|

市场调查报告书

商品编码

1684041

汽车MLCC:市场占有率分析、产业趋势与统计、成长预测(2025-2030)Automotive MLCC - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

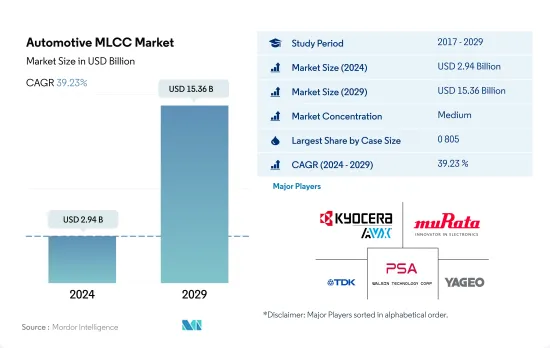

预计 2024 年汽车 MLCC 市场规模将达到 29.4 亿美元,到 2029 年将达到 153.6 亿美元,预测期内(2024-2029 年)的复合年增长率为 39.23%。

了解MLCC在汽车发展中的多方面作用正在推动对MLCC的需求

- 在不断发展的汽车产业中,MLCC 的作用已超越了简单的电子元件。这些微型动力源是现代汽车系统的核心,执行从配电和噪音抑製到讯号调节和电压调节等一系列功能。

- 0603 MLCC体积小巧,但不可或缺。这些电容器在转向更小、更节能的设计过程中发挥着至关重要的作用。随着汽车技术的进步,对精简解决方案的需求推动了 0 603 领域的存在。

- 0805 电容器在市场上占有重要地位,尤其是随着电动车 (EV) 成为主流。电动车的迅速普及凸显了有效电力分配和控制的必要性,并强调了 0 805 段的重要性。随着电动车重新定义汽车格局,这些电容器成为性能和效率的推动者。

- 1 206 电容器在尺寸和多功能性之间取得了良好的平衡,使其成为各种汽车应用的绝佳选择。随着汽车产业拥抱技术进步,1210 细分市场的重要性变得显而易见。

- 「其他」部分涵盖了满足特殊汽车要求的一系列电容值。从新技术到独特的应用,这个多样化领域展示了 MLCC 满足汽车不同需求的适应性。

揭示MLCC在亚太、欧洲和北美的影响力

- 亚太、欧洲和北美正在推动汽车产业的转型。对技术进步、永续性和智慧运输解决方案的追求凸显了积层陶瓷电容(MLCC) 在支援汽车发展方面发挥的关键作用。随着各地区朝着创新和高效的未来迈进,对高品质 MLCC 的需求持续增长,巩固了其在汽车价值链中的重要性。

- 亚太地区是汽车创新的中心,其特点是技术进步迅速、消费者需求不断增长。该地区是中国、日本和韩国等主要汽车中心的所在地,在电动车 (EV) 普及、联网汽车和自动驾驶方面处于领先地位。

- 欧洲汽车工业是创新、永续性和严格的环境法规的代名词。该地区致力于减少碳排放,转向更清洁的移动解决方案,重塑汽车格局。随着电动和混合动力汽车越来越受欢迎,对电源管理、噪音抑制和电压调节用 MLCC 的需求也日益增加。

- 北美汽车产业的特点是追求智慧运输解决方案和先进技术。随着北美消费者对改善驾驶体验和尖端功能的需求,电动车、资讯娱乐系统和 ADAS 等应用程式对 MLCC 的需求正在上升。该地区充满活力的汽车格局是 MLCC 市场扩张的主要驱动力。

汽车MLCC市场的全球趋势

加氢站基础建设持续推动销售成长

- 燃料电池电动车(FCEV)利用燃料电池将储存的氢能转化为电能,其推进机制与电动车类似。与传统内燃机动力来源的汽车相比,FCEV 不会排放有害废气。

- 预计2022年燃料电池电动车的出货量将达到4.3万辆,2029年将达到7.1万辆。随着风能、太阳能等可再生能源对氢气生产过程的贡献越来越大,对节能型FCEV的需求将大幅增加。

