|

市场调查报告书

商品编码

1683522

安全存取服务边际(SASE) -市场占有率分析、行业趋势和成长预测(2025-2030 年)Secure Access Service Edge (SASE) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

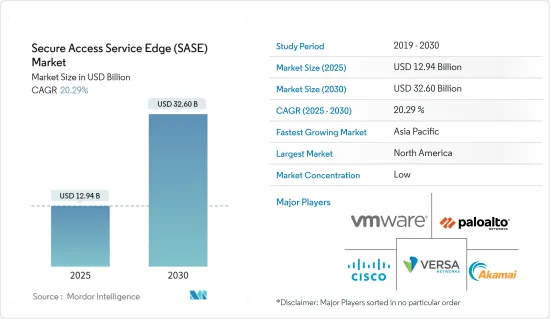

安全存取服务边际市场规模预计在 2025 年为 129.4 亿美元,预计到 2030 年将达到 326 亿美元,预测期内(2025-2030 年)的复合年增长率为 20.29%。

SASE 代表了网路存取安全的模式转移。它将网路和安全功能(如防火墙即服务 (FWaaS)、SD-WAN 甚至网路即服务 (NaaS))整合到单一云端原生服务中。这种整合以可扩展、灵活和安全的方式保护和连接您分散式的劳动力和云端基础的应用程式。

主要亮点

- SASE 提高了 SDN 环境的安全性并完善了软体定义网路 (SDN) 系统。 SDN 支援动态网路配置,SASE 确保网路在变更以满足不断变化的需求时能够得到安全保障。随着物联网 (IoT) 的发展,SASE 保护着物联网设备及其产生的资料。在物联网背景下,安全通讯和资料保护至关重要。

- 此外,云端基础的SASE 的采用可能会激增。例如,2024年2月,华为在IP Club Carnival上推出了全新的HiSec SASE解决方案。新发布的解决方案具有从云端到网路到边缘到端点的整合式智慧保护功能,为企业总部和分公司提供一致的安全保障。

- 随着公有云使用量的成长,各种类型的企业都在增加云端运算支出。云端运算支出已成为 IT 预算的重要组成部分,约有 77% 的公司报告年度云端运算支出超过 1,200 万美元,80% 的公司报告年度云端运算支出超过 120 万美元。小型企业的工作量较少、规模较小,这意味着整体云端成本较低。

- 市场相关人员关心的是,在为客户提供 SASE 服务的同时,保持适当的监管合规性和管理成本。供应商可能难以保证其技术的安全、平稳运作并遵守所有适用的法律法规。供应商未能遵守规则和标准可能会对其服务产生负面影响并危及其客户的业务运作。供应商提供的计划和服务优先考虑并遵守普遍接受的标准和服务交付最佳实践。供应商需要帮助来跟上不断发展的技术和政府法规。

- 在全球范围内更多企业中扩大投资策略可能会加速采用安全存取服务边缘来支援业务成长。在后 COVID-19 时代,我们预计提供单一供应商 SASE 的供应商数量将显着增加。后 COVID-19 时代的新 SD-WAN 购买很可能是单一供应商 SASE 产品的一部分。

安全存取服务边际(SASE) 市场趋势

大公司占有较大的市场占有率

- 边缘运算的日益普及、向云端基础设施的转变以及远端工作的快速扩展正在显着改变传统的网路架构和安全模型。拥有大量 IT 预算和技术熟练的员工的大型企业正在迅速适应这个市场现实。

- 采用分散式劳动力模式的大型企业发现,传统的 WAN 架构由于其 VPN 聚合容量严重有限,无法适应大多数随处办公 (WFA) 工作流程。现有的安全模型和静态的数位转型投资在过去几年减缓了大型企业对 SASE 的采用。

- 新IT基础设施正在全球市场扩张。越来越多的大型企业正在将安全性和网路整合到单一云端平台上。因此,恶意软体即服务正在针对暴露的物联网和OT环境(例如医院、油气天然气田、电网、运输服务和企业网路)大规模运作。威胁行为者需要付出大量调查努力才能发现并利用嵌入式物联网和营运技术设备的操作环境和配置。

