|

市场调查报告书

商品编码

1683985

中国农药:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)China Insecticide - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

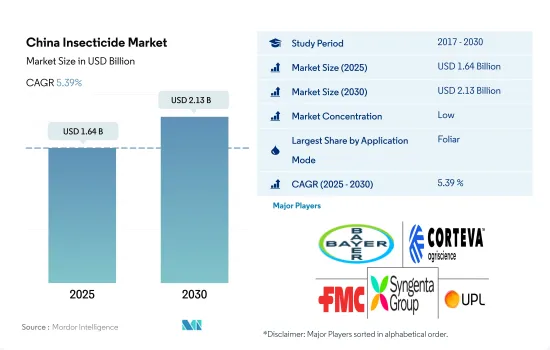

预计 2025 年中国农药市场规模为 16.4 亿美元,到 2030 年将达到 21.3 亿美元,预测期内(2025-2030 年)的复合年增长率为 5.39%。

害虫压力的增加、农作物损失的增加以及对有效害虫防治方法的需求正在推动对杀虫剂的需求。

- 中国农药市场规模不断扩大,使用方式也日益多样化。这种多样化的应用技术提供了广泛的选择,可以有效控制害虫并确保作物保护。

- 叶面喷布占据中国杀虫剂市场的主导地位。预计 2023 年至 2029 年期间,该产业的以金额为准复合年增长率将达到 5.8%。机械化、优良作物品种和先进农耕技术等现代农业实践的快速采用是这一增长的主要驱动力。随着农民采用这些进步,他们意识到有效的害虫控制在优化作物产量方面所扮演的角色。这项认知进一步推动了对杀虫剂(尤其是叶面喷布)的需求,使其成为中国害虫管理策略不可或缺的一部分。

- 预计 2023 年至 2029 年间,经济作物杀虫剂种子处理市场将成长 450 万美元。种子处理已成为中国大型商业种植者的标准做法。透过采用这种方法,他们实现了保护对高价值作物的投资的好处。

- 土壤处理是中国农药市场成长最快的领域之一,预计预测期内以金额为准年增长率为 5.2%。该国农民越来越多地采用这种方法作为其害虫管理策略的一部分,因为它可以长期控制害虫,预防土壤传播的疾病,并改善整体作物健康和生产力。因此,预计 2023 年至 2029 年中国杀虫剂市场以金额为准的复合年增长率为 5.7%。

中国杀虫剂市场趋势

农药使用量零增长和病虫害综合治理策略已显着减少每公顷农药消费量

- 由于多种因素,中国每公顷农药消费量将从2017年到2022年下降13.1%。近年来,中国政府推出了多项政策,旨在减少农药使用、禁止使用有害杀虫剂产品、实现化学农药消费量零成长。这些政策是该国促进永续农业和尽量减少农业实践对环境影响的更广泛努力的一部分。因此,人们开始转向替代方案,例如使用基因改造作物和植物来源蛋白酶抑制剂。

- 基因改造作物,也称为基因改造作物(GMO),已被开发来抵抗特定的害虫。透过将天然抗虫物种的基因引入作物,可以在不使用化学农药的情况下保护作物免受某些害虫的侵害。这种方法在中国很受欢迎,中国已经成功种植了基改棉花、玉米和其他作物。

- 除了基因改造作物外,中国还在探索使用植物来源蛋白酶抑制剂作为合成农药的天然替代品。蛋白酶抑制剂是阻断蛋白酶活性的物质,蛋白酶是参与昆虫各种生理功能的酵素。透过将这些抑制剂加入作物中,可以扰乱害虫的消化系统并减少它们对植物造成的损害。

- 由于这些政府政策的实施和替代性病虫害防治方法的日益采用,中国每公顷土地使用的农药量正在减少。

活性成分的价格在很大程度上受到当地气候、疾病爆发、能源价格和人事费用等因素的影响。

- 在中国,受作物病虫害影响的农地面积在过去50年增加了四倍,这主要是由于气候变迁造成的。中国最常见的害虫是鳞翅目害虫,包括蛾和蝴蝶(还有秋粘虫),占受灾农田的三分之一以上。接下来是同翅目昆虫,包括蚜虫、蝉和叶蝉。

- Cypermethrin是使用最广泛的拟除虫菊酯类农药,在中国用于防治蔬菜和水果上的果蝇、红火虫、蟋蟀等多种害虫。 2022 年其价格为每吨 20,900 美元。

- Malathion用于控制多种害虫,包括蚜虫、跳甲和许多其他吸食珍贵作物汁液的害虫。中国广泛种植且经常与Malathion一起使用的五种作物是樱桃番茄、西兰花、桑葚、蔓越莓和无花果。 2022 年的价格为每吨 12,400 美元。低毒性是Malathion最大的优势之一,中国致力于研发低毒性高效率的农药,并降低潜在的环境风险。这些因素可能会进一步影响中国Malathion的价格。

