|

市场调查报告书

商品编码

1686664

非洲农业机械:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Africa Agricultural Machinery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

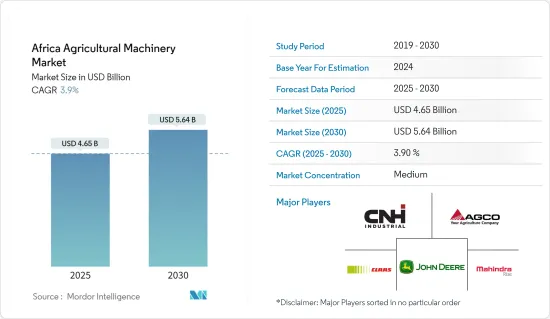

预计 2025 年非洲农业机械市场规模为 46.5 亿美元,到 2030 年将达到 56.4 亿美元,预测期内(2025-2030 年)的复合年增长率为 3.9%。

主要亮点

- 受非洲大陆农业方法现代化推动,非洲农业机械市场正稳步扩大。此次现代化旨在提高生产力和应对紧迫的粮食安全挑战。例如,根据联合国非洲经济委员会的数据,非洲人口预计将成长五倍以上,从 1960 年的 2.83 亿增加到 2023 年的 15 亿以上,然后再成长 9.5 亿,到 2050 年达到 25 亿。这种增长增加了对粮食的需求,而现代机械是提高作物产量和满足日益增长的需求的重要解决方案。

- 在南非,商业农民在农业领域发挥关键作用。根据威斯康辛州经济发展公司最近的一份报告,约有 32,000 个商业农场生产了该州 80% 的农业产值。这些农民将机械化视为增加利润和确保经营永续性的基石。这种观点着市场的成长轨迹征兆一片光明。南非农业机械协会 (SAAMA) 预计 2022 年拖拉机销量约为 9,181 台,联合收割机销量约为 373 台,这表明该国在农业机械化方面正在稳步前进。

- 在衣索比亚,大多数农民耕种小块土地,大规模机械化仍然很少见,但政府正在积极推动农业和机械产业的成长。埃塞俄比亚的旗舰计画之一「成长与转型计画 II」(GTP II)旨在振兴这些产业。该计画的一项关键策略是将大片可耕地租给国际公司,为大规模商业化农业铺路。此举不仅加强了设备的销售,也有助于扩大衣索比亚农业机械市场。在政府支持和大公司不断增加的投资下,该地区的农业机械化正在强劲增长。

非洲农业机械市场趋势

按产品类型划分,拖拉机是主要细分市场

农业对非洲经济发展至关重要。非洲儘管拥有世界上最多的未开垦耕地,但其农业生产力却落后于其他开发中地区。目前非洲农作物产量仅为世界平均的56%。为了满足人口增长和快速都市化带来的日益增长的粮食需求,非洲必须在未来几十年提高作物产量。机械化,特别是基于拖拉机的机械化,为缩小产量差距提供了可行的解决方案。

在非洲,拖拉机是农活中不可或缺的工具,帮助人们完成从耕作到播种到收割的一切工作。农业进化联盟的研究强调了非洲农业机械的巨大潜力,其中拖拉机占据主导地位。预计政府的支持将促进该行业的发展。例如,加纳政府向经营89家拖拉机租赁和维护中心的企业家提供拖拉机补贴。

近年来,拖拉机的流行趋势不断上升。根据南非农业机械协会(SAAMA)的报告,南非拖拉机销量从 2021 年的 7,680 台增加到 2022 年的 9,181 台。在小规模农户占多数的非洲,100匹马力以下的小型拖拉机是常态。製造商正在定制适合非洲需求的车型,优先考虑经济性、耐用性和易于维护性。在非洲分散的土地上,中小型拖拉机比更大、更昂贵的机器更受欢迎。

2021年,欧洲农业机械工业协会(CEMA)与联合国粮食及农业组织(FAO)将《永续农业机械化谅解备忘录》延长至2025年。新协议强调了自动化和智慧化农业机械、精密农业、数位资料管理和农业机械利用率的准确资料的重要性,特别是在非洲国家。这些努力可能会刺激包括拖拉机在内的农业机械市场的成长。

南非占市场主导地位

在非洲国家中,南非是最大的市场。从历史上看,南非的农业经济已从依赖粮食援助转变为注重国内生产。南非目前农业和农机市场具有巨大的成长潜力。

此外,南非是撒哈拉以南非洲最大的谷物生产国。产量以玉米为主,其次是小麦、大豆和葵花籽。根据粮农组织统计资料库,2022年南非谷物总产量将达1,870万吨,其中玉米约占1,610万吨。强劲的生产水准正在刺激机械化程度的提高和对最先进农业设备的投资。此外,南非的机械化率超过非洲大陆的其他国家,拖拉机普及率显着,收割机、播种机和灌溉系统的使用也十分广泛。高度的机械化使南非农民变得更有效率和更有生产力。人事费用,特别是大规模作物种植的成本,超过许多其他非洲国家。

