|

市场调查报告书

商品编码

1683884

北美 NMC 电池组:市场占有率分析、行业趋势和统计、成长预测(2025-2029 年)North America NMC Battery Pack - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

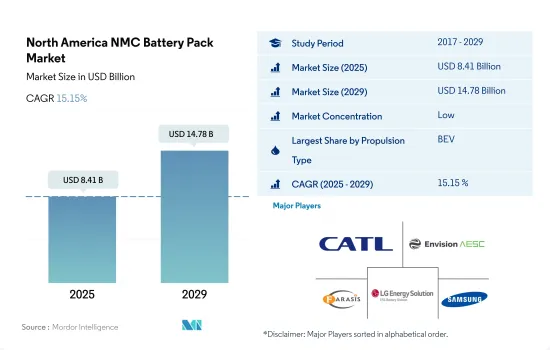

北美 NMC 电池组市场规模估计预计在 2025 年为 84.1 亿美元,预计到 2029 年将达到 147.8 亿美元,在预测期内(2025-2029 年)的复合年增长率为 15.15%。

电动车需求成长推动北美 NCM 电池组市场成长

- NCM 电池组需求的不断增长主要受到电动车(EV)需求激增的推动,电动车严重依赖 NCM 电池组进行能源储存。技术进步正在提高电池密度,延长电动车的续航里程。 2015年NCM电池组平均密度约150Wh/kg。预计 2020 年将激增至 250Wh/kg,2025 年将达到 350Wh/kg。密度的提高也降低了每千瓦时 (kWh) 的能源储存成本。 2010 年,成本约为 1,000 美元/千瓦时,但到 2020 年已骤降至 137 美元/千瓦时。预测到 2025 年将进一步下降至 100 美元/度。

- 北美正在积极研究和投资NCM电池组技术。 2020年,通用汽车宣布将投资22亿美元在俄亥俄州新建电池厂。值得注意的是,特斯拉、福特、Rivian等其他产业巨头也大力投资NCM电池组的研发。

- 在技术进步和电动车日益普及的推动下,北美 NCM 电池组的未来前景光明。这一轨迹将推动市场大幅成长并带来无数机会。在北美,向 NCM 电池组的转变将持续下去,到 2026 年 NCM 811 将成为主导电池化学成分。此外,政府推动电动车普及的政策和措施预计将进一步推动北美 NCM 电池市场的扩张。

本土生产和原料供应推动美国电池组产业扩张

- 北美NMC电池组市场正经历显着成长,前景光明。在北美,由于政府奖励、环境法规和消费者对永续交通途径的兴趣等因素,电动车的普及率正在增加。对电动车的需求不断增长,也增加了对 NMC 电池组的需求。

- 主要汽车製造商和电池製造商正在投资扩大北美NMC电池组的生产能力。其中包括建立或扩大製造设施以满足日益增长的电动车需求,并实现电池组的本地化生产。此外,NMC 电池所需原料(如镍、锰和钴)的供应和成本可能会影响市场。为了确保 NMC 电池组的永续生产,我们正在努力实现原材料供应链多样化,减少对昂贵或稀缺原材料的依赖。

- 由于规模经济、技术进步和生产流程优化,NMC电池组的成本正在随着时间的推移而下降。成本降低有助于降低电动车的价格并加速其市场普及。伙伴关係旨在汇集资源、共用专业知识并推动 NMC 电池技术的创新。此次合作将有助于2024年至2029年NMC电池组在市场上的持续提升与竞争力。

北美NMC电池组市场趋势

北美电动车市场的主要企业包括特斯拉、丰田、福特、现代和本田。

- 北美电动车市场将由五大公司强力推动,到2023年将占据70%以上的市场份额,这些领先企业包括特斯拉、丰田集团、福特集团、现代汽车和本田。特斯拉是北美最大的电动车销售商,占约33%的市场。该公司专注于强大的创新技术,并与各种电动车零件(例如电池)製造商建立了强大的策略伙伴关係。作为一家美国公司,我们提供优质的产品和服务,并在北美的美国和加拿大等主要国家拥有强大的基本客群。

- 丰田集团是北美第二大电动车销售商,市场占有率约30.8%。该公司拥有强大的供应链和分销网络。丰田在客户中拥有值得信赖的品牌形象。其电动车销量在北美国家中排名第三。福特集团以约9.9%的市场占有率收购了它。凭藉强大的品牌形象和多样化的产品,在北美国家拥有庞大的基本客群。

- 现代汽车位居第四,在北美电动车销售市场占有率。凭藉强大的生产和供应链网络,该公司为不同类型的客户提供从实惠到高端定价的各种创新和多样化产品。本田在电动车市场排名第五,市场占有率约5.22%。在北美销售电动车的其他公司包括吉普、雪佛兰、宝马和沃尔沃。

