|

市场调查报告书

商品编码

1685708

电动马达:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Electric Motors for Electric Vehicle - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

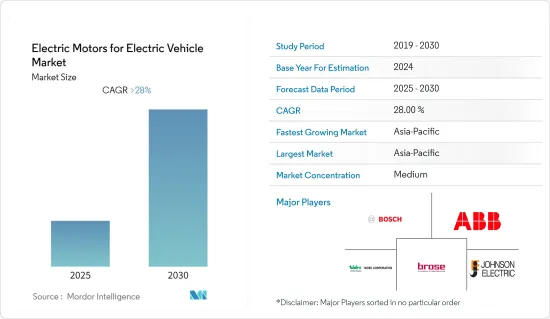

预计预测期内电动马达电动马达市场复合年增长率将超过 28%。

新冠疫情导致製造业停摆、封锁和贸易限制,对 2020 年上半年电动车产业的马达产生了负面影响。然而,新冠疫情后的復苏、更严格的车辆排放气体标准以及政府为加快电动车普及而提供的慷慨奖励,导致电动车销量非常健康地增长。此外,电动汽车马达的销量也大幅成长。例如,2020年电动乘用车销量飙升至310万辆,较2019年成长39%。

此外,製造商已实施应急计划,透过多样化生产和供应链来减轻未来的业务不确定性,以确保与汽车行业关键领域的客户的连续性。例如

主要亮点

- 2020 年 2 月,Brose Fahrzeugteile SE & Co. KG 在印度普纳附近的 Hinjewadi 开设了新园区。新工厂将僱用 430 名员工。 Brose Fahrzeugteile SE & Co. KG 宣布将在未来几年向印度投资 6,000 万欧元(6,240 万美元)。

从长远来看,严格的排放和燃油经济性法规的颁布、政府奖励以及充电基础设施的改善导致电动车销量增加,是推动研究市场成长的关键因素。丰田、本田、特斯拉、通用汽车和福特等主要汽车公司对电动车的大规模投资预计很快就会推动电动马达市场的发展。此外,马达製造商和汽车公司之间日益增长的伙伴关係预计将在全球范围内扩大所研究的市场。

从地理位置来看,由于中国和印度等新兴市场的存在,预计亚太地区将在预测期内成为最大的马达市场。由于政府采取措施抑制二氧化碳排放,欧洲一直是市场发展的动力。英国、德国和法国正在为该地区的市场扩张做出贡献。

因此,上述因素可能会进一步推动全球电动汽车马达市场的成长。

电动汽车马达市场趋势

电动车需求成长将推动市场成长

由于中国、美国、日本、韩国和欧洲的电动车销量快速成长,马达的需求预计将呈指数级增长。由于各国政府推出的推广电动车的奖励、普通购车者环保意识的增强以及燃料价格的上涨,全球电动车销售量呈指数级增长。造成这种情况的其他因素包括电动车的营业成本低于传统内燃机汽车,以及中国和欧盟政府宣布将在 2035 年前禁止所有内燃机汽车出行。例如

- 2021年,全球电动车註册量达690万辆,与前一年同期比较成长107%。

推动电动车马达成长的主要因素是对提高电动车行驶里程的需求不断增加,预计这将对电动车马达市场的成长产生积极影响。

此外,世界各国政府都在积极实施鼓励采用电动车的政策。中国、印度、法国和英国已宣布计划在 2040 年前逐步淘汰汽油和柴油汽车。例如,

- 2022年10月,欧盟宣布将从2035年起禁止在欧盟成员国销售新的内燃机汽车。

- 欧洲宣布了2050年实现气候中和的宏伟目标。未来几年,欧盟委员会预计将提出几项新的立法提案来实现这一目标。其中许多旨在提高机动性。为了实现这一目标,我们需要一套政策和目标,引导国家、企业和消费者走上正确的道路。欧盟委员会已从其 7,500 亿欧元(7,800 亿美元)的新冠疫情奖励策略中拨款 200 亿欧元(212 亿美元),用于快速广泛地采用清洁出行方式。欧盟也宣布,到2030年将推动洁净汽车,包括3,000万辆电动车和100万辆氢动力汽车。

