|

市场调查报告书

商品编码

1683933

中国汽车 LED 照明:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)China Automotive LED Lighting - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

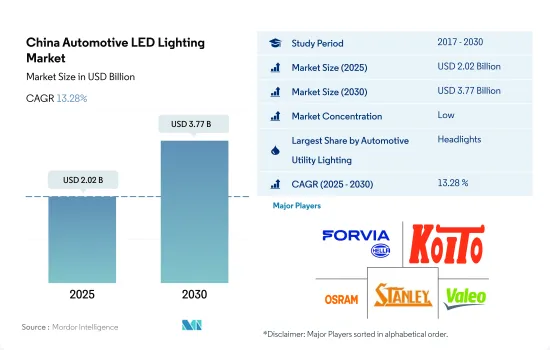

预计2025年中国汽车LED照明市场规模为20.2亿美元,到2030年将达到37.7亿美元,预测期间(2025-2030年)的复合年增长率为13.28%。

汽车采用 LED 灯可减少事故发生

- 2023年,头灯将占据中国汽车照明市场大部分金额份额,其次是其他灯和方向灯。转向信号灯和煞车灯的市场占有率预计将保持不变,而前照灯的市场份额预计在预测期内将略有下降。市场上的一个新趋势是将DRL(日间行车灯)与投影灯相结合的头灯,上汽汽车、吉利汽车等知名厂商即将推出的车型将配备这种头灯。此外,由于事故发生率呈上升趋势, LED灯的采用率也预计将增加。 2019年,全国道路交通事故受伤人数为25,6101人,死亡人数为6,2,763人,较2016年有较大成长。

- 从出货量份额来看,2022年方向灯将占多数,其次是头灯和其他。预计这些灯的市场占有率将保持相对稳定,波动不大。在所有类型的车辆中,方向灯都是一个主要部件,在轻微至重大事故中很可能会受到影响并需要更换。

- 中国汽车市场竞争激烈,比亚迪、上汽、吉利、宝马、宾士等老牌汽车製造商以及蔚来、小鹏、理想汽车等中国新能源汽车新兴企业都在争夺市场占有率。对电动车的追求也吸引了小米和百度等科技巨头的注意。因此,新能源汽车的成长可能会增加 LED 的市场渗透率。

中国汽车LED照明市场趋势

亚太地区汽车 LED 照明技术创新不断提升,将推动整体 LED 市场发展

- 预计2022年中国汽车总产量将达4,668万辆,2023年将达4,949万辆。中国汽车供应业受到新冠肺炎疫情的严重影响。海上运输受到不利影响,由于工厂和组装关闭导致需求大幅下降,关键的汽车零件不再透过大型货柜运往欧洲。结果,该航线的货柜船和生产商船队数量减少了30%。汽车零件的中断对汽车使用的 LED 照明产生了负面影响。

- 上汽汽车、吉利汽车、长城汽车、奇瑞汽车、一汽集团是中国顶级汽车製造商。上汽集团是一家知名公司,正在大力投资人工智慧(AI)技术、智慧燃料电池和汽车智慧互联。由于这些发展,LED 作为汽车连网技术的使用预计会增加。

- LED 照明现在被视为汽车应用的明显选择,因为它环保且本质上节能。 LED 灯有助于创造创新的照明概念,从而增强汽车的外观。主要企业正在合作开发用于汽车行业的技术 LED 产品。例如,2022年9月,ams Osram与TactoTek共同开发了一款搭载前卫RGB侧视LED OSIRE E5515的示范器。它可以轻鬆整合到车辆中,实现更紧凑的设计。预计在预测期内,此类创新和即将到来的汽车 LED 照明投资将推动市场发展。

