|

市场调查报告书

商品编码

1683998

北美除草剂:市场占有率分析、产业趋势和成长预测(2025-2030)North America Herbicide - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

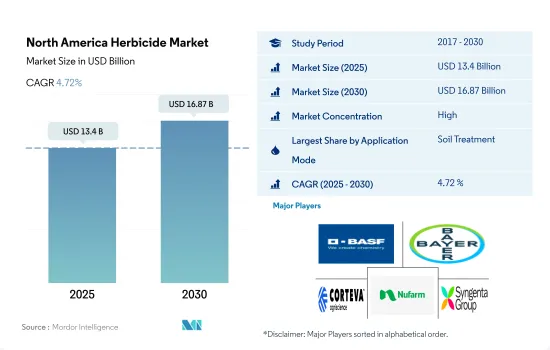

北美除草剂市场规模预计在 2025 年达到 134 亿美元,预计到 2030 年将达到 168.7 亿美元,预测期内(2025-2030 年)的复合年增长率为 4.72%。

土壤应用主导北美除草剂市场

- 杂草是造成农业系统产量损失和品质下降的主要原因。杂草与作物争夺光、水和养分。杂草也会成为破坏性昆虫媒介的储存器,将病原体从一株植物传播到另一作物植物,对农作物造成危害。使用除草剂是控制杂草最有效的方法,并且比其他方法更便宜、更省力、更省时。可以使用多种除草剂施用技术来控制各种杂草。

- 北美除草剂市场以土壤施用为主,2022 年占市场占有率的 48.8%。主要透过土壤处理施用出苗前除草剂。儘早抑制杂草可以使作物在生长季节有一个良好的开始。土壤活性除草剂具有不同的活性成分和施用时间,可以帮助解决棘手的抗性杂草并减缓除草剂抗性的产生。在出苗前除草剂中,最常用且施用于土壤时最有效的三种除草剂是恶草酮、二甲戊灵和Pretilachlor。

- 叶面喷布是北美第二大使用的除草剂施用方法,2022 年的市场占有率为 29.8%。出苗后除草剂就是以这种方式施用的。后浸除草剂必须从叶面迁移到目标区域才能发挥作用。当除草剂施用于具有光合作用活性的叶子时,叶子会吸收除草剂并直接影响叶组织或将除草剂转移到植物的其他部位。预计叶面部分在预测期内将显着成长。

由于杂草侵染导致收成损失增加,美国占市场主导地位

- 杂草是北美各种种植制度生产的主要生物限制因素。杂草造成的作物产量损失取决于几个因素,包括杂草出现的时间、杂草密度、杂草类型和作物类型。如果不加以控制,杂草将导致 100% 的产量损失。除草剂是杂草控制的重要组成部分。

- 美国在2022年占据82.0%的市场占有率。它是世界上最大的小麦生产国和出口国之一。然而,杂草造成的小麦产量损失对该国的小麦生产和农民的经济繁荣构成了严重威胁。 2022 年,WSSA 杂草损失委员会估计,因杂草造成的冬小麦产量损失约 25.6%。 WSSA 杂草损失委员会发现,除草剂的使用和最佳管理措施相结合可将小麦产量损失从 60% 减少到 20%。

- 加拿大占2022年北美除草剂市场的7.8%。油菜是该国的主要作物。因杂草造成的油菜籽平均产量损失因州而异。根据基准估计的收穫面积和平均产量,亚伯达的产量损失最大,估计为 34.6%,即损失了 7,200 万蒲式耳。萨斯喀彻尔的产量损失估计为 30.2%,损失了 8,600 万蒲式耳。曼尼托巴省的产量损失估计为 18.1%,损失了 1,900 万蒲式耳。北达科他州的产量预计将下降27.9%,导致2022年损失1,100万蒲式耳。

- 杂草侵染的增加极大地促进了国内和国际需求的增加,而人们对粮食安全的日益担忧也推动了市场的发展。预计预测期内(2023-2029 年)的复合年增长率为 4.9%。

北美除草剂市场趋势

除草剂配方的进步推动了北美农民的采用

- 北美除草剂消费量自2017年以来增加,达到每公顷5.6公斤。美国每公顷的消费量最高,到2022年将达到每公顷2.7公斤。

- 抗除草剂杂草的出现和日益普及越来越引起北美农民的关注,导致他们使用更高剂量的除草剂或多种除草剂来控制抗除草剂杂草。例如,长芒苋和普通水麻对Glyphosate有抗性,马唐和大豚草对多种除草剂有抗性,而藜芦对乙酰乳酸合成酶(ALS)抑制除草剂也有抗性。

