|

市场调查报告书

商品编码

1687277

动态随机存取记忆体(DRAM):市场占有率分析、产业趋势与成长预测(2025-2030)Dynamic Random Access Memory (DRAM) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

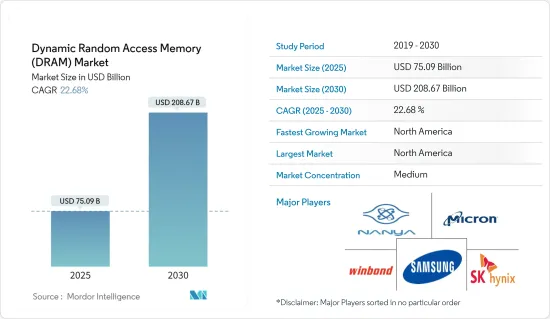

动态随机存取记忆体市场规模预计在 2025 年为 750.9 亿美元,预计到 2030 年将达到 2086.7 亿美元,预测期内(2025-2030 年)的复合年增长率为 22.68%。就出货量而言,预计市场将从 2025 年的 196.2 亿台成长到 2030 年的 348.2 亿台,预测期间(2025-2030 年)的复合年增长率为 12.16%。

关键亮点

- 一种称为动态随机存取记忆体 (DRAM) 的半导体记忆体存储和处理电脑处理器运作所需的资料和程式码。这种类型的 RAM 常见于个人电脑、智慧型手机、ADAS 系统、智慧型手錶、工作站和伺服器。

- 生成式人工智慧的日益普及正在推动对更快处理速度和更有效率 DRAM 解决方案的需求。例如,美光科技正与高通科技公司合作,加速智慧型手机边缘产生人工智慧的发展。该公司于 2023 年 10 月向高通交付了其低功耗双倍资料速率 5X (LPDDR5X) 记忆体的生产样品。 LPDDR5X 记忆体的运行速度等级为 9.6Gbps,可提供行动生态系统释放边缘 AI 力量所需的速度和效能。

- 美光 LPDDR5X 采用其创新的 1B 製程节点技术,为行动用户带来先进的省电功能。此外,SK海力士于2023年9月在加州举办的2023年AI硬体与边缘AI高峰会上,发布了基于高速、低功耗、高密度记忆体解决方案GDDR6-AiM的AI加速卡AiMX1的原型。预计AiMX1将为高效能、资料密集型AI系统的开发做出重大贡献。

- 资料中心对 DRAM 的需求预计将大幅成长,从而推动每年整体 DRAM 需求的成长。人工智慧、串流媒体、游戏、自动驾驶汽车和其他最尖端科技可能会继续推动对资料中心的强劲需求。随着资料中心营运商努力提供支援高效能运算所需的不断增加的功率密度的能力,我们将看到资料中心架构和技术的进一步创新。人工智慧、物联网和5G的融合将极大地推动运算和DRAM的需求。

- 由于消费者支出下降、景气衰退和通货膨胀上升,预计 23 财年全球智慧型手机出货量将较 22 财年大幅下降。三星、苹果、小米和 Oppo(包括 One Plus)等智慧型手机供应商的智慧型手机销售量均下滑。继智慧型手机、平板电脑和个人电脑/笔记型电脑之后,由于消费者支出疲软、利率下降以及持续的地缘政治紧张局势导致不确定性增加,2023 财年的需求有所下降。这些因素将限制DRAM市场的成长。

- 新冠疫情对DRAM市场的需求与供应都产生了重大影响。世界各地的封锁和工厂关闭导致供不应求,但预计大部分影响是暂时的。世界各国政府正在采取措施支持半导体产业,这可能会带来復苏。

动态随机存取记忆体(DRAM)市场趋势

资料中心应用领域预计将占据较大的市场占有率

- 疫情加速了数位平台和云端服务的采用,促进了资料中心的发展。资料中心的成长正在推动市场需求,因为 DRAM 是现代企业和资料中心应用正常运作的关键元件。据Cloudscene称,截至2023年9月,全球共有超过9,380个资料中心。

