|

市场调查报告书

商品编码

1687266

主动地理围篱 -市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Active Geofencing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

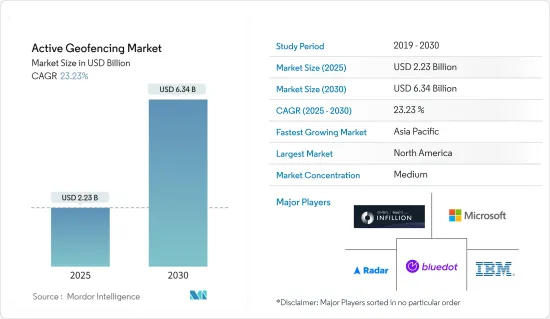

预计 2025 年主动地理围篱市场规模将达到 22.3 亿美元,到 2030 年将达到 63.4 亿美元,预测期内(2025-2030 年)的复合年增长率为 23.23%。

由于空间资料的更有效利用、即时定位技术的改进以及全球消费者越来越多地采用定位应用程序,主动地理围栏正在不断发展。

关键亮点

- 地理围栏是一种基于位置的服务,个人最终用户可以透过应用程式和软体使用该服务,这些应用程式和软体利用 GPS、PFID、WiFI 和行动资料等技术,一旦设备离开称为地理围栏的地理区域虚拟边界,就会触发预先编程的操作。

- 空间资料和即时定位技术的日益普及正在改变人们和企业与世界互动的方式,并带来巨大的节省。各种设备和系统都连接到互联网:电话、智慧建筑、汽车导航、工业、自动驾驶汽车等等。为了维持系统日常正常运行,需要提供即时位置资讯的技术。

- 由于技术的灵活性和能力,主动地理围栏的进步正在不断增加。市场成长受到数位行销、丛集、自动驾驶汽车以及自带设备日益普及等趋势的推动。因此,预计所研究的市场将保持强劲,并见证市场参与企业的显着成长贡献。

- 对于位置追踪日益增长的担忧和监管可能会威胁主动地理围栏技术。此外,由于缺乏处理各地区隐私和资料收集的监管机构,主动地理围栏解决方案受到阻碍。

- COVID-19 病毒增加了医疗保健、工业等多个领域对主动地理围篱的使用。例如,每家公司都必须提交申请来识别其场所内的员工并立即直接联繫他们。主动地理围篱有助于紧急情况下的安全及时通讯。

主动地理围篱市场趋势

零售领域显着成长

- 主动地理围篱允许零售商识别销售点规定半径范围内的潜在客户,并向他们发送个人化通知和具体优惠。此外,随着数位化不断扩展到所有零售领域,零售业对有效地理围篱的需求正在迅速增长。

- 利用地理围栏资料的广告宣传往往具有更高的投资收益,因为零售商可以瞄准最有可能使用其服务或产品的消费者。这意味着零售商的利润更高。

- 展望未来,主动地理围栏有望与扩增实境(AR)、客户和先进技术相结合,创造更数位优先、个人化的购物体验。随着越来越多的行动装置变得可穿戴,顾客将期望体验更数位化、个人化的购物体验。预计在未来预测期内,零售业中的主动地理围篱将变得更加普遍。

- 最近一项关于影响未来购物趋势的研究预测,到 2025 年,大约三分之一的美国消费者将在线上购买商品时使用 AR 技术。 AR技术允许在网路购物时进行虚拟产品浏览。根据这项研究,沙乌地阿拉伯和阿拉伯联合大公国等国家预计 AR 使用率将高达 45%,而在欧洲,这一比例则明显较低。

预计北美将占据大部分市场份额

- 在北美,投资和创新正在涉及各种终端的主动地理围栏,包括医疗保健、运输和物流、金融服务业和安全。空间资讯和即时定位技术的融合正在推动该地区市场的发展。

- 此外,该地区主要由能够使用主动地理围栏的 BFSI 行业、零售业以及运输和物流行业的公司主导。此外,北美是世界上两个最新兴的经济体的所在地:美国和加拿大。由于该地区拥有强大的通讯互联网基础设施,该地区也处于市场领先地位。

- 此外,数位技术的广泛部署和所有企业对商业智慧工具的需求的增长,导致各种地理围栏解决方案对自动化工具的采用增加。

- 然而,许多本地零售商现在正在透过数位优惠和促销活动应用主动地理围栏来增强客户忠诚度。零售商还可以更好地了解顾客在访问特定商店之前和之后来自哪里。

主动地理围篱产业概述

由于 Bluedot Innovation Pty Ltd、Infillion Inc. (GIMBLE)、IBM Corporation、Microsoft Corporation、Radar Labs Inc. 等知名供应商的存在,主动地理围篱市场已半固体。主要企业参与了收购和伙伴关係等各种策略,以提高市场占有率并增加所研究市场的盈利。

