|

市场调查报告书

商品编码

1687253

航空燃料:市场占有率分析、行业趋势和统计数据、成长预测(2025-2030 年)Aviation Fuel - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

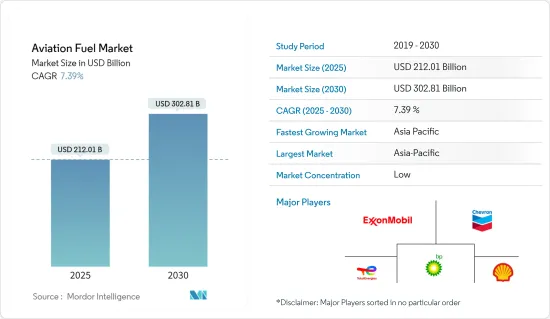

预计 2025 年航空燃料市场规模为 2,120.1 亿美元,到 2030 年将达到 3,028.1 亿美元,预测期内(2025-2030 年)的复合年增长率为 7.39%。

关键亮点

- 从中期来看,预计预测期内航空旅行需求的增加和飞机持有的增加将推动市场发展。

- 然而,预计在预测期内,人们对空气污染日益增长的环境问题将阻碍市场成长。

- 永续航空燃料技术的进步有望为航空燃料市场创造巨大的机会。

- 由于亚太地区航空旅行和飞机持有的增加,预计该地区将成为航空燃料市场的主导地区。

航空燃料市场趋势

航空涡轮燃料可望主导市场

- 航空涡轮燃料(ATF),俗称喷射机燃料,是一种石油衍生的燃料,其成分类似煤油。全球有各种等级可供选择,包括 Jet A、Jet A-1 和 Jet B,其中 Jet A-1 是最常用的。 Jet A-1 适用于各种飞机的涡轮发动机。其最低闪点为摄氏 38 度 (100°F),最高凝固点为摄氏 -47 度。

- 航空涡轮燃料用于各种飞机,包括商用客机、军用飞机和喷射机。现今大多数服役的飞机,特别是大型民航机,都依赖喷射机燃料作为初级能源。喷射机燃料喷射机燃料在各类飞机上的广泛使用使其在市场上占据主导地位。

- 此外,在民用和军用航空中流行的喷射发动机需要航空涡轮燃料才能高效运作。这些引擎的设计旨在利用喷射机燃料的能量和燃烧特性。只要喷射发动机仍然是航空业的主导推进技术,对航空涡轮燃料的需求就会保持很大。

- 例如,根据美国能源资讯署的数据,预计2022年至2021年间,美国的喷射机燃料消费量将成长近14%,这意味着飞机营运和燃料消耗量将会增加。

- 航空涡轮燃料的能量密度比活塞发动机飞机使用的其他燃料(如航空汽油)更高。这意味着喷射机燃料每单位体积可以提供更多的能量,这对于远距飞行和大型飞机至关重要。航空涡轮燃料的高能量密度使其动力来源喷射发动机的理想动力,可实现高效、长时间的飞行。

- 2023 年 1 月,印度石油公司 (IOC) 开始出口航空燃料,以满足小型飞机和无人机 (UAV) 的需求。此举将使印度透过开展石油出口进入价值约 27 亿美元的全球市场。贾瓦哈拉尔·尼赫鲁港务局 (JNPT) 已成功将委託80 桶航空燃油运往巴布亚纽几内亚。每桶容量为16千公升,能够运输大量航空瓦斯。

- 因此,正如所讨论的,预计航空涡轮燃料市场在预测期内将萎缩。

亚太地区可望主导市场

- 亚太地区正在经历显着的经济成长,其中中国、印度和东南亚国家引领着这一成长。经济成长导致航空旅行需求增加,直接导致航空燃料消费量增加。该地区强劲的经济成长正在提升航空燃料市场的主导地位。

- 亚太地区航空业蓬勃发展,航空公司众多,飞机持有不断壮大。该地区的航空公司不断扩张,增加新航线和航班频率。这种扩张推动了对航空燃料的需求,并有助于该地区航空燃料市场的主导地位。

