|

市场调查报告书

商品编码

1690132

木质颗粒:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Wood Pellet - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

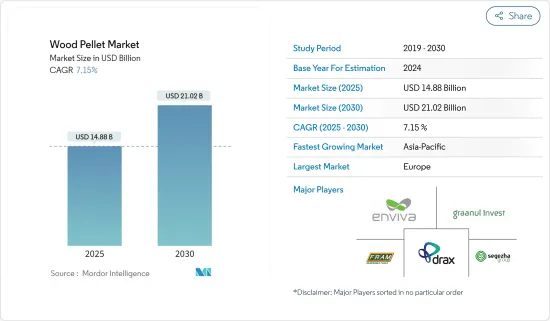

预计 2025 年木质颗粒市场规模为 148.8 亿美元,预计到 2030 年将达到 210.2 亿美元,预测期内(2025-2030 年)的复合年增长率为 7.15%。

中期市场驱动因素包括清洁能源发电对木质颗粒的需求不断增长,尤其是在欧洲。

然而,全球范围内越来越多地采用和实施太阳能、风能和地热能等替代可再生能源可能会阻碍预测期内的市场成长。

然而,据全球生质能源协会称,木质颗粒有潜力在发电设施中取代煤炭。随着近年来技术的发展,木质颗粒正在透过热解、热液碳化和蒸汽爆破等各种製程进行热升级。热升级使木质颗粒能够作为具有煤炭特性的燃料。亚太地区拥有全球最多的燃煤发电厂,预计将成为未来市场的成长机会。

预计 2022 年欧洲木质颗粒产量将大幅增加,并将在预测期内占据大部分市场份额。

木质颗粒市场趋势

暖气应用可望主导市场

- 颗粒是一种固态生物质燃料,主要由木材残渣和稻草等其他农产品生产。与原始生物质相比,颗粒的具体优势包括标准化特性、高能量含量和高密度。

- 用于供暖的木质颗粒主要用于住宅和商业领域的食品、烹饪、烧烤和家庭供暖。它的喷射成本长期以来一直低于其他燃料,使其成为更经济的选择,并解决了住宅和商业领域的关键问题。

- 木质颗粒是一种緻密的生物质燃料,燃烧后可产生电能和热能。 21 世纪末,多个国家的木质颗粒产量、消费量和商业量大幅增加。消费量的成长是由工业发电厂推动的,在这些发电厂中,木质颗粒通常与煤共燃或替代煤。

- 根据德国能源木材和颗粒协会的数据,到 2022 年,德国的颗粒加热系统数量将达到 648,000 个,高于 2021 年的 57 万个。

- 此外,木质颗粒作为再生能源来源,受到许多国家政府的补贴和鼓励,近年来许多国家推出或更新了与木质颗粒供暖相关的政策和计划。

- 英国政府已实施仅限颗粒燃料的品质禁令,该禁令将于 2022 年 11 月 23 日生效,为期一年。这意味着,在禁令生效期间,生物质锅炉或从 OFGEM 获得可再生热能激励支付的工厂使用的木质颗粒将不需要遵守燃料品质标准。政府于 2022 年 2 月修改了法规,要求具有生物质供应商名单 (BSL) 编号的木质燃料也必须符合相关品质标准。

- 因此,鑑于上述情况,预计在预测期内,加热应用将占据木质颗粒的主导地位。

欧洲主导市场

- 预计 2022 年至 2028 年间,欧洲木质颗粒需求将增加 30-40%。欧洲占全球颗粒需求的 50% 以上。此外,球团也被用于学校、办公室等地方政府和政府建筑的煤炭转化计划。

- 根据美国对外农业服务局的报告,2022年欧盟颗粒消费量将达2,480万吨,与前一年同期比较增加1.2%。欧洲约 66% 的颗粒消费量来自住宅和商业部门,34% 来自工业部门。各国的情况有所不同。在荷兰和丹麦,主要驱动力是工业(电力和热电联产)。在义大利、德国和法国,住宅供暖占木质颗粒使用量的大部分。

