|

市场调查报告书

商品编码

1687293

中东和非洲工业空气品质控制系统市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)Middle-East and Africa Industrial Air Quality Control Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

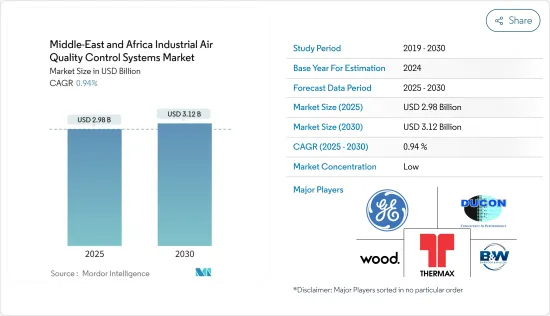

中东和非洲工业空气品质控制系统市场规模预计在 2025 年为 29.8 亿美元,预计到 2030 年将达到 31.2 亿美元,预测期内(2025-2030 年)的复合年增长率为 0.94%。

主要亮点

- 从长远来看,工业基础设施的快速成长加上对空气品质的担忧预计将在预测期内推动中东和非洲空气品质控制系统市场的发展。

- 另一方面,若干宪法障碍和可再生能源的持续使用预计将成为市场研究的主要限制因素。

- 然而,对旧工业厂房进行空气品质控制系统的维修以满足全部区域政府制定的严格监管标准可能会成为未来的机会。

中东和非洲工业空气品质控制系统市场趋势

钢铁可望占较大市场份额

- 无论是采用综合炉、直接还原炉或电弧炉製程生产钢铁,都需要将原料运输、储存、物料输送、加热和转化。所有这些过程都会产生空气排放,主要形式为灰尘(或颗粒物 (PM))、二氧化硫 (SO2) 和氧化亚氮(NOx)。其他小规模排放包括戴奥辛和重金属,通常附着在灰尘颗粒中。

- 炼铁和炼钢作业产生的排放,包括高炉出铁场地板的排放,透过建筑物内的收集点和二次除尘系统(即袋式过滤器、湿式洗涤器、静电除尘器等)进行控制。

- 所有钢铁厂都必须遵守环境法规,这些法规规定限制空气排放。现代生活很大一部分由钢铁构成。基础设施、建筑、机械、电气设备、汽车以及从烹调器具到家具等各种产品都需要大量的钢铁。预计到 2050 年钢铁需求将增加五倍。

- 根据世界钢铁协会统计,截至2022年,该地区粗钢产量主要由土耳其、伊朗、沙乌地阿拉伯、南非、阿尔及利亚和阿联酋等国家主导。

- 中东和非洲地区拥有丰富的高等级铁矿石,具有巨大的钢铁生产潜力。此外,近年来该地区的钢铁产量经历了显着增长,部分原因是钢铁业的投资增加,特别是中东和北非地区。

- 2022年5月,安赛乐米塔尔与茅利塔尼亚铁矿石开采公司SNIM签署了一份不具约束力的谅解备忘录,以评估在茅利塔尼亚联合开发球团厂和直接还原铁生产厂的机会。

- 2022年9月,沙乌地阿拉伯宣布有意实施三个钢铁生产计划,总价值93.2亿美元,年产能为620万吨。同月,埃萨集团宣布将投资 40 亿美元在该国建立一座综合扁平材厂。该厂年钢铁产能为400万吨,预计2025年完工。

- 考虑到该地区钢铁和钢铁业的发展和投资,预计预测期内工业空气品质控制系统的需求将大幅成长。

沙乌地阿拉伯主导市场

- 由于发电、水泥、石油和天然气、金属和其他行业的显着增长,沙乌地阿拉伯很可能成为工业空气品质控制系统最大和成长最快的市场之一。鑑于空气品质控制系统(AQCS)对这些产业至关重要,预计市场在预测期内将以类似的速度成长,从而支持市场的成长。

- 沙乌地阿拉伯是该地区最大的污染国之一,2022 年二氧化碳排放达到约 7.24 亿吨二氧化碳当量。日本是世界主要排放之一,人均二氧化碳排放量约 19 吨。

- 电力有一部分来自石油和天然气等石化燃料,为引入空气品质控制系统等更先进的技术铺平了道路。 2022 年,石化燃料将占沙乌地阿拉伯发电量的约 99.8%,其次是非水力可再生(约 0.2%)。

- 此外,该国继续投资基于石化燃料的发电工程,预计将支持IAQCS市场的需求。例如,2022年9月,韩国斗山能源公司订单了在沙乌地阿拉伯建造一座价值3.83亿美元的热电联产厂的合约。该电厂预计于2025年完工,每小时将产生320兆瓦的电力和314吨蒸气,为贾富拉天然气田提供电力和热能。

