|

市场调查报告书

商品编码

1685878

欧洲液体肥料:市场占有率分析、行业趋势和成长预测(2025-2030 年)Europe Liquid Fertilizers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

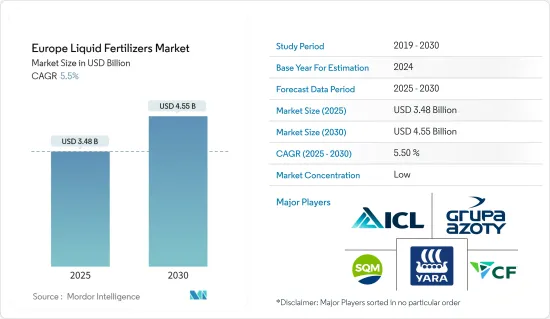

预计 2025 年欧洲液体肥料市场规模将达到 34.8 亿美元,预计到 2030 年将达到 45.5 亿美元,预测期内(2025-2030 年)的复合年增长率为 5.5%。

受高效和永续农业需求不断增长的推动,欧洲液体肥料市场正在稳步增长。液体肥料因其施用方便、养分吸收快等特点,已成为该地区农民的首选。提高作物产量、改善土壤肥力和满足不断增长的人口日益增长的粮食需求的需求进一步刺激了这些肥料的使用。根据联合国经济和社会事务部的数据,德国人口预计将从 2022 年的 8,410 万增长到 2023 年的 8,460 万,这将对液体肥料产生巨大的需求,以提高生产力并满足消费者的需求。另一个好处是,精密农业技术的进步促进了液体肥料的精准施用,减少了浪费并减轻了对环境的影响。

乌克兰、德国、法国和英国等国家凭藉其发达的农业部门和高度采用现代农业技术,主导欧洲液体肥料市场。例如,根据粮农组织统计资料库(FAOSTAT)的资料,2022年法国尿素硝酸铵肥料消费量将达190万吨,与前一年同期比较增加5.5%。对市场需求做出贡献的主要作物包括谷物、油籽、水果和蔬菜,这些作物都受益于液体肥料的营养效率。

此外,2022 年 11 月进行的一项研究表明,在俄罗斯,在马铃薯种植中施用液态氮尿素硝酸铵 (UAN) 可使马铃薯的产量提高 6.4%,产量提高 12.2%。 2023年,欧盟统计局报告称,小农户占欧洲地区所有农场的近70%,凸显了他们在欧洲农业格局中的关键作用。农场通常面积小于10公顷,对于培养农村创业精神和保护传统农业实践至关重要。这使得液体肥料成为这些农民提高产量最有效的选择。

永续性已成为欧洲农业领域的焦点,影响着液体肥料市场的成长。日益严格的环境法规和欧盟的绿色新政倡议正在鼓励使用环保肥料,以减少二氧化碳排放。目前,许多液体肥料的开发都考虑到了这些目标,结合生物基和有机成分来支持永续农业。这种转变不仅满足了监管要求,也响应了消费者对环保农业方法的需求。因此,由于对高效肥料的持续需求,即在增加产量的同时尽量减少对环境的有害影响,以及企业的积极参与和介入,预计这一领域在预测期内将逐步增长。

欧洲液体肥料市场趋势

精密农业和消费者需求日益重要

在欧洲,液体肥料市场正在经历重大变革,受到技术创新和精密农业技术等因素的影响。气候条件的变化、人口的增长以及由于可耕地减少而导致的对粮食安全的日益担忧是推动该地区采用精密农业的主要驱动力。液体肥料为现代农民带来了一系列好处,因为它们可以改善作物对养分供应的反应并提高生产力。

尿素硝酸铵 (UAN) 肥料是植物营养的液体宝库,是水溶液中尿素和硝酸铵的混合物,专门用于高效的植物营养管理。国际植物营养研究所强调,UAN 的氮效力通常为 28% 至 32%,使其成为该地区精密农业的重要液体肥料。此外,在欧洲尿素硝酸铵肥料市场,市场参与企业正在实施各种策略,包括策略伙伴关係,以保持市场竞争力。 2022年,总部位于大雅茅斯的液体肥料製造商Bryneflow与德国知名肥料製造商HELM AG组成了一家战略合资企业。透过此次合作,在特立尼达拥有液态氮(UAN)製造能力的HEML AG旨在提高对英国化肥供应的安全性。此次伙伴关係体现了该产业为加强其供应链和保持在欧洲市场的竞争力所做的努力。

