|

市场调查报告书

商品编码

1683533

欧洲木质颗粒-市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Europe Wood Pellet - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

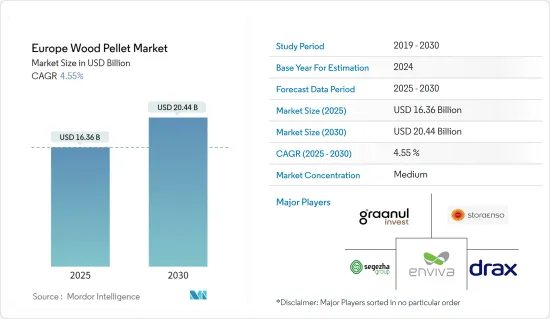

预计 2025 年欧洲木质颗粒市场规模为 163.6 亿美元,预计到 2030 年将达到 204.4 亿美元,预测期内(2025-2030 年)的复合年增长率为 4.55%。

主要亮点

- 从中期来看,清洁能源发电和供暖应用对木质颗粒的需求增加预计将推动欧洲木质颗粒市场的发展。

- 然而,清洁能源替代品的竞争加剧以及政府对木质颗粒补贴的终止可能会阻碍预测期内的市场成长。

- 然而,新应用的出现和木质颗粒技术的进步预计将推动未来市场的成长。

- 由于木质颗粒在各种应用中的采用越来越多,预计英国将主导欧洲木质颗粒市场。

欧洲木质颗粒市场的趋势

加热应用领域预计将占据市场主导地位

- 用于供暖的木质颗粒主要用于住宅和商业领域,用于食品、烹饪、烧烤和为住宅供暖。这些木质颗粒与连接的管道、锅炉和暖气散热器一起用于建造家庭供暖系统。用于暖气方面有颗粒集中暖气锅炉,颗粒炉,颗粒集中暖气炉等。

- 由于木质颗粒消费量的增加,尤其是在德国和法国,欧洲木质颗粒市场的暖气应用领域预计将产生巨大的需求。欧洲是世界上最大的木质颗粒市场。 2022 年,该地区木质托盘总消费量量为 2,480 万吨 (MMT)。根据欧盟委员会 (EC) 的指令和欧盟成员国 (MS) 的激励措施,预计 2023 年需求将进一步扩大至 2,560 万吨。

- 预计未来几年住宅供暖对木质颗粒的需求不断增加将推动市场成长。住宅用途包括家用炉灶和容量低于50千瓦的暖气锅炉。容量超过50kW的中小型商务用包括住宅和公共建筑使用的热锅炉。

- 木质颗粒可用作生物质锅炉或专用颗粒燃烧炉的家庭暖气燃料。颗粒炉优于传统的木质炉,因为它们燃烧更清洁,产生的烟雾和烟灰更少。木质颗粒密度高,水分含量低(低于 10%),这使得它们可以在炉子中以更高的温度燃烧,从而提高效率,并且产生的灰烬比传统木柴(低于 2%)少得多。

- 使用木质颗粒加热是减少电费的替代方案。由于燃料成本上升,欧洲消费者正在寻找替代供暖方法。

- 根据炉灶行业联合会的数据,木柴是最便宜的家庭暖气燃料,每千瓦时成本比电加热低 74%,比燃气加热低 21%。预计木质颗粒的这些优势将在预测期内增加其在加热应用中的需求。

- 德国、义大利、法国、丹麦和瑞典是使用木质颗粒取暖的主要国家。根据《2023年EPC调查》,2022年德国将成为木质颗粒加热的最大用户,销售量达320万吨。

- 在德国和义大利,木质颗粒产生的热量有70%以上用于住宅供暖,而在丹麦和瑞典,木质颗粒主要用于热电联产供热。气候在木质颗粒消费中扮演重要角色。由于预计未来欧洲国家的气候将变得更加寒冷,预计在预测期内用于供暖的颗粒利用率将会增加。

- 因此,预计预测期内加热应用领域将占据市场主导地位。

英国可望主导市场

- 在英国,颗粒用于多种用途,包括住宅供暖、发电站、商业供暖和热电联产厂。颗粒燃料也被用于学校、办公室等地方政府和政府建筑的煤炭转化计划。

- 截至 2024 年,大多数混燃发电厂已经关闭或改造,一些发电厂正在转向使用 100%木质颗粒作为燃料。其中最大的是位于北约克郡的德拉克斯发电厂。六台 65MWe 发电机组当中,有四台已经改装为仅使用木质颗粒运作。

