|

市场调查报告书

商品编码

1683937

欧洲室内 LED 照明:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)Europe Indoor LED Lighting - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

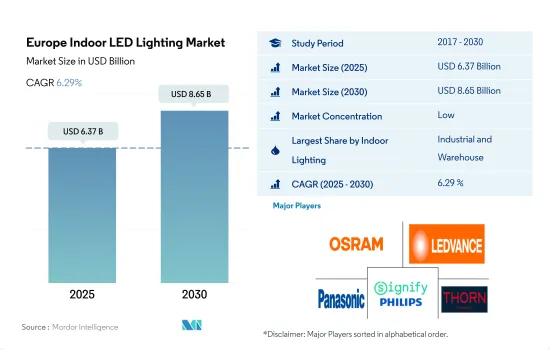

预计 2025 年欧洲室内 LED 照明市场规模为 63.7 亿美元,到 2030 年将达到 86.5 亿美元,预测期内(2025-2030 年)的复合年增长率为 6.29%。

工业和住宅领域的发展不断加快,推动市场成长

- 就以金额为准,到 2023 年,工业和仓库照明将占据最大份额,其次是商业、住宅和农业照明。法国、俄罗斯和波兰占仓库建设的大部分。新冠肺炎疫情危机加速了法国恢復工业能至疫情前水准的努力。 2022年12月,法国工业生产成长1.1%,11月则成长了2%。波兰拥有近440万平方公尺的土地。到 2022 年中期,波兰将建造近 450 万平方公尺的仓库和工业空间。

- 在商业设施中,医院、学校和机场占据了大部分市场。在受访的42个国家中,可支配所得差异很大。列支敦士登、瑞士和卢森堡的可支配收入最高,因此人们更容易负担学校或大学的学费。

- 截至 2023 年,住宅领域将占最大份额。在强劲需求的支撑下,义大利住宅市场保持稳定。 2021年第四季住宅房地产交易量年增14.1%至263,795套。所有地区的销售额均强劲成长。自 2022 年 1 月上一次封锁结束以来,儘管许多企业正处于转型期,但办公室入住率仍持续呈上升趋势。截至 2022 年第三季度,办公大楼领域的平均折扣为 26%,低于 31% 的整体平均值。 年终整体空置率为7.2%,与年终相比大致稳定(+10bp)。整体而言,办公室及住宅的吸收率呈上升趋势,带动LED需求大幅增加。

工业生产成长与住宅需求旺盛推动市场需求

- 截至 2023 年,就金额和数量而言,其他欧洲国家占最大份额,其次是法国、德国和英国。其他欧洲国家包括瑞典、义大利、西班牙、俄罗斯、波兰和荷兰。来自美国和斯堪的纳维亚半岛的外国买家正在西班牙南海岸购买住宅。儘管房屋抵押贷款利率大幅上升,但 2022 年房地产需求依然强劲,交易数量较 2021 年激增 16%,房屋抵押贷款发放数量增加 11%。在欧洲,波兰以约 440 万平方公尺的土地面积处于领先地位。到 2022 年中期,波兰将建造近 450 万平方公尺的仓库和工业空间。总体而言,由于该地区仓库建设的增加和住宅的蓬勃发展,预计 LED 的需求将会增加。

- 在法国(马约特岛除外),2022 年前 11 个月的新建筑许可证年增 5.6%,至 448,416 套,而 2021 年全年则增长了 18.5%。自从新冠疫情封锁以来,法国许多人从大城市搬到了乡村。总体而言,预计未来几年住宅市场将更加稳定。

- 德国工业企业占德国全国研发支出总额的60%左右,为德国的繁荣做出了重大贡献。企业也正在进行策略发展。例如,2023 年,Osvetlenyi Cernoch SRO 建造了一个新的生产和仓储大厅,以提高其工业生产能力。这种扩张意味着工业和仓储空间的增加以及 LED 照明的使用。

欧洲室内 LED 照明市场趋势

可支配收入的增加和政府奖励可能会增加 LED 的采用

- 2022年,欧盟共有1.98亿个居住,平均每个居住有2.2人。该地区人口在2020年为7.462亿,但预计到2023年将减少至7.422亿。欧盟住房自有率从2021年的69.90%下降到2022年的69.10%。这些案例表明,儘管家庭数量略有下降,但住宅开发计划比平时少。因此,预计 LED 渗透率将呈正增长,但与先前相比,其在住宅领域的增长速度较低。