此外,由于都市化,欧洲的可耕地面积正在逐渐减少。这种趋势迫使农民在不断缩小的土地上维持或提高作物产量,增加了他们对肥料的依赖,以优化生产力。根据联合国粮农组织统计资料库(FAOSTATS)的资料,欧洲谷物种植面积达1.167亿公顷,比前一年下降3.42%。由于都市化和工业化加剧了可耕地面积的减少,土耳其在维持粮食安全方面面临重大挑战。据土耳其农业和林业部称,为了缓解这些问题,土耳其的化肥使用量在 2023 年达到了历史最高水平,全国施用了近 1400 万吨化肥。这项增产是应对可用耕地减少和确保充足粮食生产的更广泛努力的一部分。

农产品进口量的增加表明该地区的需求不断增长,而产量却出现短缺。例如,根据 ITC 贸易地图,德国的小麦进口量将从 2022 年的 410 万吨增加到 2023 年的 513 万吨。预计在预测期内,耕地面积减少、进口量增加、精密农业的采用率不断提高以及提高农业生产率的需求将推动液体肥料市场的发展。

俄罗斯主导欧洲液体肥料市场

俄罗斯凭藉其强大的农业基础和大规模的肥料生产,在欧洲液体肥料市场中发挥关键作用。该国是氮基液体肥料的主要生产国,包括尿素硝酸铵(UAN)溶液,这些肥料对欧洲农业生产力至关重要。例如,根据俄罗斯主要肥料製造商PhosAgro的资料,该国每年生产6,000万吨肥料,其中2023年PhosAgro将贡献1,100万吨。

此外,俄罗斯 Life Force LLC 还提供液体肥料 Life Force Acti Grow Fe/B/Zn/Mn,其特点是植物活性成分的创新组合。随着俄罗斯农业用地面积因都市化和环保努力而不断缩小,液体肥料的作用变得越来越重要。例如,2022年俄罗斯水稻收穫面积为16.96万公顷,较上年下降8.94%。透过使用能够精确施肥的液体肥料,俄罗斯的目标是在有限的土地面积上提高作物产量。

俄罗斯的农产品出口能力,尤其是化肥出口能力,使其能够满足国内和欧洲的需求。随着欧洲农民寻求在日益缩小的土地上提高作物产量,俄罗斯的出口导向策略使该国成为区域和全球肥料市场的关键参与者。例如,根据ITC贸易地图,2023年俄罗斯尿素和硝酸铵液体混合物出口量为2,025,979吨,占全球出口额的30.9%。据俄罗斯联邦统计局称,欧盟最大的俄罗斯化肥买家是波兰、法国和德国。波兰的进口量比与前一年同期比较增加了2.7倍,而法国的进口量在2023年增加了18%。

然而,与其他国家的持续衝突扰乱了国内和国际供应链,导致化肥供应出现不确定性。儘管面临这些挑战,俄罗斯仍然处于欧洲液体肥料市场的前沿,并以创新和永续性为重点,在满足欧洲日益增长的农业需求方面发挥关键作用。

欧洲液体肥料产业概况

欧洲液体肥料市场分散,领先公司之间的竞争日益激烈,以维持稳定的基本客群并占领相当大的市场占有率。市场上一些最热门的公司包括 Yara International ASA、ICL Group Ltd.、Grupa Azoty SA、CF Industries Holdings, Inc. 和 Sociedad Quimica y Minera de Chile SA (SQM)。每家公司都专注于扩大其设施和开发新产品,以加强其产品组合併在欧洲液体肥料市场确立战略地位。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场动态