- 此外,石油和天然气、采矿和金属行业的快速增长大大增加了空气中的污染物含量。因此,预计将采用工业空气品管系统 (IAQCS)。

- 钢铁业也是空气污染的主要原因之一。钢铁生产的主要能源来源是煤炭,而燃煤会产生大量排放。钢铁厂排放颗粒物(PM2.5 和 PM10)、二氧化碳、硫氧化物、氮氧化物和一氧化碳等空气污染物,使其成为沙乌地阿拉伯工业空气品质控制系统 (IAQCS) 的潜在终端用户。

- 根据世界钢铁协会预测,2022年沙乌地阿拉伯的钢铁产量将达到约910万吨,与前一年同期比较增加4.5%。投资部长表示,到2022年9月,得益于低成本电力和天然气等技术选择以及沙乌地阿拉伯绿色倡议等政府计划,沙乌地阿拉伯钢铁业将有望向绿色和永续产品转型。

- 此外,沙乌地阿拉伯正在建造新的炼油厂和石化综合体。例如,2022年12月,沙乌地阿拉伯石油公司与道达尔能源公司达成最终投资决定,将兴建一座世界级的石化设施。阿米尔综合设施将与位于沙乌地阿拉伯东海岸朱拜勒的现有沙乌地阿美道达尔精製和石化 (SATORP) 炼油厂共同运作、拥有和整合。该石化设施的建设将使SATORP能够将阿美公司提供的炼油厂废气、石脑油、乙烷和天然汽油转化为更高价值的化学品,支持阿美公司的液体转化学品策略。作为该综合计画的一部分,将建造一座年产 165 万吨乙烯的混合进料裂解装置。

- 鑑于目前南非各产业的投资及其价值链的成长,製造业对于该国工业空气品质控制系统的发展至关重要。

中东和非洲工业空气品质控制系统产业概况

中东和非洲工业空气品质控制系统市场分散。主要企业(不分先后顺序)包括 Alfa Laval AB、Aircure、CFW Environmental、Pure Air Solutions 和 ERG Group。

CFW Environmental 的空气污染控制系统产品组合基于多种技术,以满足众多工业应用的要求和特定属性。此外,该公司还提供全面的服务,从最初的咨询到售后服务。我们也致力于在空气污染控制系统的设计和製造方面采用国际最佳实践。为了在全球市场保持永续,我们透过市场研究和创新产品开发评估客户需求,不断改进我们的产品。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究范围

- 市场定义

- 调查前提

第 2 章执行摘要

第三章调查方法

第四章 市场概况

- 介绍

- 2028 年市场规模与需求预测(美元)

- 最新趋势和发展

- 政府法规和政策

- 市场动态

- 驱动程式

- 下游产业需求

- 限制因素

- 采用可再生和清洁能源来源

- 驱动程式

- 供应链分析

- 波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争强度

第五章 市场区隔

- 类型

- 静电除尘设备(ESP)

- 排烟脱硫(FGD) 和洗涤器

- 选择性催化还原 (SCR)

- 袋滤式集尘器

- 其他的

- 应用

- 发电业

- 水泥工业

- 化学品和肥料

- 钢铁业

- 汽车

- 石油和天然气

- 其他用途

- 排放气体

- 氮氧化物(NOX)

- 硫氧化物(SO2)

- 颗粒物 (PM)

- 地区

- 沙乌地阿拉伯

- 南非

- 阿尔及利亚

- 其他中东和非洲地区

第六章 竞争格局

- 併购、合资、合作、协议

- 主要企业策略

- 公司简介

- Alfa Laval AB

- Aircure

- CFW Environmental

- Pure Air Solutions

- The ERG Group

- Redecam Group SpA

- Donaldson Company Inc.

- Durr AG

- FLSmidth & Co. A/S

- Siloxa Engineering AG

第七章 市场机会与未来趋势

- 本公司开发新技术空气品管系统

The Middle-East and Africa Industrial Air Quality Control Systems Market size is estimated at USD 2.98 billion in 2025, and is expected to reach USD 3.12 billion by 2030, at a CAGR of 0.94% during the forecast period (2025-2030).

Key Highlights

- Over the longer term, a surge in industrial infrastructure, coupled with air quality issues, is expected to drive the market for air quality control systems in Middle-East and Africa over the forecast period.

- On the other hand, several constitutional barriers and growth in renewable energy usage which is pollution-free are expected to act as major restraints for the market studied.

- Nevertheless, retrofitting of old industrial plants with air quality control system to meet stringent regulatory norms set up by governments across the region is likely to acts as an opportunity in the future.

MEA Industrial Air Quality Control Systems Market Trends

Iron and Steel is Expected to Have Significant Share in the Market

- Steel, produced by either integrated, direct reduced iron, or electric arc furnace route, requires transportation, storage, handling, heating, and transformation of raw materials. All these processes have the potential to generate emissions into the air, primarily in the form of dust (or particulate matter (PM), sulfur dioxide (SO2), and nitrous oxides (NOx). Other emissions generated in small quantities include dioxins and heavy metals, typically attached to dust particles.