- 2022年9月,中国宣布将对新能源电动车(包括纯电动车、混合动力车、插电式混合动力车和氢燃料电池车)免征5%的购置税政策延长至2023年终。

- 2021年,印度联邦政府宣布将混合动力汽车和电动车快速采用和製造(FAME)计画第二阶段延长两年,至2024年3月31日。该计划旨在促销。

此外,政府和私人公司打算在全球范围内建造充电基础设施,以最大限度地减少排放气体并保持环保。因此,对电动车不断增长的需求将进一步推动马达在汽车中的应用,从而在预测期内增加马达的製造。

亚太地区可望主导市场

在全球范围内,亚太地区占据电动马达市场的最大份额。中国和印度是亚太地区最突出的电动车製造商和消费国。国家销售目标、有利的立法和当地空气品质目标支持了这两个国家的国内需求。例如,

- 印度政府宣布,到 2022 年,将在未来三年内根据 FAME II(混合动力电动车的快速采用和製造)计划引进 7,000 辆电动公车、5,000 辆电动三轮车、55,000 辆电动四轮车(包括大功率混合动力汽车)和 10,000 辆电动二轮车。已为 FAME II(混合动力电动车的快速采用和製造)拨款 10 亿印度卢比(12 亿美元)。

- 中国对电动和混合动力汽车製造商设定了超过10%的新车销量配额。而北市每月仅发放1万张内燃机汽车登记许可证,以鼓励居民转换电动车。

这些国家的电动车销售每年也在大幅成长,进一步推动了马达市场的成长。例如

- 2021年中国乘用车销量为299万辆,与前一年同期比较去年成长169.1%。 2021年印度共售出17,802辆电动车,与前一年同期比较增长168%。

因此,由于上述因素,预计亚太地区仍将是电动汽车马达市场最主导的地区。

电动汽车马达产业概况

由于众多地区和国际参与者的存在,电动车马达市场得到了适度整合。主要参与者包括博世行动解决方案、ABB、日本电产公司、Brose Fahrzeugteile GmbH &Co.KG 和德昌电机集团。许多参与者正在透过合资、併购、推出新产品、扩大产能等方式巩固其市场地位。例如

- 2022 年 12 月,印度汽车零件製造商 Shriram Pistons Ltd. 宣布已收购 EMF Innovations 的多数股权,EMF Innovations 是一家总部位于新加坡的各类电动汽车马达设计和製造商。 SPR Engineous 是 Shriram Pistons Ltd 的全资子公司,将执行此交易。透过此次交易,我们将进入电动车市场并满足所有电动车细分市场的需求。

- 2022年10月,博世汽车出行解决方案宣布将投资2.6亿美元,扩大其位于美国南卡罗来纳州查尔斯顿工厂为Rivian R1T皮卡生产的电动马达马达的生产。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 调查前提条件

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场动态

- 市场驱动因素

- 市场限制

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买家/消费者的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争强度

第五章市场区隔

- 集会

- 轮毂

- 中央动力传动系统

- 应用

- 搭乘用车

- 商用车

- 马达类型

- 无刷直流马达

- 永磁同步马达

- 非同步马达

- 同步磁阻马达

- 其他(无铁心永磁马达、开关磁阻马达等)

- 输出

- 100kW以下

- 101~250 kW

- 超过250千瓦

- 地区

- 北美洲

- 美国

- 加拿大

- 北美其他地区

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 其他欧洲国家

- 亚太地区

- 印度

- 中国

- 日本

- 韩国

- 其他亚太地区

- 世界其他地区

- 南美洲

- 中东和非洲

- 北美洲

第六章竞争格局

- 供应商市场占有率

- 公司简介

- Aisin Seiki Co. Ltd

- Toyota Motor Corporation

- Hitachi Automotive Systems

- DENSO Corporation

- Honda Motor Company Ltd

- Mitsubishi Electric Corp.