由于有约翰迪尔、马恆达、爱科集团等多家跨国公司的存在,其产品很容易进入南非市场。 2022 年,约翰迪尔在 2022 年南浦收穫日推出了 X9 系列联合收割机。从那时起,这款全新 11 级联合收割机抵达南非海岸,其惊人的工作能力和性能引起了广泛关注。

非洲农机产业概况

非洲农机市场相对集中。市场的主要企业包括 Deere &Company、AGCO Corporation、CNH Industrial NV、Mahindra &Mahindra Ltd、Claas KGaA mbH 等。为了保持其在市场中的地位,主要企业正在扩大产品系列併扩大其业务范围。透过向市场推出创新的新产品来扩大产品系列是这些公司最常采用的策略。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场动态

- 市场概况

- 市场驱动因素

- 农业劳动力减少

- 不断提高的技术进步

- 加大政府对加强农业机械化的支持

- 市场限制

- 农业支出增加

- 现代农业机械的安全问题

- 波特五力分析

- 新进入者的威胁

- 购买者/消费者的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争强度

第五章 市场区隔

- 产品类型

- 联结机

- 耕作及栽培机械

- 播种施肥机

- 收割机

- 牧草和饲料机械

- 灌溉机械

- 其他产品类型

- 地区

- 南非

- 其他非洲地区

第六章 竞争格局

- 最受欢迎的策略

- 市场占有率分析

- 公司简介

- Tractors and Farm Equipment Limited(TAFE)

- Claas KGaA mbH

- AGCO Corporation

- Mahindra & Mahindra Ltd

- Deere & Company

- CNH Industrial NV

第七章 市场机会与未来趋势

The Africa Agricultural Machinery Market size is estimated at USD 4.65 billion in 2025, and is expected to reach USD 5.64 billion by 2030, at a CAGR of 3.9% during the forecast period (2025-2030).

Key Highlights

- Africa's agriculture machinery market is steadily expanding, fueled by the continent's push to modernize farming practices. This modernization aims to enhance productivity and tackle pressing food security challenges. For instance, according to the United Nations Economic Commission for Africa, its population expanded from 283 million in 1960 to more than 1.5 billion in 2023 - a more than five-fold increase-and is projected to increase by 950 million and touch 2.5 billion by 2050. Such growth amplifies the demand for food, and modern machinery stands as a pivotal solution to boost crop yields and meet this escalating demand.

- In South Africa, commercial farmers play a crucial role in the agricultural sector. Recently, according to the Wisconsin Economic Development Corporation, approximately 32,000 commercial farmers produce 80% of the country's agricultural value. These farmers view mechanization as a cornerstone for enhancing profits and ensuring the sustainability of their operations. This perspective bodes well for the market's growth trajectory. The South African Agricultural Machinery Association (SAAMA) has sales of about 9,181 tractors and 373 combined harvesters for 2022, underscoring the nation's steady march towards agricultural mechanization.

- In Ethiopia, while most farmers operate on small landholdings and large-scale mechanization remains rare, the government is actively promoting growth in both agriculture and the machinery sector. One of its flagship initiatives, the Growth and Transformation Plan (GTP II), aims to invigorate these sectors. A key strategy under this plan involves leasing vast arable lands to international entities, paving the way for large-scale commercial farming. This move is not only bolstering equipment sales but also propelling the agricultural machinery market's expansion in Ethiopia. With government backing and heightened investments from major players, the region witnesses robust growth in agricultural mechanization.

Africa Agricultural Machinery Market Trends

Tractors is the Significant Segment by Product Type

Agriculture is pivotal to Africa's economic development. Despite boasting the world's largest expanse of uncultivated arable land, Africa's agricultural productivity lags behind other developing regions. Current crop yields in Africa stand at just 56% of the global average. To meet the rising food demand spurred by population growth and swift urbanization, Africa must boost its crop yields in the coming decades. Mechanization, particularly through tractors, presents a viable solution to bridge this yield gap.

In Africa, tractors are indispensable, facilitating everything from plowing and tilling to planting and harvesting. Research by Agri Evolution Alliance underscores the vast potential for agricultural machinery in Africa, with tractors leading the charge. Government support is anticipated to drive sector development. For instance, the Ghanaian government provides subsidized tractors to entrepreneurs operating 89 centers for tractor rental and servicing.

Tractor sales have shown an upward trend in recent years. The South African Agricultural Machinery Association (SAAMA) reports that tractor sales in South Africa increased from 7,680 units in 2021 to 9,181 units in 2022. Given Africa's predominant smallholder farms, compact tractors, typically under 100 HP, reign supreme. Manufacturers are tailoring models to suit African needs-prioritizing affordability, durability, and ease of maintenance. In Africa's fragmented land holdings, small and medium-sized tractors shine, as opposed to larger, costlier machinery.

In 2021, the European Agricultural Machinery Industry Association (CEMA) and the Food and Agriculture Organization of the United Nations (FAO) extended their memorandum of understanding (MoU) on sustainable agricultural mechanization until 2025. This renewed agreement emphasizes the importance of automated and intelligent agricultural machinery, precision agriculture, digital data management, and accurate statistical data on agricultural machinery use, particularly in African countries. These initiatives are likely to stimulate growth in the agricultural machinery including tractor market.