美国是最大的电动车市场,需求庞大,到 2023 年将占全部区域电池组市场的 60% 以上。

- 随着北美几个国家的电动车数量稳定成长,2023 年对电池的需求将飙升。虽然该地区销售许多其他品牌和车型,但 2023 年排名前五的车型——特斯拉 Model Y、特斯拉 Model 3、丰田 Rav 4、丰田 Sienta 和本田 CRV——占据了相当大的市场份额。特斯拉 Model Y 在 2023 年以 247,344 辆的销量继续保持美国销量第一的宝座。 Model Y 因其续航里程长、座位数多、载货负载容量足而极受欢迎。

- 特斯拉Model 3位居第二,2023年在美国售出215,500辆,有后轮驱动和性能版本可供选择。由于强大的效能特性,Model 3 正在吸引客户。在电动车销量方面,ToyotaRav4在美国和北美的销量为149,938辆,排名第三。该车配备了插电式混合动力技术和包括 Toyota Safety Sense 在内的多项 ADAS 功能。

- Toyota Sienta 是美国第四畅销的电动车,销量为 69,720 辆。该车可选配 2.5 升引擎和混合动力传动系统。那些拥有大家庭且需要七人座的消费者对于丰田 Sienna 的反应非常好。排名第五的是本田CRV,2023年美国销量为69,720辆。其他畅销车型包括丰田Highlander、吉普牧马人、丰田凯Camry、本田雅阁和福特野马 Mach-E。

北美NMC电池组产业概况

北美NMC电池组市场较为分散,前五大公司占比为2.97%。市场的主要企业有:宁德时代新能源科技(CATL)、远景 AESC 日本、孚能科技(赣州)、LG 能源解决方案有限公司和三星 SDI(按字母顺序排列)。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章执行摘要和主要发现

第二章 报告要约

第 3 章 简介

- 研究假设和市场定义

- 研究范围

- 调查方法

第四章 产业主要趋势

- 电动汽车销售

- 电动车销量(按OEM)

- 最畅销的电动车车型

- 具有首选电池化学成分的OEM

- 电池组价格

- 电池材料成本

- 每种电池化学成分的价格表

- 谁供给谁?

- 电动车电池容量和效率

- 发布的电动车车型数量

- 法律规范

- 北美洲

- 价值链与通路分析

第五章 市场区隔

- 体型

- 公车

- LCV

- M&HDT

- 搭乘用车

- 推进类型

- BEV

- PHEV

- 容量

- 15 kWh~40 kWh

- 40 kWh~80 kWh

- 超过80度

- 少于15千瓦时

- 电池形状

- 圆柱形

- 小袋

- 方块

- 方法

- 雷射

- 金属丝

- 成分

- 阳极

- 阴极

- 电解

- 分隔符

- 材料类型

- 钴

- 锂

- 锰

- 天然石墨

- 镍

- 其他材料

- 国家名称

- 加拿大

- 美国

第六章 竞争格局

- 主要策略趋势

- 市场占有率分析

- 业务状况

- 公司简介

- A123 Systems LLC

- ACDELCO(Subsidiary Of General Motors)

- American Battery Solutions Inc.

- Clarios International Inc.

- Contemporary Amperex Technology Co. Ltd.(CATL)

- Electrovaya Inc.

- Envision AESC Japan Co. Ltd.

- Farasis Energy(Ganzhou)Co. Ltd.

- LG Energy Solution Ltd.

- Nikola Corporation

- QuantumScape Corp.

- Samsung SDI Co. Ltd.

第七章:执行长的关键策略问题

第 8 章 附录

- 世界概况

- 概述

- 五力分析框架

- 全球价值链分析

- 市场动态(DRO)

- 资讯来源和进一步阅读

- 图片列表

- 关键见解

- 资料包

- 词彙表

The North America NMC Battery Pack Market size is estimated at 8.41 billion USD in 2025, and is expected to reach 14.78 billion USD by 2029, growing at a CAGR of 15.15% during the forecast period (2025-2029).

Increasing demand for BEVs is driving growth in the North American NCM battery pack market

- The rising demand for NCM battery packs is primarily fueled by the surging need for electric vehicles (EVs), which heavily rely on these packs for energy storage. Technological advancements have led to an uptick in battery density, translating to increased EV ranges. In 2015, the average density of NCM battery packs stood at approximately 150 Wh/kg. By 2020, it had surged to 250 Wh/kg, and projections indicate it will hit 350 Wh/kg by 2025. This densification has also driven down the cost per kilowatt-hour (kWh) of energy storage. In 2010, the cost was roughly USD 1,000/kWh, which plummeted to USD 137/kWh by 2020. Forecasts suggest it will further dip to USD 100/kWh by 2025.