- 此外,在北美,犁地和犁地等保护性耕作措施因其对环境和土壤健康有益而越来越受欢迎。例如,2012年至2017年间,美国实施集约化耕作的农场数量下降了35%,加拿大和墨西哥的农业农场也出现了类似的趋势。集约化耕作的减少导致人们更加依赖除草剂来有效控制杂草。

- 此外,为了满足日益增长的粮食和饲料需求,对产量作物的需求不断增加,这也推动了除草剂使用量的增加。农民可以依靠增加除草剂的使用来有效地管理杂草竞争,以最大限度地提高作物产量并确保最佳的作物生长和生产力。

- 除草剂配方技术的进步和基因改造作物的日益普及使得农民能够将除草剂直接喷洒在作物上,而只影响杂草。预计这些趋势将导致北美每公顷土地的除草剂使用量进一步增加。

杂草导致农作物损失增加,并推高了对除草剂的需求,进而推高了除草剂的价格。

- 杂草侵染仍是农业面临的一大挑战,造成产量损失并增加农民的生产成本。在北美,Atrazine、Paraquat和Glyphosate是常用的除草剂。

- Atrazine是氯化三嗪类系统性除草剂,专门针对一年生禾本科植物和阔叶杂草,在它们出现之前进行控制。含有Atrazine的除草剂配方已被核准用于多种作物,包括玉米、甜玉米、高粱、甘蔗、小麦、澳洲坚果和番石榴。此外,Atrazine也用于苗圃/观赏植物和草皮管理。 2022 年的价值为每吨 13,800 美元。

- Paraquat二氯化物,通常称为“Paraquat”,是一种在北美广泛使用的除草剂,在美国以其最终用途产品名称克无踪而闻名。Paraquat在各种农业和非农业环境中的杂草控制中发挥着重要作用。它也用于在收穫前干燥棉花等作物。 2022年,Paraquat价格预计将维持在4,600美元/吨。

- Glyphosate是一种系统性、广谱除草剂,在抽穗后有效。近几十年来,它的使用量显着增加,成为最广泛使用的除草剂之一。含Glyphosate的产品以多种形式出售,包括液体浓缩物、固态製剂和即用型液体製剂。该化合物具有农业和非农业用途,可控制杂草生长。截至 2022 年,Glyphosate的市场价值为每吨 16,600 美元。

北美除草剂行业概况

北美除草剂市场相当集中,前五大公司占73.81%的市占率。市场的主要企业有:BASF公司、拜耳公司、科迪华农业科技、纽髮姆有限公司和先正达集团(按字母顺序排列)。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章执行摘要和主要发现

第二章 报告要约

第三章 引言

- 研究假设和市场定义

- 研究范围

- 调查方法

第四章 产业主要趋势

- 每公顷农药消费量

- 活性成分价格分析

- 法律规范

- 加拿大

- 墨西哥

- 美国

- 价值炼和通路分析

第五章市场区隔

- 执行模式

- 化学喷涂

- 叶面喷布

- 熏蒸

- 土壤处理

- 作物类型

- 经济作物

- 水果和蔬菜

- 粮食

- 豆类和油籽

- 草坪和观赏植物

- 原产地

- 加拿大

- 墨西哥

- 美国

- 北美其他地区

第六章竞争格局

- 关键策略趋势

- 市场占有率分析

- 业务状况

- 公司简介(包括全球概况、市场层级概况、主要业务部门、财务状况、员工人数、关键资讯、市场排名、市场占有率、产品和服务、最新发展分析)

- ADAMA Agricultural Solutions Ltd.

- American Vanguard Corporation

- BASF SE

- Bayer AG

- Corteva Agriscience

- FMC Corporation

- Nufarm Ltd

- Sumitomo Chemical Co. Ltd

- Syngenta Group

- UPL Limited

第七章:CEO面临的关键策略问题

第 8 章 附录

- 世界概况

- 概述

- 五力分析框架

- 全球价值链分析

- 市场动态(DRO)

- 资讯来源及延伸阅读

- 图片列表

- 关键见解

- 资料包

- 词彙表

简介目录

Product Code: 50001700

The North America Herbicide Market size is estimated at 13.4 billion USD in 2025, and is expected to reach 16.87 billion USD by 2030, growing at a CAGR of 4.72% during the forecast period (2025-2030).

Soil applications dominate the North American herbicide market

- Weeds are a major contributor to yield loss and reduced quality in an agricultural system. They compete with the crop for light, water, and nutrients. Weeds can also harm crop plants by acting as reservoirs for destructive insect vectors that move pathogens from plant to plant. Using herbicides is the most effective weed management tool, as they are cheaper, require less labor, and save more time than other measures. Several herbicide application techniques can be used to control various weeds.