- Emissions from iron and steelmaking operations, including cast house floor emissions from blast furnaces, are controlled via secondary dedusting systems (i.e., bag filters, wet scrubbers, ESPs, etc.) with a collection point inside the building.

- All steel plants are subject to environmental regulation, which sets the requirements to restrict emissions into the air. A large portion of modern life is comprised of steel. Infrastructure, buildings, machinery, electrical equipment, automobiles, and various products, from cookware to furniture, require large amounts of iron and steel. The steel demand is estimated to increase by five times by 2050.

- According to the World Steel Association statistics, as of 2022, the crude steel production in the region is mainly dominated by countries like Turkey, Iran, Saudi Arabia, South Africa, Algeria, and the United Arab Emirates, amongst others.

- The Middle East and Africa region has a very high potential for steel production due to the availability of high-grade iron ore. Additionally, in recent years steel production in the area has witnessed significant growth, mainly driven by increasing investments in the sector, especially in the Middle East and North Africa.

- In May 2022, ArcelorMittal signed a non-binding Memorandum of Understanding with SNIM, an iron ore mining company based in Mauritania, to evaluate an opportunity to jointly develop a pelletization plant and a direct reduced iron production plant in Mauritania.

- In September 2022, Saudi Arabia announced that it intends to implement three steel production projects worth USD 9.32 billion with a total production capacity of 6.2 million tons annually. In the same month, Essar Group announced it is looking to invest USD 4 billion in setting up an integrated flat steelworks plant in the country. The plant will have a steel production capacity of 4 million tonnes annually and will be completed by 2025.

- Considering the developments and investments in the steel and iron industry in the region, the demand for industrial air quality control systems is expected to witness significant growth during the forecast period.

Saudi Arabia to Dominate the Market

- Due to the significant growth in its power generation, cement, oil & gas, metal, and other sectors, Saudi Arabia is likely to be one of the largest and fastest-growing markets for industrial air quality control systems. The market is expected to grow at a similar rate during the forecast period, supporting the market growth, as air quality control systems (AQCS) are crucial to these industries.

- Saudi Arabia is one of the largest polluters in the region, with CO2 emissions amounting to approximately 724 million tonnes of CO2 equivalent in 2022. The country is one of the largest producers of CO2 emissions per capita worldwide, at about 19 metric tons per person.

- A significant share of power generated from fossil fuels, such as oil and gas, paving the way for more advanced technologies, such as air quality control systems, to be implemented. In 2022, Saudi Arabia's power generation was dominated by fossil fuels, which account for approximately 99.8% of the electricity generated, followed by non-hydro renewable sources (~0.2%).

- Further, the country continues to invest in fossil fuel-based power projects, which are expected to support the demand for the IAQCS market. For instance, in September 2022, South Korean company Doosan Enerbility was awarded a contract to construct a combined heat and power plant in Saudi Arabia valued at USD 383 million. Upon completion of the construction work scheduled for 2025, the plant will generate 320 MWs of electricity and 314 tons per hour of steam to supply electricity and heat to the Jafurah gas field.

- Further, the rapid growth of the oil & gas, mining, and metal sectors has resulted in a massive increase in the levels of pollutants in the air. Accordingly, the adoption of industrial air quality control systems (IAQCS) is anticipated.

- The Iron and Steel industry is another significant contributor to air pollution. Steel mainly requires coal for energy, so considerable emissions are caused by coal combustion. Steel plants emit air pollutants, such as particulate matter (PM2. 5 and PM10), carbon dioxide, sulfur oxides, nitrogen oxides, carbon monoxide, etc. hence, being a potential end-user for the industrial air quality control systems (IAQCS) in Saudi Arabia.

- According to World Steel Association, in 2022, steel production in Saudi Arabia was approximately 9.1 million, an increase of 4.5% from the previous year. In September 2022, according to the minister of investment, In Saudi Arabia, the iron and steel industry is well positioned for the transition to green and sustainable products due to its technology options, such as low-cost electricity and natural gas, and government programs, such as the Saudi Green Initiative.

- Further, the country has been constructing new refineries and petrochemical complexes. For instance, in December 2022, Saudi Arabian Oil Company and TotalEnergies reached a final investment decision on constructing a world-scale petrochemical facility. The "Amiral" complex is going to be operated, owned, and integrated with the existing Saudi Aramco Total Refining and Petrochemical Co. (SATORP) refinery located on Saudi Arabia's eastern coast, Jubail. With the construction of the petrochemical facility, SATORP will be able to convert its refinery off-gases, naphtha, ethane, and natural gasoline supplied by Aramco into higher-value chemicals, thus supporting Aramco's liquids-to-chemicals strategy. As part of the complex, there will be a mixed feed cracker capable of producing 1.65 million tons of ethylene annually, a first of its kind in the region that will be integrated with a refinery.

