|

市场调查报告书

商品编码

1686645

智慧计量(AMI) -市场占有率分析、产业趋势与统计、成长预测(2025-2030)Smart Meters (AMI) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

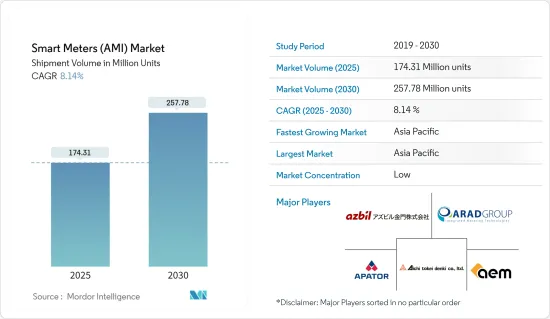

智慧电錶市场规模(基于出货量)预计将从 2025 年的 1.7431 亿台扩大到 2030 年的 2.5778 亿台,预测期内(2025-2030 年)的复合年增长率为 8.14%。

主要亮点

- 智慧电錶正在全球被引入电力、天然气和水等公共产业领域。这些仪表具有双向通讯功能,可即时追踪供应商和消费者的公用事业使用情况。此功能不仅使供应商能够远端启动、读取和切断供应,而且还有助于实施家庭能源管理系统 (HEMS) 和建筑能源管理系统 (BEMS)。此类系统既适用于单一住宅,也适用于整栋建筑,并能提供电力消耗的透明视图。随着智慧电錶的普及,它们将增强能源管理和效率,有助于实现各种地方永续性目标。

- 随着经济活动的激增导致能源消耗的增加,能源效率已成为全球的首要任务。考虑到这一点,世界各地正在迅速整合各行业的智慧电錶等节能解决方案,以优化能源和公用事业的使用。政府和组织越来越重视永续能源实践,而且这种势头还会持续下去。智慧电錶有望透过促进更有效率的能源发行和消耗为这些努力做出贡献。

- 财政奖励和政府对电网数位化的支持政策正在推动智慧电錶市场的成长。这些因素将推动未来几年智慧电錶市场的发展,并为该领域的未来创新和进步奠定坚实的基础。

- 然而,智慧电錶市场面临挑战,尤其是与更换电力供应商相关的成本。由于这些系统依赖数位组件和连接,因此它们有可能随着技术变革而过时,并可能限制其在不同供应商之间的适应性。此外,每个公用事业公司独特的使用者介面使智慧电錶相容性变得复杂,而缺乏标准化的介面开发则加剧了这项挑战。

- 此外,持续的全球景气衰退可能会减少对电子设备的需求,从而导致对智慧电錶的需求减少,阻碍市场成长。

智慧电錶(AMI)市场趋势

智慧电錶占据市场主导地位,这一趋势在预测期内仍将持续

- 商业建筑对智慧电錶的需求很高。企业正在其办公室和其他空间采用这些计量表来优化收费。商业空间通常跨越多层,因此监控电力消耗以减少浪费非常重要。这些智慧电錶还可以检测供电线路中断情况,从而快速做出反应。

- 根据英国领先的新房屋担保和保险公司国家住宅建筑委员会 (NHBC) 的资料,2024 年第二季登记建造的住宅有 29,281 套。建筑数量的增加表明英国对智慧电錶的需求不断增长。

- 此外,许多公司正在推出创新解决方案来满足日益增长的智慧电錶需求。例如,Areti于2024年5月宣布其在罗马的智慧电錶数量已超过100万台,并计划在2025年底前在罗马及其附近的福尔梅洛市更换约170万台智慧电錶。

- 根据美国能源资讯署(EIA)的数据,2023年美国公用事业规模的发电设施将产生约4.178兆千瓦时(kWh)的电力,显示美国电力需求将持续成长。电力公司越来越需要更好地管理和优化其能源发行网路。因此,随着有关能源消耗的详细资讯的出现,智慧电錶在该国的采用率预计将会增加,这可以帮助消费者发现利用智慧电錶减少能源使用和节省资金的机会。

