|

市场调查报告书

商品编码

1685937

欧洲农业机械:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Europe Agricultural Machinery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

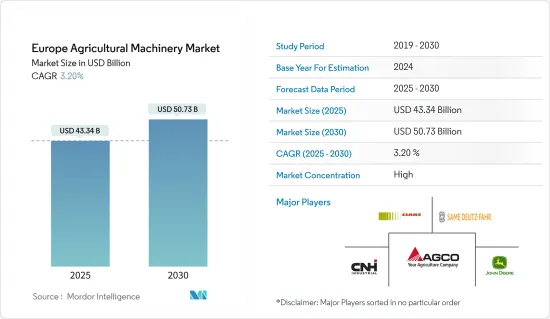

预计 2025 年欧洲农业机械市场规模为 433.4 亿美元,到 2030 年将达到 507.3 亿美元,预测期内(2025-2030 年)的复合年增长率为 3.20%。

欧盟农业正在经历重大转型,从传统的密集型密集模式,严重依赖季节性移工在成员国的农场工作。技术纯熟劳工的短缺日益严重,推动了欧洲国家的机械化进程,从而导致该地区农业机械销售增加。根据世界银行的资料,欧盟农业就业率将从2020年的4.32%下降到2022年的3.99%。可耕地面积的减少和淡水供应的减少也加剧了这一趋势,进一步增加了欧洲国家对农业机械化的需求。

拖拉机销售是欧洲农业机械市场成长的主要动力。根据欧洲国家主管机关的数据,2023年欧洲各地将註册211,700台拖拉机,其中158,100台为专用农业拖拉机。业界领导者正在引进配备先进技术的新机械,以提高该地区的农业效率和营运可行性。例如,2022年,约翰迪尔公司推出了一款无人操作员田间耕作拖拉机,以应对该地区劳动力短缺的挑战。

欧洲农业机械市场趋势

技术纯熟劳工短缺

欧洲农业传统上依赖季节性移工作为各成员国的农业劳动力。然而,更好的就业机会、更高的薪资和更高的生活水准正吸引越来越多的农村人口迁移到都市区,导致都市区迁移现象激增。例如,西班牙的农村人口预计将从 2019 年的 19.4% 下降到 2023 年的 18.4%,突显了这项人口结构变化。此外,农业工作要求高,工作时间长,需要体力劳动,并且经常暴露在风雨中,因此人们对农业的兴趣正在下降,尤其是年轻一代。这一趋势加剧了该地区农业劳动力短缺的问题,并对农业生产力构成了挑战。

世界银行预测,欧盟农业就业率将从2020年的4.32%下降到2022年的3.99%,凸显农业劳动力持续下降。持续的劳动力短缺正在推动欧洲农业向机械化和自动化转变,因为农民正在寻求其他方法来保持生产力。拖拉机作为农业机械的关键部件,由于机械化需求的不断增长,其市场成长潜力巨大。拖拉机作为重要的农业机械之一,市场具有巨大的成长潜力。为了提高作物产量和提高农业经营效率,该地区的农民越来越倾向于购买高端拖拉机来耕种更大的田地。

德国占据市场主导地位

德国是欧洲重要的农业机械设备市场。该国以精密工程和创新而闻名,是世界领先的农业机械出口国之一。此外,德国是欧洲最大的农业机械製造国和消费国。

在德国,拖拉机是农业机械的主要动力来源。在拖拉机市场,爱科集团凭藉 Massey Ferguson 和 Valtra Inc. 等品牌占据重要地位。市场参与企业正在推出创新设备以提高农业机械化水准。 2022年,凯斯推出大型方形打包机LB 424 XLD。此型号可生产尺寸为 120 公分 x 70 公分的超高密度捆包,密度提高 10%,进而提高捆包品质、处理和转子切割效率。

德国农民每年都会获得欧盟的补贴,帮助他们投资昂贵的现代化机械。这项补贴将使农场管理更有效率。然而,随着工人越来越多地转向非农业部门,对执行劳动密集型任务的农业机械的需求日益增长。

欧洲农机产业概况

欧洲农业机械市场主要受众多跨国公司的影响与推动。同样,Deutz-Fahr、John Deere、CNH Industrial、CLAAS KGaA mbH 和 AGCO Corporation 是欧洲农业机械市场中占有主要份额的一些知名公司。在这个市场运营的公司旨在透过产品特色、价格、品质、规模和技术创新来提高其影响力。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场动态