- DRAM供应商一直在调整其产品组合,增加伺服器DRAM产品的晶圆投入,同时尽量减少行动DRAM产品的晶圆投入。造成这种趋势的原因有二。首先,伺服器DRAM需求前景光明。 AMD 和英特尔的最新伺服器平台最终将于 2022 年向OEM发货,但认证预计需要六个月时间,这将对近期的伺服器出货量和相关记忆体需求造成阻力。同时,由于产量持续超过需求,DRAM 供应商一直在大幅增加库存。

- 第二个原因是,行动DRAM领域在2022年面临严重的供过于求。即使在2023年,对于智慧型手机出货量的发展以及智慧型手机平均DRAM含量的大幅增加的预测仍然相当保守。因此,DRAM 製造商打算继续增加伺服器 DRAM 在其产品组合中的份额,从而实现资料中心领域的显着成长。

- 这标誌着企业越来越多地采用与云端运算、人工智慧和高效能运算 (HPC) 应用相关的新兴技术的一个里程碑。为了处理新兴技术工作负载,伺服器的平均 DRAM 容量预计将大幅增加。

- 此外,DDR5 买家库存在资料中心领域越来越受欢迎。例如,美光科技推出了其 DDR5 晶片,并透露在它们用于客户端设备之前,其需求主要来自资料中心应用。瑞萨电子以配备 DDR5多工器组合列 (MCR) 双列直插式记忆体模组的高效能记忆体模组新晶片组引领资料中心领域。另一方面,三星加强减产力度,使得DDR4晶圆的投入量大幅减少,导致伺服器用DDR4库存吃紧。在这种情况下,伺服器DDR4已经没有进一步降价的空间。

预计北美将占很大份额

- 由于资料中心、汽车和家用电子电器的应用日益广泛,北美 DRAM 市场预计将经历强劲成长。

- 在美国,DRAM 的成长预计将超越个人设备,在云端运算、伺服器和汽车应用领域的应用也将增加。智慧型手机越来越多地配备DRAM,由于市场渗透率不断提高且价格下降,行动电话越来越受到消费者的接受,预计手机将占据DRAM市场的很大份额。随着使用案例变得更加多样化以及行动电话变得越来越普及,DRAM 市场的需求预计也将增加。

- 美国行动电话产业是最大的产业之一,对市场的成长有重大影响。该地区投资的增加和生产力的提高是市场的主要驱动力。

- 资料中心营运商需要利用先进的记忆体功能和处理器进步来优化平台效能,从而推动对 DDR5 DRAM 市场的需求。美国继续对资料中心进行大规模投资,预计将刺激DRAM的需求。

- 影响市场的另一个关键因素是5G技术的引进。儘管 5G 技术刚刚推出,但预计它将对无线通讯市场产生重大影响。根据埃森哲的分析,预计2021年至2025年间,5G的普及将为美国国内生产总值)贡献超过1.5兆美元。

动态随机存取记忆体(DRAM)市场概览

动态随机存取记忆体 (DRAM) 市场已呈现半固体状态,三星电子、SK 海力士和美光等主要参与者占据了相当大的市场份额。地域扩张和产品创新在市场竞争中发挥重要作用。供应商需要提高生产和处理能力,以满足日益增长的需要提高速度和效能的资料中心、行动和消费者应用的需求。 DRAM 市场的领先供应商正在大力投资 24GB、DDR5、HBM 等下一代晶片,并正在进入为 AI 和 5G 製造 FRAM 的下一阶段。这有助于他们在竞争中保持领先,但也意味着他们需要承担研发成本。

- 2023 年 9 月:三星电子推出其开创性的低功耗压缩附加记忆体模组 (LPCAMM)外形规格,为个人电脑、笔记型电脑和资料中心的 DRAM 市场带来重大突破。这项尖端开发成果已通过英特尔平台上的严格系统检验,实现了惊人的 7.5Gbps 速度。

- 2023 年 6 月:美光科技公司揭露在印度古吉拉突邦建立新的组装和测试工厂的意图。该工厂将为国内和国际市场生产 DRAM 和 NAND 产品。新设施将于 2023 年开始建设,并将分阶段进行。第一阶段将包括 50 万平方英尺的无尘室空间,预计将于 2024 年底运作。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概览

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买家的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争强度