- 增加对智慧电网计划的投资是推动市场成长的主要因素之一。据中国国家电网公司称,这家总部位于北京的国有公司计划今年增加对国家电网建设的投资,以稳定国家的就业和能源消耗。该公司表示,2023年将为电网计划拨款超过5,200亿元人民币(769.5亿美元)。由于后续稳定经济的措施,预计今年电力消耗量将进一步上升。

- 根据美国能源资讯署(EIA)的数据,预计未来30年全球发电量将成长一倍以上,到2050年将达到约14.7兆瓦。 2020年全球装机发电能力为7.1兆瓦,显示全球电力需求持续成长。电力公司越来越需要管理和优化其能源发行网路。

亚太地区占主要市场占有率

- 中国对智慧电錶的需求不断增长是一个关键趋势,受到多种因素的影响,包括政府政策、快速都市化、智慧电网技术的进步以及对能源效率和减碳的日益重视。作为世界上最大的能源消费国之一,中国正在大力投资电网现代化,而智慧电錶的引入是这项战略倡议的核心要素。

- 由于中国唯一电网营运商国家电网公司和中国南方电力集团公司的严格要求,中国目前在亚太地区的智慧电錶部署方面处于领先地位。然而,随着中国智慧电錶全面部署的临近,年度需求量明显下降,显示推广阶段正在逐渐结束。

- 中国是智慧电錶製造领域的主要参与者,当地企业实力雄厚。该公司也是最大的智慧电錶生产商之一,其产品在推广阶段主要在国内销售。中国市场由国营企业主导,非中国公司几乎不可能在中国境内有效竞争。

- 此外,随着国内对智慧电錶的需求不断增长,企业也进行了多项投资。例如,三菱电机公司于2024年6月宣布,将与系统整合商光荣科技服务股份有限公司及台湾主要通讯公司中华电信合作提供智慧电錶系统。

- 日本政府宣布计划拨款 20 兆日圆(1,550 亿美元),以刺激对新电网技术、节能住宅和其他可减少该国二氧化碳排放的技术的投资。这项重大投资凸显了政府致力于推广永续能源解决方案的决心。

- 印度政府正积极推动智慧电錶的研发。为了实现全印度的普遍用电,政府还建立了智慧电网,承诺提供实惠的价格和其他客户利益。实现这种智慧电网的第一步是引入先进的计量基础设施(AMI)。智慧电錶国家计画(SMNP)促进了智慧电錶在全国的推广。该倡议由电力部下属的公共部门合资企业能源效率服务有限公司(EESL)统筹。

智慧电錶(AMI)市场概况

某些地区的智慧电錶市场正在成长。这是因为 AEM、手錶、Apator SA、Arad Group 和 Azbil Kimmon 等主要企业都努力保持市场竞争力。例如,中国市场的衰退导致全球层面的竞争加剧。同时,欧洲的扩张和美国的替代计划为市场供应商创造了新的机会。

此外,大规模投资的介入也提高了现有企业的门槛,加剧了竞争。此外,智慧电錶正在被推广到各种最终用户和地区。因此,需求的大幅增长加上政府努力增加各个地区的部署数量,预计将导致市场参与者之间的竞争加剧,以满足日益增长的需求。

此外,智慧家庭和工业解决方案的日益普及,加上政府的支持政策,正在鼓励一些新参与企业进入市场。 SteamaCo 等製造业新兴企业已获得种子投资,为非洲製造智慧离网电錶。

该公司得到了多家解决方案新兴企业公司的支持,其中包括 Sympower,该公司帮助公用事业公司将智慧电錶设备连接到最终用户,并使用电錶资料建立可靠的智慧电网。因此,由于对能源问题的日益关注,市场竞争水平很高,预计在预测期内竞争将会加剧。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概览

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买家的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

