|

市场调查报告书

商品编码

1687098

义大利太阳能:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)Italy Solar Energy - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

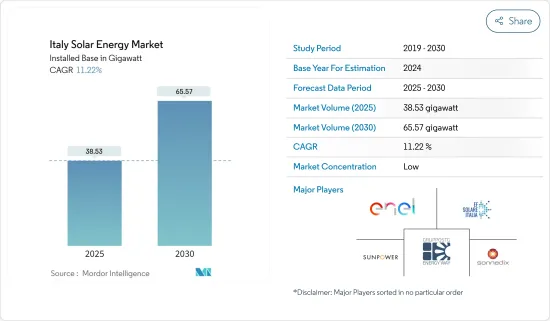

义大利太阳能市场规模(安装基数)预计将从 2025 年的 38.53 GW 成长到 2030 年的 65.57 GW,预测期内(2025-2030 年)的复合年增长率为 11.22%。

主要亮点

- 从中期来看,政府鼓励可再生能源发电的支持政策和太阳能光电设备成本的下降预计将成为预测期内推动义大利太阳能发电市场发展的因素之一。

- 然而,预计在预测期内,风能等替代再生能源来源的采用越来越多、电网基础设施和能源储存系统有限将阻碍市场的成长。

- 然而,预计未来海上太阳能设施将为市场参与者提供充足的机会。

义大利太阳能市场趋势

太阳能光伏 (PV) 领域占据市场主导地位

- 光伏(PV)是含有光伏材料的电池阵列,可将太阳的辐射或能量转换为直流电。它们之所以昂贵,是因为它们由各种半导体(通常是硅)和高导电性电线组成,以减少电流损耗。但由于营运成本较低,预计未来几年成本将进一步下降。

- 由于政府推出优惠措施推动太阳能发电应用,併网太阳能市场的成长也可能加速。例如,义大利政府于 2022 年初在其 DL Energia 法令中引入了新规定,以降低家庭和企业的能源费用。义大利企业已经能够获得计划回扣,几个南部地区也获得了屋顶太阳能光电和能源效率的财政措施。

- 政府宣布的新规包括大幅简化安装容量在50kW至200kW之间的商业屋顶太阳能发电系统的许可。在义大利,这些系统被允许在该国被称为「Scambio sul posto」的净计量製度下运作。

- 2022年5月,欧盟委员会宣布,将强制要求2027年在商业和公共建筑屋顶安装太阳能光电,2029年在住宅建筑屋顶安装太阳能光电。此外,欧盟的可再生能源目标从40%提高到45%。预计这些规定将在未来几年内提升义大利併网太阳能光电市场的渗透率。

- 义大利政府也计划大幅提高装置容量至60GW左右,到2030年终生产超过72TWh至74TWh的电力。 2023年初,义大利能源和环境部宣布,其目标是到2030年增加至少70GW的可再生能源容量。这些目标预计将推动新太阳能发电厂,特别是公用事业规模太阳能发电厂的部署大幅成长。

- 根据国际可再生能源机构 (IRENA) 的数据,2022 年太阳能装置容量较 2021 年成长了 10.97%。在预测期内,未来几年这一数字可能会增加。

- 因此,在政府优惠政策的支持下,随着太阳能发电的持续发展和装置容量的不断增加,预计预测期内太阳能发电将占据市场主导地位。

即将实施的计划和政府政策预计将推动市场

- 义大利是世界领先的太阳能消费国之一,也是全球太阳能发电容量扩张的主要贡献者。该国的太阳能新增装置容量市场是世界上最大的市场之一。在欧盟内部,义大利的太阳能产业仅次于德国。

- 义大利政府推广太阳能的原因有几个。首先,它致力于减少对石化燃料的依赖,增加可再生在能源结构中的比重。这符合义大利的国家能源和气候计划,该计划的目标是到 2030 年实现可再生能源在最终能源消费量总量中的占比达到 45%。

- 2023年2月,义大利能源和环境部宣布,政府计画在2030年为国家电网增加至少70吉瓦的可再生能源容量。为了实现这一目标,政府正在起草一项法令,加快可再生能源计划的许可程序。

- 例如,2022年3月,义大利政府在DL Energia法令中宣布了一揽子新措施。新规定显着简化了安装容量在 50kW 至 200kW 之间的商业屋顶太阳能光电(PV)系统的许可流程。这些系统有资格参与义大利的净计量计划,即「Scambio sul posto」。

- 根据国际可再生能源机构(IRENA)的数据,2022 年可再生能源容量较 2021 年成长了 5.33%。这一增长归因于过去一年该地区新计画的启动和政府实施的支持政策。在预测期内和未来几年,这一数字可能还会增加。

- 根据环境与能源安全部发布的《2021年国家能源状况与年度数据关係》报告,经过7年的抑製成长,太阳能市场新增容量为21吉瓦(+3%)。义大利表现出最强劲的趋势,成长了 83%,这得益于超级奖金计画提供的优惠待遇。