- 根据微软《2023年数位防御报告》,全球的攻击呈现增加趋势,其中以身分攻击最为常见,占所有攻击的42%。此外,网路攻击逐年增多,全球勒索软体相关损失的成本不断上升。根据微软 2024 年的报告,密码攻击尝试次数从每月约 30 亿次飙升至每月 300 亿多亿次。

- 在我们互联的数位世界中,设备上线并与更大的系统通讯,收集大量资料并创造可视性,从而为大型企业创造商机。这种情况也为网路威胁打开了大门,并使网路犯罪成为价值数十亿美元的产业。电脑、路由器、印表机、网路摄影机和远端系统管理设备等物联网设备都面临安全风险。由于这些设备对于许多组织的业务至关重要,因此它们很快就会成为负担和安全风险。各行各业迅速采用物联网解决方案增加了攻击媒介机会组织面临风险。针对远端管理设备的攻击、基于网路的攻击和资料库攻击在大型企业中最为普遍。

- 上述事件可能会促进大型企业采用网路即即服务(NaaS),因为它具有区别于其他安全网路策略的功能。 SASE 不依赖资料中心的安全性,而是采取直接的方法,因为来自使用者装置的所有流量在发送到最终目的地之前会在更靠近使用者的点进行检查。这使其成为保护云端中的分散式劳动力和资料的理想选择。在当今以云端为中心的大型企业中,使用者、装置和应用程式需要从任何地方安全地存取工作。旧有系统无法承受提供这种灵活性所需的频宽。然而,SASE 透过允许任何使用者或装置(无论位于何处)进行访问,同时保持企业级安全性,从而增强了该领域的需求。

北美占很大份额

- 美国是一个发达的经济体,其先进技术的采用和接受、网路自动化的发展以及云端基础的服务的普及为安全接入服务边际市场做出了重大贡献。终端用户产业数位化,以及Cisco、 VMware、Palo Alto Networks、Versa Networks 和 Akamai Technologies 等知名供应商的出现,促进了市场的成长。

- 随着企业数位化转型快速加速,安全正转向云端运算。随着多个终端用户产业广泛采用云端服务,需要保护网路基础架构、降低复杂性并提高速度和灵活性。预计这将为未来几年的市场供应商提供巨大的成长机会。

- 美国有三大云端服务供应商:Amazon Web Services,Microsoft Azure和Google Cloud。它也被认为是 5G、自动驾驶、物联网、区块链、人工智慧和游戏等重大技术创新的中心。整合 SASE 功能可以将零信任安全功能整合到企业架构中,这对于实现可信任的网路安全态势至关重要。透过这种方式,SASE 解决方案正在改变最终用户网路和安全架构,降低网路风险、成本和复杂性。

- Orange Business、Palo Alto Networks 和 Orange Cyberdefense 于 2023 年 8 月建立合作伙伴关係,为全球企业提供云端原生、託管的安全存取服务边际(SASE) 解决方案。随着企业加速采用云端来支援混合业务并向客户提供现代产品和服务,数位攻击面正在扩大。该伙伴关係将提供业界最完整的人工智慧 SASE 解决方案、咨询和顾问服务以及全球託管网路、安全和数位服务。这项服务使组织能够最大限度地提高其 SASE 转型的投资收益(ROI)。

- 加拿大在云端运算应用方面处于领先地位。许多组织正在部署公有云、私有云和边缘云端的组合。混合工作和云端转型的兴起增加了对超越网路边界的保全服务的需求,对加拿大市场的成长产生了积极影响。此外,该国拥有严格的资料保护和监管法律,进一步推动了终端用户产业对 SASE 解决方案的需求。

- 预计自动化程度的提高和连网设备的引入将推动市场需求的大幅成长。网路即服务 (NaaS) 模式使中小型企业受益,因为它减轻了日常设备维护的负担,使他们能够专注于客户服务等任务。由于加拿大拥有大量小型企业,预计 NaaS 将成为未来几年的一大趋势。