- Imidacloprid是一种典型的新烟碱类杀虫剂,2022年价格为每吨1.7万美元。Imidacloprid主要用于防治水稻、小麦、蔬菜、棉花等作物中的飞蝨和蚜虫。稻米是Imidacloprid最大的消费者,小麦是中国第二大作物。

- 活性成分的价格在很大程度上受到当地气候、疾病爆发、能源价格和人事费用等因素的影响。

中国农药产业概况

中国农药市场较为分散,前五大企业的市占率达37.15%。市场的主要企业是:拜耳股份公司、科迪华农业科技、FMC 公司、先正达集团和 UPL 有限公司(按字母顺序排列)。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章执行摘要和主要发现

第二章 报告要约

第 3 章 简介

- 研究假设和市场定义

- 研究范围

- 调查方法

第四章 产业主要趋势

- 每公顷农药消费量

- 有效成分价格分析

- 法律规范

- 中国

- 价值链与通路分析

第五章 市场区隔

- 如何使用

- 化学灌溉

- 叶面喷布

- 熏蒸

- 种子处理

- 土壤处理

- 作物类型

- 经济作物

- 水果和蔬菜

- 粮食

- 豆类和油籽

- 草坪和观赏植物

第六章 竞争格局

- 主要策略趋势

- 市场占有率分析

- 业务状况

- 公司简介(包括全球概况、市场层级概况、主要业务部门、财务状况、员工人数、关键资讯、市场排名、市场占有率、产品和服务、最新发展分析)

- BASF SE

- Bayer AG

- Corteva Agriscience

- FMC Corporation

- Jiangsu Yangnong Chemical Co. Ltd

- Lianyungang Liben Crop Technology Co. Ltd

- Rainbow Agro

- Syngenta Group

- UPL Limited

- Wynca Group(Wynca Chemicals)

第七章:执行长的关键策略问题

第 8 章 附录

- 世界概况

- 概述

- 五力分析框架

- 全球价值链分析

- 市场动态(DRO)

- 资讯来源和进一步阅读

- 图片列表

- 关键见解

- 资料包

- 词彙表

简介目录

Product Code: 50001687

The China Insecticide Market size is estimated at 1.64 billion USD in 2025, and is expected to reach 2.13 billion USD by 2030, growing at a CAGR of 5.39% during the forecast period (2025-2030).

The rising pest pressure, increasing crop losses, and the need for effective pest control methods are driving the demand for insecticides

- The Chinese insecticide market is experiencing growth across various application methods. These diverse application techniques offer a wide range of options to effectively control insect pests and ensure crop protection.

- The foliar application method dominates the insecticide market in China. This segment is projected to register a CAGR of 5.8% in terms of value from 2023 to 2029. The rapid adoption of modern agricultural practices, such as mechanization, enhanced crop varieties, and advanced farming techniques, has been a key driver of this growth. As farmers adopt these advancements, they are increasingly realizing the role of effective pest control in optimizing crop yields. This recognition has further fueled the demand for insecticides, specifically through foliar application, as an essential part of pest management strategies in China.

- Between 2023 and 2029, the insecticide seed treatment market in commercial crops is projected to grow by USD 4.5 million. Large-scale commercial growers in China are adopting seed treatment as standard practice. By adopting this method, they are recognizing the advantages of protecting their investments in highly valuable crops.

- Soil treatment is one of the fastest-growing segments in the insecticide market in China, which is expected to register a CAGR of 5.2% in terms of value during the forecast period. Farmers in the country are increasingly incorporating this method into their pest management strategies due to its effectiveness in long-term pest control, prevention of soil-borne diseases, and enhancement of overall crop health and productivity. Therefore, the Chinese insecticide market is forecast to register a CAGR of 5.7% in terms of value during 2023-2029.

China Insecticide Market Trends

Zero growth in pesticide usage and IPM strategies have contributed to a significant reduction in the per hectare insecticide consumption

- The consumption of insecticides in China per hectare decreased by 13.1% from 2017 to 2022, attributed to several factors. In recent years, China has implemented several government policies aimed at reducing the usage of insecticides, banning harmful insecticidal products, and achieving zero growth in chemical pesticide consumption. These policies are part of the country's broader efforts to promote sustainable agriculture and minimize the environmental impact of agricultural practices. As a result, there has been a shift toward alternative methods of pest control, including the use of transgenic crops and plant-derived protease inhibitors.

- Transgenic crops, also known as genetically modified organisms (GMOs), have been developed with built-in resistance to certain pests. Introducing genes from naturally pest-resistant species into crops can help them defend themselves against specific insects without the need for chemical insecticides. This approach has gained traction in China, where genetically modified cotton, maize, and other crops have been successfully cultivated.

- In addition to transgenic crops, China has been exploring the use of plant-derived protease inhibitors as a natural alternative to synthetic insecticides. Protease inhibitors are substances that inhibit the activity of proteases, which are enzymes involved in various physiological processes of insects. Incorporating these inhibitors into crops can aim to disrupt the digestive systems of insect pests, rendering them less harmful to plants.

- The implementation of the above-mentioned government policies and the rising adoption of alternative pest control methods have contributed to a reduction in the usage of insecticides per hectare in China.