- 德拉克斯发电厂是英国最大的发电站,到 2023 年将生产英国总电力的 5% 左右。它也是世界上最大的生物质发电厂,每年接收约 650 万吨(MT)颗粒,占该国年度颗粒进口量的大部分。该公司还在美国和加拿大拥有 17 家颗粒工厂,为发电厂供应原料。

- 然而,根据英国政府的数据,该国在 2023 年进口了 600 万吨木质颗粒,而 2022 年为 752 万吨,2021 年为 913 万吨。

- 根据联合国粮食及农业组织的数据,2022 年该国木质颗粒产量约 326,000 吨。木质颗粒产量与前一年同期比较大幅成长约7.2%。

- 英国政府已製定计划,到 2035 年发展碳捕获、利用和储存(CCUS) 的竞争性市场,并于 2023 年 12 月宣布扩大 CfD 计划,以支持生质能源的捕碳封存(BECCS)。预计到 2050 年,这些计划将使英国经济每年增长 50 亿欧元,使英国成为该技术的先驱。

- Drax 每年获得数亿英镑的补贴来资助其营运。 2027年,英国政府计划停止对未燃烧生质能发电的支持。

- 为了防止补贴在 2027 年后逐步取消,Drax 正在寻求为其木材燃烧业务获得新的长期补贴。该公司旨在透过其计划中的 BECCS(生物能源与碳捕获)计划实现这一目标。该计划最初提案在现有发电能力的一半上增加碳捕获和储存(CCS),该公司表示这将每年产生 8 吨负排放。目标是将 CCS 添加到所有发电能力中。

- 2024 年 1 月,作为 CfD 计画延伸的一部分,英国政府核准在德拉克斯发电厂引入碳捕获技术的计画。该工厂将获准在其四个生物质装置中的两个装置中安装该技术,这些装置透过燃烧木质颗粒发电。

- 因此,由于这些发展,预计英国将在预测期内主导欧洲木质颗粒市场。

欧洲木质颗粒产业概况

欧洲木质颗粒市场正朝向半固体发展。市场的主要企业包括 Stora Enso Oyj、Enviva Partners LP、AS Graanul Invest、Drax Group PLC 和 Segezha Group PJSC。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究范围

- 市场定义

- 调查前提

第 2 章执行摘要

第三章调查方法

第四章 市场概况

- 介绍

- 2029 年市场规模与需求预测

- 最新趋势和发展

- 政府法规和政策

- 市场动态

- 驱动程式

- 清洁能源生产对木质颗粒的需求不断增加

- 供热应用

- 限制因素

- 清洁能源替代品的竞争日益激烈,政府对木质颗粒的支持也终止

- 驱动程式

- 供应链分析

- 波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争强度

第五章 市场区隔

- 应用

- 加热

- 发电

- 地区

- 德国

- 英国

- 法国

- 荷兰

- 比利时

- 西班牙

- 俄罗斯

- 欧洲其他地区

第六章 竞争格局

- 併购、合资、合作与协议

- 主要企业策略

- 公司简介

- Stora Enso Oyj

- Enviva Partners LP

- AS Graanul Invest

- Drax Group PLC

- Segezha Group PJSC

- Svenska Cellulosa Aktiebolaget SCA

- German Pellets GmbH

- Pure Biofuel Ltd

- Pfeifer Group

- Erdenwerk Gregor Ziegler GmbH

- 市场排名分析

第七章 市场机会与未来趋势

- 木质颗粒技术的新应用与进展

简介目录

Product Code: 91897

The Europe Wood Pellet Market size is estimated at USD 16.36 billion in 2025, and is expected to reach USD 20.44 billion by 2030, at a CAGR of 4.55% during the forecast period (2025-2030).

Key Highlights

- Over the medium period, the increasing demand for wood pellets in clean energy generation and heat-supply applications will likely drive the European wood pellets market.

- On the other hand, the increasing competition from alternative clean energy sources and the ending of supportive government schemes for wood pellets will likely hinder market growth during the forecast period.

- Nevertheless, the emerging applications and advancements in wood pellet technology are expected to boost the market's growth in the future.

- The United Kingdom is expected to dominate the European wood pellet market due to the increasing adoption of wood pellets for various applications.

