|

市场调查报告书

商品编码

1683992

印度农药:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)India Insecticide - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

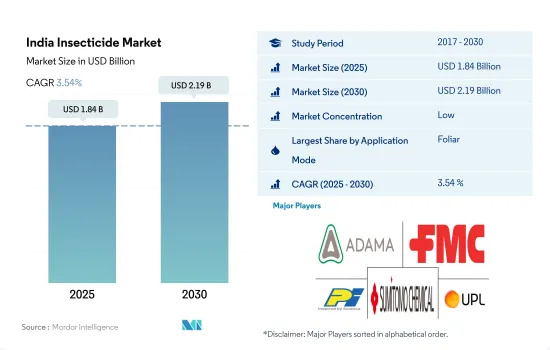

印度农药市场规模预计在 2025 年为 18.4 亿美元,预计到 2030 年将达到 21.9 亿美元,预测期内(2025-2030 年)的复合年增长率为 3.54%。

叶面喷布是施用预防和治疗杀虫剂的常见且有效的方法。

- 在印度,农业生产中以各种方式使用农药来控制昆虫。农民可以透过选择正确的施用方法来覆盖特定区域并减少浪费来节省成本。效率的提升可以优化农药的使用,有助于降低农民的投入成本。

- 叶面喷布是农业中施用农药的主要形式,占 2022 年农药施用部分的 57.5%。此方法主要用于谷物和谷类种植,占据最大的市场占有率,为 44.6%。叶面喷洒杀虫剂之所以受欢迎,是因为它们能快速消灭害虫,这对于有效的害虫管理至关重要。

- 种子处理是第二大最受欢迎的施用方法,占该领域的市场占有率的 16.9%。这主要是因为农民意识到保护种子和幼苗免受害虫侵害、确保作物最佳生长、最大限度提高产量和减少未来生长阶段农药使用的重要性。

- 喷雾模式市场预计在 2019 年至 2021 年期间的复合年增长率为 2.2%。农民对特定施用模式的偏好取决于目标昆虫、作物类型、昆虫阶段和设备可用性。世界人口不断增长以及随之而来的粮食需求增加使得农业生产力必须提高。因此,预计应用模式部分在预测期内的复合年增长率为 3.8%。

印度农药市场趋势

预测期内,保护农作物免受害虫侵害和提高生产力的需求不断增长,可能会推动农药消费

- 印度的农业气候条件多样,导致各种昆虫的盛行。如果不有效处理,臭虫、尺蠖、黏虫、蚜虫和粉蝨等昆虫会对作物造成严重损失。为了保护作物免受害虫侵害,农民正在增加杀虫剂的使用。 2021年至2022年,印度每公顷农药消费量增加了0.5%。印度人均农药使用量增加,从而提高了每公顷平均农业产量。

- 2022年,印度每公顷农药消费量为151.9公克/公顷。这是因为种植的作物种类繁多,包括大米和小麦等主粮,以及棉花、甘蔗和蔬菜等经济作物。保护这些作物免受昆虫侵害对于保持产量非常重要。

- 印度总合173种入侵物种,其中47种已经入侵农业生态系。这些入侵昆虫导致杀虫剂的使用量增加。此外,昆虫对某些杀虫剂产生抗药性也是一个问题。随着时间的推移,昆虫会进化并对某些杀虫剂产生抗药性,从而降低其杀虫剂效果。为了达到所需的病虫害防治效果,可能需要增加农药的喷洒量或使用次数,这将增加农药的消费量。

- 印度正在寻求扩大农业生产以满足日益增长的粮食需求。农药透过保护植物免受害虫侵害而对提高农业产量起着至关重要的作用。满足人口的食物需求导致了对杀虫剂的依赖增加。

杀虫剂需求的不断增长是由于害虫侵袭和作物损失的增加。

- Cypermethrin是一种合成除虫菊酯,用于控制跳甲、果子狸、蟑螂、白蚁、瓢虫、蝎子和黄蜂。 2022年的价格为21000美元。在印度,Cypermethrin已由CIBRC登记用于八种特定作物,包括高丽菜、小麦、棉花、稻米、甘蔗、茄子、向日葵和秋葵。

- Imidacloprid是一种新烟碱类神经活性杀虫剂。在印度,它可以用作喷雾剂来控制棉花、水稻、甘蔗、芒果、花生、葡萄、辣椒和番茄等各种作物上的吸汁性昆虫,如蓟马、蚜虫、千足虫、小棕蝨和白带蝨。 2022年印度Imidacloprid价格为17,100美元。

- Malathion是一种有机磷杀虫剂,2022 年的售价为 12,500 美元。它用于控制蚜虫、蓟马、螨虫、介壳虫、扫帚虫、蚯蚓、潜叶虫、跳蚤、蚱蜢、臭虫、蛆等。根据 CIBRC 的指导方针,Malathion仅允许用于高粱、豌豆、大豆、蓖麻、向日葵、秋葵、茄子、花椰菜、萝卜、芜菁、番茄、苹果、芒果和葡萄。

