|

市场调查报告书

商品编码

1686609

石墨烯:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Graphene - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

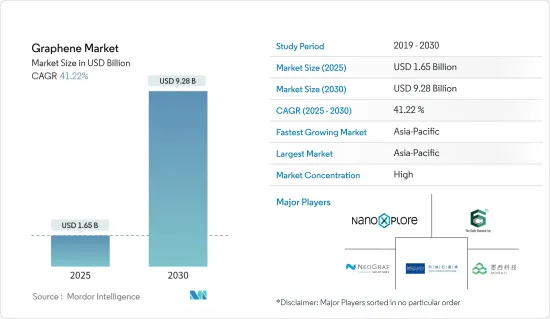

预计 2025 年石墨烯市场规模为 16.5 亿美元,到 2030 年将达到 92.8 亿美元,预测期内(2025-2030 年)的复合年增长率为 41.22%。

主要亮点

- 在新冠疫情期间,石墨烯的需求受到各产业不确定性的影响。然而,随着各国取消限制,医疗保健和生物医学等领域对石墨烯的需求正在上升。

- 石墨烯的需求主要受到其在航太、电子和通讯行业的广泛应用的推动。

- 然而,高昂的生产成本和与现有材料的竞争可能会阻碍市场成长。

- 用于 DNA定序的石墨烯奈米装置的开发以及石墨烯在检测器中的应用预计将为研究市场提供成长机会。

- 预计亚太地区将成为石墨烯消费量最大的地区。该市场受到中国、日本、印度和韩国电子和通讯产业快速发展的支持。

石墨烯市场趋势

电子和通讯产业主导市场

- 石墨烯及其衍生物在电子、通讯产业有广泛的应用。在该领域,石墨烯被广泛应用于各种应用,包括防碎触控萤幕、电晶体、增强型锂离子电池、光学电子、印刷电子和导电油墨。

- 石墨烯具有多种有用的特性,包括高机械强度、高电子迁移率和优异的导热性。

- 电子业是全球规模最大、成长最快的产业之一。在数位时代,电子设备发挥着至关重要的作用。这些产品的需求正在激增,巩固了它们作为全球重要经济驱动力的地位。

- 为了满足日益增长的需求,各公司最近都在投资建立电子製造工厂。值得注意的投资包括:

- 台湾晶片巨擘台积电于 2023 年 8 月表示,将采取战略倡议,在 2023 年欧洲建造第一家晶圆厂,投资 38 亿美元,该晶圆厂将设在德国。这项投资是在政府大力支持这座价值 110 亿美元的工厂之后进行的,该工厂旨在解决欧洲供应链本地化计划。

- 2024 年 6 月,义法半导体公司 (STMicroelectronics NV) 宣布打算在义大利卡塔尼亚投资 50 亿欧元(54 亿美元)建立晶片製造和封装工厂。该多年计划部分资金来自欧盟晶片法案。义大利政府计划向意法半导体提供20亿欧元的补贴。

- 此外,各国政府也推出了各种倡议来发展电子製造业。例如,2024年5月,英国政府宣布建立英国半导体研究所的计画。该独立研究所旨在成为研究人员、学者以及公共和私营部门的中心枢纽,将在实现政府雄心勃勃的国家战略中发挥至关重要的作用。

- 所有这些因素预计将推动电子和通讯行业的石墨烯消费。

亚太地区占市场主导地位

- 受快速工业化和石墨烯应用专利激增的推动,亚太地区引领石墨烯市场。因此,氧化石墨烯将迎来巨大的成长。

- 中国是全球最大的电子产品生产基地之一,为韩国、新加坡和台湾等现有的上游製造商带来了激烈的竞争。智慧型手机、OLED 电视和平板电脑等电子产品在市场家用电子电器领域的需求成长最快。

- 石墨烯由于其多种技术优势,在电子产业的应用正在迅速扩大。最近值得注意的投资:

- 2024年1月,美国科研人员联合研发出新型稳定半导体石墨烯,其性能为硅的10倍、其他二维半导体的20倍。

- 医疗设备製造和医疗保健产业也是石墨烯近期的主要消费者。近年来,医疗设备製造业的投资不断增加。例如:

- 2024年5月,日本Omron Healthcare宣布将斥资1,550万美元在印度泰米尔纳德邦建立一家医疗设备製造厂。

- 2023年7月,深圳先进技术研究院开始大量生产其新开发的磁振造影(MRI)技术。

- 预计所有这些因素都将推动亚太地区对石墨烯的需求。

石墨烯产业概况

石墨烯市场本质上是整合的。主要参与者(不分先后顺序)包括 NanoXplore Inc.、第六元素(常州)材料科技、NeoGraf、Morsh(宁波墨希科技)和厦门科纳石墨烯科技。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 调查前提条件

