|

市场调查报告书

商品编码

1685909

生物刺激素:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Biostimulants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

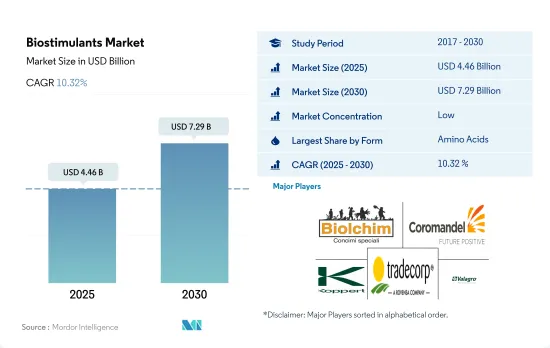

生物刺激素市场规模预计在 2025 年为 44.6 亿美元,预计到 2030 年将达到 72.9 亿美元,预测期内(2025-2030 年)的复合年增长率为 10.32%。

- 近年来,随着农民越来越意识到生物刺激素产品对作物生长和产量的益处,生物刺激素在农业中的应用也日益增加。生物刺激素是促进植物生长并改善营养吸收、抗逆性和整体健康的天然或合成物质。

- 胺基酸成为全球消费量最大的生物刺激素,2022 年的市场占有率为 32.0%。这一高份额主要归因于喷洒氨基酸对作物产生的正面影响,例如增加了欧洲国家冬小麦作物的种子产量和每穗粒数。生物刺激素在连续作物中的消费量最高,占2022年74.6%的市场占有率,其次是园艺作物和经济作物。

- 生物刺激素领域将以欧洲为主导,2022 年的市场占有率为 40.6%,其次是北美和亚太地区。这一高比例得益于该地区农民的意识很高,以及政府对有机农业的推广,目标是到2030年使25.0%的农地实现有机化。

- 受有机产品需求不断增长和有机作物面积增加的推动,生物刺激素领域预计在 2023 年至 2029 年期间的复合年增长率为 10.1%。

- 生物刺激素在农业领域越来越受欢迎,可以减少化学肥料和农药的使用。健康成长的有机食品产业也是生物刺激素市场成长的主要动力。

- 欧洲是全球最大的生物刺激素市场,2022年价值为13亿美元,占市场金额的40.6%。欧盟委员会已为成员国设定了将25%的农业用地转变为有机农业的目标,这强化了欧洲生物经济智慧成长与创新的关键优先事项。生物刺激素是实现此目的的重要成分。德国透过投资研发来提高生物刺激素的有效性,在实现这些目标方面发挥主导作用。

- 北美是全球生物刺激素市场的第二大市场,2022 年市场规模为 8.402 亿美元。该地区的国家正在推出增加有机农业的政策,包括美国农业部的有机转型计划,到 2022 年将投资 3 亿美国。该倡议旨在鼓励农民之间的指导,包括向农民提供财政支持并提高人们对生物刺激素有益影响的认识。

- 亚太地区在生物刺激素市场上占据第三大地位,其中中国是世界上最大的肥料消费国,已经在作物生产中使用有机投入品。同样,由于生产商的认识不断提高,南美和非洲的生物刺激素市场也出现了波动。预计化学投入品使用的减少和全球有机种植面积的增加将推动生物刺激素市场在预测期内以 10.1% 的复合年增长率成长。

全球生物刺激素市场趋势

意识的增强和政府的倡议正在推动北美和欧洲的有机生产。

- 有机农业已成为永续粮食系统的主要贡献者,并已在全球 187 个国家实践。截至2021年,全球有机农地面积为7,230万公顷,2018年至2021年各地区平均成长2.9%。其中,2021年有机种植面积为1,440万公顷,占有机农地总面积的19.9%。有机农业最强劲的市场是北美和欧洲,占2022年世界有机耕地面积的41.0%。 2022年,欧洲的有机耕地面积将为650万公顷,占有机耕地总面积的44.1%。北美和欧洲最重要的有机作物包括苹果、草莓、谷物和橄榄。