- 根据印度政府统计,每年约有15-25%的作物因害虫而损失。印度农民最关心的问题就是保护作物免受害虫侵害。例如,根据印度蔬菜研究所的数据,全国各地的番茄种植者每年因水果害虫而损失 65% 的产量。虫害会导致花朵掉落、植物健康状况不佳,并降低果实质量,对作物产量负面影响。所有这些因素都会影响农药的需求,进而影响农药的价格。

印度农药业概况

印度农药市场较为分散,前五大公司的市占率为37.36%。该市场的主要企业是:ADAMA Agricultural Solutions Ltd、FMC Corporation、PI Industries、住友化学和UPL Limited(按字母顺序排列)。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章执行摘要和主要发现

第二章 报告要约

第 3 章 简介

- 研究假设和市场定义

- 研究范围

- 调查方法

第四章 产业主要趋势

- 每公顷农药消费量

- 有效成分价格分析

- 法律规范

- 印度

- 价值链与通路分析

第五章 市场区隔

- 如何使用

- 化学灌溉

- 叶面喷布

- 熏蒸

- 种子处理

- 土壤处理

- 作物类型

- 经济作物

- 水果和蔬菜

- 粮食

- 豆类和油籽

- 草坪和观赏植物

第六章 竞争格局

- 主要策略趋势

- 市场占有率分析

- 业务状况

- 公司简介(包括全球概况、市场层级概况、主要业务部门、财务状况、员工人数、关键资讯、市场排名、市场占有率、产品和服务、最新发展分析)

- ADAMA Agricultural Solutions Ltd

- BASF SE

- Bayer AG

- Corteva Agriscience

- FMC Corporation

- Gharda Chemicals Ltd

- PI Industries

- Sumitomo Chemical Co. Ltd

- Syngenta Group

- UPL Limited

第七章:执行长的关键策略问题

第 8 章 附录

- 世界概况

- 概述

- 五力分析框架

- 全球价值链分析

- 市场动态(DRO)

- 资讯来源和进一步阅读

- 图片列表

- 关键见解

- 资料包

- 词彙表

简介目录

Product Code: 50001694

The India Insecticide Market size is estimated at 1.84 billion USD in 2025, and is expected to reach 2.19 billion USD by 2030, growing at a CAGR of 3.54% during the forecast period (2025-2030).

The foliar application mode is a common and effective way of applying insecticides for preventive and curative methods

- In India, insecticides are applied through various modes to control insects in agricultural practices. Farmers can achieve cost savings by choosing a suitable application method covering specific areas and minimizing wastage. This increased efficiency leads to optimized insecticide usage and reduced input costs for farmers.

- The dominant mode of insecticide application in agricultural practices is foliar application, which accounted for 57.5% of the insecticide application segment in 2022. This method is predominantly used in grains and cereals cultivation, which holds the largest market share at 44.6%. The popularity of foliar treatment insecticides can be attributed to their rapid effectiveness in controlling insect infestations, making them crucial for efficient pest management.

- Seed treatment is the second most prevalent application method, accounting for a market share of 16.9% in the segment. This is primarily because farmers have acknowledged the significance of safeguarding seeds and seedlings from insect pests to ensure optimal crop establishment, maximize yield, and reduce insecticide usage in future growth stages.

- From 2019 to 2021, the application mode market demonstrated a projected increase with a CAGR of 2.2%. Farmers' preference for a specific application mode depends on the target insect, crop type, insect stage, and equipment availability. The growing global population and the resulting higher demand for food have led to a necessity to enhance agricultural productivity. As a result, the application mode segment is expected to witness a CAGR of 3.8% during the forecast period.

India Insecticide Market Trends

The rising need to protect the crops from harmful insects and improve production may fuel the consumption of insecticides during the forecast period

- India has a diverse range of agro-climatic conditions, which can contribute to the prevalence of various insects. Insects such as stink bugs, loopers, armyworms, aphids, and whiteflies can cause major crop losses if not successfully handled. To protect crops from such insects, farmers are resorting to increased insecticide use. The consumption of insecticides in India per hectare experienced an increase of 0.5% from 2021 to 2022. Insecticide usage per capita in India increased to boost the average agricultural output per hectare.

- The consumption of insecticides in India per hectare in 2022 accounted for 151.9 g/ha. This is attributed to the cultivation of a wide range of crops, including staple food grains, like rice and wheat, and cash crops, like cotton, sugarcane, and vegetables. It is critical to protect these crops against insects to maintain yields.

- India has a total of 173 invasive species, including 47 invasive agricultural ecosystem species, 23 of which are insects. These invasive insects contribute to the need for increased pesticide use. Furthermore, the development of insect resistance to certain insecticides is a rising problem. Insects can evolve and develop resistance to the effects of particular pesticides over time, making them less effective. To achieve the necessary degree of pest control, larger application rates or more frequent usage of insecticides are required, increasing the consumption of insecticide.

- India aims to boost agricultural output to meet rising food demand. Insecticides serve an important role in increasing agricultural yields by protecting plants from pests that might disrupt output. The necessity to fulfill the population's food requirements drives the reliance on pesticides.

