区迫在眉睫的景气衰退威胁可能会对市场成长产生不利影响,因为经济不确定性将阻止消费者和企业在高价值产品上增加支出,这可能会影响所研究市场的成长率。

- COVID-19 疫情对整个半导体製造市场的需求和供应都产生了影响。此外,全球各地半导体工厂的停产、关闭,也加剧了供不应求的情况。其影响已在受调查的市场中反映出来。然而,许多影响都是短暂的。世界各国政府为支持汽车和半导体产业采取的预防措施有助于恢復工业成长。

光电产业趋势

消费终端用户产业细分市场占据主要市场占有率

- 光电用于多种消费设备,如条码扫描器、DVD参与企业、电视遥控器、电视和智慧型手机。条码扫描器常见于印表机、CD/DVD/蓝光设备和远端设备等消费性设备。条码扫描器在物流和供应链管理中发挥着至关重要的作用。透过扫描产品包装和运输标籤上的条码来追踪库存、管理存量基准并确保准确交货。

- 基于光电的条码扫描器用于物流应用中的包装分类。这些扫描器有助于根据条码资讯自动对包裹进行分类。它也广泛用于零售环境中的销售点交易、库存控制和价格验证。快速且准确地扫描产品条码可以提高效率和客户服务。

- 光电技术在DVD参与企业的运作中也扮演关键角色。 DVD参与企业在光碟机中使用光电技术,包括 CD、DVD、蓝光和高清参与企业和录影机。 DVD参与企业使用雷射在光碟上读取和写入资料。雷射二极体将狭窄的聚焦光束照射到光碟表面,从而实现精确的资料搜寻和记录。参与企业是参与企业,他们使用光电技术在DVD上读取和写入资料。来自雷射二极体的雷射光束与凹坑相互作用并撞击 DVD 表面,使参与企业能够提取储存的资讯。

- 根据美国消费者技术协会 (CTA) 和美国人口普查局的数据,美国智慧型手机销售额预计将从 2021 年的 730 亿美元增至 2022 年的 747 亿美元。此外,根据 GSMA 的数据,到 2025 年,北美智慧型手机用户数量预计将达到 3.28 亿。此外,到 2025 年,北美的行动用户数量 (86%) 和网路普及率 (80%) 可能会增加。行动电话需求的不断增长和行业趋势可能为所研究市场的成长提供有利的机会。

- 此外,美国人口普查局估计2022-2023年智慧型手机销售额将达747亿美元。这种放缓是由于美国智慧型手机出货量下降所造成的。在经济挑战、高通膨和季节性需求疲软的背景下,低阶智慧型手机销量下滑是导致销量下滑的最大因素。不过,预计未来几年这种情况将会消退。这些行业趋势预计将对智慧型手机相机镜头的成长产生重大影响。

亚太地区全球市场大幅成长

- 日本是亚洲的高科技强国。全球相机产业正在快速发展,日本一直是该市场的领导者和创新者。无反光镜混合相机、数位单眼相机和可更换镜头轻便型相机目前正在推动相机市场的发展,为市场研究创造了更多的机会。

- 日本有许多光电相关的大学和研究机构。例如,日本大阪大学的光子学先端研究中心(PARC)已成为日本领先的光电科学和工业研究中心。

- 由于亚太地区的经济成长和全球市场占有率,预计中国将在亚太国家中呈现强劲成长。中国是重要的电子产品生产国和消费国之一。该地区的製造业正在快速成长,并引进了一系列製造和通讯技术。

- 印度是世界上最大且成长最快的经济体之一。预计不断增强的购买力和社交媒体的影响力将推动电子产品市场的发展。政府正在做出许多努力以成为新兴经济体。印度电子和资讯技术部核准了各种数位计划,在预测期内创造了巨大的市场成长机会。

- 韩国是该市场的主要贡献者之一。人口成长、对硅光子产品开发的投资增加、国内外参与企业专注于开发最先进的硅光子产品、以及为提高该地区的资料传输速度而加强的研发活动都是推动市场成长的一些因素。

- 其他亚太市场包括印尼、新加坡和泰国。 5G、人工智慧、物联网、虚拟实境等新技术的快速发展和商业性应用,对资料处理和资讯互动的需求日益增加。这种情况可能会促进该地区资料中心的建设,从而带来该行业的爆炸性增长。

光电产业概况

光电行业市场高度分散,有许多大型参与者。其中主要参与者有滨松光子株式会社、英特尔公司、Polatis 公司(Huber+Suhner)、阿尔卡特朗讯公司(诺基亚公司)和 Molex 公司。市场主要参与者正在采用合作和收购等策略来加强其产品阵容并获得可持续的竞争优势。

