|

市场调查报告书

商品编码

1907324

欧洲发泡聚苯乙烯(EPS)市场份额分析、产业趋势、统计和成长预测(2026-2031)Europe Expanded Polystyrene (EPS) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

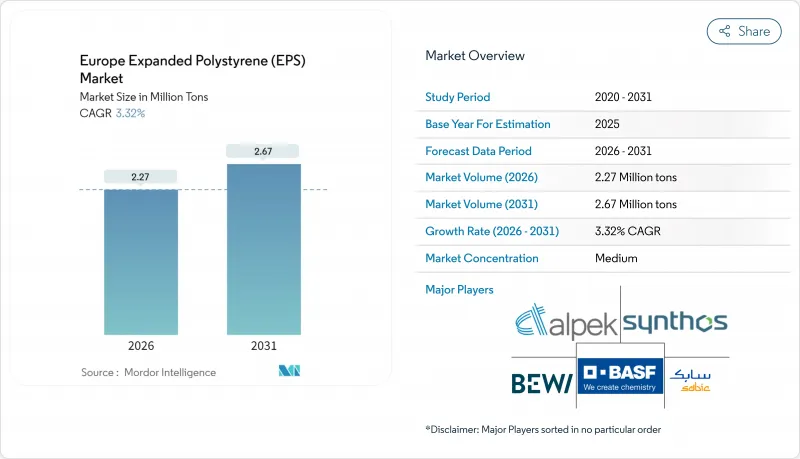

2025年欧洲发泡聚苯乙烯(EPS)市场价值为220万吨,预计2031年将达到267万吨,高于2026年的227万吨。

预计在预测期(2026-2031 年)内,复合年增长率将达到 3.32%。

需求主要由建筑保温维修和精密设备的防护包装驱动,强大的国内供应链、不断提高的回收率以及技术创新带来的碳排放减少,都增强了产业的韧性。欧盟《建筑能源性能指令》(将于2025年生效)等监管因素将强制要求新建和维修建筑提高隔热性能(R值),从而在替代材料份额不断增长的情况下,保持隔热材料需求的稳定。同时,mRNA生物製剂物流的激增和家用电器生产回流将支撑包装需求,缓衝苯乙烯价格波动对大宗商品利润率的影响。然而,欧洲发泡聚苯乙烯市场仍需应对许多挑战,例如原材料价格波动风险增加、人口密集都市区消防安全法规以及客户对纸基、纸浆基和菌丝基替代品的测试。

欧洲发泡聚苯乙烯(EPS)市场趋势与洞察

建筑能效标准决定了隔热性能要求。

更严格的国家和欧盟能源标准迫使开发商设计更低的墙体、屋顶和地板的U值,提高了隔热材料厚度要求,并支撑了欧洲市场对EPS保温解决方案的稳定需求。德国《建筑能源法》(Gebaudeenergiegesetz)规定外墙的U值约为0.20 W/(m²K),这通常需要12-16公分厚的EPS隔热材料。儘管存在基于高度的防火限制,但这仍然有助于发泡聚苯乙烯在德国外墙系统中保持了约40%的市场份额。法国和北欧国家也正在扩大类似的性能要求,计划于2024年实施的修订版《建筑能源性能指令》将透过对2030年及以后新建建筑强制执行净零能耗标准,锁定长期的隔热材料需求。欧盟的维修计画「翻新浪潮」(Renovation Wave)也推动了维修需求的成长,该计画透过补贴鼓励住宅选择更有效率、更经济的系统。为了应对这一监管趋势,製造商正在扩大其 Neopor 和石墨增强产品线,以在不进行昂贵的结构改造的情况下提供卓越的绝缘性能(R 值)。

扩大mRNA生物製剂的低温运输

mRNA疫苗和先进疗法的快速商业化要求从工厂到临床的运输温度保持在2°C至8°C之间。 EPS(聚苯乙烯泡沫塑胶)运输容器是该领域的主流选择,因为其闭孔结构能够为长途和最后一公里配送提供可预测的隔热和缓衝性能。像Cold Chain Technologies这样的製造商已在荷兰布雷达建立了新的欧洲生产基地,专门针对覆盖欧盟80%核心GDP且位于六小时车程范围内的药品分销网络。欧洲药典补充11.7的日益严格的法规迫使包装供应商对可萃取物和可浸出物进行检验,这使得具有良好合规记录的现有EPS配方更受青睐。低温运输市场盈利丰厚,部分抵销了苯乙烯价格波动对建筑发泡材市场的影响。