- 义大利政府的这些措施也反映在太阳能发电量的大幅增加。例如,2022年太阳能发电总量为27.55吉瓦时,较2016年成长逾24.6%。此外,计划在2030年引入超过7,000万千瓦可再生能源,未来太阳能的引入预计还会进一步增加。

- 因此,由于雄心勃勃的可再生能源目标和政府的支持性倡议,如税额扣抵、净计量和对太阳能领域的投资,预计太阳能市场在预测期内将大幅增长。

义大利太阳能产业概况

义大利太阳能市场比较分散。主要企业包括(不分先后顺序):Gruppo STG SRL、Sonnedix Power Holdings Ltd、EF Solare Italia SpA、SunPower Corporation 和 Enel SpA。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究范围

- 市场定义

- 调查前提

第二章调查方法

第三章执行摘要

第四章 市场概况

- 最新趋势和发展

- 政府法规和政策

- 市场动态

- 驱动程式

- 降低安装太阳能发电的成本

- 政府对可再生能源的支持政策

- 限制因素

- 其他能源来源的普及

- 驱动程式

- 供应链分析

- PESTLE分析

第五章 市场区隔

- 类型

- 光伏(PV)

- 聚光型太阳光电(CSP)

- 最终用户

- 住宅

- 工业和商业

- 实用规模

- 扩张

- 屋顶

- 地面安装

第六章 竞争格局

- 併购、合资、合作、协议

- 主要企业策略

- 公司简介

- Gruppo STG SRL

- Sonnedix Power Holdings Ltd

- SunPower Corporation

- SunEdison Inc.

- Enel SpA

- Peimar SRL

- EF Solare Italia SpA

- 市场排名分析

第七章 市场机会与未来趋势

- 适合安装太阳能设备的近海区域

简介目录

Product Code: 55026

The Italy Solar Energy Market size in terms of installed base is expected to grow from 38.53 gigawatt in 2025 to 65.57 gigawatt by 2030, at a CAGR of 11.22% during the forecast period (2025-2030).

Key Highlights

- Over the medium period, supportive government policies to promote renewable power generation and the declining cost of Solar PV installations are expected to be some of the driving factors for the solar energy market in Italy during the forecast period.

- On the other hand, the increasing adoption of alternate renewable sources such as wind and limited grid infrastructure and storage systems are expected to hinder the market growth during the forecast period.

- Nevertheless, offshore areas for solar installation are expected to provide ample opportunities for market players in the future.

Italy Solar Energy Market Trends

Solar Photovoltaic (PV) Segment to Dominate the Market

- Photovoltaics (PVs) are arrays of cells containing solar photovoltaic material that converts radiation or energy from the sun into direct current electricity. They consist of various semiconductors, usually silicon, and highly conductive wire to reduce any current loss, making them expensive. However, low operational costs are expected to further lower the costs in the coming years.

- The growth of the on-grid solar PV market is also likely to accelerate due to the government's favorable initiatives to boost its adoption. For instance, in early 2022, the Italian government launched new provisions in the DL Energia decree to decrease energy bills for households and businesses. Italian companies can now secure project rebates, and several southern regions have also been granted a fiscal break for rooftop solar PV and energy efficiency.

- The new provisions published by the government include an extreme simplification of permits to install commercial rooftop PV systems with a capacity of between 50 kW and 200 kW. In Italy, these systems are allowed to operate under the country's net metering scheme, known as Scambio sul posto.

- In May 2022, the European Commission announced a mandate for rooftop solar on commercial and public buildings by 2027 and for residential buildings by 2029. In addition, the EU target for renewable energy increased from 40% to 45%. Such mandates are anticipated to push the adoption of Italy's on-grid solar PV market in the coming years.

- The Italian government has also planned to significantly increase the installed solar PV capacity by up to about 60 GW to produce more than 72 TWh to 74 TWh of electricity by the end of 2030. In early 2023, the Italian Energy and Environment Ministry announced that it aims to add at least 70 GW of renewable energy capacity by 2030. These targets are expected to result in significant growth in deploying new solar PV plants, especially utility-scale sized PV plants.

- According to the International Renewable Energy Agency (IRENA), in 2022, the Solar Energy Installed Capacity increased by 10.97 % compared to 2021; the increase is due to new projects started in the past year. This number is likely to increase in the upcoming years during the forecast period.

- Thus, with such ongoing developments and capacity additions supported by favorable government policies, the solar PV segment is expected to dominate the market during the forecast period.

Upcoming Projects and Government Policies Expected to Drive the Market

- Italy is a prominent consumer of solar electricity worldwide and a significant contributor to the growth of solar energy capacity worldwide. The country's market for solar energy capacity additions is one of the largest globally. Within the European Union, Italy is ranked second, just behind Germany, in terms of its photovoltaic sector.