- 随着对低排放气体汽车的需求不断增加,更严格的二氧化碳排放法规正在实施,快速加油等优势使得 FCEV 得到更广泛的采用。为了促进燃料电池电动车的发展,多个政府机构和商业实体正在共同投资燃料电池技术的进步和加氢基础设施的建设。根据国际能源总署的数据,到 2021年终,全球将有约 730 个加氢站 (HRS),为约 51,600 辆 FCEV 供应燃料。这意味着从2020年起,全球FCEV保有量将增加近50%,HRS数量将增加35%。这些因素有助于 FCEV 未来的高速成长。

严格的政府法规推动电动车的普及

- MLCC 具有耐高温和易于表面黏着技术的外形规格,已成为电动车电子设备和子系统的首选组件。一辆电动车大约使用 8,000 到 10,000 个 MLCC。电动车中的 MLCC 通常用于电池管理系统 (BMS)、车载充电器 (OBC) 和 DC/DC 转换器。除了满足这些电动汽车子系统所需的通用规格并能够在电动车内部的恶劣环境中可靠运作外,零件製造商还必须符合 IATF16949 资格和 AEC-Q200 标准。

- 预计2022年电动车出货量将达1,640万辆,2029年将增加至2,552万辆。为减少温室气体排放、应对气候变化,多个国家实施了严格的环境法规。因此,汽车製造商面临越来越大的压力,需要生产更多的电动车并减少对石化燃料的依赖。消费者的环保意识也越来越强,寻求传统汽油动力汽车的永续替代品。

- 新冠疫情和俄罗斯在乌克兰的战争扰乱了全球供应链,汽车产业受到严重影响。但从长远来看,电动车市场在世界某些地区的销售量正在成长。同时,政府和企业努力支持部署公共充电基础设施,为电动车销售的进一步成长奠定了坚实的基础。全球公共充电桩数量已接近180万个,2021年安装量将接近50万个,其中三分之一为快速充电桩,超过2017年安装的公共充电桩总数。

汽车MLCC产业概况

汽车MLCC市场适度整合,前五大企业占60.58%。此市场的主要企业有:京瓷AVX元件株式会社(京瓷株式会社)、村田製作所、TDK株式会社、华新科技株式会社和国巨株式会社(依字母顺序排列)。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章执行摘要和主要发现

第二章 报告要约

第三章 引言

- 研究假设和市场定义

- 研究范围

- 调查方法

第四章 产业主要趋势

- 汽车销售

- 全球BEV(纯电动车)产量

- 全球电动车销量

- 全球FCEV(燃料电池电动车)产量

- 全球HEV(混合动力电动车)产量

- 全球重型商用车销售

- 全球ICEV(内燃机汽车)产量

- 全球轻型商用车销售

- 非电动车的全球销量

- 全球插电式混合动力汽车(PHEV)产量

- 全球乘用车销量

- 全球摩托车销售

- 法律规范

- 价值炼和通路分析

第五章市场区隔

- 车辆类型

- 重型商用车

- 轻型商用车

- 搭乘用车

- 摩托车

- 燃料类型

- 电动车

- 非电动车

- 推进类型

- 纯电动车

- FCEV-燃料电池电动车

- HEV-混合动力电动车

- ICEV-内燃机汽车

- PHEV - 插电式油电混合动力电动车

- 其他的

- 组件类型

- ADAS

- 资讯娱乐

- 动力传动系统

- 安全系统

- 其他的

- 錶壳尺寸

- 0 603

- 0 805

- 1 206

- 1 210

- 1 812

- 其他的

- 电压

- 50V~200V

- 小于50V

- 200V以上

- 电容

- 10μF 至 1,000μF

- 小于10μF

- 1,000μF 以上

- 介电类型

- 1级

- 2级

- 地区

- 亚太地区

- 欧洲

- 北美洲

- 世界其他地区

第六章 竞争格局

- 关键策略趋势

- 市场占有率分析

- 商业状况

- 公司简介

- Kyocera AVX Components Corporation(Kyocera Corporation)

- Maruwa Co ltd

- Murata Manufacturing Co., Ltd

- Nippon Chemi-Con Corporation

- Samsung Electro-Mechanics

- Samwha Capacitor Group

- Taiyo Yuden Co., Ltd

- TDK Corporation

- Vishay Intertechnology Inc.