- 市场概览

- 市场驱动因素

- 精密农业的重要性日益增加

- 耕地面积减少

- 扩大政府支持和倡议

- 市场限制

- 有机农业的普及率不断提高

- 高成本

- 波特五力分析

- 供应商的议价能力

- 买家的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争强度

第五章市场区隔

- 复合型

- 直的

- 微量营养素

- 氮

- 磷酸盐

- 钾

- 次要微量营养素

- 申请方式

- 受精

- 叶面喷布

- 类型

- 田间作物

- 园艺作物

- 草坪和观赏作物

- 地区

- 法国

- 德国

- 义大利

- 荷兰

- 俄罗斯

- 西班牙

- 英国

- 乌克兰

- 其他欧洲国家

第六章 竞争格局

- 最受欢迎的策略

- 市场占有率分析

- 公司简介

- Yara International ASA

- ICL Group Ltd

- Grupa Azoty SA

- BMS Micro-nutrients NV

- CF Industries Holdings, Inc.

- Nordfert

- YILDIRIM Group

- Sociedad Quimica y Minera de Chile SA(SQM)

第七章 市场机会与未来趋势

The Europe Liquid Fertilizers Market size is estimated at USD 3.48 billion in 2025, and is expected to reach USD 4.55 billion by 2030, at a CAGR of 5.5% during the forecast period (2025-2030).

The European liquid fertilizer market has experienced steady growth, propelled by the increasing demand for efficient and sustainable agricultural practices. Liquid fertilizers, valued for their ease of application and rapid nutrient absorption, are becoming a preferred choice for farmers in the region. The need to enhance crop yields, improve soil fertility, and meet the rising food demand of the growing population has further accelerated the adoption of these fertilizers. According to the United Nations, Department of Economic and Social Affairs, Germany's population increased to 84.6 million in 2023 from 84.1 million in 2022, creating a significant need for liquid fertilizers to boost productivity and satisfy consumer demand. Additionally, the market benefits from technological advancements in precision agriculture, which promote the precise application of liquid fertilizers, reducing wastage and environmental impact.

Countries such as Ukraine, Germany, France, and the United Kingdom dominate the European liquid fertilizer market due to their advanced agricultural sectors and higher adoption rates of modern farming techniques. For instance, according to FAOSTAT data, France's urea ammonium nitrate fertilizer consumption reached 1.9 million metric tons in 2022, an increase of 5.5% from the previous year. Key crops contributing to the market demand include cereals, oilseeds, fruits, and vegetables, all of which benefit from the nutrient efficiency offered by liquid fertilizers.

Furthermore, a research study conducted in November 2022 demonstrated that the application of Urea Ammonium Nitrate (UAN), a liquid nitrogenous fertilizer in potato cultivation resulted in a 6.4% increase in marketable potato yield and up to a 12.2% increase in total yield in Russia. In 2023, Eurostat reported that small-scale farmers constituted nearly 70% of all farms in the European region, underscoring their pivotal role in Europe's agricultural landscape. Typically spanning under 10 hectares, these farms are essential for fostering rural entrepreneurship and upholding traditional farming practices. Hence, liquid fertilizer is the most effective option for better yield for these farmers.

Sustainability has become a central focus in the European agricultural sector, influencing the growth of the liquid fertilizer market. Stricter environmental regulations and the European Union's Green Deal initiatives encourage the use of environmentally friendly fertilizers with reduced carbon footprints. Many liquid fertilizers are now developed to align with these goals, incorporating bio-based or organic ingredients to support sustainable farming. This shift not only meets regulatory requirements but also addresses consumer demand for eco-friendly farming practices. Therefore, due to the continued demand for high-efficiency fertilizers to boost production while minimizing harmful impacts on the environment, coupled with the active participation and involvement of players, the segment is anticipated to grow gradually during the forecast period.

Europe Liquid Fertilizer Market Trends

Rising Importance of Precision Farming and Consumer Demand

In Europe, the liquid fertilizers market is evolving significantly, influenced by factors such as technological innovations, and precision agriculture techniques. Rising food security concerns due to changing climatic conditions, increasing population, and decreasing arable land availability are the primary factors bolstering the adoption of precision farming practices in the region. This, in turn, drives the market for liquid fertilizers as they provide an array of benefits to modern farmers that lead to improved crop response to the availability of nutrients and better productivity.