- 宏观经济因素对DRAM产业的影响

第五章市场动态

- 市场驱动因素

- 云端运算、物联网、5G、人工智慧和行动等大趋势的持续发展预计将推动未来的需求

- 市场限制

- 行动装置、平板电脑和笔记型电脑/个人电脑的需求放缓

第六章定价分析

- DRAM现货价格(每GB)

- 价格趋势分析

第七章市场区隔

- 按建筑

- DDR3

- DDR4

- DDR5

- DDR2/其他架构

- 按应用

- 智慧型手机/平板电脑

- 个人电脑/笔记型电脑

- 资料中心

- 图形

- 消费品

- 车

- 其他的

- 按地区

- 美国

- 欧洲

- 韩国

- 中国

- 台湾

- 其他亚太地区

- 其他的

第八章竞争格局

- 公司简介

- Samsung Electronics Co. Ltd

- Micron Technology Inc.

- SK Hynix Inc.

- Nanya Technology Corporation

- Winbond Electronics Corporation

- Powerchip Semiconductor Manufacturing Corp.

- Transcend Information Inc.

9.供应商市场占有率分析

第十章投资分析

第11章:投资分析市场的未来

The Dynamic Random Access Memory Market size is estimated at USD 75.09 billion in 2025, and is expected to reach USD 208.67 billion by 2030, at a CAGR of 22.68% during the forecast period (2025-2030). In terms of shipment volume, the market is expected to grow from 19.62 billion units in 2025 to 34.82 billion units by 2030, at a CAGR of 12.16% during the forecast period (2025-2030).

Key Highlights

- Semiconductor memory, called dynamic random access memory (DRAM), stores and processes data or program code necessary for a computer processor's functioning. This type of RAM is commonly found in personal computers, smartphones, ADAS systems, smartwatches, workstations, and servers.

- The growing adoption of generative AI boosts the demand for fast processing and highly efficient DRAM solutions. For instance, Micron Technology partnered with Qualcomm Technologies Inc. to accelerate generative AI at the edge for smartphones. The company shipped production samples of the low-power double data rate 5X (LPDDR5X) memory to Qualcomm in October 2023. The LPDDR5X memory operates at a 9.6 Gbps speed grade, delivering the speed and performance the mobile ecosystem needs to unleash the power of AI at the edge.

- Micron LPDDR5X provides advanced power-saving capabilities for mobile users using its innovative, 1B process node technology. Also, in September 2023, SK Hynix presented a prototype of AI accelerator card, AiMX1, based on the high-speed, low-power, and high-density memory solution GDDR6-AiM at the AI hardware & edge AI Summit 2023 in California. AiMX1 is expected to significantly contribute to developing high-performance, data-intensive, and AI-based systems.

- Datacenter demand for DRAM is projected to grow significantly, which will lift overall DRAM demand annually. Artificial intelligence and other cutting-edge technologies like streaming, gaming, and autonomous vehicles will continue to drive robust demand for data centers. This will drive innovation in data center architecture and technology as operators strive to provide the capacity that supports the increased power density required by high-performance computing. Integrating artificial intelligence, the Internet of Things, and 5G will be a massive tailwind to the demand for computing and DRAM.

- Worldwide smartphone shipments declined significantly in FY 2023 compared to FY 2022 due to decreased consumer spending, economic downturn, and increased inflation. Smartphone vendors such as Samsung, Apple, Xiaomi, and Oppo (including One Plus) witnessed declining smartphone sales. Following smartphones, tablets, and PCs/laptops, demand fell in FY 2023 due to weakened consumer spending, interest rates, and increasing uncertainty due to ongoing geopolitical tensions. These factors will restrict the growth of the DRAM market.

- The COVID-19 pandemic had a significant impact on the DRAM market, both on the demand side and the supply side. Lockdowns and factory shutdowns worldwide contributed to the supply shortage, but many of these impacts are expected to be temporary. Governments worldwide are taking steps to support the semiconductor industries, which could lead to a recovery.