- 产业价值链分析

- 宏观经济因素对全球智慧电錶市场的影响

第五章市场动态

- 市场驱动因素

- 加大智慧电网计划投资

- 需要提高公用事业效率

- 加强政府监管

- 智慧城市部署的成长

- 所有最终用户对永续公用事业供应的需求

- 市场挑战

- 高成本和安全隐患

- 与智慧电錶整合困难

- 缺乏基础设施资本投资和投资报酬率

- 更换电力供应商的成本

第六章市场区隔

- 按地区 - 智慧燃气表

- 北美洲

- 美国

- 加拿大和中美洲

- 欧洲

- 英国

- 法国

- 义大利

- 亚洲

- 中国

- 日本

- 澳洲和纽西兰

- 拉丁美洲

- 中东和非洲

- 北美洲

- 按地区 - 智慧水錶

- 北美洲

- 美国

- 加拿大和中美洲

- 欧洲

- 英国

- 法国

- 义大利

- 亚洲

- 中国

- 日本

- 澳洲和纽西兰

- 拉丁美洲

- 中东和非洲

- 北美洲

- 按地区 - 智慧电錶

- 北美洲

- 美国

- 加拿大和中美洲

- 欧洲

- 英国

- 法国

- 义大利

- 亚洲

- 中国

- 日本

- 澳洲和纽西兰

- 拉丁美洲

- 中东和非洲

- 北美洲

第七章竞争格局

- 公司简介

- AEM

- Aichi Tokei Denki Co.Ltd.

- Apator SA

- Arad Group

- Azbil Kimmon Co. Ltd.

- Badger Meter Inc.

- Diehl Stiftung & Co. KG

- Elster Group GmbH(Honeywell International Inc.)

- General Electric Company

- Hexing Electric company Ltd.

- Holley Technology Ltd.

- Itron Inc.

- Jiangsu Linyang Energy Co. Ltd.

- Kamstrup A/S

- Landis+GYR Group AG

- Mueller Systems LLC(Muller Water Products Inc.)

- EDMI Limited(OSAKI ELECTRIC CO. LTD.)

- Neptune Technology Group Inc.(Roper Technologies, Inc.)

- Ningbo Sanxing Medical Electric Co., Ltd

- Pietro Fiorentini SpA

- Sagemcom SAS

- Sensus USA Inc.(Xylem Inc.)

- Aclara Technologies LLC(Hubbell Inc.)

- Wasion Holdings Limited

- Yazaki Corporation

- Zenner International GmbH & Co. KG

- Market Rankings Analysis

- Smart Electricity Meter Market

- Smart Gas Meter Market

- Smart Water Meter Market

第八章 市场机会与未来趋势

- 智慧电錶市场的未来

- 智慧燃气表市场的未来

- 智慧水錶市场的未来

The Smart Meters Market size in terms of shipment volume is expected to grow from 174.31 million units in 2025 to 257.78 million units by 2030, at a CAGR of 8.14% during the forecast period (2025-2030).

Key Highlights

- Globally, utilities such as electricity, gas, and water are increasingly adopting smart meters. These meters enable real-time tracking of utility usage for both suppliers and consumers through their two-way communication feature. This functionality not only allows suppliers to remotely start, read, and cut off supply but also aids in implementing home energy management systems (HEMS) and building energy management systems (BEMS). Such systems offer a transparent view of electric power consumption, catering to both individual homes and entire buildings. As smart meters become more prevalent, they are set to enhance energy management and efficiency, aligning with the sustainability goals of various regions.

- As economic activities surge, leading to increased energy consumption, energy efficiency has taken center stage as a global priority. In light of this, regions worldwide are rapidly integrating energy-efficient solutions, like smart meters, across diverse industries to optimize energy and utility usage. This momentum is likely to persist, with governments and organizations increasingly valuing sustainable energy practices. Smart meters are poised to be instrumental in these endeavors, promoting more efficient energy distribution and consumption.

- Financial incentives for grid digitalization, coupled with supportive government policies, are fueling growth in the smart metering market. These elements are set to broaden the market for smart meters in the years ahead, laying a solid groundwork for future innovations and advancements in the sector.

- However, the smart metering market faces challenges, particularly concerning the costs associated with switching utility suppliers. Given that these systems depend on digital components and connectivity, they risk becoming obsolete with technological shifts, which can restrict their adaptability across various suppliers. Furthermore, the unique user interfaces of each utility provider complicate the interchangeability of smart meters, a challenge intensified by the lack of standardized interface developments.