- 该地区大多数国家正计划关闭或改造其混燃发电厂,其中有几个国家正在转向 100%木质颗粒燃料。例如,维美德于 2023 年 5 月宣布,将在芬兰赫尔辛基的 Salmisaari ‘A’ 发电厂将 Helen 的燃煤区域供热锅炉和鼓泡流体化床(BFB) 燃烧转换为木质颗粒燃烧。这一转变推进了公司摆脱煤炭的目标,同时加强了永续能源系统的建设。

- 同时,2022年7月,欧盟为因应乌克兰战争,禁止进口用于发电的俄罗斯木质生物质。据报导,欧盟正在从美国和东欧进口木质颗粒,以取代俄罗斯木质生物质供应。自战争开始以来,Enviva 增加了对欧盟的出货量,并宣布与一位未透露姓名的欧洲客户达成一项为期 10 年的协议,到 2027 年每年供应 80 万吨颗粒。

- 此外,在研究期间,该地区市场技术进步也可能增加对木质颗粒的需求。

- 因此,鑑于上述情况,预计欧洲将在预测期内占据市场主导地位。

木质颗粒产业概况

木质颗粒市场适度整合。市场的主要企业包括(不分先后顺序)Enviva Partners LP、AS Graanul Invest、Drax Group Plc、Fram Renewable Fuels LLC 和 Segezha Group JSC。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究范围

- 市场定义

- 调查前提

第 2 章执行摘要

第三章调查方法

第四章 市场概况

- 介绍

- 2029 年市场规模与需求预测(美元)

- 最新趋势和发展

- 政府法规和政策

- 市场动态

- 驱动程式

- 清洁能源产出对木质颗粒的需求不断增加

- 木质颗粒製造基础设施的成长

- 限制因素

- 越来越多地采用和部署替代可再生能源

- 驱动程式

- 供应链分析

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争强度

第五章 市场区隔

- 应用

- 加热

- 发电

- 地区

- 北美洲

- 美国

- 加拿大

- 北美其他地区

- 欧洲

- 法国

- 义大利

- 德国

- 英国

- 西班牙

- 北欧国家

- 土耳其

- 俄罗斯

- 其他欧洲国家

- 亚太地区

- 中国

- 印度

- 印尼

- 日本

- 韩国

- 马来西亚

- 泰国

- 越南

- 其他亚太地区

- 南美洲

- 巴西

- 阿根廷

- 哥伦比亚

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 南非

- 奈及利亚

- 卡达

- 埃及

- 其他中东和非洲地区

- 北美洲

第六章 竞争格局

- 併购、合资、合作与协议

- 主要企业策略

- 公司简介

- Enviva Partners LP

- AS Graanul Invest

- Drax Group PLC

- Fram Renewable Fuels LLC

- Segezha Group JSC

- Lignetics Inc.

- Biopower Sustainable Energy Corp.

- Asia Biomass Public Company Limited

- PT South Pacific

- Market Ranking/Share Analysis

第七章 市场机会与未来趋势

- 由于技术发展,木质颗粒的温度升高

The Wood Pellet Market size is estimated at USD 14.88 billion in 2025, and is expected to reach USD 21.02 billion by 2030, at a CAGR of 7.15% during the forecast period (2025-2030).

Over the medium period, the primary drivers for the market include increasing demand for wood pellets in clean energy generation, especially in the European region.

On the other hand, the adoption and increasing deployment of alternative renewable energy sources such as solar photovoltaic, wind energy, and geothermal in various parts of the world is likely to hinder market growth during the forecast period.

Nevertheless, as per the World Bioenergy Association, wood pellets have the potential to replace coal in power generation facilities. With technology development in recent years, wood pellets have undergone thermal upgrading through various processes like torrefaction, hydrothermal carbonization, and steam explosion. The thermal upgrading enables wood pellets to act as a fuel with coal properties. The Asia-Pacific region, with the world's highest number of coal power plants, is expected to be an opportunity for the market to grow in the future.

With a significant production of wood pellets during 2022, Europe was expected to have a significant share of the market during the forecast period.