- Magna International

- Robert Bosch GmbH

- BMW AG

- Nissan Motor Co. Ltd

- Tesla Inc.

- Toshiba Corporation

- BYD Co. Ltd

第七章 市场机会与未来趋势

第八章 免责声明

The Electric Motors for Electric Vehicle Market is expected to register a CAGR of greater than 28% during the forecast period.

COVID-19 led to manufacturing shutdowns, lockdowns, and trade restrictions that negatively impacted the electric motors for the electric vehicle industry in the first half of the year 2020. However, the post-COVID-19 recovery, the stringent automotive emissions norms adoption, and the provision of generous government incentives for the quick adoption of electromobility led to a very healthy rise in the sales of electric vehicles. It further produced significant growth in the sales of electric motors for electric cars. For instance, in 2020, electric passenger vehicle sales jumped to 3.1 million units, an increase of 39% over 2019.

In addition, the manufacturers implemented contingency plans to mitigate future business uncertainties to retain continuity with clients in the critical sectors of the automobile industry by diversifying their manufacturing and supply chains. For instance,

Key Highlights

- In February 2020, Brose Fahrzeugteile SE & Co. KG opened its new campus in India at Hinjewadi near Pune. The new location will employ 430 people. Brose Fahrzeugteile SE & Co. KG announced an investment of EUR 60 million ( USD 62.4 million) in India in the future.

Over the long term, some of the major factors driving the growth of the market studied are the rising sales of electric vehicles due to the enactment of stringent emission and fuel economy norms, government incentives, and improving charging infrastructure. Massive investments in electric vehicles by major automotive companies, such as Toyota, Honda, Tesla, General Motors, and Ford, are expected to drive the electric motor market shortly. Additionally, the evolving partnerships between motor manufacturers and automotive companies are expected to expand the studied market globally.

Geographically Asia-Pacific is expected to be the largest electric motor market during the forecast period due to the presence of emerging markets such as China and India. Europe became a driving force in the market's development for the government's steps to curb carbon emissions. The United Kingdom, Germany, and France are all contributing to the market's expansion in this region.

Thus the factors mentioned above will further drive the growth in the electric motors for electric vehicles market globally.

Electric Vehicle Motor Market Trends

Rising Demand for Electric Vehicles to Augment Growth of Market

The demand for electric motors is expected to increase exponentially, owing to the rapid growth of electric vehicle sales across China, the United States, Japan, South Korea, and Europe. Electric vehicle sales are rising exponentially worldwide due to government incentives offered by various Governments to promote electromobility, increasing environmental consciousness amongst general car buyers, and rising fuel prices. It is also due to lower operating costs provided by electric vehicles than traditional ICE vehicles and announcements by the governments of China and the EU to ban ICE mobility by 2035. For instance,

- In 2021, 6.9 million electric cars were registered worldwide, an increase of 107% from the previous year.

The primary factor driving the electric vehicle motor growth is the increase in demand for improving the electric vehicles driving range, which is, in turn, anticipated to positively impact the electric motors market growth for electric cars.

Moreover, governments worldwide have also been proactive in enacting policies to encourage the adoption of electric vehicles. China, India, France, and the United Kingdom have announced plans to phase out the petrol and diesel vehicles industry entirely before 2040. For instance,

- In October 2022, European Union announced the ban on the sale of new ICE vehicles from 2035 in EU member states.