- Soil application dominated the North American herbicide market, accounting for a market share of 48.8% in 2022. Mainly, pre-emergence herbicides can be applied through soil treatment. By reducing weed pressures early on, crops can get off to a strong start in the cropping season. With different active ingredients and application timings, soil-active herbicides can help tackle troublesome resistant weeds and slow down the development of herbicide resistance. Among the pre-emergence herbicides, the three most commonly used and the most effective through soil treatment are oxadiazon, pendimethalin, and pretilachlor.

- Foliar application is the second most used method to apply herbicides in North America, accounting for a market share of 29.8% in the year 2022. Post-emergence herbicides will be applied through this method. A post-emergence herbicide must move from the leaf surface and reach the target site to be effective. As herbicide is applied to photosynthesize foliage actively, the leaves take up the chemical and either directly impact the leaf tissue or translocate the herbicide to other parts of the plants. The foliar segment is expected to record significant growth during the forecast period.

The United States dominated the market due to increased yield losses because of weed infestation

- Weeds are a major biotic constraint to production in different cropping systems of North America. Yield losses in crops due to weeds depend on several factors, such as weed emergence time, weed density, the type of weed, and the type of crops. If left uncontrolled, weeds can result in 100% yield loss. Herbicides are an integral part of weed control.

- The United States dominated the market, accounting for a market share of 82.0% in 2022. It is one of the world's largest wheat producers and exporters. However, wheat yield losses caused by weeds pose a serious threat to the country's wheat production and farmers' economic prosperity. In 2022, the WSSA's Weed Loss Committee estimated the winter wheat yield loss at approximately 25.6% due to weeds. The WSSA Weed Loss Committee found that the use of herbicides combined with best management practices resulted in a decrease in wheat yield loss from 60% to 20%.

- Canada accounted for 7.8% of the North American herbicide market in 2022. Canola is the major crop grown in the country. Average canola yield losses due to weeds varied by province/state. Alberta had the highest yield losses, estimated at 34.6%, a loss of 72 million bushels, based on the average harvested area and average yield. Saskatchewan had an estimated yield loss of 30.2%, a loss of 86 million bushels. Manitoba's estimated yield loss was 18.1%, resulting in a loss of 19 million bushels. North Dakota had an estimated yield loss of 27.9%, resulting in a loss of 11 million bushels in 2022.

- The increase in weed infestations, which greatly impacts the increasing domestic and international demand, and increasing concerns for food security are driving the market. The market is anticipated to witness a CAGR of 4.9% during the forecast period (2023-2029).

North America Herbicide Market Trends

Advancements in herbicide formulations are driving adoption among North American farmers

- Herbicide consumption in North America has been increasing since 2017 and reached 5.6 kg per hectare of cropland. The United States is the largest consumer per hectare, with 2.7 kg/hectare in 2022.

- The increase in the emergence and spread of herbicide-resistant weeds has been an increasing concern for farmers in North America, resulting in the application of higher amounts of herbicides or multiple herbicides to control herbicide-resistant weeds. For instance, Palmer amaranth and common water hemp are resistant to glyphosate, Horseweed and Giant ragweed are resistant to multiple herbicides, and Kochia is resistant to acetolactate synthase (ALS) inhibiting herbicides.

- Moreover, conservation tillage practices, such as no-till and reduced-till farming, have gained popularity in North America due to their environmental and soil health benefits. For instance, the number of farms practicing intensive tillage in the United States declined by 35% between 2012 and 2017, and a similar trend was observed in Canadian and Mexican agricultural farms. This decrease in intensive tillage has caused heavy reliance on herbicides to effectively control weeds.

- In addition, there is a growing demand for high-yielding crops to meet increasing food and feed requirements, which is boosting the need for higher herbicide usage. Farmers may rely on increased herbicide usage to effectively manage weed competition to maximize crop yields, ensuring optimal crop growth and productivity.

- Advancements in herbicide formulation technologies and the growing popularity of genetically modified crops have enabled farmers to apply herbicides directly to the crop, only affecting the weeds. These trends are further anticipated to increase herbicide usage per hectare of land in North America.

The rising yield losses due to weeds is driving the demand for herbicides, thereby driving the prices of herbicides

- Weed infestation remains a significant challenge in agriculture, causing yield losses and increased production costs for farmers. Atrazine, paraquat, and glyphosate are commonly used herbicides in North America.

- Atrazine, a systemic herbicide classified under the chlorinated triazine group, is employed to specifically target and manage annual grasses and broadleaf weeds before they sprout. Herbicide formulations containing atrazine are approved for application on a range of agricultural crops, such as corn, sweet corn, sorghum, sugarcane, wheat, macadamia nuts, and guava. In addition, atrazine is used in nursery/ornamental and turf management. Its value in 2022 was recorded at USD 13.8 thousand per metric ton.