- North America is witnessing a flurry of research and investments in NCM battery pack technology. In 2020, General Motors unveiled a USD 2.2 billion investment for a new Ohio-based battery factory, dedicated to NCM battery pack production for their upcoming EV lineup. Notably, other industry giants like Tesla, Ford, and Rivian are also channeling significant investments into NCM battery pack R&D.

- The future of NCM battery packs in North America appears bright, propelled by technological strides and the growing EV adoption. This trajectory is poised to fuel substantial market growth, opening up a plethora of opportunities. In North America, the shift toward NCM battery packs is set to persist, with NCM 811 emerging as the dominant battery chemistry by 2026. Furthermore, governmental policies and initiatives aimed at bolstering EV adoption are anticipated to further catalyze the NCM battery market's expansion in North America.

Local production and raw material supply drive the expansion of the battery pack industry in the United States

- The North American market for NMC battery packs was experiencing significant growth and had a promising outlook. The adoption of EVs in North America has been increasing, driven by factors such as government incentives, environmental regulations, and consumer interest in sustainable transportation. This growing demand for EVs is fueling the need for NMC battery packs.

- Major automakers and battery manufacturers have been investing in expanding their production capacity for NMC battery packs in North America. This includes establishing or expanding manufacturing facilities to meet the rising demand for EVs and localize battery pack production. Furthermore, the availability and cost of raw materials needed for NMC batteries, such as nickel, manganese, and cobalt, can impact the market. Diversification of the raw material supply chain and efforts to reduce reliance on expensive or scarce materials are ongoing to ensure the sustainable production of NMC battery packs.

- The cost of NMC battery packs has decreased over time due to economies of scale, technological advancements, and optimization of production processes. This cost reduction helps make EVs more affordable and accelerates their market adoption. Partnerships aim to pool resources, share expertise, and drive innovation in NMC battery technology. These collaborations contribute to the continuous improvement and competitiveness of NMC battery packs in the market during 2024-2029.

North America NMC Battery Pack Market Trends

The major players in the North American electric vehicle market include Tesla, Toyota, Ford, Hyundai, and Honda

- The North American electric vehicle market is majorly driven by the five major players, accounting for more than 70% of the market in 2023. These prominent players include Tesla, Toyota Group, Ford Group, Hyundai, and Honda. Tesla is the highest seller of electric vehicles in the various North American countries, accounting for around 33% of the market. The company focuses on strong innovation technologies and has strong strategic partnerships with various EV components (such as a battery) manufacturers. Being a US-based company, it has a strong customer base with great product and service offerings in major countries like the United States and Canada across North America.

- Toyota Group is the second largest seller of electric vehicles, accounting for around 30.8% market share across North America. The company has a strong supply chain and distribution network. Toyota has a reliable brand image among its customers. It ranks third in EV sales across various countries in North America. Ford Group acquired it with around 9.9% of the market share. The company has a large customer base in North American countries due to its strong brand image and diverse offerings.

- Hyundai is the fourth largest player, acquiring around 5.48% of the market share in EV sales across North America. The company has a strong production and supply chain network, with wide innovative and diverse products offered for various types of customers looking from reasonable to premium pricing. The fifth-largest player operating in the EV market is Honda, maintaining its market share at around 5.22%. Some of the other players selling EVS in North America include Jeep, Chevrolet, BMW, and Volvo.

The United States was the largest market with huge EV demand and captured more than 60% of the battery pack market across the region in 2023

- In 2023, the demand for batteries surged as the number of electric vehicles steadily climbed across several North American countries. Many other brands and models are sold in the region, but the top five models in 2023, the Tesla Model Y, Tesla Model 3, Toyota Rav 4, Toyota Sienna, and Honda CRV, acquired a significant portion of the market. With 247,344 units sold in the United States in 2023, the Tesla Model Y maintained its top spot. The Model Y is very well-liked because of its long range, strong seating capacity, and huge luggage capacity.

- The Tesla Model 3 took second place with 215,500 sales in the United States in 2023. The rear-wheel drive and performance versions of the vehicle are available. Due to its strong performance characteristics, Model 3 is drawing customers. The Toyota Rav4 took third position in electric car sales, with sales of 149,938 in the United States and throughout North America. The vehicle has plug-in hybrid technology and several ADAS features, including Toyota Safety Sense.