- 此外,亚太地区快速的都市化和不断增长的中产阶级人口也导致航空旅行激增。随着该地区越来越多的人使用航空运输,对航空燃料的需求也在增加。都市化加快和中阶的蓬勃发展是推动亚太市场主导的关键因素。

- 此外,亚太地区正在见证廉价航空公司(LCC)的出现和发展。这些航空公司提供价格实惠的机票,吸引了更多的乘客,刺激了航空旅行的需求。低成本航空公司通常以较高的载客率运营,这会导致更高的燃料消费量,从而增加其在该地区航空燃料市场的主导地位。

- 此外,亚太地区许多国家正在大力投资机场基础建设。新机场正在建设中,现有机场也正在进行扩建和现代化改造。这些基础设施投资为空中交通和燃料消费量的成长创造了有利条件,进一步加强了该地区在航空燃料市场的主导地位。

- 例如,2023年5月,印度石油公司计划建造一座价值1.22亿美元的可持续航空燃料(SAF)工厂,因为航空公司实现脱碳目标所需的全球燃料供应面临严重短缺。拟建的设施每年将有 88,000 吨 SAF 生产能力。

- 因此,预计亚太地区将在预测期内占据市场主导地位。

航空燃料产业概况

航空燃料市场是细分的。市场上的主要企业(不分先后顺序)包括埃克森美孚、雪佛龙公司、壳牌公司、道达尔能源公司和英国石油公司。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究范围

- 市场定义

- 调查前提

第二章调查方法

第三章执行摘要

第四章 市场概述

- 介绍

- 至2028年的市场规模及需求预测(单位:美元)

- 近期趋势和发展

- 政府法规和政策

- 市场动态

- 驱动程式

- 航空旅行需求增加

- 飞机扩建

- 限制因素

- 油价波动

- 驱动程式

- 供应链分析

- 波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

第五章市场区隔

- 燃料类型

- 空气涡轮燃料

- 喷射机 A-1

- 喷射机

- 喷射机

- 航空生质燃料

- AVGAS

- 空气涡轮燃料

- 最终用户

- 商业

- 防御

- 通用航空

- 市场分析:按地区分類的市场规模及至2028年的需求预测(按地区划分)

- 北美洲

- 美国

- 加拿大

- 北美其他地区

- 欧洲

- 德国

- 英国

- 法国

- 俄罗斯

- 其他欧洲国家

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 其他亚太地区

- 南美洲

- 巴西

- 阿根廷

- 智利

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 埃及

- 南非

- 其他中东和非洲地区

- 北美洲

第六章 竞争格局

- 併购、合资、合作与协议

- 主要企业策略

- 公司简介

- Exxon Mobil Corporation

- Chevron Corporation

- Shell Plc.

- TotalEnergies SE

- BP Plc

- Gazprom Neft'PAO

- Neste Oyj

- Swedish Biofuels AB

- Red Rock Biofuels LLC

- Abu Dhabi National Oil Company

- Bharat Petroleum Corp. Ltd.

- Indian Oil Corporation Ltd.

- Emirates National Oil Company

- Valero Energy Corporation

- Allied Aviation Services Inc.

第七章 市场机会与未来趋势

- 生质燃料和永续替代燃料

简介目录

Product Code: 57160

The Aviation Fuel Market size is estimated at USD 212.01 billion in 2025, and is expected to reach USD 302.81 billion by 2030, at a CAGR of 7.39% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, the increasing demand for air travel and an increasing fleet of aircraft is expected to drive the market during the forecasted period.

- On the other hand, the increasing environmental concerns for air pollution are expected to hinder the growth of the market during the forecasted period.

- Nevertheless, the increasing advancements in sustainable aviation fuel technology are expected to create huge opportunities for the aviation fuel market.

- Asia-Pacific is expected to be a dominant aviation fuel market region due to the increasing air travel and aircraft fleets in the region.