安全存取服务边际(SASE) 市场概览

安全接入服务边际市场中的供应商提供各种服务,并且适度整合。然而,VMware、Palo Alto Networks、Versa Networks Inc. 和 Cisco Systems Inc. 等主要供应商是不同地区各类终端使用者高度青睐的网路服务供应商。

- 2024 年 1 月-Kindrill 宣布将与思科合作推出两项新的 Security Edge 服务,以协助客户改善安全管理并主动解决和应对网路事件。新推出的安全边缘服务,以及 Kyndryl 和思科可用的 SD-WAN 服务,使企业能够为向安全存取服务边际(SASE) 架构的过渡奠定坚实的基础。

- 2024 年 1 月 - Vertha Networks 是领先的基于 AI/ML 的整合安全存取服务边际(SASE) 解决方案供应商,宣布推出一系列新的整合 SASE 闸道。这些网关提供超过 100Gbps 的惊人吞吐量,旨在满足对增强运算能力日益增长的需求。这项需求是由产业内网路和安全功能日益融合所推动的。 Versa 的新网关将高效能硬体与 Versa 作业系统 (VOS)(该公司的整合 SASE 软体堆迭)结合,具有单一途径架构。这种效能的提升使企业首次能够将安全功能和多种网路功能整合到单一网关上。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 竞争对手之间的竞争

- 替代品的威胁

- 评估影响市场的宏观经济因素

第五章 市场动态

- 市场驱动因素

- 越来越需要结合 SD-WAN、FWaaS、SWG、CASB 和 ZTNA 功能的单一网路架构

- 缺乏安全程序和工具

- 强制遵守资料保护和监管法律

- 市场限制

- 缺乏有关云端资源、云端安全架构和 SD-WAN 策略的知识

- 前期成本高,且 SASE 架构及其组件缺乏标准化

第六章 市场细分

- 依产品类型

- 网路即服务

- 安全即服务

- 按组织规模

- 大型企业

- 中小型企业

- 按最终用户产业

- BFSI

- 资讯科技/通讯

- 零售

- 卫生保健

- 政府

- 製造业

- 其他最终用户产业

- 按地区

- 北美洲

- 美国

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 比利时

- 荷兰

- 卢森堡

- 丹麦

- 芬兰

- 挪威

- 瑞典

- 冰岛

- 亚洲

- 印度

- 中国

- 日本

- 台湾

- 韩国

- 马来西亚

- 香港

- 澳洲和纽西兰

- 拉丁美洲

- 中东和非洲

- 北美洲

第七章 竞争格局

- 公司简介

- Cisco Systems Inc.

- VMWare Inc.

- Palo Alto Networks.

- Versa Networks Inc.

- Akamai Technologies Inc.

- Cato Networks

- Fortinet Inc.

- Check Point Software Technologies Ltd

- Cloudflare Inc.

- Forcepoint

第八章投资分析

第九章:未来市场展望

The Secure Access Service Edge Market size is estimated at USD 12.94 billion in 2025, and is expected to reach USD 32.60 billion by 2030, at a CAGR of 20.29% during the forecast period (2025-2030).

SASE signifies a paradigm shift in network access security. It combines network and security features, like Firewall-as-a-service (FWaaS) and SD-WAN, further combining network-as-a-service (NaaS) into a single cloud-native service. With this convergence, distributed workforces and cloud-based applications will be protected and connected in a scalable, flexible, and secure manner.

Key Highlights

- SASE improves security in SDN environments, thereby completing software-defined networking (SDN) systems. Dynamic network configuration is made possible by SDN, and SASE guarantees that these networks are secure as they change in order to meet the changing requirements. SASE protects IoT devices and the data they generate as the Internet of Things (IoT) develops. In the context of the IoT, secure communications and data protection are essential.

- Furthermore, cloud-based SASE may witness a surge in adoption. For instance, in February 2024, Huawei announced the new HiSec SASE Solution launch at the IP Club Carnival. This newly launched solution comes with cloud-network-edge-endpoint integrated intelligent protection, providing consistent security assurance for the enterprise headquarters and branches.