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场动态

- 市场驱动因素

- 石墨烯支持航太工业

- 印刷电子产品需求不断成长

- 其他驱动因素

- 市场限制

- 生产成本高

- 替代方案的可用性

- 其他限制因素

- 产业价值链分析

- 波特五力分析

- 供应商的议价能力

- 买家的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章 市场区隔

- 依产品类型

- 石墨烯片和薄膜

- 奈米带

- 奈米血小板

- 氧化石墨烯

- 其他产品类型

- 按最终用户产业

- 电子和通讯

- 生医保健

- 活力

- 航太和国防

- 其他最终用户产业

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 东南亚国协

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 义大利

- 法国

- 西班牙

- 其他欧洲国家

- 南美洲

- 巴西

- 阿根廷

- 哥伦比亚

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争格局

- 併购、合资、合作、协议

- 市场占有率(%)**/排名分析

- 主要企业策略

- 公司简介

- ACS Material

- 2D Carbon Graphene Material Co. Ltd

- Elcora Advanced Materials Corp.

- First Graphene

- G6 Materials Corp.

- Global Graphene Group

- Grafoid Inc.

- Grupo Graphenano

- Graphene Manufacturing Group Ltd

- Graphene Production

- Graphenea

- Haydale Graphene Industries PLC

- Morsh(Ningbo Moxi Technology Co. Ltd)

- Nanoxplore Inc.

- Neograf

- Perpetuus Advanced Materials Plc

- The Sixth Element(Changzhou)Materials Technology Co. Ltd

- Thomas Swan & Co. Ltd

- Universal Matter

- Versarien PLC

- Vorbeck Materials Corp.

- Xiamen Knano Graphene Technology Corporation Limited

第七章 市场机会与未来趋势

- 用于 DNA定序的石墨烯奈米装置的开发

- 检测器中的石墨烯

- 其他机会

简介目录

Product Code: 53191

The Graphene Market size is estimated at USD 1.65 billion in 2025, and is expected to reach USD 9.28 billion by 2030, at a CAGR of 41.22% during the forecast period (2025-2030).

Key Highlights

- During the COVID-19 pandemic, the demand for graphene experienced volatility from various industries. However, the demand for graphene has seen a rise from sectors such as healthcare and biomedical as various countries have lifted lockdowns.

- The demand for graphene is majorly driven by its increased utilization from aerospace and electronics and communication industry.

- However, the high cost of production and the competition from existing materials is likely to hamper the market growth.

- The development of graphene nanodevices for DNA sequencing and adoption of graphene in photodetectors are expected to create growth opportunities for the market studied.

- The Asia-Pacific region is expected to become the largest region consuming graphene. The fast-developing electronics & telecommunication industry in China, Japan, India, and South Korea is supporting the market.

Graphene Market Trends

Electronics and Telecommunication Segment to Dominate the Market

- Graphene and its derivatives are extensively used in the electronics and telecommunications industry. This sector harnesses graphene for a myriad of applications, such as unbreakable touchscreens, transistors, enhanced lithium-ion batteries, optical electronics, printed electronics, and conductive inks.

- Graphene has several useful properties, including high mechanical strength, electron mobility, and superior thermal conductivity.

- The electronics industry stands as one of the largest and fastest-growing sectors globally. In the digital age, electronic devices play a pivotal role. The demand for these gadgets is set to surge, solidifying their status as a key economic driver globally.

- Inorder to meet the growing demand, various companies have invested in the setting up electronic manufacturing plants in recent times. Some of the notable investments include:

- In August 2023, in a strategic move, Taiwanese chip giant TSMC pledged USD 3.8 billion for its inaugural European factory, to be based in Germany. This investment follows significant support from the state, with the USD 11 billion facility corresponding to Europe's initiative to localize its supply chains.

- In June 2024, STMicroelectronics NV announced its intention to invest EUR 5 billion (USD 5.4 billion) in a chip manufacturing and packaging facility in Catania, Italy. This multi-year project is receiving partial funding from the European Union's Chips Act. The Italian government is set to provide STMicro with EUR 2 billion in subsidies.

- Furthermore, various governments have started various initiatives inorder to develop the electronic product manufacturing. For instance, In May 2024, The UK government unveiled plans to establish the UK Semiconductor Institute. Designed as a central hub for researchers, academics, and both public and private entities, this independent institute will play a pivotal role in executing the government's ambitious national strategy.

- All such factors are expected to drive the consumption of graphene in the electronics and telecommunication industry.

Asia Pacific to Dominate the Market

- Asia-Pacific leads the graphene market, driven by swift industrialization and a surge in graphene-based application patents. As a result, graphene oxide is set for significant growth.

- China has one of the world's largest electronics production bases and offers tough competition to the existing upstream producers, such as South Korea, Singapore, and Taiwan. Electronic products, such as smartphones, OLED TVs, and tablets, have the highest growth rates in the consumer electronics segment of the market in terms of demand.

- In the electronics industry, the usage of graphene has been growing at a rapid pace owing to its various technological advantages. Some of the notable investments in recent times include:

- In January 2024, researchers from China and the United States jointly created a new type of stable semiconductor graphene, which performs ten times higher than silicon and 20 times larger than the other two-dimensional semiconductors.