- 在欧洲,大多数国家的可支配收入都很高,这反过来又增加了个人消费能力,尤其是在新住宅空间方面的消费能力。 2022年英国的人均所得达到3,3,138美元,法国达到2,5,337.7美元。

- 在欧洲,各国政府正在提供奖励计划来促进 LED 的普及。英国政府公布了节能照明的新提案。根据该提案,耗能较低的照明设备(如 LED)将取代旧款卤素灯泡。此类措施可以在灯泡的使用寿命内为家庭节省 2,000 至 3,000 英镑。 2021年1月,德国启动「联邦资助高效建筑」计画。任何在德国拥有或考虑购买房产的人都可以申请这笔资金。该能源效率计划还包括照明节能建筑。 2017年6月,法国政府宣布了一项能源效率证书计划,允许家庭根据其收入获得最高LED灯泡价格100%的补贴。预计此类案例将在预测期内推动该地区对 LED 照明的需求。

政府专案和卤素灯销售禁令或将刺激 LED 照明成长

- 工业部门是欧盟主要的能源消耗部门之一,2021年占总能源消费量的25.6%,其次是住宅和商业部门,是最大的能源用户。随着大量家庭转向智慧家庭技术,住宅等室内空间照明控制的需求正在以意想不到的速度增长。 2020 年 9 月宣布的《欧洲绿色交易》的核心内容是欧盟政府实施的住宅改造计画。这些项目正在帮助该地区扩大 LED 照明。

- 商业用电需求往往在8-10小时左右,而工业用电全天和全年保持一致。住宅用电需求在7-9小时左右波动。市长会议示范产业计画维修了坎泰米尔市的 27 条道路,并安装了 419 盏智慧 LED 灯。在奥国田,约有 386 个低效率灯泡已被更换,以减少排放到大气中的二氧化碳量,导致该地区 LED 的使用量增加。

- 2018年9月,该地区也禁止销售非定向卤素灯泡。这些法律的变化使消费者更容易逐步从传统照明转向 LED 技术。该地区的各国政府也正在逐步淘汰老旧、效率较低的技术,以提高消费者对 LED 产品的接受度,并提供补贴和奖励,以提高该地区 LED 的整体效率。

欧洲室内LED照明产业概况

欧洲室内LED照明市场较为分散,前五大企业占比为37.37%。该市场的主要企业是:ams-OSRAM AG、LEDVANCE GmbH(MLS)、松下控股公司、Signify(飞利浦)和Thorn Lighting Ltd.(Zumtobel Group)(按字母顺序排列)。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章执行摘要和主要发现

第二章 报告要约

第 3 章 简介

- 研究假设和市场定义

- 研究范围

- 调查方法

第四章 产业主要趋势

- 人口

- 人均收入

- LED进口总量

- 照明电力消耗量

- 家庭数量

- LED渗透率

- 园艺区

- 法律规范

- 法国

- 德国

- 英国

- 价值链与通路分析

第五章 市场区隔

- 室内照明

- 农业照明

- 商业照明

- 办公室

- 零售

- 其他的

- 工业/仓库

- 住宅

- 国家名称

- 法国

- 德国

- 英国

- 其他欧洲国家

第六章 竞争格局

- 主要策略趋势

- 市场占有率分析

- 业务状况

- 公司简介(包括全球概况、市场层级概况、主要业务部门、财务状况、员工人数、关键资讯、市场排名、市场占有率、产品和服务、最新发展分析)

- ams-OSRAM AG

- Dialight

- EGLO Leuchten GmbH

- LEDVANCE GmbH(MLS Co Ltd)

- NVC INTERNATIONAL HOLDINGS LIMITED

- Panasonic Holdings Corporation

- Signify(Philips)

- Thorlux Lighting(FW Thorpe Plc)

- Thorn Lighting Ltd.(Zumtobel Group)

- TRILUX GmbH & Co. KG

第七章:执行长的关键策略问题

第 8 章 附录

- 世界概况

- 概述

- 五力分析框架

- 全球价值链分析

- 市场动态(DRO)

- 资讯来源和进一步阅读

- 图片列表

- 关键见解

- 资料包

- 词彙表

The Europe Indoor LED Lighting Market size is estimated at 6.37 billion USD in 2025, and is expected to reach 8.65 billion USD by 2030, growing at a CAGR of 6.29% during the forecast period (2025-2030).

