|

市场调查报告书

商品编码

1685736

汽车连接器:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)Automotive Connector - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

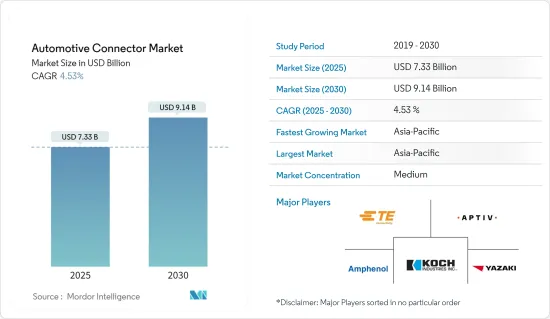

汽车连接器市场规模预计在 2025 年为 73.3 亿美元,预计到 2030 年将达到 91.4 亿美元,预测期内(2025-2030 年)的复合年增长率为 4.53%。

新冠肺炎疫情为市场带来了负面影响,一些汽车和零件製造厂暂时关闭,导致汽车销量略有下降。不过,随着一些国家逐步解除封锁,汽车需求也略有增加。因此,随着需求的增加,主要企业也正在扩大生产设施以提高产量。

从长远来看,预计市场将主要受技术进步和系统创新的推动。导航和资讯娱乐系统越来越受欢迎,并成为全球大多数汽车的标准配备。为了连接这些系统,需要一个用于电控系统的汽车连接器。

消费者对安全的担忧日益增加,加上政府机构采取的安全相关倡议,推动了各种车辆系统对可靠连接器的需求。例如,汽车使用的安全带、安全气囊和煞车等安全系统需要由固定器和安全约束系统连接器组成的连接系统。因此,汽车安全系统需求的不断增长直接影响汽车连接器的需求,从而推动市场成长。

预计预测期内亚太地区将占据市场的大部分份额。强劲的汽车行业、电动和混合动力汽车的兴起以及政府倡议预计将在预测期内支撑全部区域的需求。然而,由于市场对汽车连接器的需求不断增加,主要企业也在该地区进行投资。

例如,2021年9月,李尔公司(Lear)宣布与台湾汽车连接器产品製造商胡连联合股份有限公司签署合资最终协议。此举将立即扩展李尔公司的垂直整合能力,使其能够为全球汽车製造商提供的现有和未来的车辆架构设计和製造一系列连接系统产品。

汽车连接器市场趋势

资讯娱乐系统的进步

启用车辆的先进安全功能和对电动车(EV)的需求不断增加是推动市场成长的主要因素。此外,汽车感测器和资讯娱乐系统的日益复杂化正在推动全球对汽车线束和连接器的需求。塑胶光纤 (POF) 越来越多地取代汽车中的铜缆,以改善资料传输、提高设计灵活性并减轻车辆整体重量。 POF 需要汽车连接器才能正常运作。

除此之外,由于技术采用而导致的空调和 HVAC 系统的演变预计将对预测期内连接器的成长产生积极影响。市场的主要企业正在进行收购,以製造连接器并满足汽车的功能。

例如,2021年2月,JAE电子开发了MX79A汽车资讯娱乐连接器,用于车载导航系统、ADAS(高级驾驶辅助系统)、倒车相机和车上娱乐系统。此外,2021年6月,座椅和电子电气系统领域的全球汽车技术领导者李尔公司与总部位于德国洛芬根的科技公司IMS Connector Systems GmbH签署了共同开发契约,后者专门从事汽车应用的高速乙太网路解决方案。

此外,记忆体和资料储存连接器正在先进的汽车系统中用于支援自动驾驶汽车中的 Wi-Fi 网路。再加上混合动力汽车的日益普及,推动了市场的成长。此外,自我调整头灯、巡航控制、停车辅助、出发警报系统以及自动驾驶汽车中机器学习的融入等产品创新预计将在未来几年推动市场发展。

预计欧洲将在预测期内占据更大的市场占有率

欧洲在实施车辆安全功能方面处于领先地位,其次是美洲和亚太地区。该地区对汽车电气化的需求不断增长,以及政府旨在发展该国汽车工业的支持措施,预计将为预测期内汽车连接器的成长提供积极的前景。