- Walsin Technology Corporation

- Wurth Elektronik GmbH & Co. KG

- Yageo Corporation

第 7 章 CEO 的关键策略问题CEO 的关键策略问题

第 8 章 附录

- 世界概况

- 概述

- 五力分析框架

- 全球价值链分析

- 市场动态(DRO)

- 资讯来源及延伸阅读

- 图片列表

- 关键见解

- 资料包

- 词彙表

简介目录

Product Code: 50001984

The Automotive MLCC Market size is estimated at 2.94 billion USD in 2024, and is expected to reach 15.36 billion USD by 2029, growing at a CAGR of 39.23% during the forecast period (2024-2029).

Unveiling the multifaceted role of MLCCs in the automotive evolution is driving MLCC demand

- In the ever-evolving landscape of the automotive industry, the role of MLCCs has moved beyond mere electronic components. These miniature powerhouses are the cornerstone of modern vehicular systems, orchestrating a symphony of functions ranging from power distribution and noise suppression to signal conditioning and voltage regulation.

- The 0 603 MLCCs are compact yet indispensable contributors. These capacitors play a pivotal role in shifting toward compact and energy-efficient designs. With advancements in automotive technologies, the demand for streamlined solutions has elevated the prominence of the 0 603 segment.

- The 0 805 capacitors occupy a significant position in the market, particularly as electric vehicles (EVs) become mainstream. The surge in EV adoption emphasizes the need for effective power distribution and control, underscoring the relevance of the 0 805 segment. As EVs redefine the automotive landscape, these capacitors act as enablers of performance and efficiency.

- The 1 206 capacitors represent a balance between size and versatility, making them a preferred choice for diverse automotive applications. As the automotive industry embraces technological advancements, the importance of the 1 210 segment becomes evident.

- The 'others' segment encompasses an array of capacitance values that cater to specialized automotive requirements. From emerging technologies to unique applications, this diverse segment exemplifies the adaptable nature of MLCCs in meeting distinct automotive needs.

Unveiling the impact of MLCCs in Asia-Pacific, Europe, and North America

- Asia-Pacific, Europe, and North America are driving transformative changes in the automotive industry. Their pursuit of technological advancements, sustainability, and smart mobility solutions underscores the crucial role of multi-layer ceramic capacitors (MLCCs) in supporting the evolution of vehicles. As each region propels toward a future of innovation and efficiency, the demand for high-quality MLCCs continues to grow, cementing their significance in the automotive value chain.

- Asia-Pacific stands as an epicenter of automotive innovation characterized by rapid technological advancements and growing consumer demand. With major automotive hubs like China, Japan, and South Korea, this region is at the forefront of electric vehicle (EV) adoption, connected cars, and autonomous driving.

- Europe's automotive industry is synonymous with innovation, sustainability, and stringent environmental regulations. The region's commitment to reducing carbon emissions and transitioning toward cleaner mobility solutions is reshaping the automotive landscape. As electric and hybrid vehicles gain traction, the demand for MLCCs for power management, noise suppression, and voltage regulation is escalating.

- North America's automotive sector is characterized by its pursuit of smart mobility solutions and advanced technologies. As North American consumers seek enhanced driving experiences and cutting-edge features, the demand for MLCCs in applications like EVs, infotainment systems, and ADAS is on the rise. The region's dynamic automotive landscape positions it as a key driver of the MLCC market's expansion.