- 亚太地区的新兴国家也正在加入有机农业运动,并在生产和供应新鲜有机农产品方面实现自给自足,以满足国内需求。亚太地区有机农业呈现成长趋势,2017年至2022年有机耕地面积将成长18.8%。该地区政府的主要措施也在促进有机农业发展方面发挥关键作用。例如,日本的2021年基本农业管理计画旨在2030年将有机农民的数量和有机耕地面积增加两倍。

- 有机农业在世界各地越来越受欢迎,许多国家都采用有机农业来实现永续的粮食体系。有机农业的成长源于人们对其益处的认识不断提高,例如促进土壤健康、减少环境影响和生产更健康的食品。

人均有机食品支出的成长主要出现在美国和德国,这是由消费者对更健康、更永续食品的需求所推动的。

- 过去十年,有机食品市场经历了显着成长,全球销售额预计将从 2012 年的 708 亿美元成长到 2020 年的 1,206 亿美元。有机食品的流行趋势受到多种因素的推动,包括消费者对更健康、更永续的食品选择的需求不断增长,以及对传统农业对环境影响的认识不断提高。

- 根据有机贸易协会的调查,2021年有机蔬果销量年增约4.5%,占有机产品总销售量的15%。目前,北美在有机产品平均支出方面占据市场主导地位,2021年美国的人均支出达到186.7美元,是北美国家中最高的。欧洲有机市场预计也将强劲成长,其中德国 2019 年人均有机消费最高,达到 75.6 美元。

- 有机食品市场仍由可支配收入较高的已开发国家主导,但预计在新兴国家也将成长。例如,在亚太地区,不断壮大的工人阶级可能会促进市场扩张。随着有机产品越来越普及,它们的价格也越来越便宜。

- 有机食品市场在全球范围内经历了显着的增长,预计在预测期内仍将持续增长。

生物刺激素产业概况

生物刺激素市场较为分散,前五大公司市占率合计为11.95%。市场的主要企业是:Biolchim SpA、Coromandel International Ltd、Koppert Biological Systems Inc.、Trade Corporation International 和 Valagro(按字母顺序排列)。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章执行摘要和主要发现

第二章 报告要约

第 3 章 简介

- 研究假设和市场定义

- 研究范围

- 调查方法

第四章 产业主要趋势

- 有机栽培面积

- 有机产品人均支出

- 法律规范

- 阿根廷

- 澳洲

- 巴西

- 加拿大

- 中国

- 埃及

- 法国

- 德国

- 印度

- 印尼

- 义大利

- 日本

- 墨西哥

- 荷兰

- 奈及利亚

- 菲律宾

- 俄罗斯

- 南非

- 西班牙

- 泰国

- 土耳其

- 英国

- 美国

- 越南

- 价值链与通路分析

第五章 市场区隔

- 形式

- 胺基酸

- 富里酸

- 腐植酸

- 蛋白质水解物

- 海藻萃取物

- 其他生物刺激素

- 作物类型

- 经济作物

- 园艺作物

- 田间作物

- 地区

- 非洲

- 按国家

- 埃及

- 奈及利亚

- 南非

- 非洲其他地区

- 亚太地区

- 按国家

- 澳洲

- 中国

- 印度

- 印尼

- 日本

- 菲律宾

- 泰国

- 越南

- 其他亚太地区

- 欧洲

- 按国家

- 法国

- 德国

- 义大利

- 荷兰

- 俄罗斯

- 西班牙

- 土耳其

- 英国

- 其他欧洲国家

- 中东

- 按国家

- 伊朗

- 沙乌地阿拉伯

- 其他中东地区

- 北美洲

- 按国家

- 加拿大

- 墨西哥

- 美国

- 北美其他地区

- 南美洲

- 按国家

- 阿根廷

- 巴西

- 南美洲其他地区

- 非洲

第六章 竞争格局

- 主要策略趋势

- 市场占有率分析

- 业务状况

- 公司简介.

- Agriculture Solutions Inc.

- Agrinos

- Atlantica Agricola

- Biolchim SpA

- Bionema

- Coromandel International Ltd

- Haifa Group

- Koppert Biological Systems Inc.

- Plant Response Biotech Inc.