- The Medical device manufacturing and healthcare industry is another major consumer of graphene in recent times. There has been growing investments in the medical device production in recent times. For instance:

- In May 2024, Omron Healthcare, a Japanese company, announced that it would establish a medical device manufacturing plant in Tamil Nadu, India for USD15.5 million

- In July 2023, the Shenzen Institute of Advanced Technology commenced mass production of its newly developed magnetic resonance imaging (MRI) technology.

- All these factors are expected to drive the demand of graphene in the Asia-Pacific region.

Graphene Industry Overview

The graphene market is consolidated in nature. The major players (not in any particular order) include NanoXplore Inc., The Sixth Element (Changzhou) Materials Technology Co. Ltd, NeoGraf, Morsh (Ningbo Moxi Technology Co. Ltd), and Xiamen Knano Graphene Technology Co. Ltd .

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Graphene Aiding the Aerospace Industry

- 4.1.2 Rising Demand for Printed Electronics

- 4.1.3 Other Drivers

- 4.2 Market Restraints

- 4.2.1 High Production Cost

- 4.2.2 Availability of Substitutes

- 4.2.3 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 By Product Type

- 5.1.1 Graphene Sheets and Films

- 5.1.2 Nanoribbons

- 5.1.3 Nanoplatelets

- 5.1.4 Graphene Oxide

- 5.1.5 Other Product Types

- 5.2 By End-user Industry

- 5.2.1 Electronics and Telecommunication

- 5.2.2 Bio-medical and Healthcare

- 5.2.3 Energy

- 5.2.4 Aerospace and Defense

- 5.2.5 Other End-user Industries

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Spain

- 5.3.3.6 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 ACS Material

- 6.4.2 2D Carbon Graphene Material Co. Ltd

- 6.4.3 Elcora Advanced Materials Corp.

- 6.4.4 First Graphene

- 6.4.5 G6 Materials Corp.

- 6.4.6 Global Graphene Group

- 6.4.7 Grafoid Inc.

- 6.4.8 Grupo Graphenano

- 6.4.9 Graphene Manufacturing Group Ltd

- 6.4.10 Graphene Production

- 6.4.11 Graphenea

- 6.4.12 Haydale Graphene Industries PLC

- 6.4.13 Morsh (Ningbo Moxi Technology Co. Ltd)

- 6.4.14 Nanoxplore Inc.

- 6.4.15 Neograf

- 6.4.16 Perpetuus Advanced Materials Plc

- 6.4.17 The Sixth Element (Changzhou) Materials Technology Co. Ltd

- 6.4.18 Thomas Swan & Co. Ltd

- 6.4.19 Universal Matter

- 6.4.20 Versarien PLC

- 6.4.21 Vorbeck Materials Corp.

- 6.4.22 Xiamen Knano Graphene Technology Corporation Limited

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Development of Graphene Nanodevices for DNA Sequencing

- 7.2 Adoption of Graphene into Photodetectors

- 7.3 Other Opportunities

02-2729-4219

+886-2-2729-4219

石墨烯市场(按石墨烯类型、生产技术、原料来源、石墨烯衍生物、应用和最终用户产业划分)-2025-2030 年全球预测

石墨烯市场(按石墨烯类型、生产技术、原料来源、石墨烯衍生物、应用和最终用户产业划分)-2025-2030 年全球预测 二维材料市场-全球产业规模、份额、趋势、机会和预测(按类型、应用、地区和竞争细分,2020-2030 年)

二维材料市场-全球产业规模、份额、趋势、机会和预测(按类型、应用、地区和竞争细分,2020-2030 年) 全球二维材料市场预测(至 2032 年):按形式、材料类型、生产方法、应用、最终用户和地区划分

全球二维材料市场预测(至 2032 年):按形式、材料类型、生产方法、应用、最终用户和地区划分 2025 年至 2033 年石墨烯市场规模、份额、趋势及预测(按类型、应用、最终用途行业和地区)Mxene 市场,2032 年全球预测:按类型、形式、细分市场、应用、最终用户和地区全球石墨烯市场:2032 年预测-按产品、形态、通路、应用和地区进行分析

2025 年至 2033 年石墨烯市场规模、份额、趋势及预测(按类型、应用、最终用途行业和地区)Mxene 市场,2032 年全球预测:按类型、形式、细分市场、应用、最终用户和地区全球石墨烯市场:2032 年预测-按产品、形态、通路、应用和地区进行分析 2025年石墨烯全球市场

2025年石墨烯全球市场 全球石墨烯市场:2025-2030 年预测全球石墨烯市场研究报告-产业分析、规模、份额、成长、趋势及2025年至2033年预测

全球石墨烯市场:2025-2030 年预测全球石墨烯市场研究报告-产业分析、规模、份额、成长、趋势及2025年至2033年预测 2025年二维材料全球市场报告

2025年二维材料全球市场报告

▼