- The increasing usage of the public cloud is boosting cloud spending for businesses of all kinds. Cloud spending is already a significant aspect of IT budgets, wherein about 77% of companies stated that their annual cloud spending value surpasses USD 12 million, and 80% of them stated that the value exceeds USD 1.2 million. As SMBs have fewer and smaller workloads, their overall cloud costs are cheaper.

- The market players are concerned about maintaining proper regulatory compliance while offering clients SASE services and executing expenses. Sometimes, vendors find it difficult to safeguard their technology, keep running smoothly, and comply with all applicable laws and regulations. Vendors' non-compliance with rules and standards can adversely affect their services and jeopardize clients' business operations. By adhering to the accepted standards and best service-delivery practices, they offer programs and services to prioritize them. Vendors need help keeping up with evolving technologies and government regulations.

- The growth in investment strategies in a larger share of businesses globally will accelerate the adoption of secure access service edge in supporting business growth. In the post-COVID-19 era, there will be a significant increase in the number of vendors with single-vendor SASE offerings. New SD-WAN purchases in the post-COVID-19 era will be part of a single-vendor SASE offering.

Secure Access Service Edge (SASE) Market Trends

Large Enterprises will Hold Major Market Shares

- Increased adoption of edge computing, the shift to cloud infrastructure, and a surge in remote work have challenged many traditional network architectures and security models. Large enterprises with access to larger IT budgets and skilled employees are rapidly adapting to this market reality.

- Large enterprises with a distributed workforce model find the traditional WAN architectures with rigidly limited VPN aggregation capacity inadequate for most work-from-anywhere (WFA) workflows. Existing security models and fixed digital transformation investments have slowed down the adoption of SASE among large enterprises over the last few years.

- The global market is witnessing an expansion in new IT infrastructure. Large enterprises that combine security and networks into a single cloud platform are proliferating. As a result, Malware-as-a-service has moved to large-scale operations against exposed IoT and OT in hospitals, oil and gas fields, electrical grids, transportation services, and corporate networks. Threat actors require significant research efforts to uncover and exploit the configuration of operating environments and embedded IoT and OT devices.

- According to the Microsoft Digital Defense Report 2023, Microsoft said that globally, there has been a growing number of attacks, of which identity attacks are the most common, and 42% of the total attacks are only identity attacks. Also, every year, there has been an increasing number of cyberattacks, and the cost of ransomware-related damage increases globally. As per the report published by Microsoft in 2024, attempted password attacks have soared to over 30 billion from around 3 billion per month.

- In a connected digital world, devices communicate online with larger systems, collecting voluminous data and creating visibility to bring business opportunities to large enterprises. This situation also opens the doors for cyber threats, making the cybercrime business worth multi-billion dollars. IoT devices such as computers, routers, printers, web cameras, and remote management devices are at a security risk. These devices are critical to many organizations' operations; hence, they can quickly become a liability and security risk. The rapid adoption of IoT solutions close to every industry has increased the number of attack vectors and organizations' risk exposure. Attacks against remote management devices, attacks via the web, and attacks on databases are most prevalent among large enterprises.

- The aforementioned incidents are likely to boost the adoption of the network-as-a-service (NaaS) in large enterprises due to its ability to stand out from other secure networking strategies. Rather than relying on data center security, SASE has a direct approach as the overall traffic from the users' devices is inspected at a nearby point of presence before being sent to its final destination. This makes it an ideal option for protecting distributed workforces and data in the cloud. In modern cloud-centric large enterprises, users, devices, and applications require secure access while working from anywhere. Legacy systems cannot tolerate the bandwidth needed to provide this flexibility. However, SASE can do so while maintaining enterprise-level security for users and devices at any location, which bolsters this segment's demand.

North America will Hold a Significant Share

- The United States is a developed economy with a significant inclination toward implementing and accepting advanced technology, development in network automation, and surge in cloud-based services, thereby contributing to the secure access service edge market. The growing digitization among end-user industries and the presence of prominent market vendors, like Cisco Systems Inc., Vmware Inc., Palo Alto Networks, Versa Networks Inc., and Akamai Technologies, are contributing to the market's growth.