- 市场概况

- 市场驱动因素

- 技术纯熟劳工短缺

- 政府支持加强农业机械化

- 市场限制

- 初期采购成本高、维护成本高

- 波特五力分析

- 供应商的议价能力

- 买家的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争强度

第五章 市场区隔

- 类型

- 联结机

- 小于50马力

- 50至100马力

- 100~150 HP

- 超过150马力

- 犁地机械

- 犁

- 光环

- 耕作和耕耘机

- 其他设备

- 灌溉机械

- 喷水灌溉

- 滴灌

- 其他灌溉机械

- 收割机

- 联合收割机

- 青贮收割机

- 其他收割机械

- 牧草和饲料机械

- 草坪修剪机

- 打包机

- 其他牧草及饲料机械

- 其他类型

- 联结机

- 地区

- 德国

- 法国

- 英国

- 西班牙

- 义大利

- 俄罗斯

- 其他欧洲国家

第六章 竞争格局

- 最受欢迎的策略

- 市场占有率分析

- 公司简介

- CLAAS KGaA mbH

- Deere & Company

- Lely France

- CNH Industrial NV

- Kubota Corporation

- AGCO Corporation

- Same Deutz-Fahr

- Yanmar Co. Ltd

- Kuhn Group

第七章 市场机会与未来趋势

The Europe Agricultural Machinery Market size is estimated at USD 43.34 billion in 2025, and is expected to reach USD 50.73 billion by 2030, at a CAGR of 3.20% during the forecast period (2025-2030).

Agriculture in the European Union has undergone a significant transformation from its traditionally labor-intensive model, which relied heavily on seasonal immigrant workers in member states' farm fields. The increasing shortage of skilled labor has driven a rise in mechanization across European countries, leading to increased sales of agricultural machinery in the region. World Bank data indicates that employment in agriculture in the European Union decreased from 4.32% in 2020 to 3.99% in 2022. Additional factors contributing to this trend include the reduction in arable land area and declining freshwater availability, further intensifying the demand for farm mechanization in European countries.

Tractor sales are a primary driver of growth in the European agricultural machinery market. According to National Authorities of Europe, 211,700 tractors were registered across Europe in 2023, with 158,100 of these being specifically agricultural tractors. Industry leaders are introducing new machinery equipped with advanced technologies to enhance farming efficiency and ease of operations in the region. For example, in 2022, John Deere & Co. launched an operator-less tractor for field tilling, addressing the challenge of labor shortages in the region.

Europe Agricultural Machinery Market Trends

Shortage of Skilled Labor

European agriculture has traditionally depended on seasonal immigrant workers for farm labor across various member states. However, rural populations are increasingly drawn to urban areas due to better job prospects, higher salaries, and improved living standards, resulting in a rapid increase in rural-to-urban migration. For example, Spain's rural population decreased from 19.4% in 2019 to 18.4% in 2023, highlighting this demographic shift. Furthermore, the demanding nature of farm work, which often involves long hours, physical labor, and exposure to weather conditions, has led to a decline in interest in agricultural careers, particularly among younger generations. This trend has exacerbated the farm labor shortage in the region, creating challenges for agricultural productivity.

According to the World Bank, agricultural employment in the European Union decreased from 4.32% in 2020 to 3.99% in 2022, underscoring the ongoing decline in the agricultural workforce. This persistent labor shortage has prompted a significant shift towards mechanization and automation in European agriculture, as farmers seek alternative solutions to maintain productivity. Tractors, a crucial component of agricultural machinery, have experienced substantial growth potential in the market due to this increased demand for mechanization. Tractors, one of the essential agricultural machinery, have witnessed enormous growth potential in the market. Farmers in the region increasingly prefer purchasing high-end tractors to work on larger fields as part of their effort to improve crop yields and boost farm efficiencies.

Germany Dominates the Market

Germany stands as a significant market for agricultural machinery and implements in Europe. The country's reputation for precision engineering and innovation has positioned it as one of the world's leading exporters of agricultural machinery. Additionally, Germany ranks among the largest manufacturers and consumers of agricultural machinery within Europe.

Tractors serve as the primary power source for agricultural machinery in Germany. AGCO Corporation holds a prominent position in the tractor market, offering brands such as Massey Ferguson and Valtra Inc. Market participants are introducing innovative equipment to promote farm mechanization. In 2022, Case IH launched the LB 424 XLD large square baler model, which produces extra-dense 120 cm x 70 cm bales with a 10% increase in density, enhancing bale quality, handling, and rotor cutting efficiency.