原材料成本波动会对利润率造成压力。

苯乙烯占EPS现金成本的70%之多,因此盈利极易受到苯和石脑油价格波动的影响。 Trinseo宣布将其2025年1月合约的价格上调55欧元/吨,显示生产商正试图捍卫其利润率。 Versalis将于2025年4月关闭其位于布林迪西的裂解装置,这将加剧结构性压力,增加该地区对进口的依赖,并放大运费和外汇风险。原材料成本的波动与固定价格的建设合约之间的不匹配正在挤压转化装置的现金流,并给西北欧各地的小规模装置带来挑战。

细分市场分析

欧洲白色发泡聚苯乙烯(EPS)市场占总消费量的70.86%。白色EPS继续用于中空墙、楼板式楼板和周边排水板,在这些应用中,成本仍然是关键的选择标准,并且需要足够薄的厚度以满足监管标准。然而,预计黑色和银色EPS将最快成长,到2031年复合年增长率将达到3.74%。这主要归功于黑色EPS中含有红外线反射石墨颗粒,这些颗粒可将导热係数(λ值)降低至约0.030 W/(m·K)。在外部保温复合系统中,黑色EPS可以将层厚从16厘米减少到12厘米,同时保持相同的保温性能(U值),从而实现空间有限的都市区的建筑幕墙维修。 BEWI的CIRCULUM产品系列将性能优势与再生珠粒含量结合,帮助建筑师平衡节能和循环经济的目标。製造商正在投资在线连续发泡回收技术和连续块状成型技术,以提高回收成分含量,同时又不影响机械性能。灰色 EPS 在欧洲发泡聚苯乙烯市场被定位为一种可以提高技术和环境价值的产品。

欧洲发泡聚苯乙烯(EPS)市场报告按产品类型(白色EPS、灰色和银色EPS)、终端用户产业(建筑与施工、电气与电子、包装及其他终端用户产业)和地区(德国、英国、法国、义大利、西班牙、挪威、瑞典、丹麦、芬兰及其他欧洲地区)进行细分。市场预测以吨为单位。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 到2025年,建筑节能标准将要求更高的隔热性能(R值)。

- 提高基于mRNA的生技药品的关键低温运输能力

- 家用电器重返日本市场提振了国内对防护包装的需求

- 欧盟「维修新浪潮」维修计划中灰色EPS的应用

- 低成本模组化住宅计划

- 市场限制

- 苯乙烯单体价格波动与原油价差相关

- 菌丝体和模塑纸浆替代品的商业化。

- 碳定价会加剧石油基聚合物的范围3排放。

- 价值链分析

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

- 进出口趋势

第五章 市场规模与成长预测

- 依产品类型

- 白色 EPS

- 灰色和银色 EPS

- 按最终用户行业划分

- 建筑/施工

- 电气和电子设备

- 包装

- 其他终端用户产业(农业和汽车)

- 按地区

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 挪威

- 瑞典

- 丹麦

- 芬兰

- 其他欧洲地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率(%)/排名分析

- 公司简介

- Alpek SAB de CV

- Austrotherm

- BASF

- BEWi

- Epsilyte LLC

- Ineos

- Kaneka Corporation

- Ravago

- SABIC

- SIBUR International GmbH

- Sunde Group

- Sunpor

- Synthos

- TotalEnergies

- Versalis SpA

第七章 市场机会与未来展望

The Europe Expanded Polystyrene Market was valued at 2.20 million tons in 2025 and estimated to grow from 2.27 million tons in 2026 to reach 2.67 million tons by 2031, at a CAGR of 3.32% during the forecast period (2026-2031).

Demand flows primarily from building insulation upgrades and protective packaging for sensitive goods, while sector resilience is reinforced by robust domestic supply chains, incremental recycling gains, and technology upgrades that lower embodied carbon footprints. Regulatory drivers such as the EU Energy Performance of Buildings Directive, effective from 2025, compel higher R-values across new builds and retrofits, keeping insulation volumes stable even as substitutes gain share. Simultaneously, the surge in mRNA biologic logistics and appliance reshoring sustains packaging volumes, helping buffer commodity segments against margin compression from styrene volatility. Nevertheless, the Europe Expanded Polystyrene market negotiates mounting headline risk tied to feedstock price swings, fire-safety regulations in dense urban cores, and customer trials of paper-, pulp-, and mycelium-based alternatives.