- The Toyota Sienna has acquired fourth place in the electric vehicle models' sales, with 69,720 in the United States. The car comes with the option of a 2.5 l engine with a hybrid powertrain. Consumers with big families looking for seven-seater cars have positively responded to the Toyota Sienna. The fifth place was acquired by the Honda CRV, selling 69,720 units in 2023 in the United States. Other top-selling models include Toyota Highlander, Jeep Wrangler, Toyota Camry, Honda Accord, and Ford Mustang Mach-E.

North America NMC Battery Pack Industry Overview

The North America NMC Battery Pack Market is fragmented, with the top five companies occupying 2.97%. The major players in this market are Contemporary Amperex Technology Co. Ltd. (CATL), Envision AESC Japan Co. Ltd., Farasis Energy (Ganzhou) Co. Ltd., LG Energy Solution Ltd. and Samsung SDI Co. Ltd. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Electric Vehicle Sales

- 4.2 Electric Vehicle Sales By OEMs

- 4.3 Best-selling EV Models

- 4.4 OEMs With Preferable Battery Chemistry

- 4.5 Battery Pack Price

- 4.6 Battery Material Cost

- 4.7 Price Chart Of Different Battery Chemistry

- 4.8 Who Supply Whom

- 4.9 EV Battery Capacity And Efficiency

- 4.10 Number Of EV Models Launched

- 4.11 Regulatory Framework

- 4.11.1 North America

- 4.12 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

- 5.1 Body Type

- 5.1.1 Bus

- 5.1.2 LCV

- 5.1.3 M&HDT

- 5.1.4 Passenger Car

- 5.2 Propulsion Type

- 5.2.1 BEV

- 5.2.2 PHEV

- 5.3 Capacity

- 5.3.1 15 kWh to 40 kWh

- 5.3.2 40 kWh to 80 kWh

- 5.3.3 Above 80 kWh

- 5.3.4 Less than 15 kWh

- 5.4 Battery Form

- 5.4.1 Cylindrical

- 5.4.2 Pouch

- 5.4.3 Prismatic

- 5.5 Method

- 5.5.1 Laser

- 5.5.2 Wire

- 5.6 Component

- 5.6.1 Anode

- 5.6.2 Cathode

- 5.6.3 Electrolyte

- 5.6.4 Separator

- 5.7 Material Type

- 5.7.1 Cobalt

- 5.7.2 Lithium

- 5.7.3 Manganese

- 5.7.4 Natural Graphite

- 5.7.5 Nickel

- 5.7.6 Other Materials

- 5.8 Country

- 5.8.1 Canada

- 5.8.2 US

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 A123 Systems LLC

- 6.4.2 ACDELCO (Subsidiary Of General Motors)

- 6.4.3 American Battery Solutions Inc.

- 6.4.4 Clarios International Inc.

- 6.4.5 Contemporary Amperex Technology Co. Ltd. (CATL)

- 6.4.6 Electrovaya Inc.

- 6.4.7 Envision AESC Japan Co. Ltd.

- 6.4.8 Farasis Energy (Ganzhou) Co. Ltd.

- 6.4.9 LG Energy Solution Ltd.

- 6.4.10 Nikola Corporation

- 6.4.11 QuantumScape Corp.

- 6.4.12 Samsung SDI Co. Ltd.

7 KEY STRATEGIC QUESTIONS FOR EV BATTERY PACK CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

锂镍锰尖晶石市场按产品类型、最终用户、合成方法、应用和分销管道划分,全球预测(2026-2032年)

锂镍锰尖晶石市场按产品类型、最终用户、合成方法、应用和分销管道划分,全球预测(2026-2032年) 镍锰钴电池市场成长、规模和趋势分析 - 按类型和应用 - 区域展望、竞争策略和细分预测(截至 2034 年)

镍锰钴电池市场成长、规模和趋势分析 - 按类型和应用 - 区域展望、竞争策略和细分预测(截至 2034 年) 全球镍锰钴 (NMC) 电池市场

全球镍锰钴 (NMC) 电池市场 NMC 电池组:市场占有率分析、行业趋势和统计、成长预测(2025-2029 年)亚太地区 NMC 电池组市场占有率分析、产业趋势与统计、成长预测(2025-2029 年)欧洲 NMC 电池组:市场占有率分析、行业趋势和统计、成长预测(2025-2029 年)

NMC 电池组:市场占有率分析、行业趋势和统计、成长预测(2025-2029 年)亚太地区 NMC 电池组市场占有率分析、产业趋势与统计、成长预测(2025-2029 年)欧洲 NMC 电池组:市场占有率分析、行业趋势和统计、成长预测(2025-2029 年) 镍锰钴 (NMC) 电池市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

镍锰钴 (NMC) 电池市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测