电动车需求成长将推动市场成长

- 儘管受到新冠疫情影响并导致供应链受限,中国的电动车 (EV) 市场仍呈现强劲成长。儘管近期电动车销售遭遇挫折且原物料价格上涨导致生产成本上升,但电动车销售仍持续快速成长。截至年终,中国将拥有约160万座电动车充电站和521万个充电桩(其中2022年已建成超过259万个)。此外,至2022年,全国将建成换电站1973座,其中2022年建成换电站675座,动力电池回收服务店将超过1万家。因此,充电设施的快速增加表明该国新能源汽车(NEV)产业的蓬勃发展。

- 在销售成长放缓的情况下,中国计划延长电动车税收优惠政策。购买电动车和插电式混合动力汽车可减税高达 30 万元人民币(42,062.76 美元)(最高减税 195,000 元人民币(27,340.03 美元))。在中国,高于这个标准的车都被广泛归类为豪华车,这使得人们更容易购买更实惠的清洁能源汽车。这些因素可能会推动中国电动车的普及,并帮助该国实现 2060 年实现净零排放的目标。

- 2023年5月,罗杰斯宣布将在中国建造新基板,生产电源基板,以便更好地服务国内外客户,满足电动和混合动力汽车(EV/HEV)以及可再生能源应用领域对电源电路板日益增长的需求。扩建工程一期预计于2025年完工。为因应电动车日益增长的需求,汽车製造商竞相开发生产新能源车,从而带动了汽车LED的需求。 LED 汽车灯比卤素灯泡消耗的能量更少,有助于节省能源并延长电动车的行驶里程。

中国汽车LED照明产业概况

中国汽车LED照明市场较为分散,前五大企业的市占率达到35.95%。市场的主要企业是:HELLA GmbH & Co. KGaA (FORVIA)、KOITO MANUFACTURING、OSRAM GmbH.、Stanley Electric 和 Valeo(按字母顺序排列)。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章执行摘要和主要发现

第二章 报告要约

第 3 章 简介

- 研究假设和市场定义

- 研究范围

- 调查方法

第四章 产业主要趋势

- 汽车产量

- 人口

- 人均收入

- 汽车贷款利率

- 充电站数量

- 汽车持有量

- LED进口总量

- #家庭数量

- 道路网络

- 渗透率

- 法律规范

- 中国

- 价值链与通路分析

第五章 市场区隔

- 汽车实用照明

- 日间行车灯 (DRL)

- 方向指示器

- 头灯

- 倒车灯

- 红绿灯

- 尾灯

- 其他的

- 汽车照明

- 二轮车

- 商用车

- 搭乘用车

第六章 竞争格局

- 主要策略趋势

- 市场占有率分析

- 业务状况

- 公司简介(包括全球概况、市场层级概况、主要业务部门、财务状况、员工人数、关键资讯、市场排名、市场占有率、产品和服务、最新发展分析)

- Changzhou Xingyu Automotive Lighting System Co, Ltd.

- Hasco Vision Technology Co., Ltd.

- HELLA GmbH & Co. KGaA(FORVIA)

- HYUNDAI MOBIS

- KOITO MANUFACTURING CO., LTD.

- Nichia Corporation

- OSRAM GmbH.

- Stanley Electric Co., Ltd.

- Sunway Autoparts

- Valeo

第七章:执行长的关键策略问题

第 8 章 附录

- 世界概况

- 概述

- 五力分析框架

- 全球价值链分析

- 市场动态(DRO)

- 资讯来源和进一步阅读

- 图片列表

- 关键见解

- 资料包

- 词彙表

简介目录

Product Code: 50001631

The China Automotive LED Lighting Market size is estimated at 2.02 billion USD in 2025, and is expected to reach 3.77 billion USD by 2030, growing at a CAGR of 13.28% during the forecast period (2025-2030).