South Africa Dominates the Market

Among African nations, South Africa stands out as the largest market. Historically, the South African agricultural economy transitioned from relying on food aid to emphasizing domestic production, a shift initiated by the Green Revolution, championed by the World Food Program of the United Nations. South Africa now has major potential for the growth of the agriculture and agriculture machinery market.

Moreover, South Africa holds the title of the leading cereal producer in Sub-Saharan Africa. Maize dominates its production, trailed by wheat, soybeans, and sunflower seeds. According to the FAOSTAT, the total cereal production in South Africa reached 18.7 million metric tons in 2022, with maize accounting for approximately 16.1 million metric tons. Such robust production levels have spurred a push towards mechanization and investments in cutting-edge agricultural equipment. Additionally, South Africa outpaces its continental counterparts in mechanization rates, showcasing notable tractor penetration and the prevalent use of harvesters, planters, and irrigation systems. This advanced mechanization empowers South African farmers to boost efficiency and productivity, particularly in large-scale crop farming, where labor costs surpass those in many other African nations.

The presence of several global companies, like John Deere, Mahindra, and AGCO Corporation, may enable the easy introduction of products in the South African market. In 2022, John Deere launched X9 Series combine harvesters at NAMPO Harvest Day 2022. It has since created a massive buzz around the incredible operational capacity and performance of the all-new class 11 Combine to arrive on South African shores.

Africa Agricultural Machinery Industry Overview

The African agricultural machinery market is relatively consolidated. The major players in the market include Deere & Company, AGCO Corporation, CNH Industrial NV, Mahindra & Mahindra Ltd, and Claas KGaA mbH. Major players in the market have extended their product portfolio and broadened their businesses to maintain their positions in the market. Expanding the product portfolio by introducing new and innovative products into the market is the most adopted strategy by these companies.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Declining Agricultural Labor

- 4.2.2 Rising Technological Advancements

- 4.2.3 Growing Government Support to Enhance Farm Mechanization

- 4.3 Market Restraints

- 4.3.1 Increasing Farm Expenditure

- 4.3.2 Security Concerns in Modern farming Machinery

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Product Type

- 5.1.1 Tractors

- 5.1.2 Plowing and Cultivating Machinery

- 5.1.3 Planting and Fertilizing Machinery

- 5.1.4 Harvesting Machinery

- 5.1.5 Haying and Forage Machinery

- 5.1.6 Irrigation Machineries

- 5.1.7 Other Product Types

- 5.2 Geography

- 5.2.1 South Africa

- 5.2.2 Rest of Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Most Adopted Strategies

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 Tractors and Farm Equipment Limited (TAFE)

- 6.3.2 Claas KGaA mbH

- 6.3.3 AGCO Corporation

- 6.3.4 Mahindra & Mahindra Ltd

- 6.3.5 Deere & Company

- 6.3.6 CNH Industrial NV

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

除草机器人市场:按组件、类型、运作方式、销售管道、应用和最终用途划分-2026-2032年全球市场预测农作物残渣处理机械市场:按类型、机械化程度、动力来源、应用、最终用途和分销管道划分-2026-2032年全球市场预测

除草机器人市场:按组件、类型、运作方式、销售管道、应用和最终用途划分-2026-2032年全球市场预测农作物残渣处理机械市场:按类型、机械化程度、动力来源、应用、最终用途和分销管道划分-2026-2032年全球市场预测 2026年全球自主作物残茬管理机器人市场报告农业橡胶履带市场:2026-2032年全球市场预测(依应用程式、销售管道、履带宽度、橡胶配方类型、履带长度及最终用户类型划分)

2026年全球自主作物残茬管理机器人市场报告农业橡胶履带市场:2026-2032年全球市场预测(依应用程式、销售管道、履带宽度、橡胶配方类型、履带长度及最终用户类型划分) 自主农业车辆市场:策略性洞察与预测(2026-2031年)全球农业机械市场规模、份额、趋势和成长分析报告(2026-2034年)溶离设备市场:2026-2032年全球市场预测(依设备类型、自动化程度、技术、应用、最终用户及销售管道)农业和施工机械市场:按产品类型、功率范围、发动机类型、应用、最终用户和分销管道划分——2026-2032年全球预测谷物螺旋输送机市场:按类型、动力来源、容量、应用、最终用户和分销管道划分-2026-2032年全球预测红外线沥青加热器市场:按产品类型、电源、移动性、应用、最终用户、分销管道划分,全球预测(2026-2032年)

自主农业车辆市场:策略性洞察与预测(2026-2031年)全球农业机械市场规模、份额、趋势和成长分析报告(2026-2034年)溶离设备市场:2026-2032年全球市场预测(依设备类型、自动化程度、技术、应用、最终用户及销售管道)农业和施工机械市场:按产品类型、功率范围、发动机类型、应用、最终用户和分销管道划分——2026-2032年全球预测谷物螺旋输送机市场:按类型、动力来源、容量、应用、最终用户和分销管道划分-2026-2032年全球预测红外线沥青加热器市场:按产品类型、电源、移动性、应用、最终用户、分销管道划分,全球预测(2026-2032年)