Aviation Fuel Market Trends

Aviation Turbine Fuels Expected to Dominate the Market

- Aviation Turbine Fuel (ATF), commonly known as jet fuel, is a petroleum-derived fuel with a composition resembling kerosene. It is available in different grades globally, including Jet A, Jet A-1, and Jet B, with Jet A-1 being the most commonly utilized. Jet A-1 is compatible with a wide range of aircraft turbine engines. It exhibits a minimum flash point of 38 degrees Celsius (100°F) and a maximum freeze point of -47 degrees Celsius.

- Aviation turbine fuels are used in various aircraft, including commercial airliners, military, and business jets. Most aircraft in service today, especially larger commercial aircraft, rely on jet fuel as their primary energy source. The widespread usage of jet fuel in various aircraft types contributes to its dominance in the market.

- Moreover, jet engines, prevalent in commercial and military aviation, require aviation turbine fuels to operate efficiently. These engines are designed to utilize jet fuel's energy content and combustion properties. As long as jet engines remain the dominant propulsion technology in the aviation industry, the demand for aviation turbine fuels will continue to be significant.

- For instance, according to the United States Energy Information Administration, the consumption of jet fuel in the United States increased by almost 14% between 2022 and 2021, signifying the increasing air ravels and fuel consumption.

- Aviation turbine fuels have a higher energy density than other fuels, such as avgas used in piston-engine aircraft. This means that jet fuel can provide more energy per unit of volume, which is crucial for long-haul flights and larger aircraft. The high energy density of aviation turbine fuels makes them ideal for powering jet engines and allows for efficient and extended flight operations.

- In January 2023, The Indian Oil Corporation (IOC) initiated the export of aviation fuel, catering to the requirements of small aircraft and unmanned aerial vehicles (UAVs). This move allows India to enter the global market, valued at approximately USD 2.7 billion, by venturing into petroleum exports. The Jawaharlal Nehru Port Trust (JNPT) facilitated the shipment of the first consignment comprising 80 barrels of aviation fuel to Papua New Guinea. Each barrel has a capacity of 16 kiloliters, enabling the transport of a significant quantity of aviation gas.

- Therefore as per the points discussed, aviation turbine fuel is expected to diminish the market during the forecasted period.

Asia-Pacific Expected to Dominate the Market

- The Asia-Pacific region is experiencing significant economic growth, with countries like China, India, and Southeast Asian nations driving this expansion. As economies grow, there is a corresponding increase in air travel demand, directly translating to higher aviation fuel consumption. The region's robust economic growth fuels the dominance of the aviation fuel market.

- The Asia-Pacific region has a flourishing airline industry with numerous carriers and a growing fleet of aircraft. Airlines in the region continuously expand their operations, adding new routes and increasing flight frequencies. This expansion necessitates a higher demand for aviation fuel, contributing to the dominance of the market in the region.

- Moreover, rapid urbanization in the Asia-Pacific region and the rise of the middle-class population has led to a surge in air travel. As more people in the region access air transportation, the demand for aviation fuel grows. The increasing urbanization and a burgeoning middle-class population are key factors driving the dominance of the market in the Asia-Pacific region.

- Furthermore, Asia-Pacific region has witnessed the emergence and growth of low-cost carriers (LCCs). These airlines offer affordable airfares, attracting a larger segment of the population and stimulating air travel demand. LCCs typically operate with higher load factors, leading to increased fuel consumption and subsequently driving the aviation fuel market's dominance in the region.

- Additionally, many countries in the Asia-Pacific region are investing heavily in airport infrastructure development. New airports are being built, and existing ones are undergoing expansion and modernization. These infrastructure investments create favorable conditions for increased air traffic and fuel consumption, further contributing to the region's dominance in the aviation fuel market.

- For instance, in May 2023, Indian Oil Corp. intends to construct a sustainable aviation fuel (SAF) plant worth USD 122 million due to the substantial shortfall in global supplies required by airlines to achieve decarbonization targets. The planned facility will have the capability to manufacture 88,000 tons of SAF annually.

- Therefore as per the above-mentioned points the Asia-Pacific region is expected to dominate the market during the forecasted period.