- Security is moving toward cloud computation due to the fast acceleration of the digital transformation of businesses. The significant adoption of cloud services in several end-user industries necessitates securing the network infrastructure and reducing complexity to improve speed and agility. This is anticipated to create substantial growth opportunities for market vendors in the coming years.

- The United States is home to three major cloud service providers: Amazon Web Services, Microsoft's Azure, and Google Cloud. It is also considered to be the hub for major technological innovations such as 5G, autonomous driving, IoT, Blockchain, artificial intelligence, and gaming. Integrating SASE capabilities converges zero trust security capabilities into enterprise architectures, which is paramount in achieving a trusted network security posture. Thus, SASE solutions are analyzed to transform the end-users networks and security architectures to reduce cyber risks, costs, and complexities.

- Orange Business, Palo Alto Networks, and Orange Cyberdefense partnered in August 2023 to deliver a cloud-native managed security access service edge (SASE) solution to enterprises globally. The digital attack surface has expanded as organizations expedite cloud adoption to accommodate hybrid work and deliver the latest products and services to their customers. The partnership provides the industry's most complete AI-powered SASE solutions, advisory and consultant services, and global managed network, security, and digital services. Organizations using this offering can maximize their SASE transformation's return on investments (ROI).

- Canada is at the forefront of cloud adoption. Many organizations are deploying a mix of public, private, and edge clouds. With the rise of hybrid work and cloud transformation, the demand for security services to expand beyond the network perimeter is increasing, positively impacting the growth of the country's market. In addition, stringent data protection and regulatory legislation in the country further drive the demand for SASE solutions in end-user industries.

- The market demand is anticipated to rise significantly due to increasing automation and deploying connected devices. The network-as-a-service (NaaS) model benefits small businesses by offloading day-to-day equipment maintenance and focusing on tasks such as customer service. With a large base of small businesses in Canada, NaaS is expected to become a significant trend in the coming years.

Secure Access Service Edge (SASE) Market Overview

The secure access service edge market vendors are moderately consolidated with an array of services. However, major vendors like VMware, Palo Alto Networks, Versa Networks Inc., and Cisco Systems Inc. are highly preferred network service providers for various end users in various regions.

- January 2024 - Kyndryl announced that the company partnered with Cisco to launch two of its new security edge services in order to help customers improvise their security controls and address and respond to cyber incidents proactively. The newly launched security edge services along with Kyndryl and Cisco's available SD-WAN services, enable organizations to build a solid foundation to transition into a secure access service edge (SASE) architecture.

- January 2024-Versa Networks, a leading provider of AI/ML-powered Unified Secure Access Service Edge (SASE) solutions, has announced the launch of a new series of Unified SASE gateways. These gateways offer an impressive throughput exceeding 100 Gbps, designed to address the rising demand for enhanced computing capabilities. This demand is driven by the industry's increasing integration of networking and security functions. Versa's new gateways integrate high-performance hardware with the Versa Operating System (VOS), the company's unified SASE software stack, which features a single-pass architecture. This improved performance allows organizations to consolidate security functions and multiple networking into a single gateway for the first time.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Intensity of Competitive Rivalry

- 4.2.5 Threat of Substitute Products and Services

- 4.3 Assessment of Macro Economic Factors Impact on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Need for a Single Network Architecture that Combines SD-WAN, FWaaS, SWG, CASB, and ZTNA Capabilities

- 5.1.2 Lack of Security Procedures and Tools

- 5.1.3 Mandatory Compliance with Data Protection and Regulatory Legislation

- 5.2 Market Restraints

- 5.2.1 Lack of Knowledge of Cloud Resources, Cloud Security Architecture, and SD-WAN Strategy

- 5.2.2 High Upfront Implementation Costs and Lack of Standardization Around SASE Architecture and Its Components