Increasing development in the industrial and residential sectors drives market growth

- In terms of value, as of 2023, industrial and warehouse had a major share, followed by commercial, residential, and agricultural lighting. France, Russia, and Poland had the majority of warehouse constructions. The COVID-19 crisis accelerated France's efforts to return industrial production capacities to the pre-pandemic levels. French industrial production increased by 1.1% over one month in December 2022, after +2% in November 2022. Poland has close to 4.4 million sq. m of space. By the middle of 2022, almost 4.5 million sq. m of warehouse and industrial space was under construction in Poland.

- In commercial, hospitals, schools, and airports comprise the majority of the share. The disposable net income among the 42 countries surveyed varies significantly. Liechtenstein, Switzerland, and Luxembourg have the highest disposable net income by a wide margin, which means more affordability for schools and college studies.

- In terms of volume, as of 2023, the residential sector had a major share. Italy's housing market remains stable, supported by strong demand. In Q4 2021, residential property transactions increased by 14.1% to 263,795 units compared to a year earlier. All regions saw a strong sales increase during the period. Despite many businesses remaining in transition, office usage rates continued on an upward trend from the end of the last lockdown in January 2022. As of Q3 2022, the office sector traded at an average discount of 26%, which was below the 31% overall average. The overall vacancy rate stood at 7.2% at the end of 2022, almost stable compared to the end of 2021 (+10bp). Overall, there is a positive trend toward a higher office and residential absorption rate, leading to a major increase in the demand for LEDs.

Growing number of industrial production and surge in residential property drive the demand for market

- In terms of value and volume, as of 2023, the Rest of Europe held the major share, followed by France, Germany, and the United Kingdom. The Rest of Europe comprises Sweden, Italy, Spain, Russia, Poland, Netherlands, and others. Foreign buyers from the United States and northern Europe have been buying homes on Spain's southern coast. Despite a significant rise in mortgage rates, demand for real estate remained strong in 2022, with a 16% surge in transactions and an 11% uptick in mortgage production compared to 2021. In Europe, Poland was at the top with nearly 4.4 million sq. m of space. By the middle of 2022, almost 4.5 million sq. m of warehouse and industrial space was under construction in Poland. Overall, the demand for LEDs is expected to increase with increasing warehouse construction and a surge in residential property in the region.

- In the first eleven months of 2022, new dwellings authorized in France, excluding Mayotte, rose by 5.6% to 448,416 units compared to the same period the previous year, following an 18.5% increase during 2021. Since COVID-19 confinements, many people have moved from the major cities to the provinces in France. Overall, the residential market is expected to be more stable in the coming years.

- In Germany, with around 60% of total R&D expenditure, German industrial companies significantly contribute to the country's prosperity. Companies also engage in strategic development. For instance, in 2023, Osvetleni Cernoch SRO built a new production and storage hall to increase its industrial production capacity. Such expansions indicate an increase in the number of industries and storage areas and the use of LED lighting.

Europe Indoor LED Lighting Market Trends

Increasing disposable income and government incentives may lead to more LED penetration

- In 2022, 198 million households resided in the EU, with 2.2 members per household on average. The region's population was 746.2 million in 2020, which reduced to 742.2 million by 2023. Homeownership rates in the EU declined by 69.10% in 2022 from 69.90% in 2021. Such instances suggest that housing development projects are less than in previous years despite a slight decline in the number of households. Thus, LED penetration is expected to grow positively but less in the residential segment compared to previous years.

- In Europe, disposable income is high for most countries, resulting in rising spending power of individuals, especially on new residential spaces. The United Kingdom's per capita income reached USD 33,138 in 2022, while that of France reached USD 25,337.7.

- In Europe, the governments provide incentive programs to create more LED penetration. The UK government announced the launch of a new energy-efficient lighting proposal. Under this, lighting, such as low energy-use LEDs, would replace old halogen bulbs. Such initiatives could save households between GBP 2,000 and GBP 3,000 over the lifetime of these bulbs. The "Federal Funding for Efficient Buildings" program was launched in January 2021 in Germany. Anyone who owns a property in Germany or who is looking to buy property in the country can apply for the funding. The energy efficiency program also includes lighting energy efficiency buildings. In June 2017, the French government announced the Energy Savings Certificate scheme, which allows people to get subsidies that can cover up to 100% of the price of LED bulbs based on the householder's income. Such instances are expected to boost the demand for LED lighting in the region during the forecast period.