- Additionally, the ongoing global economic downturn has dampened the demand for electronic devices, leading to a reduced appetite for smart meters, which could hinder market growth.

Smart Meters (AMI) Market Trends

Smart Electricity Meter Dominates the Market and will Continue the Trend Over the Forecast Period

- Smart electricity meters are in high demand within commercial buildings. Businesses are adopting these meters in offices and other spaces to optimize billing. Since commercial spaces often span multiple floors, monitoring power consumption and minimizing waste is crucial. These smart meters can also detect supply line disturbances, allowing for swift responses.

- Data from the National House Building Council (NHBC), the UK's leading new home warranties and insurance provider, reveals that 29,281 new homes were registered for construction in Q2 2024. This uptick in construction signals a rising demand for smart meters in the UK.

- Furthermore, numerous companies are launching innovative solutions to meet the rising demand for smart meters. For example, in May 2024, Areti announced surpassing the milestone of 1 million smart meters in Rome, with plans to replace the roughly 1.7 million meters in Rome and the nearby municipality of Formello by the close of 2025.

- According to the Energy Information Administration (EIA), in 2023, nearly 4,178 billion kilowatt hours (kWh) of electricity were generated at utility-scale electricity generation facilities in the United States, which shows the demand for electricity in the United States is growing continuously. There is a growing need for utilities to manage better and optimize their energy distribution network. Thus, the availability of detailed information about energy consumption, which can help the consumer identify opportunities to reduce energy usage and save money with smart electricity meters, is projected to increase the adoption of smart electricity meters in the country.

- Increased investments in smart grid projects are one of the main drivers fueling market growth. According to the State Grid Corp. of China, the Beijing-based state-owned company plans to increase its investment in domestic grid construction this year to stabilize the nation's employment and energy consumption. The company announced it would allocate more than CNY 520 billion (USD 76.95 billion) to power grid projects in 2023. This year's power consumption is anticipated to rise further due to follow-up measures to stabilize the economy.

- According to the Energy Information Administration (EIA), global electricity generation capacity is expected to more than double in the next three decades, reaching approximately 14.7 terawatts by 2050. In 2020, the world's installed electricity capacity stood at 7.1 terawatts, which shows the demand for electricity around the globe is growing continuously. There is a growing need for utilities to manage and optimize their energy distribution networks.

Asia Pacific Holds Major Market Share

- The increasing demand for smart electricity meters in China represents a significant trend influenced by various factors, including government policies, rapid urbanization, advancements in smart grid technology, and a growing emphasis on energy efficiency and carbon reduction. As one of the world's largest energy consumers, China has been making substantial investments in modernizing its electricity grid, with the deployment of smart meters being a central component of its strategic initiatives.

- China currently leads the Asia Pacific region in smart meter rollouts, driven by stringent mandates from the State Grid Corporation of China and China Southern Power Grid, the country's sole grid operators. However, as China approaches the full deployment of smart meters, there is a noticeable reduction in annual demand, signaling the gradual conclusion of the rollout phase.

- China is a major player in the manufacturing of smart electricity meters, with a strong presence of local companies. It is also one of the largest producers of smart electricity meters, primarily consumed domestically during the rollout phase. The Chinese market is dominated by state-owned enterprises, making it nearly impossible for non-Chinese companies to compete effectively within the country.

- Additionally, companies have made several investments in response to the country's growing demand for smart electricity meters. For instance, in June 2024, Mitsubishi Electric Corporation announced its collaboration with system integrator Glory Technology Service Inc. and Taiwan's leading telecommunications company, Chunghwa Telecom Co., Ltd., to deliver a Smart-meter System.

- The Japanese government has announced plans to allocate JPY 20 trillion (USD 155 billion) to foster investments in new power grid technology, energy-efficient homes, and other technologies to reduce the nation's carbon footprint. This substantial financial commitment underscores the government's dedication to promoting sustainable energy solutions.