Wood Pellet Market Trends

Heating Application Expected to Dominate the Market

- Pellets are a solid biomass fuel, primarily produced from wood residues and agricultural by-products like straw. Specific advantages of pellets as compared to unprocessed biomass include standardized properties, high energy content, and high density.

- Wood pellets for heating applications are primarily used in residential and commercial sectors for food, cooking and grilling, and supplying heat to homes. Since the cost of shots remained cheaper than other fuels for a long time, it has become a more economical option, addressing the primary concern of the residential and commercial sectors.

- When burned, utility wood pellets (wood pellets) are a densified biomass fuel that can create power or heat. Wood pellet production, consumption, and commerce significantly increased in a few nations during the late 2000s. Industrial power plants, where wood pellets are usually co-fired with or replaced by coal, are the source of consumption growth.

- According to the German Energy Wood and Pellet Association, in 2022, there were 648 thousand pellet heating systems in Germany, an increase compared to 570 thousand in 2021.

- Moreover, as a renewable energy source, wood pellets have received subsidies and incentives from governments in many countries, and many countries either launched or updated their policies and schemes related to wood pellets for heating applications in recent years.

- The UK government has implemented a suspension of fuel quality for pellets exclusively, which went into effect on November 23, 2022, for up to one year. This means that while the rest is in effect, the fuel quality criteria for wood pellets used in biomass boilers and plants where the owner receives Renewable Heat Incentive payments from OFGEM are not required. The government revised regulations in February 2022 to require that any wood fuel having a Biomass Suppliers List (BSL) number also meet the relevant quality criteria.

- Therefore, owing to the above points, the heating application is expected to dominate the wood pellet during the forecast period.

Europe to Dominate the Market

- Europe's demand for wood pellets is expected to increase by 30-40% between 2022 and 2028. Europe represents more than 50% of global pellet demand. Moreover, pellets have also made their way into coal conversion projects in local authority or public administration buildings such as schools and offices.

- According to the USDA Foreign Agricultural Service Report, in 2022, the EU's pellet consumption reached 24.8 million tonnes, up 1.2% from the previous year. The household and commercial sectors consumed around 66% of European pellets, while the industry consumed 34%. The situation varies from one country to the next. The main driver for the Netherlands and Denmark is industrial use (for electricity and CHP). Residential heating accounts for most wood pellet use in Italy, Germany, and France.

- Most countries in the region plan to close or convert co-firing power stations, with several moving to 100% wood pellets for fuel. For instance, in May 2023, Valmet announced the convert Helen Ltd's coal-fired district heat boiler and bubbling fluidized bed (BFB) combustion to enable wood pellet firing at the Salmisaari 'A' power plant in Helsinki, Finland. The conversion promotes the company's goal of phasing out coal and simultaneously strengthens the construction of a sustainable energy system.

- On the other hand, in July 2022, the European Union banned importing Russian woody biomass used to generate energy in response to the war in Ukraine. According to reports, the EU has imported wood pellets from the United States and Eastern Europe to replace the Russian woody biomass supply. Enviva has increased EU shipments since the war began and announced a 10-year contract with an unnamed European customer to provide 800,000 metric tons of pellets yearly by 2027.

- Further, technological advancements in the market in the region are also likely to increase the demand for wood pellets during the studied period.

- Hence, owing to the above points, Europe is expected to dominate the market during the forecast period.

Wood Pellet Industry Overview

The wood pellet market is moderately consolidated. Some of the key players in the market include (in no particular order) Enviva Partners LP, AS Graanul Invest, Drax Group Plc, Fram Renewable Fuels LLC, and Segezha Group JSC, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecasts in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increasing Demand for Wood Pellets in Clean Energy Generation