Active ingredient prices are majorly influenced by factors like weather conditions, disease outbreaks, energy prices, and labor costs in the country

- The amount of farmland hit by crop pests in China has quadrupled in the past 50 years, mainly due to climate change. The most prevalent pests in China are lepidoptera, the order that includes moths and butterflies (and fall armyworms), which accounted for more than a third of the affected cropland. This was followed by homoptera, which includes aphids, cicadas, and leafhoppers.

- Cypermethrin is the most widely used pyrethroid pesticide to control many pests, such as fruit flies, borers, and mealy bugs in vegetables and fruits in China. It was valued at a price of USD 20.9 thousand per metric ton in 2022.

- Malathion is used to control a wide range of pests, including aphids, fleas, and other sucking pests on a number of valuable crops. Five crops that are extensively grown in China that use malathion frequently are cherry tomato, broccoli, mulberry, cranberry, and fig. It was valued at a price of USD 12.4 thousand per metric ton in 2022. Low toxicity is one of malathion's largest advantages, as China is dedicated to developing low-toxic and highly efficient pesticides to reduce potential environmental risks. Such factors will further influence the price of malathion in China.

- Imidacloprid is a typical neonicotinoid insecticide, priced at USD 17.0 thousand per metric ton in 2022. Imidacloprid is mainly used in the control of planthoppers and aphids on crops like rice, wheat, vegetables, and cotton. Rice is the largest consumer of imidacloprid, and wheat ranks second among crops cultivated in China.

- The active ingredient prices are majorly influenced by factors like weather conditions, disease outbreaks, energy prices, and labor costs in the country.

China Insecticide Industry Overview

The China Insecticide Market is fragmented, with the top five companies occupying 37.15%. The major players in this market are Bayer AG, Corteva Agriscience, FMC Corporation, Syngenta Group and UPL Limited (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Consumption Of Pesticide Per Hectare

- 4.2 Pricing Analysis For Active Ingredients

- 4.3 Regulatory Framework

- 4.3.1 China

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Application Mode

- 5.1.1 Chemigation

- 5.1.2 Foliar

- 5.1.3 Fumigation

- 5.1.4 Seed Treatment

- 5.1.5 Soil Treatment

- 5.2 Crop Type

- 5.2.1 Commercial Crops

- 5.2.2 Fruits & Vegetables

- 5.2.3 Grains & Cereals

- 5.2.4 Pulses & Oilseeds

- 5.2.5 Turf & Ornamental

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 BASF SE

- 6.4.2 Bayer AG

- 6.4.3 Corteva Agriscience

- 6.4.4 FMC Corporation

- 6.4.5 Jiangsu Yangnong Chemical Co. Ltd

- 6.4.6 Lianyungang Liben Crop Technology Co. Ltd

- 6.4.7 Rainbow Agro

- 6.4.8 Syngenta Group

- 6.4.9 UPL Limited

- 6.4.10 Wynca Group (Wynca Chemicals)

7 KEY STRATEGIC QUESTIONS FOR CROP PROTECTION CHEMICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

02-2729-4219

+886-2-2729-4219

储粮杀虫剂市场报告:按产品类型、应用和地区划分(2026-2034年)

储粮杀虫剂市场报告:按产品类型、应用和地区划分(2026-2034年) Buprofezin市场:2026-2032年全球市场预测(按剂型、作物、应用方法、最终用户和销售管道)Chlorantraniliprole市场:全球市场按作物类型、剂型、应用方法和最终用户分類的预测-2026-2032年克百威市场:按剂型、作物类型、最终用户、分销管道和应用划分-2026-2032年全球预测高效能Cypermethrin市场:按製剂类型、销售管道和应用划分-2026-2032年全球预测二唑唑市场:依作物类型、剂型、应用方法、最终用户和分销管道划分-2026-2032年全球预测

Buprofezin市场:2026-2032年全球市场预测(按剂型、作物、应用方法、最终用户和销售管道)Chlorantraniliprole市场:全球市场按作物类型、剂型、应用方法和最终用户分類的预测-2026-2032年克百威市场:按剂型、作物类型、最终用户、分销管道和应用划分-2026-2032年全球预测高效能Cypermethrin市场:按製剂类型、销售管道和应用划分-2026-2032年全球预测二唑唑市场:依作物类型、剂型、应用方法、最终用户和分销管道划分-2026-2032年全球预测 农药市场规模、份额、成长及全球产业分析:按类型、应用和地区划分,并预测至2026-2034年

农药市场规模、份额、成长及全球产业分析:按类型、应用和地区划分,并预测至2026-2034年 美国农药:市场占有率分析、产业趋势与统计、成长预测(2026-2031)全球农药市场规模、份额、趋势和成长分析报告(2026-2034年)

美国农药:市场占有率分析、产业趋势与统计、成长预测(2026-2031)全球农药市场规模、份额、趋势和成长分析报告(2026-2034年) 全球农药市场报告(2026 年)

全球农药市场报告(2026 年)

▼