The growing demand for insecticides owing to the increasing pest attack and crop losses.

- Cypermethrin is a synthetic pyrethroid used to control flea beetles, boxelder bugs, cockroaches, termites, ladybugs, scorpions, and yellow jackets. It was priced at USD 21.0 thousand in 2022. In India, cypermethrin is registered by CIBRC for use in eight specified crops, such as cabbage, wheat, cotton, rice, sugarcane, brinjal, sunflower, and okra.

- Imidacloprid is a neonicotinoid, which is a class of neuroactive insecticides. It can be used as a spray for the control of sucking and other insects, such as thrips, aphids, jassids, brown plant hoppers, and white-backed plant hoppers, in different crops, like cotton, paddy, sugarcane, mango, groundnut, grapes, chilies, and tomato, in India. In 2022, imidacloprid was priced at USD 17.1 thousand in India.

- Malathion is an organophosphate insecticide, which was valued at USD 12.5 thousand in 2022. It is used to control aphids, thrips, mites, scales, borers, worms, leaf miners, fleas, grasshoppers, bugs, and maggots. As per guidelines of CIBRC, malathion is permitted to be used only in sorghum, pea, soybean, castor, sunflower, bhindi, brinjal, cauliflower, radish, turnip, tomato, apple, mango, and grape crops.

- According to the Government of India statistics, about 15 to 25% of crops are lost due to pests every year. Indian farmers' major concern is safeguarding their crops from pests. For instance, according to the Indian Institute of Vegetable Research, tomato farmers across the country lose up to 65% of their yields to fruit borers every year. The infestation of the pest leads to flower dropping and poor plant health, resulting in poor quality fruiting, thus adversely impacting crop yields. All these factors will influence the demand for insecticides, which will further affect their prices.

India Insecticide Industry Overview

The India Insecticide Market is fragmented, with the top five companies occupying 37.36%. The major players in this market are ADAMA Agricultural Solutions Ltd, FMC Corporation, PI Industries, Sumitomo Chemical Co. Ltd and UPL Limited (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Consumption Of Pesticide Per Hectare

- 4.2 Pricing Analysis For Active Ingredients

- 4.3 Regulatory Framework

- 4.3.1 India

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Application Mode

- 5.1.1 Chemigation

- 5.1.2 Foliar

- 5.1.3 Fumigation

- 5.1.4 Seed Treatment

- 5.1.5 Soil Treatment

- 5.2 Crop Type

- 5.2.1 Commercial Crops

- 5.2.2 Fruits & Vegetables

- 5.2.3 Grains & Cereals

- 5.2.4 Pulses & Oilseeds

- 5.2.5 Turf & Ornamental

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 ADAMA Agricultural Solutions Ltd

- 6.4.2 BASF SE

- 6.4.3 Bayer AG

- 6.4.4 Corteva Agriscience

- 6.4.5 FMC Corporation

- 6.4.6 Gharda Chemicals Ltd

- 6.4.7 PI Industries

- 6.4.8 Sumitomo Chemical Co. Ltd

- 6.4.9 Syngenta Group

- 6.4.10 UPL Limited

7 KEY STRATEGIC QUESTIONS FOR CROP PROTECTION CHEMICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

02-2729-4219

+886-2-2729-4219

Buprofezin市场:2026-2032年全球市场预测(按剂型、作物、应用方法、最终用户和销售管道)Chlorantraniliprole市场:全球市场按作物类型、剂型、应用方法和最终用户分類的预测-2026-2032年克百威市场:按剂型、作物类型、最终用户、分销管道和应用划分-2026-2032年全球预测高效能Cypermethrin市场:按製剂类型、销售管道和应用划分-2026-2032年全球预测二唑唑市场:依作物类型、剂型、应用方法、最终用户和分销管道划分-2026-2032年全球预测

Buprofezin市场:2026-2032年全球市场预测(按剂型、作物、应用方法、最终用户和销售管道)Chlorantraniliprole市场:全球市场按作物类型、剂型、应用方法和最终用户分類的预测-2026-2032年克百威市场:按剂型、作物类型、最终用户、分销管道和应用划分-2026-2032年全球预测高效能Cypermethrin市场:按製剂类型、销售管道和应用划分-2026-2032年全球预测二唑唑市场:依作物类型、剂型、应用方法、最终用户和分销管道划分-2026-2032年全球预测 美国农药:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

美国农药:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 全球农药市场规模、份额、趋势和成长分析报告(2026-2034年)

全球农药市场规模、份额、趋势和成长分析报告(2026-2034年) 全球农药市场报告(2026 年)

全球农药市场报告(2026 年) 农药市场-全球产业规模、份额、趋势、机会、预测:按类型、应用、地区和竞争格局划分,2021-2031年技术级多杀菌素市场依製剂类型、作物类型、害虫类型和应用方法划分-2026-2032年全球预测

农药市场-全球产业规模、份额、趋势、机会、预测:按类型、应用、地区和竞争格局划分,2021-2031年技术级多杀菌素市场依製剂类型、作物类型、害虫类型和应用方法划分-2026-2032年全球预测

▼