Europe Wood Pellet Market Trends

The Heating Application Segment is Expected to Dominate the Market

- Wood pellets for heating applications are primarily used in residential and commercial sectors for food, cooking and grilling, and supplying heat to homes. These wood pellets, along with connected pipes, boilers, and heating radiators, are used to build heating systems at home. For heating proposes, several systems using wood pellets include pellet central heating boilers, pellet stoves, and pellet central heating stoves.

- The heating application segment of the European wood pellet market is expected to generate significant demand due to the rising consumption of wood pellets, especially in Germany and France. Europe is the largest global wood pallet market. In 2022, the region's total wood pallet consumption accounted for 24.8 million metric tons (MMT). According to the European Commission's (EC) mandates and incentives by EU Member States (MS), demand was expected to further expand to 25.6 MMT in 2023.

- The increasing demand for wood pellets for residential heating purposes is expected to fuel the market's growth in the future. Residential uses include domestic stoves and dedicated heat boilers with a capacity below 50 kW. Small-to-medium-scale commercial use with more than 50 kW capacity includes heat boilers used in residential and public buildings.

- Wood pellets can be used as a home heating fuel in biomass boilers or special pellet-burning stoves. Pellet stoves are better than traditional open-wood fireplaces as they burn cleaner with less smoke and soot. As the wood pellets are highly dense and contain low moisture content (lower than 10%), the pellets can burn in the stove at a very high combustion temperature with improved efficiency and much lower ash content (less than 2%) than conventional firewood.

- Using wood pellets for heating is an alternative method of reducing electricity bills. Consumers in Europe are looking for alternative ways to heat their homes following higher fuel bills.

- According to the Stove Industry Alliance, wood logs are the cheapest domestic heating fuel, costing households 74% less per kWh than electric heating and 21% less than gas heating. Such benefits of wood pellets are expected to increase their demand in heating applications during the forecast period.

- Germany, Italy, France, Denmark, and Sweden are the major countries that use wood pellets for heating purposes. According to the EPC Survey 2023, Germany used the highest amount of wood pellets for heating purposes in 2022, which accounted for 3.2 million tons.

- In Germany and Italy, more than 70% of heat generation from wood pellets was used for residential heating, while in Denmark and Sweden, pellets were used mostly for CHP heat. The climate plays an important role in the consumption of wood pellets. As the climate of European countries is expected to have colder seasons in the future, the use of pellets for heating purposes is expected to increase during the forecast period.

- Therefore, the heating application segment is expected to dominate the market during the forecast period.

The United Kingdom is Expected to Dominate the Market

- The United Kingdom uses pellets in numerous applications, such as residential heating, power plants, commercial heating, and combined heat and power plants. Pellets have also made their way into coal conversion projects in local authority buildings and public administration buildings such as schools and offices.

- As of 2024, most of the co-firing power stations have either closed or converted, with several shifting toward using 100% wood pellets for fuel. The largest of these is Drax Power Station in North Yorkshire. It has converted four of its six 65 MWe generating units to run exclusively on wood pellets.

- The Drax power plant is the country's largest, producing around 5% of the United Kingdom's total electricity in 2023. It is also the world's largest biomass-fired power station, taking in around 6.5 million metric tons (MT) of pellets each year and making up the vast majority of the country's annual pellet imports. The company also has 17 pellet plants located in the United States and Canada, which supply raw materials to its power station.

- However, according to the UK government, the country imported 6 million metric tons of wood pellets in 2023, compared to 7.52 million metric tons in 2022 and 9.13 million tons in 2021.

- According to the Food and Agriculture Organization of the United Nations, the country's wood pellet production was about 326 thousand metric tons in 2022. The production of wood pellets witnessed significant growth of about 7.2% compared to the previous year.

- In December 2023, the UK government announced its plans to extend the CfD program to support bioenergy with carbon capture and storage (BECCS) as the country set out its plan to develop a competitive market in Carbon Capture, Usage, and Storage (CCUS) by 2035. The plan is expected to boost the UK economy by EUR 5 billion a year by 2050 and make the country a pioneer in this technology.

- Drax receives hundreds of millions of pounds in annual subsidies to fund its operations. In 2027, the UK government plans to end its support for burning unabated biomass to generate electricity.