Urea ammonium nitrate (UAN) fertilizer, a liquid powerhouse of plant nutrition, blends urea and ammonium nitrate in an aqueous solution used precisely for efficient plant nutrient management. The International Plant Nutrition Institute highlights its nitrogen potency, typically ranging from 28% to 32%, hence it is an important liquid fertilizer used in precision farming in the region. Moreover, the European urea ammonium nitrate fertilizer market has witnessed the implementation of various strategies by industry participants, including strategic partnerships, to maintain market competitiveness. In 2022, Brineflow, a liquid fertilizer manufacturer headquartered in Great Yarmouth, established a strategic joint venture with HELM AG, a prominent German fertilizer producer. HEML AG, which possesses substantial liquid nitrogen (UAN) manufacturing capabilities in Trinidad, aims to enhance the security of fertilizer supply for the United Kingdom through this collaborative arrangement. This partnership exemplifies the industry's efforts to strengthen supply chains and maintain a competitive edge in the European market.

Furthermore, Europe has experienced a gradual reduction in arable land due to urbanization. This trend compels farmers to maintain or increase crop yields from a diminishing area, thereby increasing their reliance on fertilizers to optimize productivity. According to FAOSTATS data, the harvested area of cereal grains in Europe has reached 116.7 million hectares, a reduction of 3.42% from the previous year. Turkey has faced significant challenges in maintaining food security due to a decrease in arable land, exacerbated by urbanization, and industrialization. To mitigate these issues, in 2023, Turkey recorded the highest usage of chemical fertilizers in its history, with nearly 14 million metric tons applied across the country, according to the Ministry of Agriculture and Forestry, Turkey. This increase is part of a broader effort to counteract the decline in available agricultural land and ensure sufficient food production.

The growing import of agricultural produce further shows the growing demand and insufficient production in the region. For instance, according to the ITC Trade Map, in Germany, the import of wheat in 2023 reached 5.13 million metric tons which was 4.10 million metric tons in 2022. The reduction in arable land, increasing import, and growing adoption of precision agriculture, coupled with the need for increased agricultural productivity, is anticipated to drive the liquid fertilizer market in the forecast period.

Russia Dominates the European Liquid Fertilizers Market

Russia plays a critical role in the European liquid fertilizer market, driven by its strong agricultural base and extensive production of fertilizers. The country is a major producer of nitrogen-based liquid fertilizers, including urea ammonium nitrate (UAN) solutions, which are essential for European agricultural productivity. For instance, according to the data of PhosAgro, a leading fertilizer producer in Russia, the country has produced 60 million metric tons of fertilizers, with PhosAgro contributing 11 million metric tons in 2023.

Additionally, another Russian company Life Force LLC offers Life Force Acti Grow Fe/B/Zn/Mn, a liquid fertilizer featuring an innovative formula of active phytocomponents. As agricultural land in Russia continues to decrease due to urbanization and environmental initiatives, liquid fertilizers' role becomes even more significant. For instance, in 2022 the harvested area for rice was 169.6 thousand hectares in Russia with a reduction of 8.94% compared to the previous year. Using liquid fertilizer, that enables precise nutrient application, the country is aiming to boost crop yields on limited land.

Russia's agricultural export capacity, particularly in fertilizers, allows it to cater to both domestic and European needs. As European farmers seek to improve their crop yields with shrinking land, Russia's export-oriented strategy positions the country as a critical player in the regional and global fertilizer market. For instance, the export quantity of the liquid mixture of urea and ammonium nitrate in 2023 from Russia was 2,025,979 metric tons which was 30.9% value share worldwide according to the ITC trade map. According to Rosstat, the largest buyers of Russian fertilizers in the EU were Poland, France, and Germany. Poland increased its imports 2.7-fold year-on-year, and France increased its imports by 18% in 2023.

