|

市场调查报告书

商品编码

1685698

虚拟实境 (VR) - 市场占有率分析、产业趋势与统计、成长预测(2024-2029)Virtual Reality (VR) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

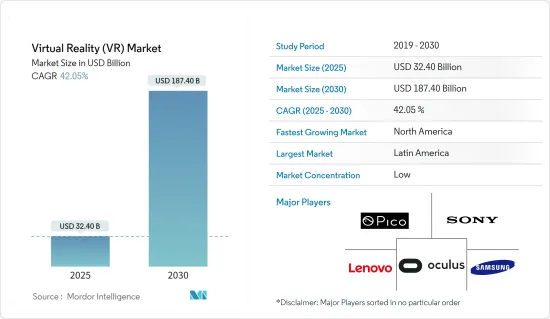

虚拟实境市场规模预计在 2024 年为 228.1 亿美元,预计到 2029 年将达到 1319.3 亿美元,预测期内(2024-2029 年)的复合年增长率为 42.05%。

主要亮点

- 虚拟实境主要利用科技来创造模拟环境。与传统使用者介面不同,VR 让使用者置身于体验之中。这意味着用户无需看着面前的显示器萤幕,而是可以沉浸在 3D 世界中并与之互动。透过模拟尽可能多的感官,包括视觉、触觉、听觉甚至嗅觉,这项技术正在改变世界。

- 学校利用 VR 技术最常见的原因之一是允许学生进行虚拟实地考察。实地考察是教育机构的悠久传统。这是因为它允许教师在身临其境型环境中教育学生,提供课堂上难以实现的实践学习机会。然而,实地考察对于一些学生来说可能会在经济上造成困难。对于行动不便的学生来说,这也会很困难。

- 随着远端工作和虚拟协作的兴起,对能够让人们在虚拟空间中进行互动和协作的 VR 软体的需求日益增长。 VR 会议平台、虚拟活动空间和协作设计工具可让使用者无论身处何处,都可以在沉浸式虚拟环境中协同工作。它也用于医疗保健等各种行业,用于医疗培训、手术模拟、疼痛管理、暴露疗法和復健。医疗保健领域对 VR 软体的需求源于其改善病患治疗效果、加强医学教育和降低医疗成本的潜力。

- 虚拟实境正在成为一项革命性的技术,能够对各种终端使用者产业产生显着影响。该技术正在持续发展,导致使用案例的广泛扩展。

- VR 通常透过追踪头部和眼球运动的耳机来实现。有些系统使用其他周边设备(例如手套)来模拟额外的感觉。对于许多消费者来说,这项技术价格昂贵,高阶 VR 设备需要功能强大的 PC 和游戏机,这限制了该技术的广泛应用。

- 自从新冠疫情爆发以来,我们看到远距协作和团队建立练习增加。与传统视讯会议工具相比,VR技术带来了更具沉浸感和互动性的体验。此外,该技术迎合了全球日益增长的游戏趋势,促进游戏成为一种娱乐形式,并有助于提供虚拟实境游戏体验。

虚拟实境(VR)市场趋势

游戏是一个蓬勃发展的终端用户产业

- 全球 AR 和 VR 游戏玩家的快速成长正在拓宽市场视野。据人工智慧、机器学习、巨量资料分析和 AR/VR 解决方案提供商 NewGenApps 称,到 2025 年,全球 AR 和 VR 游戏用户群预计将成长到 2.16 亿。

- 此外,对电玩游戏的需求不断增长,为供应商提供VR头戴装置创造了机会。 Uswitch 的 2023 年线上游戏统计数据显示,全球约有 40% 的人口参与线上游戏。在过去的几十年里,元宇宙已经从本地的单人和多人体验发展成为一个跨越国家和大洲的全球舞台。

- 伙伴关係、协作和併购等策略性倡议为主要市场参与者扩大市场占有率提供了重要机会。例如,2023年10月,总部位于印度艾哈默德巴德的主要企业Yudiz Solutions宣布与主要通讯业者沃达丰印度(Vi)合作推出一款VR战斗射击游戏,并在2023年印度行动通讯大会上展示了其功能。 5G技术将用于为VR战斗射击游戏提供动力,用户可以期待在虚拟实境中获得响应迅速、互动性强且身临其境的低延迟体验。