Government programs and the prohibition of the sale of halogen bulbs may drive the growth of LED lighting

- One of the main energy consumers in the EU, the industry sector accounted for 25.6% of total energy consumption in 2021, followed by the household and commercial sectors, which used the most energy. A significant number of households are converting to smart home technologies, which has increased the demand for lighting control in indoor spaces, such as residential buildings, at unexpected rates. The central feature of the European Green Deal, which was unveiled in September 2020, is the Housing Renovation Program, which was implemented by the EU administration. Such programs are assisting the expansion of LED lighting in the region.

- The demand for electricity in the commercial sector tends to be around 8-10 hours, while electricity use in the industrial sector does not fluctuate throughout the day or year. Electricity demand in the residential sector varies for about 7-9 hours. The Covenant of Mayors - Demonstration Projects scheme refurbished 27 roadways in Cantemir and installed 419 smart LED lighting. About 386 inefficient bulbs were replaced in Ocnita to lower the amount of CO2 released into the atmosphere, thus causing a rise in the use of LEDs in the region.

- In September 2018, the region also prohibited the sale of non-directional halogen bulbs. These legislative changes have made it easier for consumers to progressively switch from conventional lighting to LED technology. The governments in the region are also phasing out older, less efficient technologies to boost consumer acceptance of LED items, as well as giving subsidies and incentives to enhance the overall efficiency of LEDs in the region.

Europe Indoor LED Lighting Industry Overview

The Europe Indoor LED Lighting Market is fragmented, with the top five companies occupying 37.37%. The major players in this market are ams-OSRAM AG, LEDVANCE GmbH (MLS Co Ltd), Panasonic Holdings Corporation, Signify (Philips) and Thorn Lighting Ltd. (Zumtobel Group) (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Population

- 4.2 Per Capita Income

- 4.3 Total Import Of Leds

- 4.4 Lighting Electricity Consumption

- 4.5 # Of Households

- 4.6 Led Penetration

- 4.7 Horticulture Area

- 4.8 Regulatory Framework

- 4.8.1 France

- 4.8.2 Germany

- 4.8.3 United Kingdom

- 4.9 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Indoor Lighting

- 5.1.1 Agricultural Lighting

- 5.1.2 Commercial

- 5.1.2.1 Office

- 5.1.2.2 Retail

- 5.1.2.3 Others

- 5.1.3 Industrial and Warehouse

- 5.1.4 Residential

- 5.2 Country

- 5.2.1 France

- 5.2.2 Germany

- 5.2.3 United Kingdom

- 5.2.4 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 ams-OSRAM AG

- 6.4.2 Dialight

- 6.4.3 EGLO Leuchten GmbH

- 6.4.4 LEDVANCE GmbH (MLS Co Ltd)

- 6.4.5 NVC INTERNATIONAL HOLDINGS LIMITED

- 6.4.6 Panasonic Holdings Corporation

- 6.4.7 Signify (Philips)

- 6.4.8 Thorlux Lighting (FW Thorpe Plc)

- 6.4.9 Thorn Lighting Ltd. (Zumtobel Group)

- 6.4.10 TRILUX GmbH & Co. KG

7 KEY STRATEGIC QUESTIONS FOR LED CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

可调光LED轨道灯具市场按类型、光源、安装方式、功率、应用和最终用户划分-全球预测,2026-2032年

可调光LED轨道灯具市场按类型、光源、安装方式、功率、应用和最终用户划分-全球预测,2026-2032年 中东和非洲室内 LED 照明:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)中国室内 LED 照明:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)亚太室内 LED 照明:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)北美室内 LED 照明:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)南美室内 LED 照明:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)印度室内 LED 照明:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)室内 LED 照明:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)德国室内 LED 照明:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)日本室内 LED 照明:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)

中东和非洲室内 LED 照明:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)中国室内 LED 照明:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)亚太室内 LED 照明:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)北美室内 LED 照明:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)南美室内 LED 照明:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)印度室内 LED 照明:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)室内 LED 照明:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)德国室内 LED 照明:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)日本室内 LED 照明:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)