- Sigma Agriscience LLC

- T Stanes and Company Limited

- Trade Corporation International

- UPL

- Valagro

- Vittia Group

第七章:执行长的关键策略问题

第 8 章 附录

- 世界概况

- 概述

- 五力分析框架

- 全球价值链分析

- 市场动态(DRO)

- 资讯来源和进一步阅读

- 图片列表

- 关键见解

- 资料包

- 词彙表

简介目录

Product Code: 49202

The Biostimulants Market size is estimated at 4.46 billion USD in 2025, and is expected to reach 7.29 billion USD by 2030, growing at a CAGR of 10.32% during the forecast period (2025-2030).

- The use of biostimulants in agriculture has gained momentum in recent years, with increasing awareness among farmers about the benefits of these products on crop growth and yield. Biostimulants are natural or synthetic substances that enhance plant growth and improve nutrient uptake, stress tolerance, and overall health.

- Amino acids emerged as the most consumed biostimulants globally, with a market share of 32.0% in 2022. This high share was primarily due to the positive effects of amino acids on crops when applied, such as increasing seed yield and grain numbers per ear in winter wheat crops in European countries. The consumption of biostimulants was the highest in row crops, which accounted for 74.6% of the market share in 2022, followed by horticultural crops and cash crops.

- Europe dominated the biostimulants segment, with a market share of 40.6% in 2022, followed by North America and Asia-Pacific. This high share was due to the high awareness among farmers in the region and the government's promotion of organic agriculture, with a target of 25.0% of agricultural land to be organic by 2030.

- The biostimulants segment is expected to record a CAGR of 10.1% between 2023 and 2029, driven by the increasing demand for organic products and the growing area under the cultivation of organic crops.

- Biostimulants have gained popularity in the agricultural industry to reduce the use of chemical fertilizers and pesticides. The organic food industry, which is growing at a healthy rate, is another major driving force behind the growth of the biostimulant market.

- Europe is the largest market for global biostimulants, accounting for 40.6% of the market value, valued at USD 1.3 billion, in 2022. The European Commission has set a target for member countries to bring 25% of their respective agricultural land under organic farming, reinforcing Europe's key priorities for smart growth and innovation for the bio-based economy. Biostimulants represent a critical ingredient for the same. Germany plays a lead role in achieving these objectives by investing in R&D to enhance the effectiveness of biostimulants.

- North America is the second-largest market for global biostimulants, with a market value of USD 840.2 million in 2022. Countries in the region are introducing policies to increase organic farming, such as the USDA's Organic Transition Initiative in the United States, with an investment of USD 300 million in 2022. This initiative aims to provide financial assistance to farmers and encourage farmer-to-farmer mentoring, including creating awareness of the beneficial impacts of biostimulants.

- The Asia-Pacific region holds the third-largest position in the biostimulants market, with China, the world's largest fertilizer consumer, already using organic inputs for crop production. Similarly, South America and Africa have also witnessed a flux in the biostimulants market due to increased awareness among growers. The reduced usage of chemical inputs and increasing global organic area are projected to drive the biostimulants market at a CAGR of 10.1% during the forecast period.

Global Biostimulants Market Trends

The increasing awareness and Government initiatives is driving the organic production in North America and Europe.

- Organic agriculture has emerged as a significant contributor to sustainable food systems, with 187 countries practicing it globally. As of 2021, there are 72.3 million hectares of organic agricultural land globally, with an average increase of 2.9% across all regions from 2018 to 2021. Among these, organic arable land accounted for 14.4 million hectares in 2021, representing 19.9% of the total organic agricultural land. The strongest markets for organic farming are in North America and Europe, accounting for 41.0% of the global organic arable land in 2022. The total organic arable land in Europe was 6.5 million hectares in 2022, equivalent to 44.1% of the overall organic arable agricultural area. The most significant crops grown organically in North America and Europe are apples, strawberries, cereals, and olives, among others.