The use of LED lights in automobiles has resulted in a decrease in the number of accidents

- In 2023, headlights accounted for the majority of value share in the Chinese automobile lighting market, followed by others and directional signal lights. During the forecast period, the market share for directional signal lights and stoplights is expected to remain the same, with a slight decrease in headlights. An emerging trend in the market is the combination of DRLs (daytime running lamps) with projector lights in frontal illumination, which is being incorporated into forthcoming vehicles by notable manufacturers such as SAIC and Geely. The rising trend of accidents has also led to an anticipated increase in the penetration rate of fog LED lamps. In 2019, there were 256,101 injuries and 62,763 fatalities in traffic accidents in China, which has significantly increased since 2016.

- In terms of volume share, directional signal lights accounted for the majority in 2022, followed by headlights and others. The market share for these lights is expected to remain relatively stable with less fluctuation. In all types of vehicles, directional signal lights are the main component that has a high probability of getting affected in minor to major accidents and require replacement.

- The Chinese automobile market is highly competitive, with Chinese NEV (New Electric Vehicle) start-ups such as NIO, XPeng, and Li Auto vying for market share alongside established automakers such as BYD, SAIC Motors, Geely, BMW, and Mercedes-Benz. The quest for electric vehicles has also attracted tech giants such as Xiaomi and Baidu. Thus, the growth in NEV would increase the penetration of LED in the market.

China Automotive LED Lighting Market Trends

Growing innovation in automotive LED light in the Asia-Pacific region will boost the overall LED market

- The total automobile vehicle production in China was 46.68 million units in 2022, and it is expected to reach 49.49 million units in 2023. The automotive supply industry in China was severely affected by COVID-19. Maritime transportation was negatively impacted, and critical automotive parts were no longer sent in large quantities of containers to Europe, mainly because of a substantial decline in demand brought on by the closure of plants and assembly lines. Thus, the fleets of container carriers and producers on trade routes decreased by 30%. This disruption in automotive parts negatively impacted LED lights used in automobiles.

- SAIC Motor, Geely, Great Wall Motor, Chery, FAW Group, and other companies are among the nation's top automakers. One prominent business, SAIC Motor, is making significant investments in artificial intelligence (AI) technology, smart fuel cells, and intelligent interconnection for use in automobiles. The use of LEDs as a connected technology in vehicles is anticipated to increase due to this progress.

- Due to LED lights' environmental friendliness and innate energy efficiency, they are currently seen as a natural choice in automotive applications. They help create innovative lighting concepts that enhance a vehicle's looks. Companies are working together to develop technological LED products for the automobile industry. For instance, ams OSRAM and TactoTek collaborated to create a demonstrator in September 2022 that featured an avant-garde RGB side-looker LED OSIRE E5515. It can be easily incorporated into the interior of a car to create a more compact design. Such innovations and future investments in automotive LED lights will drive the market during the forecast period.

Growing demand for EVs drives the market growth

- Despite the COVID-19 pandemic and the ensuing supply chain constraints, the electric vehicle (EV) market has grown significantly in China. EV sales are continuing to increase rapidly despite recent obstacles and rising production costs due to rising raw material prices. China had around 1.6 million EV charging stations and 5.21 million charging points at the end of 2022, including over 2.59 million built in 2022. Furthermore, by 2022, the country had 1,973 battery swapping stations, including 675 built in 2022, adding that China has over 10,000 power battery recycling service outlets. Thus, the rapid growth in charging facilities indicates the booming new energy vehicle (NEV) sector in the country.

- China is set to extend EV tax incentives as sales growth slows. The purchase tax break for EVs and plug-in hybrids costs less than CNY 300,000 (USD 42062.76) (CNY 195,000 (USD 27340.03)). Vehicles over that amount are broadly classed as luxury vehicles in China, making it easier for people to buy more affordable, clean cars. These factors would boost the nation's EV adoption rate and further its goal of reaching net zero emissions by 2060.

- In May 2023, Rogers announced the construction of a new factory in China to produce its power substrates to serve both its local and international clients better and to meet the rising demand for power substrates used in electric and hybrid electric vehicles (EVs/HEVs) and renewable energy applications. The expansion's first phase is expected to be finished in 2025. Automobile manufacturers are racing to develop and produce new energy vehicles because of the growing demand for EVs, which boosts the demand for automotive LEDs. LED car lights can help EVs save energy and extend their driving range, as they consume less power than halogen bulbs.