- Europe announced a lofty target of being climate-neutral by 2050. The European Commission will publish several new legislative proposals to meet this goal over the next few years. Many of them are aimed at improving mobility. To achieve this aim, a set of policies and targets must be in place to guide states, businesses, and consumers on the correct path. European Commission earmarked EUR 20 billion (USD 21.2 billion) in the COVID-19 stimulus package of EUR 750 billion (USD 780 billion) for the faster and widespread adoption of clean mobility. It announced the promotion of sales of clean vehicles, including 30 million electric and 1 million hydrogen vehicles, in the EU by 2030.

- In September 2022, China announced that it had extended the tax exemption from a 5% purchase tax to new energy electric vehicles, including battery electric vehicles, hybrid vehicles, plug-in hybrid vehicles, and hydrogen fuel cell vehicles, till the end of 2023.

- In 2021, The Union government of India announced an extension of the second phase of the Faster Adoption and Manufacturing of Hybrid and Electric vehicle (FAME) scheme by two years to March 31, 2024. The plan aims at promoting sales of electric vehicle adoption and manufacturing of components related to EVs.

In addition, the government and private companies intend to build charging infrastructure worldwide to minimize emissions and keep the environment green. Thus, the rising demand for electric vehicles further aggravates the adoption of electric motors in cars, augmenting the manufacturing of electric motors during the forecast period.

Asia-Pacific Anticipated to Dominate the Market

Globally, Asia-Pacific is capturing the largest share of the electric motors for the electric vehicle market, owing to high EV sales, majorly from China. China and India are the most prominent manufacturers and consumers of electric vehicles in the Asia-Pacific. National sales targets, favorable laws, and municipal air-quality targets are supporting domestic demand in both these countries. For instance,

- The Government of India announced having 7000 e-Buses, five lakh e-3 wheelers, 55000 e-4 wheeler passenger cars (including strong hybrids), and ten lakh e-2 wheelers over the next three years under FAME II (Faster Adoption and Manufacturing of Hybrid Electric Vehicles) by 2022. INR 10000 Cr (USD 1.2 billion) was allocated to FAME II (Faster Adoption and Manufacturing of Hybrid Electric Vehicles).

- China imposed a quota on manufacturers of electric or hybrid vehicles, which must represent at least 10% of total new sales. Also, Beijing only issues 10,000 permits for registering combustion engine vehicles per month to encourage its inhabitants to switch to electric cars.

Electric vehicles are also posting huge annual sales gains in these countries, which will further drive the growth in the market for electric motors. For instance,

- 2.99 million passenger electric vehicles were sold in China in 2021, an increase of 169.1% over the last year, while in India, 17802 units of electric cars were sold in 2021, registering a growth of 168% over the previous year.

Thus the factors above are expected to maintain Asia-Pacific as the most dominant region for electric motors for electric vehicles market.

Electric Vehicle Motor Industry Overview

The Electric motors for electric vehicles market is moderately consolidated due to the presence of many regional and international players. Some significant players include Bosch Mobility Solutions, ABB, Nidec Corporation, Brose Fahrzeugteile GmbH & Co. KG, and Johnson Electric Group. Many of these players are engaging in joint ventures, mergers and acquisitions, new product launches, and capacity expansions to cement their market positions. For instance

- In December 2022, Indian automotive component manufacturer Shriram Pistons Ltd. announced an acquisition majority stake in EMF Innovations, a Singapore-based designer and manufacturer of electric motors for all types of electric vehicles. SPR Engineous, a wholly-owned subsidiary of Shriram Pistons Ltd, would make the transaction. They will enter the EV market with this deal and cater to all EV market segments.

- In October 2022, Bosch Mobility Solutions announced to invest USD 260 million to expand the production of electric vehicle motors for the Rivian R1T pickup truck at its Charleston plant in South Carolina, in the US.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.2 Market Restraints

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Assembly

- 5.1.1 Wheel Hub

- 5.1.2 Central Power Train

- 5.2 Application

- 5.2.1 Passenger Cars

- 5.2.2 Commercial Vehicles

- 5.3 Motor Type

- 5.3.1 Brushless DC Motor

- 5.3.2 Permanent Magnet Synchronous Motor

- 5.3.3 Asynchronous Motor

- 5.3.4 Synchronous Reluctance Motor

- 5.3.5 Others (Axial Flux Ironless Permanent Magnet Motor, Switched Reluctance Motors, etc.