- Paraquat dichloride, commonly referred to as "paraquat," is a widely utilized herbicide in North America, renowned for its well-known end-use product name, Gramoxone, in the United States. Paraquat assumes a vital role in weed control across a variety of agricultural and non-agricultural settings. Additionally, it finds application in crop desiccation, such as cotton, before harvesting. In the year 2022, paraquat held a price of USD 4.6 thousand per metric ton.

- Glyphosate functions as a systemic and wide-ranging herbicide effective post-emergence. Its utilization has witnessed substantial growth in recent decades, positioning it as one of the most prevalent herbicides. Glyphosate-containing products are available in diverse forms, including liquid concentrate, solid, and ready-to-use liquid. This compound finds application in both agricultural and non-agricultural contexts to manage weed growth. As of 2022, the market value of glyphosate stood at USD 16.6 thousand per metric ton.

North America Herbicide Industry Overview

The North America Herbicide Market is fairly consolidated, with the top five companies occupying 73.81%. The major players in this market are BASF SE, Bayer AG, Corteva Agriscience, Nufarm Ltd and Syngenta Group (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Consumption Of Pesticide Per Hectare

- 4.2 Pricing Analysis For Active Ingredients

- 4.3 Regulatory Framework

- 4.3.1 Canada

- 4.3.2 Mexico

- 4.3.3 United States

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Application Mode

- 5.1.1 Chemigation

- 5.1.2 Foliar

- 5.1.3 Fumigation

- 5.1.4 Soil Treatment

- 5.2 Crop Type

- 5.2.1 Commercial Crops

- 5.2.2 Fruits & Vegetables

- 5.2.3 Grains & Cereals

- 5.2.4 Pulses & Oilseeds

- 5.2.5 Turf & Ornamental

- 5.3 Country

- 5.3.1 Canada

- 5.3.2 Mexico

- 5.3.3 United States

- 5.3.4 Rest of North America

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 ADAMA Agricultural Solutions Ltd.

- 6.4.2 American Vanguard Corporation

- 6.4.3 BASF SE

- 6.4.4 Bayer AG

- 6.4.5 Corteva Agriscience

- 6.4.6 FMC Corporation

- 6.4.7 Nufarm Ltd

- 6.4.8 Sumitomo Chemical Co. Ltd

- 6.4.9 Syngenta Group

- 6.4.10 UPL Limited

7 KEY STRATEGIC QUESTIONS FOR CROP PROTECTION CHEMICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

02-2729-4219

+886-2-2729-4219

除草剂市场:按类型、作用机制、作物类型、剂型和施用方法划分-2026-2032年全球预测苯氯林市场:依製剂类型、作物类型、施用方法、通路和最终用途划分-2026-2032年全球预测3-苯氧基芐醇市场:按应用、纯度等级和销售管道- 全球预测,2026-2032年氟米龙市场:按作物类型、製剂类型、施用时间、最终用户和销售管道划分 - 全球预测 2026-2032阿尼罗磷市场:全球预测(2026-2032 年),依製剂类型、作物类型、施用方法、产品等级、通路和最终用途划分

除草剂市场:按类型、作用机制、作物类型、剂型和施用方法划分-2026-2032年全球预测苯氯林市场:依製剂类型、作物类型、施用方法、通路和最终用途划分-2026-2032年全球预测3-苯氧基芐醇市场:按应用、纯度等级和销售管道- 全球预测,2026-2032年氟米龙市场:按作物类型、製剂类型、施用时间、最终用户和销售管道划分 - 全球预测 2026-2032阿尼罗磷市场:全球预测(2026-2032 年),依製剂类型、作物类型、施用方法、产品等级、通路和最终用途划分 吡咯烷砜市场分析及预测(至2035年):依类型、产品类型、应用、技术、最终用户、形态、产品介绍形式、材料类型及功能划分除草剂市场分析及预测(至2035年):类型、产品类型、用途、剂型、技术、最终用户、模式、功能

吡咯烷砜市场分析及预测(至2035年):依类型、产品类型、应用、技术、最终用户、形态、产品介绍形式、材料类型及功能划分除草剂市场分析及预测(至2035年):类型、产品类型、用途、剂型、技术、最终用户、模式、功能 全球除草剂市场规模、份额、趋势和成长分析报告(2026-2034年)

全球除草剂市场规模、份额、趋势和成长分析报告(2026-2034年) 2026年全球不织布除草剂市场报告2026年全球除草剂市场报告

2026年全球不织布除草剂市场报告2026年全球除草剂市场报告

▼