China Automotive LED Lighting Industry Overview

The China Automotive LED Lighting Market is fragmented, with the top five companies occupying 35.95%. The major players in this market are HELLA GmbH & Co. KGaA (FORVIA), KOITO MANUFACTURING CO., LTD., OSRAM GmbH., Stanley Electric Co., Ltd. and Valeo (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Automotive Production

- 4.2 Population

- 4.3 Per Capita Income

- 4.4 Interest Rate For Auto Loans

- 4.5 Number Of Charging Stations

- 4.6 Number Of Automobile On-road

- 4.7 Total Import Of Leds

- 4.8 # Of Households

- 4.9 Road Networks

- 4.10 Led Penetration

- 4.11 Regulatory Framework

- 4.11.1 China

- 4.12 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Automotive Utility Lighting

- 5.1.1 Daytime Running Lights (DRL)

- 5.1.2 Directional Signal Lights

- 5.1.3 Headlights

- 5.1.4 Reverse Light

- 5.1.5 Stop Light

- 5.1.6 Tail Light

- 5.1.7 Others

- 5.2 Automotive Vehicle Lighting

- 5.2.1 2 Wheelers

- 5.2.2 Commercial Vehicles

- 5.2.3 Passenger Cars

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 Changzhou Xingyu Automotive Lighting System Co, Ltd.

- 6.4.2 Hasco Vision Technology Co., Ltd.

- 6.4.3 HELLA GmbH & Co. KGaA (FORVIA)

- 6.4.4 HYUNDAI MOBIS

- 6.4.5 KOITO MANUFACTURING CO., LTD.

- 6.4.6 Nichia Corporation

- 6.4.7 OSRAM GmbH.

- 6.4.8 Stanley Electric Co., Ltd.

- 6.4.9 Sunway Autoparts

- 6.4.10 Valeo

7 KEY STRATEGIC QUESTIONS FOR LED CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

02-2729-4219

+886-2-2729-4219

汽车LED照明市场:依产品类型、技术、车辆类型及销售管道划分-2026-2032年全球市场预测

汽车LED照明市场:依产品类型、技术、车辆类型及销售管道划分-2026-2032年全球市场预测 2026年全球汽车LED照明市场报告

2026年全球汽车LED照明市场报告 汽车LED照明市场-全球产业规模、份额、趋势、机会、预测:按位置、车辆类型、自适应照明、地区和竞争格局划分,2021-2031年

汽车LED照明市场-全球产业规模、份额、趋势、机会、预测:按位置、车辆类型、自适应照明、地区和竞争格局划分,2021-2031年 汽车LED照明市场规模、份额和成长分析(按技术类型、车辆类型、类型和地区划分)-产业预测(2026-2033年)

汽车LED照明市场规模、份额和成长分析(按技术类型、车辆类型、类型和地区划分)-产业预测(2026-2033年) 汽车用LED的世界市场趋势:照明和显示器预测

汽车用LED的世界市场趋势:照明和显示器预测 汽车LED照明市场:2025年至2030年预测

汽车LED照明市场:2025年至2030年预测 全球汽车LED市场(2025年)- 照明与显示产品趋势全球汽车LED尾灯市场:未来预测(2025-2030)

全球汽车LED市场(2025年)- 照明与显示产品趋势全球汽车LED尾灯市场:未来预测(2025-2030) 汽车用LED照明的全球市场:车辆类别,各销售管道,各应用类型,各地区,机会,预测,2018年~2032年

汽车用LED照明的全球市场:车辆类别,各销售管道,各应用类型,各地区,机会,预测,2018年~2032年 中东和非洲汽车 LED 照明:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)

中东和非洲汽车 LED 照明:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)

▼