- Considering the current investments in the various industries and the increased growth of its value chain in South Africa, the manufacturing sector is critical to the growth of the country's industrial air quality control systems.

MEA Industrial Air Quality Control Systems Industry Overview

The Middle-East and Africa industrial air quality control systems market is fragmented. some of the key players (in no particular order) include Alfa Laval AB, Aircure, CFW Environmental, Pure Air Solutions, and ERG Group, among others.

CFW Environmental's portfolio of air pollution control systems is based on a range of technologies to comply with the numerous industrial application requirements and specific attributes. Furthermore, the company provides comprehensive services, ranging from first inquiry to after-sales service. It also focused on adopting international best practices in designing and manufacturing air pollution control systems. To remain sustainable in the global market, the products are constantly enhanced by evaluating customers' requirements through market research and innovative product development.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2028

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Demand from the Downstream Industry

- 4.5.2 Restraints

- 4.5.2.1 Adoption of Renewable and Clean Energy Sources

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Electrostatic Precipitators (ESP)

- 5.1.2 Flue Gas Desulfurization (FGD) and Scrubbers

- 5.1.3 Selective Catalytic Reduction (SCR)

- 5.1.4 Fabric Filters

- 5.1.5 Others

- 5.2 Application

- 5.2.1 Power Generation Industry

- 5.2.2 Cement Industry

- 5.2.3 Chemicals and Fertilizers

- 5.2.4 Iron and Steel Industry

- 5.2.5 Automotive Industry

- 5.2.6 Oil & Gas Industry

- 5.2.7 Other Applications

- 5.3 Emissions

- 5.3.1 Nitrogen Oxides (NOX)

- 5.3.2 Sulphur Oxide (SO2)

- 5.3.3 Particulate Matter (PM)

- 5.4 Geography

- 5.4.1 Saudi Arabia

- 5.4.2 South Africa

- 5.4.3 Algeria

- 5.4.4 Rest of Middle East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Alfa Laval AB

- 6.3.2 Aircure

- 6.3.3 CFW Environmental

- 6.3.4 Pure Air Solutions

- 6.3.5 The ERG Group

- 6.3.6 Redecam Group SpA

- 6.3.7 Donaldson Company Inc.

- 6.3.8 Durr AG

- 6.3.9 FLSmidth & Co. A/S

- 6.3.10 Siloxa Engineering AG

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 New Technology Air Quality Control System Developments by Various Companies

空气清净机市场预测至2034年-按产品、技术、应用、最终用户和地区分類的全球分析2034年自动化室内空气品质监测舱市场预测-按产品类型、部署模式、感测器类型、连接技术、安装模式、最终用户和地区分類的全球分析

空气清净机市场预测至2034年-按产品、技术、应用、最终用户和地区分類的全球分析2034年自动化室内空气品质监测舱市场预测-按产品类型、部署模式、感测器类型、连接技术、安装模式、最终用户和地区分類的全球分析 2026年全球空气品质管理系统市场报告

2026年全球空气品质管理系统市场报告 全球环境颗粒物空气监测器市场(按技术、产品、颗粒尺寸、应用和最终用户划分)预测(2026-2032)

全球环境颗粒物空气监测器市场(按技术、产品、颗粒尺寸、应用和最终用户划分)预测(2026-2032) 2035年船舶静电集尘器市场分析及预测:按类型、产品、服务、技术、组件、应用、材料类型、最终用户和功能划分2026年全球燃烧排放分析仪市场报告

2035年船舶静电集尘器市场分析及预测:按类型、产品、服务、技术、组件、应用、材料类型、最终用户和功能划分2026年全球燃烧排放分析仪市场报告 室内空气品质 (IAQ) 监测系统市场规模、占有率、成长及全球产业分析:依类型、应用和地区划分的洞察与预测 (2026–2034)2026年全球二氧化碳(CO2)通风控制器市场报告全球空气排放管理软体市场(依最终用户产业、部署模式、组件、公司规模和定价模式划分)预测(2026-2032年)空气品管系统市场(按产品类型、技术、应用、最终用户和分销管道)—2025-2032 年全球预测

室内空气品质 (IAQ) 监测系统市场规模、占有率、成长及全球产业分析:依类型、应用和地区划分的洞察与预测 (2026–2034)2026年全球二氧化碳(CO2)通风控制器市场报告全球空气排放管理软体市场(依最终用户产业、部署模式、组件、公司规模和定价模式划分)预测(2026-2032年)空气品管系统市场(按产品类型、技术、应用、最终用户和分销管道)—2025-2032 年全球预测