此外,为了满足日益增长的消费者需求,製造商,尤其是电动车产业的製造商,正专注于开发创新解决方案。随着人们对车辆安全功能的认识不断提高,连接器製造商预计将专注于开发满足需求的功能。

例如,2021 年 9 月,TE Connectivity (TE) 收购了 ERNI Group AG (ERNI)。收购 ERNI 补充了 TE 广泛的连接产品系列,特别是用于工厂自动化、汽车、医疗和其他工业应用的高速和细间距连接器。此外,2021 年 1 月,浩亭技术集团扩展了其 IX Industrial® 微型资料连接器产品线,增加了用于资讯娱乐系统、乘客资讯系统和其他产品型号的新型电缆组件。此解决方案非常适合火车和公车资讯娱乐和乘客资讯系统。这款连接器比铁路应用中常用的同类圆形连接器小得多,而且轻得多。

由于汽车行业的进步,预计预测期内连接器在欧洲市场将显着增长。

汽车连接器产业概况

汽车连接器市场是一个适度整合的市场,主要参与者如 TE Connectivity Ltd、Yazaki Corporation、JST Mfg、Amphenol Corporation、Aptiv PLC 和 Sumitomo Wiring Systems Ltd 占据着相当大的市场份额。这些公司专注于在全球扩展其连接器业务,以抓住汽车先进电子和安全系统日益增长的趋势。

例如,2021年4月,TactoTek和Amphenol ICC宣布将合作开发与TactoTek IMSE技术相容的汽车级套模连接器。 Amphenol ICC 将把 TactoTek 的 IMSE 等变革性技术与 Amphenol ICC 的汽车级 MicroSpace 连接器平台和 Duflex 压接技术相结合,为客户提供新技术产品。

此外,京瓷于2021年3月推出了车内0.4mm间距8152系列电子连接器。符合高速传输标准MIPI D-PHY(2.5Gbps)、PCI Express Gen2(5Gbps)、Gen3(8Gbps)。该框架采用屏蔽设计,坚固耐用,可降低 EMI,适合要求严格的汽车应用。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 调查前提条件

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场动态

- 市场驱动因素

- 市场限制

- 产业吸引力-波特五力分析

- 新进入者的威胁

- 购买者/消费者的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争强度

第五章 市场区隔

- 应用

- 动力传动系统

- 舒适、便利、娱乐

- 安全与保障

- 车身线路和电力分配

- 导航和仪表

- 车辆类型

- 搭乘用车

- 商用车

- 地区

- 北美洲

- 美国

- 加拿大

- 北美其他地区

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 其他欧洲国家

- 亚太地区

- 中国

- 日本

- 印度

- 其他亚太地区

- 世界其他地区

- 巴西

- 阿根廷

- 南非

- 其他国家

- 北美洲

第六章 竞争格局

- 供应商市场占有率

- 公司简介

- TE Connectivity Ltd

- Yazaki Corporation

- JST Mfg Co. Ltd

- Molex Incorporated(Koch Industries Inc.)

- Amphenol Corporation

- Luxshare Precision Industry Co. Ltd

- Aptiv PLC

- Hirose Electric Co. Ltd

- Samtec

- Lumberg Holding

- Sumitomo Wiring Systems Ltd

第七章 市场机会与未来趋势

The Automotive Connector Market size is estimated at USD 7.33 billion in 2025, and is expected to reach USD 9.14 billion by 2030, at a CAGR of 4.53% during the forecast period (2025-2030).

The COVID-19 pandemic negatively impacted the market, as there was a slight decline in vehicle sales due to several vehicles and component manufacturing facilities shutting down temporarily. However, with the gradual removal of lockdowns in several countries, the demand for vehicles has slightly increased. Therefore with the increase in demand, key players are also increasing their manufacturing facilities to increase production.

Over the long term, the market is expected to be primarily driven by technological advancements and innovations in systems. Rising adoption of navigation and infotainment systems, among others, have become standard features in most cars across the world. To connect these systems, central electronic control unit automotive connectors are required.

The increase in safety concerns among consumers, coupled with safety-related initiatives from government agencies, has elevated the requirement for a reliable connector in various vehicle systems. For instance, safety systems like seatbelts, airbags, and brakes used in vehicles require a connection system comprising a retainer and safety restraint system connector. Thus, the increasing demand for automotive safety systems has a direct influence on the demand for automotive connectors, in turn driving the growth of the market.