Global Automotive MLCC Market Trends

Infrastructure improvement for hydrogen stations continues to increase sales

- Fuel cell electric vehicles (FCEVs) use hydrogen energy stored as fuel, which is then converted into electricity by the fuel cell and has a propulsion mechanism similar to that of an electric vehicle. Compared to vehicles powered by conventional internal combustion engines, FCEVs do not emit any harmful exhaust emissions.

- Fuel cell electric vehicle shipments accounted for 0.043 million units in 2022, and these are expected to reach 0.071 million units in 2029. As renewable energies like wind and solar contribute increasingly to the hydrogen manufacturing process, there will be a huge increase in the demand for energy-efficient FCEVs.

- As the demand for low-emission vehicles rises, stricter carbon emission standards are being implemented, and more emphasis is being placed on the adoption of FCEVs due to benefits like quick refueling. To encourage the development of FCEVs, several government and commercial organizations are collaborating and investing in advancing fuel cell technology and the development of hydrogen refueling infrastructure. According to the IEA, at the end of 2021, there were about 730 hydrogen refueling stations (HRSs) globally providing fuel for about 51,600 FCEVs. This represents an increase of almost 50% in the global stock of FCEVs and a 35% increase in the number of HRSs from 2020. These factors contribute to the high growth of FCEVs in the future.

Stringent government regulations are increasing the penetration of electric vehicles

- MLCCs have emerged as a perfect component for EV electronics and subsystems, offering high-temperature resistance and an easy surface-mount form factor. Approximately 8,000-10,000 MLCCs are used in an electric vehicle. MLCCs in electric vehicles are commonly used in battery management systems (BMS), onboard chargers (OBC), and DC/DC converters. In addition to meeting the general specifications required for these EV subsystems and having the ability to function reliably in harsh environments inside an EV, component manufacturers should also be IATF 16949-certified and compliant with AEC-Q200.

- Electric vehicle shipments accounted for 16.4 million units in 2022, and it is expected to rise to 25.52 million units in 2029. Several countries have implemented strict environmental regulations to reduce greenhouse gas emissions and combat climate change. As a result, automakers are under increasing pressure to produce more electric vehicles and reduce their reliance on fossil fuels. Consumers are becoming more environmentally conscious and are looking for more sustainable alternatives to traditional gasoline-powered vehicles.

- The COVID-19 pandemic and Russia's war in Ukraine disrupted global supply chains, and the automotive industry has been heavily impacted. However, in the longer term, the EV market is witnessing sales growth in some regions of the world as government and corporate efforts to support the deployment of publicly available charging infrastructure are providing a solid basis for further increase in EV sales. Publicly accessible chargers worldwide approached 1.8 million, with nearly 500,000 chargers installed in 2021, of which a third were fast chargers, which accounted for more than the total number of public chargers installed in 2017.

Automotive MLCC Industry Overview

The Automotive MLCC Market is moderately consolidated, with the top five companies occupying 60.58%. The major players in this market are Kyocera AVX Components Corporation (Kyocera Corporation), Murata Manufacturing Co., Ltd, TDK Corporation, Walsin Technology Corporation and Yageo Corporation (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Automotive Sales