- VR 游戏在各个年龄层的玩家中越来越受欢迎,扩大了消费者群体。 Oculus Quest 系列等价格实惠的 VR 装置的出现,使得更广泛的消费者可以玩 VR 游戏。开发人员拥有巨大的机会来创建更引人注目的 VR 游戏,并利用 VR 技术的独特功能。

- 游戏产业认识到VR的市场潜力。随着科技变得越来越普及和价格越来越便宜,对 VR 游戏体验的需求也越来越大。游戏开发商和发行商将 VR 视为创造令人兴奋、身临其境的体验的机会,可以吸引新的受众并在拥挤的市场中脱颖而出。

北美占最大市场占有率

- 北美对虚拟实境 (VR) 的需求正在快速增长,这在很大程度上是由于各个行业的个人越来越多地参与这项技术。这种需求的成长是由 VR 技术的多样化用途所推动的,这些用途涵盖娱乐和游戏、教育、医疗保健和企业解决方案。

- 技术进步使得 VR 设备更加易于存取和用户友好,进一步推动了对 VR 的需求。 VR头戴装置价格低廉且效能不断提升,促使其在北美广泛普及,从技术爱好者到寻求新颖有趣体验的普通用户。因此,许多公司正在推出新产品以增加市场占有率。

- 随着虚拟实境变得越来越容易取得和使用,它为政府探索创新方法提供了巨大的潜力。因此,美国政府正在将 VR 作为跨产业的一种有价值的工具。例如,美国食品药物管理局于2023年9月宣布,一些通常仅在医生办公室或医院提供的临床服务可以透过VR提供给在家中或其他非临床环境中的患者。

- 此外,在终端用户产业中,教育领域预计在预测期内将大幅成长。北美各地的教育机构正在将 VR 纳入其课程,为学生提供实践体验式学习机会。虚拟实地考察、模拟和互动课程增强了学习体验,使复杂的概念更容易理解,并促进了对一系列学科的更深入的理解。

- 这些因素显示对 VR 的需求正在成长。随着 VR 的发展及其在各个行业的普及,它可能会改变个人和行业与数位时代的互动方式。北美 VR 应用的发展轨迹表明,未来身临其境型体验将成为日常生活中不可或缺的一部分。因此,上述因素可能会促进所研究市场的成长。

虚拟实境(VR)产业概览

虚拟实境市场是分散的。随着 VR 公司专注于透过游戏、娱乐、培训和行销等用途为更广泛的大众受众带来可及性,市场竞争正在加剧。在这个行业中,由于各公司的成长,竞争对手之间的敌意很高。预计竞争将继续加剧。主要企业包括 Oculus VR LLC、联想集团有限公司、三星电子、Sony Corporation和 Pico Interactive Inc.

- 2024 年 1 月,高通技术公司宣布与 RayNeo 和应用材料公司建立策略合作伙伴关係,共同开发并向市场推出领先的下一代 AR 眼镜。此次合作预计将汇集领先科技供应商的专业知识,重新定义 AR 眼镜的未来。 RayNeo 的 AR 眼镜利用高通的骁龙 AR1 Gen1 平台和应用材料的轻量全彩波导管,为消费级 AR 产品打造全面的软体和硬体生态系统。

- 2023 年 11 月,Pico 宣布推出其下一代一体式VR头戴装置PICO 4,旨在透过结合舒适性和性能让每个人都能享受虚拟实境。 PICO 4 基于 Snapdragon XR2 平台,具有超轻机身、薄饼光学系统、4K 显示器和直觉的使用者介面。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概览

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买家的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争强度

- 产业价值链分析

- 评估影响市场的宏观经济因素

第五章市场动态

- 市场驱动因素

- VR 的商业应用日益增多

- 不同终端使用者群体对 VR 培训设备的需求不断增长

- 市场挑战/限制

- 长期使用VR头戴装置的健康风险

- 晕动症的影响

第六章市场区隔

- 按类型

- 硬体

- 系留式 HMD

- 独立式 HMD

- 无萤幕检视器

- 软体

- 硬体

- 按最终用户产业

- 游戏

- 媒体与娱乐

- 零售

- 卫生保健

- 军事和国防

- 房地产

- 教育

- 按地区

- 北美洲

- 欧洲

- 亚洲

- 澳洲和纽西兰

- 拉丁美洲

- 中东和非洲

第七章竞争格局

- 公司简介

- Oculus VR LLC

- Sony Corporation

- Samsung Electronics Co. Ltd

- Lenovo Group Ltd

- Pico Interactive Inc.