Asia-Pacific is expected to hold a dominant share of the market during the forecast period. The strong automotive industry and rising electric and hybrid vehicles, coupled with government initiatives, are anticipated to support demand across the region during the forecast period. However, key players are also investing in the region due to the increase in the demand for automotive connectors in the market.

For instance, in September 2021, Lear Corporation (Lear) announced the signing of a definitive agreement for a joint venture with Hu Lane Associate Inc., a Taiwanese manufacturer of automotive connector products. It will immediately broaden Lear's vertical integration capabilities by engineering and manufacturing a portfolio of connection systems products for current and future vehicle architectures offered by global automakers.

Automotive Connector Market Trends

Increasing Advancement in Infotainment ystem

The increasing incorporation of advanced security features in automobiles, as well as the rising demand for electric vehicles (EVs), is the primary factor driving the market growth. Furthermore, the increasing sophistication of automotive sensors and infotainment systems has increased the global demand for automotive wiring harnesses and connectors. Plastic optical fiber (POF) is replacing copper cables in automobiles to improve data transmission and design flexibility while also reducing overall vehicle weight. POF requires automotive connectors to function properly.

In addition to this, the evolution of air conditioning systems and HVAC systems, owing to technological proliferation, is expected to favorably impact connectors' growth during the forecast period. Major players in the market are manufacturing the connectors and entering acquisitions to meet the features in the vehicles.

For instance, in February 2021, JAE Electronics developed MX79A Automotive Infotainment Connectors for use in automotive navigation systems, advanced driver assistance systems, backup cameras, and in-vehicle entertainment. Additionally, in June 2021, Lear Corporation, a global automotive technology leader in seating and e-systems, signed a joint development agreement with IMS Connector Systems GmbH, a technology company based in Loffingen, Germany, specializing in high-speed Ethernet solutions for automotive applications.

Furthermore, memory and data storage connectors are used in advanced automotive systems to support Wi-Fi networks in automated vehicles. This, combined with the increasing adoption of hybrid vehicles, is fueling market growth. Furthermore, product innovations such as adaptive front lighting, cruise control, park assistance, and departure warning systems, as well as the incorporation of machine learning in self-driving vehicles, are expected to propel the market in the coming years.

Europe is Expected to Capture a Larger Market Share During the Forecast Period

Europe leads the way in implementing vehicle safety features, with the Americas and Asia-Pacific following in its footsteps. Growing demand for vehicle electrification in the region, as well as supportive government measures aimed at the development of the country's automotive industry, are expected to create a positive outlook for the growth of automotive connectors during the forecast period.

Furthermore, active developments to meet growing consumer demand, particularly from manufacturers in the electric vehicle industry, are focusing on developing innovative solutions. With increased awareness of vehicle safety and security features, connector manufacturers are anticipated to focus on developing features to meet the demand.

For instance, in September 2021, TE Connectivity (TE) acquired ERNI Group AG (ERNI). The acquisition of ERNI complements TE's broad connectivity product portfolio, particularly in high-speed and fine-pitch connectors for factory automation, automotive, medical, and other industrial applications. Additionally, in January 2021, HARTING Technology Group expanded its IX Industrial(R) line of miniature data connector products with new cable assemblies intended for infotainment and passenger information systems and other product variants. This solution is ideal for infotainment and passenger information systems in trains and buses. The connector is significantly smaller and lighter than the comparable circular connectors commonly used in railway applications.

As a result of the advancement of the automotive industry, connectors are expected to grow significantly in the European market during the forecast period.

Automotive Connector Industry Overview

The automotive connector market is a moderately consolidated market due to the major players, like TE Connectivity Ltd, Yazaki Corporation, J.S.T. Mfg Co. Ltd, Amphenol Corporation, Aptiv PLC, and Sumitomo Wiring Systems Ltd, capturing significant shares in the market. These companies are focusing on expanding their connector business globally to capture the growing trend of advanced electronics and safety systems in vehicles.