- Developing countries in the Asia-Pacific region are also joining the organic agriculture movement and becoming self-sufficient in producing and providing fresh organic produce to meet domestic demand. The Asia-Pacific region observed an increasing trend in organic farming, with an 18.8% increase in organic arable land from 2017 to 2022. The major initiatives by governments in the region have also played a vital role in boosting organic farming. For example, Japan's Basic Plan for Agriculture and Management in 2021 aims to triple the number of organic farmers and organic lands by 2030.

- Organic agriculture is becoming increasingly popular globally, with various countries adopting it to achieve sustainable food systems. The growth in organic agriculture is driven by the increasing awareness about the benefits of organic farming, such as promoting soil health, reducing environmental impacts, and producing healthier food.

Per capita spending of organic food majorly observed in United States and Germany, attributed to the consumer demand for healthier and sustainable food

- The organic food market has experienced significant growth over the past decade, with global sales reaching USD 120.6 billion in 2020, up from USD 70.8 billion in 2012. The trend toward organic food is driven by several factors, including increasing consumer demand for healthier, more sustainable food options and growing awareness about the environmental impact of conventional agriculture.

- According to a survey conducted by the Organic Trade Association, in 2021, sales of organic fruits and vegetables increased by around 4.5% that year, accounting for 15% of the overall organic sales. North America currently dominates the market in terms of average spending on organic products, with per capita spending in the United States reaching USD 186.7 in 2021, the highest among North American countries. Europe is also expected to experience significant growth in the organic market, with Germany accounting for the highest per capita spending of USD 75.6 during the same year.

- While the organic food market is still dominated by developed countries with high levels of disposable income, it is also expected to grow in developing nations. For example, in the Asia-Pacific region, the increase in the number of working-class people is likely to contribute to market expansion. As the availability of organic products increases, prices become more affordable.

- The organic food market is experiencing significant growth globally and is expected to continue during the forecast period.

Biostimulants Industry Overview

The Biostimulants Market is fragmented, with the top five companies occupying 11.95%. The major players in this market are Biolchim SpA, Coromandel International Ltd, Koppert Biological Systems Inc., Trade Corporation International and Valagro (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Area Under Organic Cultivation