However, the ongoing conflict with other nations has disrupted both domestic and international supply chains, creating uncertainty in the availability of fertilizers. Despite these challenges, Russia continues to remain at the forefront of the European liquid fertilizer market, focusing on innovation and sustainability to maintain its critical role in feeding Europe's growing agricultural demands.

Europe Liquid Fertilizer Industry Overview

The European liquid fertilizer market is fragmented, intensifying competition among major players to maintain a stable customer base and capture significant market shares. Some of the most notable companies in the market are Yara International ASA, ICL Group Ltd., Grupa Azoty S.A., CF Industries Holdings, Inc., and Sociedad Quimica y Minera de Chile SA (SQM) among others. The companies have focused on facility expansions and developing new products to enhance their portfolio and strategize their hold in the European liquid fertilizer market.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Importance of Precision Farming

- 4.2.2 Decreasing Arable Land

- 4.2.3 Growing Government Support and Initiative

- 4.3 Market Restraints

- 4.3.1 Increase in Adoption of Oragnic Farming

- 4.3.2 Comparative High Cost

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Complex

- 5.2 Straight

- 5.2.1 Micronutrients

- 5.2.2 Nitrogenous

- 5.2.3 Phosphatic

- 5.2.4 Potassic

- 5.2.5 Secondary Macronutrients

- 5.3 Mode of Application

- 5.3.1 Fertigation

- 5.3.2 Foliar Application

- 5.4 Cop Type

- 5.4.1 Field Crops

- 5.4.2 Horticultural Crops

- 5.4.3 Turf and Ornamental Crops

- 5.5 Geography

- 5.5.1 France

- 5.5.2 Germany

- 5.5.3 Italy

- 5.5.4 Netherlands

- 5.5.5 Russia

- 5.5.6 Spain

- 5.5.7 United Kingdom

- 5.5.8 Ukraine

- 5.5.9 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Most Adopted Strategies

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 Yara International ASA

- 6.3.2 ICL Group Ltd

- 6.3.3 Grupa Azoty S.A.

- 6.3.4 BMS Micro-nutrients NV

- 6.3.5 CF Industries Holdings, Inc.

- 6.3.6 Nordfert

- 6.3.7 YILDIRIM Group

- 6.3.8 Sociedad Quimica y Minera de Chile SA (SQM)

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

液态肥料市场:2026-2032年全球市场预测(依产品类型、作物、生产流程、应用及通路划分)

液态肥料市场:2026-2032年全球市场预测(依产品类型、作物、生产流程、应用及通路划分) 液体肥料市场规模、份额、成长及全球产业分析:按类型、应用和地区分類的洞察,2026-2034 年预测

液体肥料市场规模、份额、成长及全球产业分析:按类型、应用和地区分類的洞察,2026-2034 年预测 全球液体肥料市场报告(2026 年)按作物类型、包装规格、应用、最终用途和销售管道的多元素水溶性液体肥料市场—2026-2032年全球预测

全球液体肥料市场报告(2026 年)按作物类型、包装规格、应用、最终用途和销售管道的多元素水溶性液体肥料市场—2026-2032年全球预测 液态肥料市场规模、份额及成长分析(依作物类型、化合物、应用、类型及地区划分)-2026-2033年产业预测液体肥料市场-2025-2030年预测

液态肥料市场规模、份额及成长分析(依作物类型、化合物、应用、类型及地区划分)-2026-2033年产业预测液体肥料市场-2025-2030年预测 液体肥料市场-全球产业规模、份额、趋势、机会和预测,按类型、应用方式、成分类型、作物类型、地区和竞争情况划分,2020-2030 年

液体肥料市场-全球产业规模、份额、趋势、机会和预测,按类型、应用方式、成分类型、作物类型、地区和竞争情况划分,2020-2030 年 液体肥料市场机会、成长动力、产业趋势分析及2025-2034年预测

液体肥料市场机会、成长动力、产业趋势分析及2025-2034年预测 2025-2033年液体肥料市场报告(按类型、生产流程、作物、施用方式和地区)

2025-2033年液体肥料市场报告(按类型、生产流程、作物、施用方式和地区) 北美液体肥料:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)

北美液体肥料:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)