- To prevent subsidy closure after 2027, Drax is looking to secure a new long-term subsidy for its wood-burning operation. The company aims to achieve this through its planned Bioenergy with Carbon Capture (BECCS) project. This project initially proposed adding carbon capture storage (CCS) to half of its existing capacity, which the company claims will generate eight metric tons of negative emissions yearly. The aim is to add CCS to its full capacity.

- In January 2024, following the extension of the CfD program, the UK government approved Drax's plans to install carbon capture technology at Drax Power Station. The Power Station will be allowed to install the technology in two of its four biomass units, which burn wood pellets to produce electricity.

- Hence, owing to such developments, the United Kingdom is expected to dominate the European wood pellets market during the forecast period.

Europe Wood Pellet Industry Overview

The European wood pellets market is semi-consolidated. Some of the key players in the market include Stora Enso Oyj, Enviva Partners LP, AS Graanul Invest, Drax Group PLC, and Segezha Group PJSC.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increasing Demand for Wood Pellets in Clean Energy Generation

- 4.5.1.2 Heat-supply Applications

- 4.5.2 Restraints

- 4.5.2.1 Increasing Competition from Alternative Clean Energy Sources and Ending of Supportive Government Schemes for Wood Pellets

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Application

- 5.1.1 Heating

- 5.1.2 Power Generation

- 5.2 Geography

- 5.2.1 Germany

- 5.2.2 United Kingdom

- 5.2.3 France

- 5.2.4 Netherlands

- 5.2.5 Belgium

- 5.2.6 Spain

- 5.2.7 Russia

- 5.2.8 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Stora Enso Oyj

- 6.3.2 Enviva Partners LP

- 6.3.3 AS Graanul Invest

- 6.3.4 Drax Group PLC

- 6.3.5 Segezha Group PJSC

- 6.3.6 Svenska Cellulosa Aktiebolaget SCA

- 6.3.7 German Pellets GmbH

- 6.3.8 Pure Biofuel Ltd

- 6.3.9 Pfeifer Group

- 6.3.10 Erdenwerk Gregor Ziegler GmbH

- 6.4 Market Ranking Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Emerging Applications and Advancements in the Wood Pellet Technology

02-2729-4219

+886-2-2729-4219

2026-2030年全球木质颗粒市场

2026-2030年全球木质颗粒市场 全球木质颗粒市场规模、份额、趋势和成长分析报告(2026-2034)

全球木质颗粒市场规模、份额、趋势和成长分析报告(2026-2034) 2026-2034年木质颗粒市场规模、份额、趋势及预测(依原料种类、应用及地区划分)

2026-2034年木质颗粒市场规模、份额、趋势及预测(依原料种类、应用及地区划分) 2026年全球木质颗粒市场报告

2026年全球木质颗粒市场报告 木质颗粒燃料市场-全球产业规模、份额、趋势、机会和预测:按原料、暖气用途、应用、地区和竞争格局划分,2021-2031年日本木屑颗粒市场报告(按原料类型(森林木材和废弃物、农业残余物及其他)、应用(发电厂、住宅供暖、商业供暖、热电联产及其他)和地区划分,2026-2034年)

木质颗粒燃料市场-全球产业规模、份额、趋势、机会和预测:按原料、暖气用途、应用、地区和竞争格局划分,2021-2031年日本木屑颗粒市场报告(按原料类型(森林木材和废弃物、农业残余物及其他)、应用(发电厂、住宅供暖、商业供暖、热电联产及其他)和地区划分,2026-2034年) 木质颗粒市场机会、成长要素、产业趋势分析及2026年至2035年预测

木质颗粒市场机会、成长要素、产业趋势分析及2026年至2035年预测 木质颗粒市场规模、份额和成长分析(按原料、应用、最终用途和地区划分)-2026-2033年产业预测

木质颗粒市场规模、份额和成长分析(按原料、应用、最终用途和地区划分)-2026-2033年产业预测 工业木质颗粒市场规模、份额及成长分析(依原料、应用、最终用途及地区划分)-2026-2033年产业预测

工业木质颗粒市场规模、份额及成长分析(依原料、应用、最终用途及地区划分)-2026-2033年产业预测 全球公用事业木质颗粒市场(按原始材料、生产流程、等级、分销管道和应用)预测(2025-2030 年)

全球公用事业木质颗粒市场(按原始材料、生产流程、等级、分销管道和应用)预测(2025-2030 年)

▼