- The Indian government is diligently advancing the development of smart electricity meters. To achieve universal power access across India, the government also established smart grids that promise affordability and other customer benefits. The initial stride toward realizing these smart grids is the adoption of Advanced Metering Infrastructure (AMI). The Smart Meter National Program (SMNP) facilitates the nationwide deployment of smart meters. This initiative is overseen by Energy Efficiency Services Limited (EESL), a joint venture of public sector undertakings under the Ministry of Power.

Smart Meters (AMI) Market Overview

The smart meters market has grown in certain regions. This is leading companies like AEM, Aichi Tokei Denki Co.Ltd., Apator SA, Arad Group, and Azbil Kimmon Co. Ltd., strive to maintain a competitive edge in the market. For instance, the receding market in China increased this competitive intensity at a global level. At the same time, the rollouts in Europe and replacement projects in the United States offered new opportunities for the market vendors.

Moreover, the involvement of large-scale investment also increases the barriers for the existing players, thereby pushing the industry toward increasing competition. Also, smart meters are increasingly being deployed in various end users and regions. Hence, the substantial increase in demand, coupled with government initiatives to increase the number of rollouts in various regions, is expected to increase the degree of competition amongst the market players to meet the increasing demand.

Additionally, the growing penetration of smart home and industrial solutions coupled with supportive government initiatives has attracted several new players to the market. Manufacturing startups, such as SteamaCo, secured seed investments to build smart off-grid electricity meters for Africa.

The company is supported by several solution provider startups, such as Sympower, which helps utilities connect smart metering devices to their end users and use the metering data to build a reliable smart grid. Therefore, the degree of competition is high and expected to increase in the same in the market study for the forecasted period, owing to the increasing emphasis on energy concerns.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Degree of Competition

- 4.3 Industry Value Chain Analysis

- 4.4 mpact of Macroeconomic Factors on the Global Smart Meter Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increased Investments in Smart Grid Projects

- 5.1.2 Need for Improvement in Utility Efficiency

- 5.1.3 Supportive Government Regulations

- 5.1.4 Growth in Smart City Deployment

- 5.1.5 Demand for Sustainable Utility Supply for All End Users

- 5.2 Market Challenges

- 5.2.1 High Costs and Security Concerns

- 5.2.2 Integration Difficulties with Smart Meters

- 5.2.3 Lack of Capital Investment for Infrastructure Installation and Lack of ROI

- 5.2.4 Utility Supplier Switching Costs

6 MARKET SEGMENTATION

- 6.1 By Geography - Smart Gas Meter

- 6.1.1 North America

- 6.1.1.1 United States

- 6.1.1.2 Canada and Central America

- 6.1.2 Europe

- 6.1.2.1 United Kingdom

- 6.1.2.2 France

- 6.1.2.3 Italy

- 6.1.3 Asia

- 6.1.3.1 China

- 6.1.3.2 Japan

- 6.1.4 Australia and New Zealand

- 6.1.5 Latin America

- 6.1.6 Middle East and Africa

- 6.1.1 North America

- 6.2 By Geography - Smart Water Meter

- 6.2.1 North America

- 6.2.1.1 United States

- 6.2.1.2 Canada and Central America

- 6.2.2 Europe

- 6.2.2.1 United Kingdom

- 6.2.2.2 France

- 6.2.2.3 Italy

- 6.2.3 Asia

- 6.2.3.1 China

- 6.2.3.2 Japan

- 6.2.4 Australia and New Zealand

- 6.2.5 Latin America

- 6.2.6 Middle East and Africa

- 6.2.1 North America

- 6.3 By Geography - Smart Electricity Meter

- 6.3.1 North America

- 6.3.1.1 United States

- 6.3.1.2 Canada and Central America

- 6.3.2 Europe

- 6.3.2.1 United Kingdom

- 6.3.2.2 France

- 6.3.2.3 Italy

- 6.3.3 Asia

- 6.3.3.1 China

- 6.3.3.2 Japan

- 6.3.4 Australia and New Zealand

- 6.3.5 Latin America

- 6.3.6 Middle East and Africa

- 6.3.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 AEM

- 7.1.2 Aichi Tokei Denki Co.Ltd.