- The Italian government is promoting solar energy for several reasons. Firstly, it is committed to reducing the country's dependence on fossil fuels and increasing its share of renewable energy in the energy mix. This aligns with Italy's national energy and climate plans, which aim to achieve a 45% share of renewable energy in gross final energy consumption by 2030.

- In February 2023, the Energy and Environment Ministry of Italy announced that the government plans to add a minimum of 70 GW of renewable energy capacity to the national grid by 2030. To achieve this goal, the government is developing a decree to expedite the permit process for renewable energy projects.

- For instance, in March 2022, the Italian government released a new package of measures in the DL Energia decree. One of the new provisions includes a significant simplification of the permit process for installing commercial rooftop photovoltaic (PV) systems with a capacity ranging from 50 kW to 200 kW. These systems are eligible to participate in Italy's net metering scheme, which is known as the "Scambio sul posto."

- According to the International Renewable Energy Agency (IRENA), in 2022, the Renewable Energy Capacity increased by 5.33 % compared to 2021; the increase is due to new projects started and Supportive Government Policies implemented in the region during the past year. This number is likely to increase in the upcoming years during the forecast period.

- According to the Relazione annuale situazione energetica nazionale dati 2021, a report published by the Ministry of Environment and Energy Security in 2021, after seven years of reduced growth, there was an increase (+3%) in the solar energy market with 21 GW of additional capacity. Italy witnessed the greatest trend, with an increase of 83%, owing to the incentives provided by the super bonus mechanism.

- These actions from the Italian government have also been reflected in a significant increase in electricity generation through solar energy sources. For instance, in 2022, the total electricity generation through solar energy was recorded at 27.55 GWh, which was an increase of more than 24.6% compared to 2016. Furthermore, with plans to install more than 70 GW of renewable energy by 2030, the installation of solar energy is further expected to increase in the future.

- Therefore, the solar energy market is expected to grow significantly during the forecast period, owing to the ambitious renewable energy targets and supportive government initiatives, such as tax credits, net metering, and investments in solar energy sectors.

Italy Solar Energy Industry Overview

The Italian solar energy market is fragmented. Some of the major companies include Gruppo STG SRL, Sonnedix Power Holdings Ltd, EF Solare Italia SpA, SunPower Corporation, and Enel SpA (in no particular order).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definiton

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Recent Trends and Developments

- 4.2 Government Policies and Regulations

- 4.3 Market Dynamics

- 4.3.1 Drivers

- 4.3.1.1 Declining Cost of Solar PV Installations

- 4.3.1.2 Supportive Government Policies For Renewable Energy

- 4.3.2 Restraints

- 4.3.2.1 Penetration of Other Energy Sources

- 4.3.1 Drivers

- 4.4 Supply Chain Analysis

- 4.5 PESTLE Analysis

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Solar Photovoltaic (PV)

- 5.1.2 Concentrated Solar Power (CSP)

- 5.2 End-user

- 5.2.1 Residential

- 5.2.2 Industrial and Commercial

- 5.2.3 Utility-Scale

- 5.3 Deployment

- 5.3.1 Rooftop

- 5.3.2 Ground-mounted

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Gruppo STG SRL

- 6.3.2 Sonnedix Power Holdings Ltd

- 6.3.3 SunPower Corporation

- 6.3.4 SunEdison Inc.

- 6.3.5 Enel SpA

- 6.3.6 Peimar SRL

- 6.3.7 EF Solare Italia SpA

- 6.4 Market Ranking Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Offshore Areas for Solar Installation

02-2729-4219

+886-2-2729-4219

太阳能係统市场(按产品类型、系统规模、安装类型和最终用途应用)—2025-2032 年全球预测

太阳能係统市场(按产品类型、系统规模、安装类型和最终用途应用)—2025-2032 年全球预测 太阳能设备的全球市场(2025年):产品,终端用户竞争:分析,预测,机会

太阳能设备的全球市场(2025年):产品,终端用户竞争:分析,预测,机会 2025年併网太阳能市场报告太阳能 EPC(工程、采购和施工)市场(按服务类型、太阳能技术、追踪器类型、容量、安装类型和最终用途)—2025-2030 年全球预测太阳能电池电镀线市场(按电池技术、电镀工艺类型、电镀材质、材料类型和应用)—2025-2030 年全球预测

2025年併网太阳能市场报告太阳能 EPC(工程、采购和施工)市场(按服务类型、太阳能技术、追踪器类型、容量、安装类型和最终用途)—2025-2030 年全球预测太阳能电池电镀线市场(按电池技术、电镀工艺类型、电镀材质、材料类型和应用)—2025-2030 年全球预测 全球太阳能板监控系统市场

全球太阳能板监控系统市场 太阳能光伏发电的全球市场的展望:2025年第3季 - 资料全球商业和工业太阳能光电模组市场2025年全球太阳能市场报告Sunspring Systems 的全球市场

太阳能光伏发电的全球市场的展望:2025年第3季 - 资料全球商业和工业太阳能光电模组市场2025年全球太阳能市场报告Sunspring Systems 的全球市场

▼