- 2023 年 11 月—Innolume 宣布推出具有 1W 光输出的高功率 O 波段量子点 SOA。可用于 LiDAR、PON 和 FSO。

- 2023 年 9 月 - Ams OSRAM AG 与马来西亚投资发展局 (MIDA) 宣布相互支持在马来西亚继续投资和业务扩展。透过合作协议,MIDA 表达了对 Ams OSRAM AG 在马来西亚努力的大力支持。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概况

- 产业价值链分析

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 购买者/消费者的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争强度

- 新冠肺炎疫情和其他宏观经济因素的后续影响将影响市场

- 技术简介

第五章 市场动态

- 市场驱动因素

- 硅基光电应用的出现

- 越来越关注高效能、环保解决方案

- 市场限制

- 光电设备的初始成本高

第六章 市场细分

- 按最终用户产业

- 消费者

- 航太和国防

- 展示

- 太阳的

- LED 照明

- 医疗和生物测量

- 工业和製造业

- 车

- 其他的

- 按地区

- 北美洲

- 美国

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 欧洲其他地区

- 亚太地区

- 日本

- 中国

- 印度

- 台湾

- 韩国

- 其他亚太地区

- 其他的

- 北美洲

第七章 竞争格局

- Vendor Positioning Analysis

- 公司简介

- Hamamatsu Photonics KK

- Intel Corporation

- Polatis Incorporated(HUBER+SUHNER)

- Alcatel-lucent SA(Nokia Corporation)

- Molex Inc.(Koch Industries)

- Infinera Corporation

- NEC Corporation

- Innolume GmbH

- Coherent Corporation

- IPG Photonics Corporation

- AMS OSRAM AG

- Signify NV

- LEA Photonics SAS(Keopsys)

- Schott AG

- Carl Zeiss AG(Scantinel Photonics GmbH)

- Nikon Corporation

- Corning Inc.

第八章投资分析

第九章:未来市场展望

The Photonics Industry is expected to grow from USD 1.75 trillion in 2025 to USD 2.39 trillion by 2030, at a CAGR of 6.5% during the forecast period (2025-2030).

Photonics involve radiant energy (such as light), whose fundamental element is the photons and waves that can cure diseases, explore the universe, and even solve crimes. They involve the generation, manipulation, transmission, detection, and utilization of light and other forms of electromagnetic radiation. Photonics is widely regarded as a critical enabling technology for developing smart systems that efficiently use energy without sacrificing overall system efficiency. Many verticals, including healthcare, automotive, communications, manufacturing, and retail, are leveraging this technology to attain higher efficiency, driving the industry's growth. Investments from these sectors also have witnessed significant growth in recent past.

Key Highlights

- With photonics being a core technology of multiple industries, the industry outlook shows that the consumption of the technology is witnessing rapid growth, with the market expanding in new verticals. Over the past few years, there has been an increasing trend of LiDAR or additive manufacturing in photonics. LiDAR has been used to study the atmosphere's distribution of gases and contaminants for decades. In recent years, it has become a critical technology for autonomous driving. The advancements in LiDAR mapping systems and their enabling technologies have penetrated different verticals, like aerospace and defense, corridor mapping and topographical survey, automotive, mining, oil and gas, and other verticals, which are increasing the global market's scope.

- In the United States, the largest companies, such as Google, Microsoft, and Facebook, are the primary force driving the photonics market, necessitating optimizing the data transmission process for respective data centers. The country also provides a favorable environment for technological advancements and expansions. Furthermore, the significant funding landscape in the US silicon photonics devices industry has encouraged organizations and start-ups to invest in the expanding photonics market.

- Moreover, an article titled "A Survey on Silicon Photonic in Deep Learning," published by the Association of Computing Machinery stated that deep learning has led to exceptional success in solving some extremely tough problems in disciplines, including computer vision, natural language processing, and general pattern recognition. These achievements are the product of decades of research into better training methodology and deeper neural network models, as well as developments in deep neural network hardware platforms for training and execution. Many application-specific integrated circuit (ASIC) hardware accelerators for deep learning have received attention in recent years due to their improved performance and energy efficiency over standard CPU and GPU designs.

- According to this industry analysis report, the industries require a high level of initial investment to integrate such photonics technology for automation purposes. The high cost of automated systems is concerned with effective and robust hardware and efficient software. Automation equipment requires high capital investment to invest in smart production (an automated system can cost millions of dollars to install, design, and fabricate). Thus, industries rely on the existing technologies available at a lower price, ultimately challenging adoption.

- Apart from the direct impact evident in the supply chains and production of photonic solutions, the aftereffects of the pandemic are also impacting the growth of the market, as highlighted in the industry analysis report. For instance, the ongoing threat of recession looming over various regions, including the United States, may negatively influence the market's growth, as the economic uncertainty will prevent consumers and businesses from spending more on high-value products, which may impact the growth rate of the market studied.