Europe Expanded Polystyrene (EPS) Market Trends and Insights

Building Energy Codes Drive Thermal Performance Requirements

Stricter national and EU-wide energy codes compel developers to design walls, roofs, and floors with lower U-values, lifting insulation thickness requirements and supporting steady volume demand for Europe's Expanded Polystyrene market solutions. Germany's Gebaudeenergiegesetz already specifies exterior wall U-values near 0.20 W/(m2K), which typically necessitates 12-16 cm of EPS, cementing roughly 40% share for the foam in German facade systems despite height-based fire-safety limits. France and the Nordics extend similar performance stipulations, and the 2024 recast of the Energy Performance of Buildings Directive sets a net-zero mandate for new structures from 2030, locking in long-range insulation demand. Retrofit volumes also rise under the EU Renovation Wave, with grants steering homeowners toward thermally efficient yet affordable systems. Producers broaden their Neopor and graphite-enriched lines in this compliance-driven landscape to deliver superior R-values without costly structural modifications.

mRNA Biologics Cold Chain Expansion

Rapid commercialization of mRNA vaccines and advanced therapeutics requires 2 °C-to-8 °C stability from factory to clinic. EPS shippers dominate this lane because the material's closed-cell matrix provides predictable insulation and cushioning over long-haul flights and last-mile parcels. Manufacturers such as Cold Chain Technologies have added European capacity in Breda, Netherlands, specifically to serve pharma corridors reaching 80% of EU GDP centers within a six-hour drive. Regulatory tightening under European Pharmacopoeia Supplement 11.7 pushes packaging suppliers to validate extractables and leachables, favoring incumbent EPS formulations with proven compliance records. The cold-chain opportunity carries premium margins that partially offset styrene spread volatility in commodity construction foam.

Feedstock Cost Volatility Pressures Margins

Styrene accounts for up to 70% of EPS cash costs, making profitability sensitive to benzene-and naphtha swings. January 2025 contract hikes of EUR 55 per ton announced by Trinseo illustrate producer attempts to defend margins. Structural tightness deepens as Versalis shutters its Brindisi cracker in April 2025, widening the region's import dependency and magnifying freight and currency risks. The mismatch between volatile raw-material outlays and fixed-price construction contracts squeezes converter cash flows, challenging smaller plants across Northwest Europe.

Other drivers and restraints analyzed in the detailed report include:

- Appliance Manufacturing Reshoring Momentum

- EU Renovation Wave Accelerates Gray EPS Adoption

- Sustainable Alternatives Gain Market Traction

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Europe's Expanded Polystyrene market size for white grades accounted for 70.86% share of overall consumption. White EPS persists in cavity walls, slab-on-grade floors, and perimeter drainage boards where cost remains the critical selector and modest panel thicknesses suffice for code compliance. However, gray and silver grades register the fastest 3.74% CAGR to 2031 as graphite's infrared-reflective particles lower λ-values to around 0.030 W/(m*K). In external thermal insulation composite systems, gray EPS reduces layer thickness from 16 cm to 12 cm for the same U-value, unlocking facade renovation in urban districts with tight lot lines. BEWI's CIRCULUM line couples the performance edge with recycled bead content, helping architects reconcile energy and circularity targets. Producers invest in in-line blowing-agent recovery and continuous block molding to embed more reclaim without sacrificing mechanical properties, positioning gray EPS as a technical and eco-credential upgrade within the Europe Expanded Polystyrene market.

The Europe Expanded Polystyrene (EPS) Market Report is Segmented by Product Type (White EPS, Gray and Silver EPS), End-User Industry (Building and Construction, Electrical and Electronics, Packaging, Other End-User Industries), and Geography (Germany, United Kingdom, France, Italy, Spain, Norway, Sweden, Denmark, Finland, Rest of Europe). The Market Forecasts are Provided in Terms of Volume (Tons).