- 5.4 Power

- 5.4.1 Up to 100 kW

- 5.4.2 101-250 kW

- 5.4.3 Above 250 kW

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 India

- 5.5.3.2 China

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 Rest of the World

- 5.5.4.1 South America

- 5.5.4.2 Middle-East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Aisin Seiki Co. Ltd

- 6.2.2 Toyota Motor Corporation

- 6.2.3 Hitachi Automotive Systems

- 6.2.4 DENSO Corporation

- 6.2.5 Honda Motor Company Ltd

- 6.2.6 Mitsubishi Electric Corp.

- 6.2.7 Magna International

- 6.2.8 Robert Bosch GmbH

- 6.2.9 BMW AG

- 6.2.10 Nissan Motor Co. Ltd

- 6.2.11 Tesla Inc.

- 6.2.12 Toshiba Corporation

- 6.2.13 BYD Co. Ltd

7 MARKET OPPORTUNITIES AND FUTURE TRENDS**

8 DISCLAIMER

按冷却方式、马达类型、绕组技术和车辆类型分類的汽车马达铁芯市场,全球预测,2026-2032年

按冷却方式、马达类型、绕组技术和车辆类型分類的汽车马达铁芯市场,全球预测,2026-2032年 电动汽车马达市场报告:按功率、应用和地区划分(2026-2034 年)

电动汽车马达市场报告:按功率、应用和地区划分(2026-2034 年) 电动汽车马达市场-全球产业规模、份额、趋势、机会及预测(额定功率、马达类型、需求类别、地区及竞争格局划分,2021-2031年)汽车马达定子和转子市场按产品类型、材料类型、马达类型、车辆类型和应用划分-全球预测,2026-2032年电动车驱动马达核心市场按马达类型、功率范围、冷却系统和车辆类型划分,全球预测(2026-2032年)

电动汽车马达市场-全球产业规模、份额、趋势、机会及预测(额定功率、马达类型、需求类别、地区及竞争格局划分,2021-2031年)汽车马达定子和转子市场按产品类型、材料类型、马达类型、车辆类型和应用划分-全球预测,2026-2032年电动车驱动马达核心市场按马达类型、功率范围、冷却系统和车辆类型划分,全球预测(2026-2032年) 电动汽车马达市场规模、份额和成长分析(按类型、车辆类型、马达类型、额定功率、应用、动力传动系统类型、市场和地区划分)-2026-2033年产业预测

电动汽车马达市场规模、份额和成长分析(按类型、车辆类型、马达类型、额定功率、应用、动力传动系统类型、市场和地区划分)-2026-2033年产业预测 电动汽车马达市场预测至2032年:全球马达类型、电动车类型、应用、组件、额定功率、动力传动系统类型、销售管道和区域分析

电动汽车马达市场预测至2032年:全球马达类型、电动车类型、应用、组件、额定功率、动力传动系统类型、销售管道和区域分析 电动摩托车动力系统市场规模、占有率、成长及全球产业分析:依类型、应用和地区划分的洞察,以及2024-2032年预测电动车性能调校市场预测至2032年:按服务类型、车辆类型、组件、技术、应用、最终用户和地区分類的全球分析转子套筒市场(按材料、应用、最终用途行业和销售管道)——2025-2030 年全球预测

电动摩托车动力系统市场规模、占有率、成长及全球产业分析:依类型、应用和地区划分的洞察,以及2024-2032年预测电动车性能调校市场预测至2032年:按服务类型、车辆类型、组件、技术、应用、最终用户和地区分類的全球分析转子套筒市场(按材料、应用、最终用途行业和销售管道)——2025-2030 年全球预测