- The COVID-19 pandemic influenced the overall semiconductor manufacturing market from the demand and supply sides. In addition, the global lockdowns and closure of semiconductor plants also fueled the supply shortage. The effects were also reflected in the market studied. However, many of these effects were short-term. Precautions by governments worldwide to support the automotive and semiconductor sectors helped revive the industry's growth.

Photonics Industry Trends

Consumer End-user Industry Segment Holds Significant Market Share

- Photonics are utilized in several consumer devices like barcode scanners, DVD players, TV remote controls, televisions, smartphones, etc. Barcode scanners are commonly used in consumer equipment like printers, CD/DVD/Blu-ray devices, and remote devices. Barcode scanners play a crucial role in logistics and supply chain management. They are used for scanning barcodes on product packages and shipping labels to track inventory, manage stock levels, and ensure accurate delivery.

- Photonics-based barcode scanners are used for package sorting in logistics applications. These scanners help automate sorting packages based on their barcode information. They are also extensively used in retail environments, including point-of-sale transactions, inventory management, and price verification. They enable quick and accurate scanning of product barcodes, improving efficiency and customer service.

- Photonics technology also plays a crucial role in the functioning of DVD players. DVD players utilize photonics technology in their optical disc drives, including CD, DVD, Blu-ray, and HD (high-definition) players and recorders. DVD players use lasers for reading and writing data on optical discs. The laser diode emits a focused, narrow beam of light that can be directed onto the surface of the disc, allowing for precise data retrieval and recording. DVD players are optical disc players that rely on photonics technology to read and write data on DVDs. The laser beam emitted by the laser diode interacts with the pits and lands on the DVD's surface, allowing the player to retrieve the stored information.

- According to the Consumer Technology Association (CTA) and the US Census Bureau, the sales value of smartphones sold in the United States was expected to increase from USD 73 billion in 2021 to USD 74.7 billion in 2022. Additionally, according to GSMA, in North America, the number of smartphone subscribers is expected to reach 328 million by 2025. Moreover, by 2025, North America may witness an increase in the penetration rates of mobile subscribers (86%) and the Internet (80%). The increasing demand and industry trends for mobile phones are likely to offer lucrative opportunities for the growth of the market studied.

- Moreover, the US Census Bureau estimated the smartphone sales value to be USD 74.7 billion during 2022-2023. This sluggish growth is an outcome of declined smartphone shipments in the United States. Low-end smartphone sales declines were the most significant contributing factor to the downturn amid economic challenges, high inflation, and poor seasonal demand. However, this is expected to end in the coming years. These industry trends are expected to impact smartphone camera lens growth significantly.

Asia-Pacific to Register Major Growth in the Global Market

- Japan is a high-tech powerhouse economy in Asia. The global camera industry is rapidly evolving, and Japan is a consistent leader and innovator in the market. Mirror-less hybrid cameras, DSLRs, and compact interchangeable-lens cameras now drive the camera market, further creating opportunities for the market studied.

- The country has many universities and institutes related to photonics. For instance, the Photonics Advanced Research Center (PARC) at Osaka University in Japan has emerged as a leading scientific and industrial research center for Japan's photonics.

- China is expected to exhibit a significant growth rate among countries in Asia-Pacific, owing to the region's growing economy and the global electronics market share. China is one of the prominent electronics producers and consumers. The manufacturing industry is rapidly growing in the region and witnessing the deployment of various manufacturing and telecommunications technologies, which is expected to aid the market's growth.

- India is one of the largest and fastest-growing economies in the world. The growing purchasing power and the rising influence of social media are expected to drive the market for electronic goods. The government is undertaking many initiatives to become one of the developed economies. The Ministry of Electronics and Information Technology, India, approves various digital projects, creating significant market growth opportunities over the forecast period.

- South Korea is one of the significant contributors to the market. The growing population, increasing investments toward developing silicon photonic products, international and domestic players' rising focus on developing modern silicon photonic products, and the improving R&D activities to increase the region's data transmission rate fuel the market growth.

- The countries considered part of the rest of the Asia-Pacific include Indonesia, Singapore, and Thailand. The rapid development of 5G, AI, the internet of things (IoT), virtual reality (VR), and the commercial application of such new technologies increase the demand for data processing and information interaction. This scenario may boost the construction of data centers in the region, leading to explosive industry growth.

Photonics Industry Overview

The photonics market is highly fragmented, with the presence of various major players, among which the largest companies are Hamamatsu Photonics KK, Intel Corporation, Polatis Incorporated (Huber+Suhner), Alcatel-Lucent SA (Nokia Corporation), and Molex Inc. (Koch Industries). The largest companies in the market are adopting strategies, such as partnerships and acquisitions, to enhance their product offerings and gain sustainable competitive advantage.