- Qualcomm Technologies Inc.

- FOVE Inc.

- Unity Technologies Inc.

- Unreal Engine(Epic Games Inc.)

- Apple Inc.

- DPVR(Lexiang Technology Co. Ltd)

- Autodesk Inc.

- Eon Reality Inc.

- 3D Systems Corporation

- Dassault Systemes SE

- HTC Vive(HTC Corporation)

第八章投资分析

第九章:市场的未来

The Virtual Reality Market size is estimated at USD 22.81 billion in 2024, and is expected to reach USD 131.93 billion by 2029, growing at a CAGR of 42.05% during the forecast period (2024-2029).

Key Highlights

- Virtual reality primarily uses technology to create a simulated environment. Unlike the traditional user interface, VR places the user inside an experience, which means that instead of viewing a monitor screen in front of them, users are immersed and can interact with the 3D world. With the simulation of as many senses as possible, such as vision, touch, hearing, and even smell, the technology has been transformed worldwide.

- One of the most popular reasons schools are taking advantage of VR technology is its ability to let students take field trips virtually. Field trips are a time-honored tradition for educational institutions. They allow teachers to educate their students in immersive environments and provide hands-on learning opportunities that would otherwise be difficult to achieve within the classroom. However, field trips can be financially prohibitive for some students. They can also be challenging for students with mobility limitations.

- With the rise of remote work and virtual collaboration, there is a growing demand for VR software that enables users to interact and collaborate in virtual spaces. VR meeting platforms, virtual event spaces, and collaborative design tools allow users to work together in immersive virtual environments regardless of physical location. It is also used in various industries, including healthcare, for medical training, surgical simulations, pain management, exposure therapy, and rehabilitation. The demand for VR software in healthcare is driven by its potential to improve patient outcomes, enhance medical education, and reduce healthcare costs.

- Virtual reality is emerging as a revolutionary technology that can notably impact various end-user industries. The technology is witnessing continuous growth, leading to significant expansion in the number of use cases.

- VR is usually accessed using a headset that tracks the movement of the head and eye. Some systems also use other peripherals (e.g. gloves) to simulate additional senses. This technology is expensive for many consumers, and high-end VR sets require powerful PCs or gaming consoles, which is restricting widespread adoption of the technology.

- Since the COVID-19 pandemic, remote collaboration and team-building exercises have increased. VR technology facilitated immersive and interactive experiences more than traditional videoconferencing tools. Moreover, this technology caters to the growing gaming trend globally, which facilitates gaming as a form of entertainment and helps in providing VR gaming experiences.

Virtual Reality (VR) Market Trends

Gaming to be the Fastest-growing End-user Industry

- Rapid growth in AR and VR gamers worldwide has expanded the market's horizon. According to NewGenApps, a provider of artificial intelligence, machine learning, big data analytics, and AR/VR solutions, the global user base of AR and VR games is estimated to increase to 216 million users by 2025.

- Moreover, the increasing demand for video games creates an opportunity for vendors to offer VR headsets. Uswitch's 2023 online gaming statistics revealed that approximately 40% of the global population engages in online gaming. Over the past few decades, the metaverse has evolved from local single and multiplayer experiences to a global stage, spanning countries and continents.

- Strategic initiatives like partnerships, collaborations, and mergers and acquisitions give major market players a significant chance to expand their market presence. For instance, in October 2023, Yudiz Solutions, a leading digital transformation and game development company based in Ahmedabad, India, showcased its capabilities at the India Mobile Congress 2023 by unveiling a VR combat shooting game in partnership with leading telecom operator Vodafone India (Vi). 5G technology is used to power VR combat shooting games, and users can expect a low latency experience that allows them to be responsive and interactively immersed in virtual reality.

- The increasing popularity of VR gaming among various age groups is expanding the consumer base. Introducing affordable VR handsets like the Oculus Quest series has made VR gaming accessible to a more extensive consumer base. There is a significant opportunity for developers to create more engaging VR games that can employ the unique capabilities of VR technology.

- The gaming industry recognizes the market potential of VR. As the technology becomes more accessible and affordable, the demand for VR gaming experiences is increasing. Game developers and publishers see VR as an opportunity to reach new audiences and create exciting, immersive experiences that stand out in a crowded market.