Aviation Fuel Industry Overview

The Aviation fuel market is fragmented. Some of the major players in the market (in no particular order) include ExxonMobil Corporation, Chevron Corporation, Shell Plc., TotalEnergies SE, and BP Plc. among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2028

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increasing Air Travel Demand

- 4.5.1.2 Expanding Airline Fleet

- 4.5.2 Restraints

- 4.5.2.1 Volatile Crude Oil Prices

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Fuel Type

- 5.1.1 Air Turbine Fuel

- 5.1.1.1 Jet A-1

- 5.1.1.2 Jet A

- 5.1.1.3 Jet B

- 5.1.2 Aviation Biofuel

- 5.1.3 AVGAS

- 5.1.1 Air Turbine Fuel

- 5.2 End-User

- 5.2.1 Commercial

- 5.2.2 Defence

- 5.2.3 General Aviation

- 5.3 Geography (Regional Market Analysis {Market Size and Demand Forecast till 2028 (for regions only)})

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Russia

- 5.3.2.5 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Chile

- 5.3.4.4 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 Egypt

- 5.3.5.4 South Africa

- 5.3.5.5 Rest of Middle-East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Exxon Mobil Corporation

- 6.3.2 Chevron Corporation

- 6.3.3 Shell Plc.

- 6.3.4 TotalEnergies SE

- 6.3.5 BP Plc

- 6.3.6 Gazprom Neft' PAO

- 6.3.7 Neste Oyj

- 6.3.8 Swedish Biofuels AB

- 6.3.9 Red Rock Biofuels LLC

- 6.3.10 Abu Dhabi National Oil Company

- 6.3.11 Bharat Petroleum Corp. Ltd.

- 6.3.12 Indian Oil Corporation Ltd.

- 6.3.13 Emirates National Oil Company

- 6.3.14 Valero Energy Corporation

- 6.3.15 Allied Aviation Services Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Biofuels and Sustainable Alternatives

02-2729-4219

+886-2-2729-4219

全球航空燃油终端市场规模、份额、趋势及成长分析报告(2026-2034)

全球航空燃油终端市场规模、份额、趋势及成长分析报告(2026-2034) 航空燃料市场报告:按燃料类型、飞机类型、最终用途和地区划分,2026-2034年

航空燃料市场报告:按燃料类型、飞机类型、最终用途和地区划分,2026-2034年 2026年全球航空燃料市场报告航空汽油(Avgas)市场规模、占有率、成长及全球产业分析:依终端用户和地区划分的洞察与预测(2026-2034)

2026年全球航空燃料市场报告航空汽油(Avgas)市场规模、占有率、成长及全球产业分析:依终端用户和地区划分的洞察与预测(2026-2034) 航空燃料市场-全球产业规模、份额、趋势、机会、预测:按燃料类型、应用、类型、地区和竞争格局划分,2021-2031年运输燃料市场-全球产业规模、份额、趋势、机会和预测:按燃料类型、最终用户、地区和竞争对手划分,2021-2031年

航空燃料市场-全球产业规模、份额、趋势、机会、预测:按燃料类型、应用、类型、地区和竞争格局划分,2021-2031年运输燃料市场-全球产业规模、份额、趋势、机会和预测:按燃料类型、最终用户、地区和竞争对手划分,2021-2031年 2026-2030年全球国防飞机航空燃料市场日本航空燃油市场报告:按燃油类型、飞机类型、最终用途和地区划分(2026-2034年)

2026-2030年全球国防飞机航空燃料市场日本航空燃油市场报告:按燃油类型、飞机类型、最终用途和地区划分(2026-2034年) 航空燃料市场规模、份额和成长分析(按燃料类型、飞机类型、最终用户、销售管道和地区划分)-2026-2033年产业预测

航空燃料市场规模、份额和成长分析(按燃料类型、飞机类型、最终用户、销售管道和地区划分)-2026-2033年产业预测 航空生质燃料市场规模、份额及成长分析(按类型、应用和地区划分)-2026-2033年产业预测

航空生质燃料市场规模、份额及成长分析(按类型、应用和地区划分)-2026-2033年产业预测

▼