- November 2023 - Innolume announced the introduction of high-power O-Band quantum Dot SOA with 1W optical power. It can be used in LiDARs, PONs, and FSO.

- September 2023 - Ams OSRAM AG and the Malaysian Investment Development Authority (MIDA) announced mutual support for the continued investment and expansion in Malaysia. Through a collaborative agreement, MIDA demonstrated significant support for Ams OSRAM's initiatives in Malaysia.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products and Services

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Impact of COVID-19 Aftereffects and Other Macroeconomic Factors on the Market

- 4.5 Technology Snapshot

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Emergence of Silicon-based Photonics Applications

- 5.1.2 Increasing Focus on High Performance and Eco-friendly Solutions

- 5.2 Market Restraints

- 5.2.1 High Initial Cost of Photonics-enabled Devices

6 MARKET SEGMENTATION

- 6.1 By End-user Industry

- 6.1.1 Consumer

- 6.1.2 Aerospace and Defense

- 6.1.3 Display

- 6.1.4 Solar

- 6.1.5 LED Lighting

- 6.1.6 Medical and Bioinstrumentation

- 6.1.7 Industrial and Manufacturing

- 6.1.8 Automotive

- 6.1.9 Other End-user Industries

- 6.2 By Geography

- 6.2.1 North America

- 6.2.1.1 United States

- 6.2.1.2 Canada

- 6.2.2 Europe

- 6.2.2.1 United Kingdom

- 6.2.2.2 Germany

- 6.2.2.3 France

- 6.2.2.4 Italy

- 6.2.2.5 Rest of Europe

- 6.2.3 Asia-Pacific

- 6.2.3.1 Japan

- 6.2.3.2 China

- 6.2.3.3 India

- 6.2.3.4 Taiwan

- 6.2.3.5 South Korea

- 6.2.3.6 Rest of Asia-Pacific

- 6.2.4 Rest of the World

- 6.2.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Vendor Positioning Analysis

- 7.2 Company Profiles

- 7.2.1 Hamamatsu Photonics KK

- 7.2.2 Intel Corporation

- 7.2.3 Polatis Incorporated (HUBER+SUHNER)

- 7.2.4 Alcatel-lucent SA (Nokia Corporation)

- 7.2.5 Molex Inc. (Koch Industries)

- 7.2.6 Infinera Corporation

- 7.2.7 NEC Corporation

- 7.2.8 Innolume GmbH

- 7.2.9 Coherent Corporation

- 7.2.10 IPG Photonics Corporation

- 7.2.11 AMS OSRAM AG

- 7.2.12 Signify NV

- 7.2.13 LEA Photonics SAS (Keopsys)

- 7.2.14 Schott AG

- 7.2.15 Carl Zeiss AG (Scantinel Photonics GmbH)

- 7.2.16 Nikon Corporation

- 7.2.17 Corning Inc.

8 INVESTMENT ANALYSIS

9 FUTURE OUTLOOK OF THE MARKET

全球光电市场按产品类型、波长、应用、材料、最终用途产业和地区划分-预测至 2030 年

全球光电市场按产品类型、波长、应用、材料、最终用途产业和地区划分-预测至 2030 年 全球光电市场:2025-2030 年预测

全球光电市场:2025-2030 年预测 2032 年量子光电市场预测:按产品、应用、最终用户和地区分類的全球分析

2032 年量子光电市场预测:按产品、应用、最终用户和地区分類的全球分析 日本光子学市场报告(按类型、应用、最终用户和地区)2025-2033光电市场:按应用和地区划分全球光电市场规模(依产品类型、应用、最终用户、地区、预测)

日本光子学市场报告(按类型、应用、最终用户和地区)2025-2033光电市场:按应用和地区划分全球光电市场规模(依产品类型、应用、最终用户、地区、预测) 光电市场规模、份额、成长分析(按类型、应用、最终用途产业和地区)-2025 年至 2032 年产业预测2025 年至 2033 年光子学市场报告(按类型、应用、最终用户和地区)

光电市场规模、份额、成长分析(按类型、应用、最终用途产业和地区)-2025 年至 2032 年产业预测2025 年至 2033 年光子学市场报告(按类型、应用、最终用户和地区) 2025年量子光电全球市场报告

2025年量子光电全球市场报告 光电晶片市场分析及预测(至 2034 年):类型、产品、技术、组件、应用、材料类型、最终用户、功能、安装类型、设备

光电晶片市场分析及预测(至 2034 年):类型、产品、技术、组件、应用、材料类型、最终用户、功能、安装类型、设备