North America Holds the Largest Market Share

- The demand for VR in North America has experienced rapid growth owing to the significant shift in individuals across various sectors engaging with technology. This increasing demand is fueled by the various applications of VR technology, ranging from entertainment and gaming to education, healthcare, and enterprise solutions.

- The demand for VR is further propelled by technological advancements, making VR devices more accessible and user-friendly. The affordability and improved performance of VR headsets have contributed to broader adoption across North America, from tech enthusiasts to casual users seeking novel and engaging experiences. Hence, many companies are launching new products to increase their market share.

- Also, as VR becomes more accessible and easier to use, it offers a lot of great possibilities for the government to explore innovative approaches. Hence, the US government uses VR as a valuable tool across multiple industries. For instance, in September 2023, the US Food and Drug Administration announced that VR could deliver some clinical services, normally delivered only in clinics and hospitals, to patients in their homes or other non-clinical settings.

- Moreover, among end-user industries, the education segment is expected to grow significantly during the forecast period. North American educational institutions are integrating VR into their curricula to provide students with hands-on, experiential learning opportunities. Virtual field trips, simulations, and interactive lessons enhance the learning experience, making complex concepts more accessible and fostering a deeper understanding of various subjects.

- These factors indicate the growing demand for VR. As VR evolves and becomes more accessible, various industries will shape how individuals and industries interact with the digital era. The trajectory of VR adoption in North America suggests a future where immersive experiences become an integral part of everyday life. Hence, the abovementioned factors will boost the growth of the market studied in the future.

Virtual Reality (VR) Industry Overview

The virtual reality market is fragmented in nature. It is witnessing a rise in competitiveness among companies as VR companies are focused on providing accessibility to larger masses through gaming, entertainment, training, and marketing, among other applications. The competitive rivalry is high in this industry, owing to growth among various companies. Competition is expected to increase in the future. Some major players include Oculus VR LLC, Lenovo Group Ltd, Samsung Electronics Co. Ltd, Sony Corporation, and Pico Interactive Inc.

- In January 2024, Qualcomm Technologies announced strategic collaborations with RayNeo and Applied Materials to develop and bring the next generation of market-leading AR glasses to market. This collaboration is expected to bring together the expertise of industry-leading technology providers to redefine the future of AR glasses. RayNeo's AR glasses will utilize Qualcomm's Snapdragon AR1 Gen1 platform and Applied Materials' lightweight full-color waveguides to create a comprehensive software and hardware ecosystem for consumer-grade AR products.

- In November 2023, Pico announced the launch of PICO 4, a next-generation, all-in-one VR headset designed to make virtual reality accessible to everyone by combining comfort and performance. PICO 4 is based on the Snapdragon XR2 platform and features an ultra-light body, pancake optics, a 4K display, and an intuitive user interface.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of Macroeconomic Factors on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Adoption of VR in Commercial Applications

- 5.1.2 Growing Demand for VR Setups for Training Across Various End-user Segments

- 5.2 Market Challenges/Restraints

- 5.2.1 Health Risks from Using VR Headsets in the Longer Run

- 5.2.2 Impact of Cybersickness

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Hardware

- 6.1.1.1 Tethered HMD

- 6.1.1.2 Standalone HMD

- 6.1.1.3 Screenless Viewer

- 6.1.2 Software

- 6.1.1 Hardware

- 6.2 By End-user Industry

- 6.2.1 Gaming

- 6.2.2 Media and Entertainment

- 6.2.3 Retail

- 6.2.4 Healthcare

- 6.2.5 Military and Defense

- 6.2.6 Real Estate

- 6.2.7 Education

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia

- 6.3.4 Australia and New Zealand

- 6.3.5 Latin America

- 6.3.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Oculus VR LLC

- 7.1.2 Sony Corporation

- 7.1.3 Samsung Electronics Co. Ltd

- 7.1.4 Lenovo Group Ltd

- 7.1.5 Pico Interactive Inc.

- 7.1.6 Qualcomm Technologies Inc.

- 7.1.7 FOVE Inc.

- 7.1.8 Unity Technologies Inc.

- 7.1.9 Unreal Engine (Epic Games Inc.)

- 7.1.10 Apple Inc.

- 7.1.11 DPVR (Lexiang Technology Co. Ltd)

- 7.1.12 Autodesk Inc.

- 7.1.13 Eon Reality Inc.

- 7.1.14 3D Systems Corporation

- 7.1.15 Dassault Systemes SE

- 7.1.16 HTC Vive (HTC Corporation)