- 7.1.3 Apator SA

- 7.1.4 Arad Group

- 7.1.5 Azbil Kimmon Co. Ltd.

- 7.1.6 Badger Meter Inc.

- 7.1.7 Diehl Stiftung & Co. KG

- 7.1.8 Elster Group GmbH (Honeywell International Inc.)

- 7.1.9 General Electric Company

- 7.1.10 Hexing Electric company Ltd.

- 7.1.11 Holley Technology Ltd.

- 7.1.12 Itron Inc.

- 7.1.13 Jiangsu Linyang Energy Co. Ltd.

- 7.1.14 Kamstrup A/S

- 7.1.15 Landis+ GYR Group AG

- 7.1.16 Mueller Systems LLC (Muller Water Products Inc.)

- 7.1.17 EDMI Limited (OSAKI ELECTRIC CO. LTD.)

- 7.1.18 Neptune Technology Group Inc. (Roper Technologies, Inc.)

- 7.1.19 Ningbo Sanxing Medical Electric Co., Ltd

- 7.1.20 Pietro Fiorentini SpA

- 7.1.21 Sagemcom SAS

- 7.1.22 Sensus USA Inc. (Xylem Inc.)

- 7.1.23 Aclara Technologies LLC (Hubbell Inc.)

- 7.1.24 Wasion Holdings Limited

- 7.1.25 Yazaki Corporation

- 7.1.26 Zenner International GmbH & Co. KG

- 7.2 Market Rankings Analysis

- 7.2.1 Smart Electricity Meter Market

- 7.2.2 Smart Gas Meter Market

- 7.2.3 Smart Water Meter Market

8 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 8.1 Future of the Market - Smart Electricity Meter

- 8.2 Future of the Market - Smart Gas Meter

- 8.3 Future of the Market - Smart Water Meter

智慧电錶市场按类型、通讯技术、技术、组件、阶段、应用、最终用途、部署模式和客户类型划分 - 2025-2030 年全球预测

智慧电錶市场按类型、通讯技术、技术、组件、阶段、应用、最终用途、部署模式和客户类型划分 - 2025-2030 年全球预测 智慧电錶市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

智慧电錶市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测 电网现代化市场 - 全球产业规模、份额、趋势、机会和预测(按组件、应用、最终用户、地区和竞争细分,2020-2030 年预测)

电网现代化市场 - 全球产业规模、份额、趋势、机会和预测(按组件、应用、最终用户、地区和竞争细分,2020-2030 年预测) 智慧电表的北美市场 - 第7版

智慧电表的北美市场 - 第7版 智慧电錶市场规模及预测(2021-2031 年)、全球及地区份额、趋势及成长机会分析报告涵盖范围:按类型、技术、最终用户及地理划分

智慧电錶市场规模及预测(2021-2031 年)、全球及地区份额、趋势及成长机会分析报告涵盖范围:按类型、技术、最终用户及地理划分 2025年电网现代化全球市场报告美国智慧电錶市场规模、份额、趋势分析报告:按组件、类型、技术、最终用途、细分市场预测,2025 年至 2033 年智慧电錶市场规模、份额、趋势分析报告:按组件、类型、技术、最终用途、地区、细分市场预测,2025-2030 年

2025年电网现代化全球市场报告美国智慧电錶市场规模、份额、趋势分析报告:按组件、类型、技术、最终用途、细分市场预测,2025 年至 2033 年智慧电錶市场规模、份额、趋势分析报告:按组件、类型、技术、最终用途、地区、细分市场预测,2025-2030 年 日本智慧电錶市场报告(按产品(智慧电錶、智慧水錶、智慧瓦斯表)、技术、最终用途(住宅、商业、工业)和地区)2025-2033 年2025 年至 2033 年智慧电錶市场规模、份额、趋势及预测(依产品、技术、最终用途及地区)

日本智慧电錶市场报告(按产品(智慧电錶、智慧水錶、智慧瓦斯表)、技术、最终用途(住宅、商业、工业)和地区)2025-2033 年2025 年至 2033 年智慧电錶市场规模、份额、趋势及预测(依产品、技术、最终用途及地区)