- 4.2 Per Capita Spending On Organic Products

- 4.3 Regulatory Framework

- 4.3.1 Argentina

- 4.3.2 Australia

- 4.3.3 Brazil

- 4.3.4 Canada

- 4.3.5 China

- 4.3.6 Egypt

- 4.3.7 France

- 4.3.8 Germany

- 4.3.9 India

- 4.3.10 Indonesia

- 4.3.11 Italy

- 4.3.12 Japan

- 4.3.13 Mexico

- 4.3.14 Netherlands

- 4.3.15 Nigeria

- 4.3.16 Philippines

- 4.3.17 Russia

- 4.3.18 South Africa

- 4.3.19 Spain

- 4.3.20 Thailand

- 4.3.21 Turkey

- 4.3.22 United Kingdom

- 4.3.23 United States

- 4.3.24 Vietnam

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Form

- 5.1.1 Amino Acids

- 5.1.2 Fulvic Acid

- 5.1.3 Humic Acid

- 5.1.4 Protein Hydrolysates

- 5.1.5 Seaweed Extracts

- 5.1.6 Other Biostimulants

- 5.2 Crop Type

- 5.2.1 Cash Crops

- 5.2.2 Horticultural Crops

- 5.2.3 Row Crops

- 5.3 Region

- 5.3.1 Africa

- 5.3.1.1 By Country

- 5.3.1.1.1 Egypt

- 5.3.1.1.2 Nigeria

- 5.3.1.1.3 South Africa

- 5.3.1.1.4 Rest of Africa

- 5.3.2 Asia-Pacific

- 5.3.2.1 By Country

- 5.3.2.1.1 Australia

- 5.3.2.1.2 China

- 5.3.2.1.3 India

- 5.3.2.1.4 Indonesia

- 5.3.2.1.5 Japan

- 5.3.2.1.6 Philippines

- 5.3.2.1.7 Thailand

- 5.3.2.1.8 Vietnam

- 5.3.2.1.9 Rest of Asia-Pacific

- 5.3.3 Europe

- 5.3.3.1 By Country

- 5.3.3.1.1 France

- 5.3.3.1.2 Germany

- 5.3.3.1.3 Italy

- 5.3.3.1.4 Netherlands

- 5.3.3.1.5 Russia

- 5.3.3.1.6 Spain

- 5.3.3.1.7 Turkey

- 5.3.3.1.8 United Kingdom

- 5.3.3.1.9 Rest of Europe

- 5.3.4 Middle East

- 5.3.4.1 By Country

- 5.3.4.1.1 Iran

- 5.3.4.1.2 Saudi Arabia

- 5.3.4.1.3 Rest of Middle East

- 5.3.5 North America

- 5.3.5.1 By Country

- 5.3.5.1.1 Canada

- 5.3.5.1.2 Mexico

- 5.3.5.1.3 United States

- 5.3.5.1.4 Rest of North America

- 5.3.6 South America

- 5.3.6.1 By Country

- 5.3.6.1.1 Argentina

- 5.3.6.1.2 Brazil

- 5.3.6.1.3 Rest of South America

- 5.3.1 Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Agriculture Solutions Inc.

- 6.4.2 Agrinos

- 6.4.3 Atlantica Agricola

- 6.4.4 Biolchim SpA

- 6.4.5 Bionema

- 6.4.6 Coromandel International Ltd

- 6.4.7 Haifa Group

- 6.4.8 Koppert Biological Systems Inc.

- 6.4.9 Plant Response Biotech Inc.

- 6.4.10 Sigma Agriscience LLC

- 6.4.11 T Stanes and Company Limited

- 6.4.12 Trade Corporation International

- 6.4.13 UPL

- 6.4.14 Valagro

- 6.4.15 Vittia Group

7 KEY STRATEGIC QUESTIONS FOR AGRICULTURAL BIOLOGICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

02-2729-4219

+886-2-2729-4219

全球植物健康诱导剂市场:预测至2032年-按诱导剂类型、製剂、作用机制、作物类型、应用方法、最终用户、通路和地区进行分析

全球植物健康诱导剂市场:预测至2032年-按诱导剂类型、製剂、作用机制、作物类型、应用方法、最终用户、通路和地区进行分析 生物刺激剂市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)2032年农业生物刺激素市场预测:按活性成分、作物类型、施用方法、配方和地区进行的全球分析

生物刺激剂市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)2032年农业生物刺激素市场预测:按活性成分、作物类型、施用方法、配方和地区进行的全球分析 海洋生物刺激素市场-全球产业规模、份额、趋势、机会和预测,按成分、应用模式、最终用途、地区和竞争细分,2020-2030 年预测

海洋生物刺激素市场-全球产业规模、份额、趋势、机会和预测,按成分、应用模式、最终用途、地区和竞争细分,2020-2030 年预测 生物刺激素市场(按形态、来源、使用方法和作物类型)—2025-2032 年全球预测生物刺激素市场-全球产业规模、份额、趋势、机会及预测(按活性成分、作物类型、应用、地区和竞争情况细分,2020-2030 年)

生物刺激素市场(按形态、来源、使用方法和作物类型)—2025-2032 年全球预测生物刺激素市场-全球产业规模、份额、趋势、机会及预测(按活性成分、作物类型、应用、地区和竞争情况细分,2020-2030 年) 腐植酸基生物刺激素市场,依产品类型、形式、应用、作物类型、国家划分 - 2025 年至 2032 年全球产业分析、市场规模、市场份额及预测

腐植酸基生物刺激素市场,依产品类型、形式、应用、作物类型、国家划分 - 2025 年至 2032 年全球产业分析、市场规模、市场份额及预测 2025年生物刺激素全球市场报告胺基酸类生物刺激素市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

2025年生物刺激素全球市场报告胺基酸类生物刺激素市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测 生物刺激素市场规模及预测(2021-2031 年)、全球及各地区份额、趋势及成长机会分析报告涵盖范围:依产品类型、应用方式、作物类型及地理划分

生物刺激素市场规模及预测(2021-2031 年)、全球及各地区份额、趋势及成长机会分析报告涵盖范围:依产品类型、应用方式、作物类型及地理划分

▼