- 4.1.1 Global BEV (Battery Electric Vehicle) Production

- 4.1.2 Global Electric Vehicles Sales

- 4.1.3 Global FCEV (Fuel Cell Electric Vehicle) Production

- 4.1.4 Global HEV (Hybrid Electric Vehicle) Production

- 4.1.5 Global Heavy Commercial Vehicles Sales

- 4.1.6 Global ICEV (Internal Combustion Engine Vehicle) Production

- 4.1.7 Global Light Commercial Vehicles Sales

- 4.1.8 Global Non-Electric Vehicle Sales

- 4.1.9 Global PHEV (Plug-in Hybrid Electric Vehicle) Production

- 4.1.10 Global Passenger Vehicles Sales

- 4.1.11 Global Two-Wheeler Sales

- 4.2 Regulatory Framework

- 4.3 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

- 5.1 Vehicle Type

- 5.1.1 Heavy Commercial Vehicle

- 5.1.2 Light Commercial Vehicle

- 5.1.3 Passenger Vehicle

- 5.1.4 Two-Wheeler

- 5.2 Fuel Type

- 5.2.1 Electric Vehicle

- 5.2.2 Non-Electric Vehicle

- 5.3 Propulsion Type

- 5.3.1 BEV - Battery Electric Vehicle

- 5.3.2 FCEV - Fuel Cell Electric Vehicle

- 5.3.3 HEV - Hybrid Electric Vehicle

- 5.3.4 ICEV - Internal Combustion Engine Vehicle

- 5.3.5 PHEV - Plug-in Hybrid Electric Vehicle

- 5.3.6 Others

- 5.4 Component Type

- 5.4.1 ADAS

- 5.4.2 Infotainment

- 5.4.3 Powertrain

- 5.4.4 Safety System

- 5.4.5 Others

- 5.5 Case Size

- 5.5.1 0 603

- 5.5.2 0 805

- 5.5.3 1 206

- 5.5.4 1 210

- 5.5.5 1 812

- 5.5.6 Others

- 5.6 Voltage

- 5.6.1 50V to 200V

- 5.6.2 Less than 50V

- 5.6.3 More than 200V

- 5.7 Capacitance

- 5.7.1 10 µF to 1000 µF

- 5.7.2 Less than 10 µF

- 5.7.3 More than 1000µF

- 5.8 Dielectric Type

- 5.8.1 Class 1

- 5.8.2 Class 2

- 5.9 Region

- 5.9.1 Asia-Pacific

- 5.9.2 Europe

- 5.9.3 North America

- 5.9.4 Rest of the World

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Kyocera AVX Components Corporation (Kyocera Corporation)

- 6.4.2 Maruwa Co ltd

- 6.4.3 Murata Manufacturing Co., Ltd

- 6.4.4 Nippon Chemi-Con Corporation

- 6.4.5 Samsung Electro-Mechanics

- 6.4.6 Samwha Capacitor Group

- 6.4.7 Taiyo Yuden Co., Ltd

- 6.4.8 TDK Corporation

- 6.4.9 Vishay Intertechnology Inc.

- 6.4.10 Walsin Technology Corporation

- 6.4.11 Wurth Elektronik GmbH & Co. KG

- 6.4.12 Yageo Corporation

7 KEY STRATEGIC QUESTIONS FOR MLCC CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

02-2729-4219

+886-2-2729-4219

汽车多层晶片铁氧体磁珠市场按类型、封装类型、尺寸、频段、应用和最终用途划分,全球预测(2026-2032年)电动车MLCC市场按介质类型、电容范围、额定电压、应用和销售管道,全球预测,2026-2032年

汽车多层晶片铁氧体磁珠市场按类型、封装类型、尺寸、频段、应用和最终用途划分,全球预测(2026-2032年)电动车MLCC市场按介质类型、电容范围、额定电压、应用和销售管道,全球预测,2026-2032年 汽车多层压敏电阻市场:按类型、车辆类型、工作电压、应用、国家及地区划分-全球产业分析、市场规模、市场占有率及2025-2032年预测

汽车多层压敏电阻市场:按类型、车辆类型、工作电压、应用、国家及地区划分-全球产业分析、市场规模、市场占有率及2025-2032年预测 全球汽车MLCC市场

全球汽车MLCC市场 电动车 MLCC:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)

电动车 MLCC:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年) 汽车多层压敏电阻市场-全球产业分析、规模、份额、成长、趋势及预测(2025-2035)

汽车多层压敏电阻市场-全球产业分析、规模、份额、成长、趋势及预测(2025-2035) 汽车 MLCC 市场机会、成长动力、产业趋势分析与预测 2024 - 2032 年

汽车 MLCC 市场机会、成长动力、产业趋势分析与预测 2024 - 2032 年 2024-2028年全球汽车MLCC市场

2024-2028年全球汽车MLCC市场