Dynamic Random Access Memory (DRAM) Market Trends

The Data Center Application Segment is Expected to Hold Significant Market Share

- The pandemic accelerated the use of digital platforms and cloud services, boosting data center development. As DRAM is an essential component for the proper functioning of modern enterprise and data center applications, the growth in data centers has significantly fueled the demand in the market. According to Cloudscene, as of September 2023, there were over 9,380 data centers worldwide.

- DRAM suppliers have been working toward adjusting their product mixes to assign more wafer input to server DRAM products while minimizing the wafer input for mobile DRAM products. Two reasons have driven this trend. Firstly, the demand outlook is bright for the server DRAM segment. The latest server platforms from AMD and Intel finally shipped to OEMs in 2022 but are expected to need ~six months for qualifying, facilitating a headwind to near-term server shipments and associated memory demand. Simultaneously, DRAM suppliers are building up significant inventory positions as production surges continue to outpace demand.

- In the second position, the reason lies that the mobile DRAM segment faced a significant oversupply in 2022. In 2023, the projections on the development of smartphone shipments and the surge in the average DRAM content of smartphones remained pretty conservative. As a result, DRAM suppliers intend to keep expanding the share of server DRAM in their product mixes, thus providing significant growth in the data center segment.

- Semiconductor manufacturers are likely to respond to changes in demand by producing more dynamic RAM (DRAM) for servers than for mobile devices this year, a milestone highlighting increasing enterprise use of emerging technology related to cloud computing, AI, and high-performance computing (HPC) applications. To handle the emerging-tech workloads, the average DRAM content of servers is expected to increase significantly.

- Moreover, in the data center segment, the buyer inventory of DDR5 has been gaining popularity. For instance, Micron Technology unveiled its DDR5 chip, which it stated found the most demand from data center applications before popping up in client devices. Renesas has led the data center segment due to new chipsets for high-performance memory modules based on DDR5 multiplexer combined ranks (MCR) dual in-line memory modules. Meanwhile, Samsung's intensified production cutbacks have notably shrunk DDR4 wafer inputs, causing a supply crunch in server DDR4 stocks. This scenario leaves no leeway for further server DDR4 price reductions.

North America is Expected to Hold Significant Market Share

- The market for DRAM is expected to register significant growth in the region owing to its increasing adoption in data centers, automotive, and consumer electronics.

- In the United States, the growth of DRAM is projected to extend beyond personal devices and find increased utilization in cloud computing, servers, and automotive applications. Smartphones are increasingly incorporating DRAM, and mobile phones are anticipated to hold a significant portion of the DRAM market due to their expanding market penetration and declining prices, resulting in greater consumer acceptance. As the range of use cases and mobile phone adoption continues to diversify and expand, the demand for the DRAM market is expected to rise.

- The mobile phone industry in the United States is one of the largest industries, significantly impacting the market's growth positively. Rising investments and growing production rates across the region are significant market drivers.

- Data center operators must optimize platform performance by leveraging advanced memory capabilities and processor advancements, fueling the demand for DDR5 DRAMs in the market. The United States is consistently experiencing substantial investments in data centers, which is anticipated to stimulate the requirement for DRAMs.

- Another significant factor influencing the market is implementing 5G technology. Despite its recent introduction, 5G technology and wireless communication as a whole are projected to have a substantial effect on the market. As per Accenture's analysis, the adoption of 5G is anticipated to contribute more than USD 1.5 trillion to the gross domestic product (GDP) of the United States between 2021 and 2025.

Dynamic Random Access Memory (DRAM) Market Overview

The dynamic random access memory (DRAM) market is semi-consolidated, with the major players in the market, like Samsung Electronics, SK Hynix, and Micron, holding a significant market share. Geographical expansion and product innovation play a vital role in the competitive strategy of market players. Vendors need enhanced fabrication and processing capabilities in line with the increasing data center, mobile, and consumer applications that require improved speed and performance. The prominent vendors in the DRAM market are investing heavily in the next generation of chips, like 24GB, DDR5, and HBM, and have moved into the next phase of making FRAMs for AI and 5G. This is helping them stay ahead of the competition, but it also means they need to be able to pay for their research and development.

- September 2023: Samsung Electronics unveiled the pioneering low-power compression attached memory module (LPCAMM) form factor, marking a significant breakthrough in the DRAM market for personal computers, laptops, and data centers. This cutting-edge development has successfully passed rigorous system verification on Intel's platform, achieving a remarkable speed of 7.5 Gbps.