6 MARKET SEGMENTATION

- 6.1 By Offering Type

- 6.1.1 Network as a Service

- 6.1.2 Security as a Service

- 6.2 By Organization Size

- 6.2.1 Large Enterprises

- 6.2.2 Small and Medium Enterprises

- 6.3 By End-user Vertical

- 6.3.1 BFSI

- 6.3.2 IT and Telecom

- 6.3.3 Retail

- 6.3.4 Healthcare

- 6.3.5 Government

- 6.3.6 Manufacturing

- 6.3.7 Other End-user Verticals

- 6.4 By Geography

- 6.4.1 North America

- 6.4.1.1 United States

- 6.4.1.2 Canada

- 6.4.2 Europe

- 6.4.2.1 Germany

- 6.4.2.2 United Kingdom

- 6.4.2.3 France

- 6.4.2.4 Spain

- 6.4.2.5 Italy

- 6.4.2.6 Belgium

- 6.4.2.7 Netherlands

- 6.4.2.8 Luxembourg

- 6.4.2.9 Denmark

- 6.4.2.10 Finland

- 6.4.2.11 Norway

- 6.4.2.12 Sweden

- 6.4.2.13 Iceland

- 6.4.3 Asia

- 6.4.3.1 India

- 6.4.3.2 China

- 6.4.3.3 Japan

- 6.4.3.4 Taiwan

- 6.4.3.5 South Korea

- 6.4.3.6 Malaysia

- 6.4.3.7 Hong Kong

- 6.4.3.8 Australia and New Zealand

- 6.4.4 Latin America

- 6.4.5 Middle East and Africa

- 6.4.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Cisco Systems Inc.

- 7.1.2 VMWare Inc.

- 7.1.3 Palo Alto Networks.

- 7.1.4 Versa Networks Inc.

- 7.1.5 Akamai Technologies Inc.

- 7.1.6 Cato Networks

- 7.1.7 Fortinet Inc.

- 7.1.8 Check Point Software Technologies Ltd

- 7.1.9 Cloudflare Inc.

- 7.1.10 Forcepoint

8 INVESTMENT ANALYSIS

9 FUTURE OUTLOOK OF THE MARKET

2026 年全球服务边际市场报告

2026 年全球服务边际市场报告 安全存取服务边际市场 - 全球产业规模、份额、趋势、机会、预测:按组件、最终用途、组织规模、地区和竞争对手划分,2021-2031 年

安全存取服务边际市场 - 全球产业规模、份额、趋势、机会、预测:按组件、最终用途、组织规模、地区和竞争对手划分,2021-2031 年 2026-2030年全球安全存取服务边缘市场

2026-2030年全球安全存取服务边缘市场 安全存取服务边缘 (SASE) 市场机会、成长驱动因素、产业趋势分析与预测 (2026-2035)

安全存取服务边缘 (SASE) 市场机会、成长驱动因素、产业趋势分析与预测 (2026-2035) 安全存取服务边缘 (SASE) 市场规模、份额和成长分析(按产品、服务标准、组织规模、最终用户和地区划分)—2026-2033 年行业预测

安全存取服务边缘 (SASE) 市场规模、份额和成长分析(按产品、服务标准、组织规模、最终用户和地区划分)—2026-2033 年行业预测 安全存取服务边缘 (SASE) 市场按产品、性别、组织规模、部署模式和最终用户行业划分 - 2025-2030 年全球预测

安全存取服务边缘 (SASE) 市场按产品、性别、组织规模、部署模式和最终用户行业划分 - 2025-2030 年全球预测 2023 年至 2028 年全球安全存取服务边际(SASE) 市场成长机会

2023 年至 2028 年全球安全存取服务边际(SASE) 市场成长机会 安全存取服务边际(SASE) 市场预测(至 2032 年):按产品、组织规模、部署类型、存取管道、最终用户和地区进行的全球分析Frost Radar:安全存取服务边际(SASE) 2025

安全存取服务边际(SASE) 市场预测(至 2032 年):按产品、组织规模、部署类型、存取管道、最终用户和地区进行的全球分析Frost Radar:安全存取服务边际(SASE) 2025 全球 SASE 市场(按产品、SD-WAN 产品和 SSE 产品划分)- 预测至 2030 年

全球 SASE 市场(按产品、SD-WAN 产品和 SSE 产品划分)- 预测至 2030 年