German farmers receive annual subsidies from the European Union for investing in modern machinery, which can be costly. These subsidies enable more efficient farm operations. However, as workers increasingly prefer non-farming sectors, the demand for agricultural machinery to perform labor-intensive tasks is rising.

Europe Agricultural Machinery Industry Overview

The agricultural machinery market in Europe is consolidated and driven primarily by the presence of many global players. Same Deutz-Fahr, John Deere, CNH Industrial, CLAAS KGaA mbH, and AGCO Corporation are some prominent players holding a major share in the agricultural machinery market in Europe. The companies operating in the market aim to strengthen their presence through product features, pricing, quality, scale of operations, and technological innovations.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Shortage of Skilled Labor

- 4.2.2 Government Support to Enhance Farm Mechanization

- 4.3 Market Restraints

- 4.3.1 Heavy Initial Procurement Cost and High Expenditure on Maintenance

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Tractors

- 5.1.1.1 Less than 50 HP

- 5.1.1.2 50 to 100 HP

- 5.1.1.3 100 to 150 HP

- 5.1.1.4 Above 150 HP

- 5.1.2 Plowing and Cultivating Machinery

- 5.1.2.1 Plows

- 5.1.2.2 Harrows

- 5.1.2.3 Cultivators and Tillers

- 5.1.2.4 Other Equipment

- 5.1.3 Irrigation Machinery

- 5.1.3.1 Sprinkler Irrigation

- 5.1.3.2 Drip Irrigation

- 5.1.3.3 Other Irrigation Machinery

- 5.1.4 Harvesting Machinery

- 5.1.4.1 Combine Harvesters

- 5.1.4.2 Forage Harvesters

- 5.1.4.3 Other Harvesting Machinery

- 5.1.5 Haying and Forage Machinery

- 5.1.5.1 Mowers

- 5.1.5.2 Balers

- 5.1.5.3 Other Haying and Forage Machinery

- 5.1.6 Other Types

- 5.1.1 Tractors

- 5.2 Geography

- 5.2.1 Germany

- 5.2.2 France

- 5.2.3 United Kingdom

- 5.2.4 Spain

- 5.2.5 Italy

- 5.2.6 Russia

- 5.2.7 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Most Adopted Strategies

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 CLAAS KGaA mbH

- 6.3.2 Deere & Company

- 6.3.3 Lely France

- 6.3.4 CNH Industrial NV

- 6.3.5 Kubota Corporation

- 6.3.6 AGCO Corporation

- 6.3.7 Same Deutz-Fahr

- 6.3.8 Yanmar Co. Ltd

- 6.3.9 Kuhn Group

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

全球谷物螺旋钻市场

全球谷物螺旋钻市场 文化及娱乐建筑市场-全球产业规模、份额、趋势、机会及预测(按设施类型、建筑类型、最终用户、地区及竞争情况划分,2020-2030 年预测)全球农业机械市场:市场规模、市场份额、趋势分析(按产品、应用和地区)、细分市场预测(2025-2033 年)

文化及娱乐建筑市场-全球产业规模、份额、趋势、机会及预测(按设施类型、建筑类型、最终用户、地区及竞争情况划分,2020-2030 年预测)全球农业机械市场:市场规模、市场份额、趋势分析(按产品、应用和地区)、细分市场预测(2025-2033 年) 2032 年全球收穫后设备市场预测:依产品类型、作物类型、动力来源、技术、应用和地区划分2032 年农用卡车市场预测:按卡车类型、燃料类型、动力、驱动类型、销售管道、最终用户和地区进行的全球分析2032 年牧草和饲料设备市场预测:按设备类型、操作、动力来源、应用、最终用户和地区进行的全球分析全球农业切碎机市场

2032 年全球收穫后设备市场预测:依产品类型、作物类型、动力来源、技术、应用和地区划分2032 年农用卡车市场预测:按卡车类型、燃料类型、动力、驱动类型、销售管道、最终用户和地区进行的全球分析2032 年牧草和饲料设备市场预测:按设备类型、操作、动力来源、应用、最终用户和地区进行的全球分析全球农业切碎机市场 农机具的印度市场评估:类别,各功能,各流通管道,各地区,机会,预测(2019年度~2033年度)

农机具的印度市场评估:类别,各功能,各流通管道,各地区,机会,预测(2019年度~2033年度) 全球农业机械市场 -市场占有率和排名、总销售量和需求预测(2025-2031)全球开槽机市场

全球农业机械市场 -市场占有率和排名、总销售量和需求预测(2025-2031)全球开槽机市场