List of Companies Covered in this Report:

- Alpek SAB de CV

- Austrotherm

- BASF

- BEWi

- Epsilyte LLC

- Ineos

- Kaneka Corporation

- Ravago

- SABIC

- SIBUR International GmbH

- Sunde Group

- Sunpor

- Synthos

- TotalEnergies

- Versalis S.p.A.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Building-energy codes mandating higher R-values from 2025

- 4.2.2 Mandatory cold-chain capacity additions for mRNA-class biologics

- 4.2.3 Re-shoring of appliance production boosting domestic protective packaging

- 4.2.4 Grey-EPS adoption in EU "Renovation Wave" retrofit projects

- 4.2.5 Low-cost modular housing programmes

- 4.3 Market Restraints

- 4.3.1 Styrene monomer price volatility tracking crude-oil spreads

- 4.3.2 Commercialisation of mycelium and moulded-pulp substitutes

- 4.3.3 Carbon-pricing schemes inflating Scope-3 footprints of petro-polymers

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

- 4.6 Import-Export Trends

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Product Type

- 5.1.1 White EPS

- 5.1.2 Gray and Silver EPS

- 5.2 By End-user Industry

- 5.2.1 Building and Construction

- 5.2.2 Electrical and Electronics

- 5.2.3 Packaging

- 5.2.4 Other End-user Industries (Agriculture and Automotive)

- 5.3 By Geography

- 5.3.1 Germany

- 5.3.2 United Kingdom

- 5.3.3 France

- 5.3.4 Italy

- 5.3.5 Spain

- 5.3.6 Norway

- 5.3.7 Sweden

- 5.3.8 Denmark

- 5.3.9 Finland

- 5.3.10 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)**/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Alpek SAB de CV

- 6.4.2 Austrotherm

- 6.4.3 BASF

- 6.4.4 BEWi

- 6.4.5 Epsilyte LLC

- 6.4.6 Ineos

- 6.4.7 Kaneka Corporation

- 6.4.8 Ravago

- 6.4.9 SABIC

- 6.4.10 SIBUR International GmbH

- 6.4.11 Sunde Group

- 6.4.12 Sunpor

- 6.4.13 Synthos

- 6.4.14 TotalEnergies

- 6.4.15 Versalis S.p.A.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

发泡聚苯乙烯增密设备市场:按机器类型、操作模式、类别、应用和最终用户划分 - 全球预测 2026-2032

发泡聚苯乙烯增密设备市场:按机器类型、操作模式、类别、应用和最终用户划分 - 全球预测 2026-2032 发泡聚苯乙烯市场-全球产业规模、份额、趋势、机会及预测(依产品类型、最终用途、地区及竞争格局划分,2021-2031年)

发泡聚苯乙烯市场-全球产业规模、份额、趋势、机会及预测(依产品类型、最终用途、地区及竞争格局划分,2021-2031年) 发泡聚苯乙烯(EPS):市占率分析、产业趋势与统计、成长预测(2026-2031)

发泡聚苯乙烯(EPS):市占率分析、产业趋势与统计、成长预测(2026-2031) 发泡聚苯乙烯包装市场规模、份额和成长分析(按产品类型、最终用途产业、密度、形状、应用和地区划分)-2026-2033年产业预测

发泡聚苯乙烯包装市场规模、份额和成长分析(按产品类型、最终用途产业、密度、形状、应用和地区划分)-2026-2033年产业预测 珠状聚苯乙烯(EPS)泡沫包装市场规模、占有率、成长及全球产业分析:按类型、应用和地区划分的洞察与预测(2024-2032 年)

珠状聚苯乙烯(EPS)泡沫包装市场规模、占有率、成长及全球产业分析:按类型、应用和地区划分的洞察与预测(2024-2032 年) 2025-2033 年发泡聚苯乙烯市场报告(依产品(白色、灰色、黑色)、最终用途产业(建筑、包装、汽车等)及地区)

2025-2033 年发泡聚苯乙烯市场报告(依产品(白色、灰色、黑色)、最终用途产业(建筑、包装、汽车等)及地区) 2025-2029年全球发泡聚苯乙烯市场

2025-2029年全球发泡聚苯乙烯市场 全球发泡聚苯乙烯市场:市场规模、份额、趋势分析(按产品、应用和地区)、细分市场预测(2025-2033)

全球发泡聚苯乙烯市场:市场规模、份额、趋势分析(按产品、应用和地区)、细分市场预测(2025-2033) 包装用发泡聚苯乙烯市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

包装用发泡聚苯乙烯市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测 2018-2034年全球发泡聚苯乙烯(EPS)市场需求及预测分析

2018-2034年全球发泡聚苯乙烯(EPS)市场需求及预测分析