- 4.5.1.2 Growing Wood Pellet Manufacturing Infrastructure

- 4.5.2 Restraints

- 4.5.2.1 The Adoption and Increasing Deployment of Alternative Renewable Energy

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Application

- 5.1.1 Heating

- 5.1.2 Power Generation

- 5.2 Geography

- 5.2.1 North America

- 5.2.1.1 United States of America

- 5.2.1.2 Canada

- 5.2.1.3 Rest of the North America

- 5.2.2 Europe

- 5.2.2.1 France

- 5.2.2.2 Italy

- 5.2.2.3 Germany

- 5.2.2.4 United Kingdom

- 5.2.2.5 Spain

- 5.2.2.6 Nordic Countries

- 5.2.2.7 Turkey

- 5.2.2.8 Russia

- 5.2.2.9 Rest of the Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 China

- 5.2.3.2 India

- 5.2.3.3 Indonesia

- 5.2.3.4 Japan

- 5.2.3.5 South Korea

- 5.2.3.6 Malaysia

- 5.2.3.7 Thailand

- 5.2.3.8 Vietnam

- 5.2.3.9 Rest of the Asia-Pacific

- 5.2.4 South America

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 Colombia

- 5.2.4.4 Rest of the South America

- 5.2.5 Middle-East and Africa

- 5.2.5.1 Saudi Arabia

- 5.2.5.2 United Arab Emirates

- 5.2.5.3 South Africa

- 5.2.5.4 Nigeria

- 5.2.5.5 Qatar

- 5.2.5.6 Egypt

- 5.2.5.7 Rest of the Middle-East and Africa

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Enviva Partners LP

- 6.3.2 AS Graanul Invest

- 6.3.3 Drax Group PLC

- 6.3.4 Fram Renewable Fuels LLC

- 6.3.5 Segezha Group JSC

- 6.3.6 Lignetics Inc.

- 6.3.7 Biopower Sustainable Energy Corp.

- 6.3.8 Asia Biomass Public Company Limited

- 6.3.9 PT South Pacific

- 6.4 Market Ranking/Share Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Thermal Upgradation of Wood Pellets Due to Technological Development

全球木质颗粒市场规模、份额、趋势和成长分析报告(2026-2034)

全球木质颗粒市场规模、份额、趋势和成长分析报告(2026-2034) 2026-2034年木质颗粒市场规模、份额、趋势及预测(依原料种类、应用及地区划分)

2026-2034年木质颗粒市场规模、份额、趋势及预测(依原料种类、应用及地区划分) 2026年全球木质颗粒市场报告

2026年全球木质颗粒市场报告 木质颗粒燃料市场-全球产业规模、份额、趋势、机会和预测:按原料、暖气用途、应用、地区和竞争格局划分,2021-2031年日本木屑颗粒市场报告(按原料类型(森林木材和废弃物、农业残余物及其他)、应用(发电厂、住宅供暖、商业供暖、热电联产及其他)和地区划分,2026-2034年)

木质颗粒燃料市场-全球产业规模、份额、趋势、机会和预测:按原料、暖气用途、应用、地区和竞争格局划分,2021-2031年日本木屑颗粒市场报告(按原料类型(森林木材和废弃物、农业残余物及其他)、应用(发电厂、住宅供暖、商业供暖、热电联产及其他)和地区划分,2026-2034年) 木质颗粒市场机会、成长要素、产业趋势分析及2026年至2035年预测

木质颗粒市场机会、成长要素、产业趋势分析及2026年至2035年预测 木质颗粒市场规模、份额和成长分析(按原料、应用、最终用途和地区划分)-2026-2033年产业预测

木质颗粒市场规模、份额和成长分析(按原料、应用、最终用途和地区划分)-2026-2033年产业预测 工业木质颗粒市场规模、份额及成长分析(依原料、应用、最终用途及地区划分)-2026-2033年产业预测

工业木质颗粒市场规模、份额及成长分析(依原料、应用、最终用途及地区划分)-2026-2033年产业预测 2025-2030 年全球木质颗粒市场预测(按产品类型、原料、应用和分销管道)全球公用事业木质颗粒市场(按原始材料、生产流程、等级、分销管道和应用)预测(2025-2030 年)

2025-2030 年全球木质颗粒市场预测(按产品类型、原料、应用和分销管道)全球公用事业木质颗粒市场(按原始材料、生产流程、等级、分销管道和应用)预测(2025-2030 年)