- June 2023: Micron Technology Inc. revealed its intention to construct a new assembly and test facility in Gujarat, India. The facility will cater to manufacturing DRAM and NAND products in domestic and international markets. The construction of the new facility was to commence in 2023 and will be carried out in phases. The first phase will include 500,000 square feet of cleanroom space and is expected to become operational in late 2024.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Impact of Macroeconomic Factors on the DRAM Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Continuous Evolution of Mega Trends Such As Cloud Computing, IoT, 5G, AI, and Mobility are Expected to Create Demand in the Future

- 5.2 Market Restraints

- 5.2.1 Slowdown in the Mobile Device, Tablet, Laptop/PC Demand

6 PRICING ANALYSIS

- 6.1 DRAM Spot Price (Per GB)

- 6.2 Pricing Trends Analysis

7 MARKET SEGMENTATION

- 7.1 By Architecture

- 7.1.1 DDR3

- 7.1.2 DDR4

- 7.1.3 DDR5

- 7.1.4 DDR2/Others Architectures

- 7.2 By Application

- 7.2.1 Smartphones/Tablets

- 7.2.2 PC/Laptop

- 7.2.3 Datacenter

- 7.2.4 Graphics

- 7.2.5 Consumer Products

- 7.2.6 Automotive

- 7.2.7 Other Applications

- 7.3 By Geography

- 7.3.1 United States

- 7.3.2 Europe

- 7.3.3 Korea

- 7.3.4 China

- 7.3.5 Taiwan

- 7.3.6 Rest of Asia-Pacific

- 7.3.7 Rest of the World

8 COMPETITIVE LANDSCAPE

- 8.1 Company Profiles

- 8.1.1 Samsung Electronics Co. Ltd

- 8.1.2 Micron Technology Inc.

- 8.1.3 SK Hynix Inc.

- 8.1.4 Nanya Technology Corporation

- 8.1.5 Winbond Electronics Corporation

- 8.1.6 Powerchip Semiconductor Manufacturing Corp.

- 8.1.7 Transcend Information Inc.

9 VENDOR MARKET SHARE ANALYSIS

10 INVESTMENT ANALYSIS

11 FUTURE OF THE MARKET

2025年全球DRAM模组与组件市场报告2025年电阻式随机存取记忆体(ReRAM)全球市场报告

2025年全球DRAM模组与组件市场报告2025年电阻式随机存取记忆体(ReRAM)全球市场报告 双列直插式记忆体模组 (DIMM) 市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

双列直插式记忆体模组 (DIMM) 市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测 DRAM 市场规模、份额、成长分析(按类型、应用、最终用户行业、外形规格和地区)- 2025 年至 2032 年行业预测

DRAM 市场规模、份额、成长分析(按类型、应用、最终用户行业、外形规格和地区)- 2025 年至 2032 年行业预测 2032 年 DRAM 市场预测:按类型、技术、应用和地区进行的全球分析

2032 年 DRAM 市场预测:按类型、技术、应用和地区进行的全球分析 DRAM 模组和组件市场(按产品类型、设备尺寸、应用和销售管道)——2025-2030 年全球预测动态随机存取记忆体市场按类型、技术、架构、容量、最终用户产业、分销管道和应用划分——2025 年至 2030 年全球预测2025年动态随机存取记忆体全球市场报告

DRAM 模组和组件市场(按产品类型、设备尺寸、应用和销售管道)——2025-2030 年全球预测动态随机存取记忆体市场按类型、技术、架构、容量、最终用户产业、分销管道和应用划分——2025 年至 2030 年全球预测2025年动态随机存取记忆体全球市场报告 2025-2033 年动态随机存取记忆体市场(按类型、技术、最终用户和地区划分)

2025-2033 年动态随机存取记忆体市场(按类型、技术、最终用户和地区划分) 动态随机存取记忆体 (DRAM) 市场、全球市场规模、成长率与预测 2025-2029

动态随机存取记忆体 (DRAM) 市场、全球市场规模、成长率与预测 2025-2029