For instance, in April 2021, TactoTek and Amphenol ICC announced that they were collaborating to develop automotive-grade in-mold connectors for TactoTek IMSE technology. Amphenol ICC will bring new technology products to customers with transformational technologies like TactoTek's IMSE combined with Amphenol ICC's automotive-grade MicroSpace connector platform and Duflex crimp technology.

Additionally, in March 2021, KYOCERA launched 0.4mm-Pitch 8152 series electronic connectors for automotive applications. It conforms to high-speed transmission standard MIPI D-PHY (2.5 Gbps), PCI Express Gen2 (5Gbps), and Gen3 (8Gbps). The frame is shielded for a robust design and EMI reduction suitable for demanding automotive applications.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.2 Market Restraints

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size in USD Million)

- 5.1 Application

- 5.1.1 Powertrain

- 5.1.2 Comfort, Convenience, and Entertainment

- 5.1.3 Safety and Security

- 5.1.4 Body Wiring and Power Distribution

- 5.1.5 Navigation and Instrumentation

- 5.2 Vehicle Type

- 5.2.1 Passenger Car

- 5.2.2 Commercial Vehicle

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Rest of Asia-Pacific

- 5.3.4 Rest of the World

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 South Africa

- 5.3.4.4 Other Countries

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 TE Connectivity Ltd

- 6.2.2 Yazaki Corporation

- 6.2.3 J.S.T. Mfg Co. Ltd

- 6.2.4 Molex Incorporated (Koch Industries Inc. )

- 6.2.5 Amphenol Corporation

- 6.2.6 Luxshare Precision Industry Co. Ltd

- 6.2.7 Aptiv PLC

- 6.2.8 Hirose Electric Co. Ltd

- 6.2.9 Samtec

- 6.2.10 Lumberg Holding

- 6.2.11 Sumitomo Wiring Systems Ltd

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

汽车连接器市场按产品类型、连接器类型、额定电流、安装类型、应用、车辆类型和最终用户划分 - 2025-2032 年全球预测

汽车连接器市场按产品类型、连接器类型、额定电流、安装类型、应用、车辆类型和最终用户划分 - 2025-2032 年全球预测 汽车和运输连接器市场规模、份额、成长分析(按类型、连接技术、应用、最终用途和地区)- 2025-2032 年产业预测

汽车和运输连接器市场规模、份额、成长分析(按类型、连接技术、应用、最终用途和地区)- 2025-2032 年产业预测 按车辆类型、连接类型、应用类型、地区、机会和预测对全球汽车连接器市场进行评估(2018 年至 2032 年)

按车辆类型、连接类型、应用类型、地区、机会和预测对全球汽车连接器市场进行评估(2018 年至 2032 年) 汽车连接器市场规模、份额和成长分析(按产品类型、车辆类型、应用、最终用户和地区)- 产业预测 2025-2032

汽车连接器市场规模、份额和成长分析(按产品类型、车辆类型、应用、最终用户和地区)- 产业预测 2025-2032 汽车连接器市场报告(按连接类型、连接器类型、系统类型、车辆类型、应用和地区)2025-2033

汽车连接器市场报告(按连接类型、连接器类型、系统类型、车辆类型、应用和地区)2025-2033 汽车和交通领域的无损检测:市场占有率分析、行业趋势和成长预测(2025-2030)

汽车和交通领域的无损检测:市场占有率分析、行业趋势和成长预测(2025-2030) 全球汽车和交通连接器市场,2025-2029

全球汽车和交通连接器市场,2025-2029 汽车连接器市场 - 全球产业规模、份额、趋势机会和预测,按连接类型、应用、车辆类型、地区和竞争细分,2019-2029 年

汽车连接器市场 - 全球产业规模、份额、趋势机会和预测,按连接类型、应用、车辆类型、地区和竞争细分,2019-2029 年 汽车连接器市场规模、份额、趋势分析报告:按产品、连接性别、车辆、应用、地区和细分市场预测,2024-2030

汽车连接器市场规模、份额、趋势分析报告:按产品、连接性别、车辆、应用、地区和细分市场预测,2024-2030 汽车连接器市场,按产品、按应用、按车辆类型、按国家和地区 - 2024-2032 年行业分析、市场规模、市场份额和预测

汽车连接器市场,按产品、按应用、按车辆类型、按国家和地区 - 2024-2032 年行业分析、市场规模、市场份额和预测