- 2023 年 7 月,Radar 宣布与 Cordial 合作,透过基于位置的体验(包括内部应用模式、商店地图和定位器以及地址自动完成)来提高参与度和收益。 JOANN 等品牌正在利用 Radar 的位置基础设施和 Cordial 的行销和资料平台的组合,即时为客户提供高度个人化、与情境相关的体验。

- 2023 年 6 月,Autodesk 宣布与地理资讯系统 (GIS) 软体的全球产业领导者 Esri 建立策略联盟。 ArcGIS GeoBIM 将 Autodesk BIM Collaborate Pro 与 Esri 的 ArcGIS Online 整合,提供设计模型和智慧定位的整体视图,以降低风险、增加计划协作并改善相关人员的沟通。

- 2022 年 9 月,M3 宣布对其专有劳动力管理软体 M3 labor 进行重大改进,该软体包含地理围栏和信标技术。此新功能可让 M3 Labor Service 使用者在一定半径范围内设定员工可以打卡上下班的区域。这些新功能旨在使饭店员工能够在需要的时间和地点打卡上下班,同时防止他们在其他地点打卡上下班,从而避免打卡错误的可能性。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概览

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买家的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 产业价值链分析

- COVID-19 市场影响

第五章市场动态

- 市场驱动因素

- 空间资料的使用日益增多,即时定位技术的改进

- 基于位置的应用程式的消费者渗透率

- 市场限制

- 提高消费者对位置追踪安全保障的意识

第六章市场区隔

- 按组织规模

- 中小企业

- 大型企业

- 按最终用户产业

- 银行、金融服务和保险

- 零售

- 国防、政府和军队

- 医疗保健

- 製造业

- 运输和物流

- 其他的

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

第七章竞争格局

- 公司简介

- Bluedot Innovation Pty Ltd

- Infillion Inc.(GIMBLE)

- IBM Corporation

- Microsoft Corporation

- Radar Labs Inc.

- Google LLC

- Samsung Electronics Co.

- Verve Inc.

- Apple Inc.

- LocationSmart

- SZ DJI Technology Co.

- ESRI

第八章投资分析

第九章:市场的未来

The Active Geofencing Market size is estimated at USD 2.23 billion in 2025, and is expected to reach USD 6.34 billion by 2030, at a CAGR of 23.23% during the forecast period (2025-2030).

Active geofencing is growing due to more effective use of Spatial Data, improving Real Time Location Technologies, and increased adoption worldwide for location-bassed applications by consumers.

Key Highlights

- Geofencing is a location-based service used by each end user, for which an application or software uses technologies such as GPS, PFID, WiFI, and mobile data to enable them to trigger preprogrammed actions when the device leaves virtual boundaries of geographical zones known as geofences.

- How people and businesses interact with the world and make huge savings has changed due to the increased use of spatial data and real-time location technologies. All kinds of devices and systems are connected to the Internet, such as phones, Smart buildings, car navigation systems, industries, or fleets of autonomous vehicles. Technology that provides real-time location data is required to maintain the system's proper functioning on a daily basis.

- With technological flexibility and capabilities, advancement in Active Geofencing is increasing. The market's growth is driven by trends such as digital marketing and clustering, autonomous cars, increased adoption of Bring Your Own Device, etc. The market studied, therefore, is expected to remain robust and will have a significant growth contribution from players in the market.

- Increasing concerns and regulations regarding location tracking can threaten active geofencing technologies. Moreover, active geofencing solutions are being held back due to the lack of regulatory bodies dealing with privacy and data collection in various regions.

- The COVID-19 virus increased the use of Active Geofences in several sectors, such as healthcare, industry, and many others. For example, an application had to be submitted by individual companies to identify staff at their premises and communicate with them directly and immediately. Active geofencing has facilitated secure, timely communication during an emergency.

Active Geofencing Market Trends

Retail Segment to Witness Significant Growth

- An active geofence enables retailers to determine potential customers within a defined radius of any point of sale, sending them personalised notifications and specific offers that they can use in order to make their purchases. In addition, as digitisation continues to spread across all retail sectors, demand for effective geofencing is growing rapidly in the retail sector.

- In view of the fact that retailers can target consumers who are most likely to take part in their services or products, advertising campaigns using geofenced data tend to deliver higher return on investment. This leads to higher profits for retail organisations.

- Moreover, In the future, active geofencing will be combined with augmented reality (AR), customers and advanced technologies andexpect a more digital-first, personalized shopping experience. As more mobile devices become wearables, customers are expected to experience a more digital first and personalised shopping experience. In the coming forecast period, this will lead to a higher uptake of active geofencing in retail.

- Recent research on trends which are shaping the future of shopping, predicts that by 2025, about one third of consumers in the United States will be using AR technologies when purchasing products online. AR technologies enable virtual product viewing when shopping online. The study showed that while in countries like Saudi Arabia and United Arab Emirates, the expected use of AR was as high as 45 percent, in Europe, this share was much lower.

North America is Expected to Hold the Major Share of the Market

- In North America, active geofencing investments and innovation have been made at various endpoints, such as healthcare, transport, logistics, financial services sector, security, and many others. Market forces push for integrating spatial information and real-time location technologies in this region.

- Further, this region is dominated by companies in the BFSI sector, retail and transport, and logistics sectors capable of using active geofencing. In addition, North America has one of the most developed economies in the world in the form of the United States and Canada. As a result of the strong communication and Internet infrastructure in the region, it is also leading the market.

- In addition, the adoption of automated tools that take different geofence solutions has increased due to the wide deployment of digital technologies and the growing demand for business intelligence tools in all kinds of enterprises.

- However, many regional retailers are increasingly applying active geofencing through digital offers and promotions to strengthen customer loyalty. Retailers can also better understand where their customers are coming from before and after they visit one particular shop.

Active Geofencing Industry Overview

The active geofencing market is semi-consolidated due to prominent vendors like Bluedot Innovation Pty Ltd, Infillion Inc. (GIMBLE), IBM Corporation, Microsoft Corporation, Radar Labs Inc., etc. The key players are involved in various strategies, such as acquisitions and partnerships, to improve their market share and enhance their profitability in the market studied.

- In July 2023, Radar announced our partnership with Cordial, Increasing engagement and revenue through location-based experiences like on-premise app modes, store maps and locators, and address autocomplete. In real time, brands such as JOANN deliver highly personalised, contextually relevant experiences to their customers through the combination of Radar's industry location infrastructure with Cordial's marketing and data platform.

- In June 2023, Autodesk has announced the strategic partnership with Esri, one of the global industry leader in Geographic Information System (GIS) software, Where the Autodesk BIM Collaborate Pro and Esri's ArcGIS Online integrate through ArcGIS GeoBIM for a holistic view of design models and location intelligence to reduce risk, provide better project collaboration, and improve communication with stakeholders.

- In September 2022, M3 announced significant advancements to its proprietary Labour Management software, M3 labor, consisting of geofencing and beacon technologies. With this new functionality, users of the M3 Labour service can create an area radius where staff can punch in and out at work. These new features are intended to ensure that hotel staff clock in and out when and where they should while preventing them from doing so elsewhere, thereby avoiding the possibility of false and erroneous punching.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat Of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increased Use of Spatial Data and Improved Real-time Location Technology

- 5.1.2 Higher Adoption of Location-based Application among Consumers

- 5.2 Market Restraints

- 5.2.1 Rising Awareness Regarding Safety and Security among Consumers of Location Tracking

6 MARKET SEGMENTATION

- 6.1 By Organization Size

- 6.1.1 Small-Scale and Medium-Scale Businesses

- 6.1.2 Large-Scale Businesses

- 6.2 By End-user Industry

- 6.2.1 Banking, Financial Services, and Insurance

- 6.2.2 Retail

- 6.2.3 Defense, Government, and Military

- 6.2.4 Healthcare

- 6.2.5 Industrial Manufacturing

- 6.2.6 Transportation and Logistics

- 6.2.7 Other End-user Industries

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia Pacific

- 6.3.4 Latin America

- 6.3.5 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Bluedot Innovation Pty Ltd

- 7.1.2 Infillion Inc. (GIMBLE)

- 7.1.3 IBM Corporation

- 7.1.4 Microsoft Corporation

- 7.1.5 Radar Labs Inc.

- 7.1.6 Google LLC

- 7.1.7 Samsung Electronics Co.

- 7.1.8 Verve Inc.

- 7.1.9 Apple Inc.

- 7.1.10 LocationSmart

- 7.1.11 SZ DJI Technology Co.

- 7.1.12 ESRI