|

市场调查报告书

商品编码

1687379

北美蒸发冷却:市场占有率分析、行业趋势和统计数据、成长预测(2025-2030 年)NA Evaporative Cooling - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

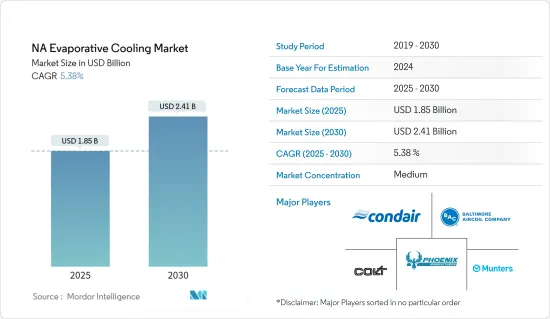

北美蒸发冷却市场规模预计在 2025 年为 18.5 亿美元,预计到 2030 年将达到 24.1 亿美元,预测期内(2025-2030 年)的复合年增长率为 5.38%。

主要亮点

- 北美正大力推动永续能源管理。因此,传统空调不是一个可行的选择。这一关键因素推动了蒸发冷却的普及,使其成为冷却大型开放空间和区域的最有效选择。

- 在该地区,尤其是美国,已经实施了各种政府标准,透过蒸发冷却技术实现商业和工业部门的高效能源利用。因此,加拿大自然资源部正在考虑提高蒸发冷却产品的最低能源性能标准 (MEPS),以使其与美国此类产品的 MEPS 保持一致。蒸发冷却是传统冷却技术的一种更可取的替代方案,因为它利用了透过蒸发水来降低空气温度的自然过程。

- 除了多功能(它们可用于开放环境中的冷却、空气净化和通风)之外,蒸发冷却器还为最终用户提供了几个关键优势,包括成本效益、节能、低维护和操作要求。因此,由于永续能源法规的发展,技术进步及其相对于传统冷却技术的优势正在推动该地区的市场研究。

- 美国的另一个关键驱动因素是资料中心越来越多地采用蒸发冷却器。由于数位内容、巨量资料和电子商务的采用,该国对资料中心的需求正在快速增长。必须始终保持这些设施正常运转,特别是对于在该领域运营的跨国公司而言。除了可靠性之外,该行业还在寻求各种节能解决方案,以帮助降低营运成本和资料中心营运的碳排放。

- 然而,蒸发冷却技术对外部气候的依赖可能是一个限制整体市场成长的主要问题。

- 新冠疫情的突然爆发导致多个国家采取了严格的封锁措施,造成许多製造工厂暂时关闭,从而导致蒸发冷却系统的需求波动。在后 COVID-19 时代,预计市场将在整个预测期内享有充足的成长机会,尤其是由于该地区对资料中心的需求不断增加。

北美蒸发冷却市场趋势

商业部门预计将大幅成长

- 商业机构面临维持最佳气候条件的巨大压力,特别是为了保护客户和员工的健康和福祉。医院、电影院、机场、饭店、购物中心等商业场所通常会根据其通风和冷却需求同时采用空调和蒸发冷却器。

- 此外,蒸发式空气冷却器主要用于商业场所,作为空调的替代品。除此之外,由于空调的安装成本相当高,越来越多的中小型企业采用空调作为替代方案,预计这也将推动市场发展。

- 近期资料中心营运需求的激增使得 HVAC 公司必须为资料中心提供经济高效的解决方案。资料中心解决方案供应商正在寻找能够减少整体排放的可靠解决方案,这极大地推动了市场成长。

- 典型的资料中心通常需要大约 0.5-50MW 的冷却能力,但 ASHRAE 指南的最新变更已将允许的动作温度提高到 27°C。这是资料中心对蒸发式空气冷却器整体需求的主要驱动因素。此外,这些产品不使用冷媒或氟碳化合物,最大限度地减少了最终用户应用的碳排放。

- 根据美国人口普查局的数据,今年商业建筑投资达到约1,150亿美元。美国最初建造的商业建筑大多为仓库和私人办公室。同时,去年的总额约为 945.5 亿美元,显示商业建筑领域显着成长。该地区商业建筑行业的成长预计将成倍地推动市场成长。

直接冷却预计将占主导地位

- 直接蒸发式空气冷却是最古老、最简单、最广泛使用的蒸发式空气冷却类型。该系统的风扇透过潮湿的海绵状垫片吸入热空气,然后将产生的冷空气直接或透过管道分布到室内空间。随着空气中的热量蒸发水分,温暖干燥的空气变成凉爽潮湿的空气。

- 直接蒸发冷却系统主要适用于需要去除大量热负荷的应用,也可以为此目的使用外部空气。主要应用包括对舒适度要求较低的住宅、商用厨房和仓库。因此,系统需求取决于最终使用者及其指定的操作性能要求。

- 此外,直接蒸发冷却(DEC)通常是资料中心冷却最节能的方法,因为外部空气透过蒸发直接冷却并用于调节内部气候。因此,区域资料中心总数的增加预计将倍增市场成长。

- 根据Cloudscene的数据,截至2022年1月,美国共有2,701个资料中心,德国则位居第二,拥有487个资料中心。就资料中心总数而言,英国排名第三,拥有456个资料中心,中国位居第三,拥有443个资料中心。预计美国大量资料中心的存在将在整个预测期内加速市场成长。

- 例如,ST Engineering宣布将于2022年7月推出其新型Airbitat DC冷却系统,标誌着其进入资料中心冷却市场。 Airbitat 直流冷却系统是该公司城市环境解决方案 (UES) 业务的一项创新,为热带地区的资料中心提供强大的预冷功能,与传统的冷却器系统相比,每年可实现 20% 以上的净节能。

北美蒸发冷却产业概况

北美蒸发冷却市场处于半静态状态。市场竞争激烈,许多全球大公司都进入该市场。从市场占有率来看,目前市场主要被几家大公司占据。这些占据了绝对市场份额的大公司正致力于扩大海外基本客群。这些公司正在利用策略合作计划来最大限度地提高市场占有率并提高盈利。

- 2023 年 11 月,美卓宣布推出增强型蒸发冷却水塔。这种创新的解决方案透过蒸发有效地冷却了热的外炉气体。该塔通常与高温静电除尘设备或袋式除尘器配合使用,可有效将气体温度从约 600-700°C 降低至约 200-350°C。值得注意的是,塔在干状态下运行,任何添加的水都会蒸发。塔内小液滴的快速蒸发大大减少了所需的停留时间和长度,并确保了完全蒸发。

- 2023 年 3 月,总部位于凤凰城的蒸发冷却系统製造商 Air2O 获得 EREN 集团 1,410 万美元的投资。该投资将用于加强供应链物流、营运和劳动力。事实证明,这项创新解决方案能够帮助资料中心实现低于 1.1 的 PUE。此外,我们也成功开发并获得专利的智慧控制系统,可适应不同应用不断变化的外部和内部气候条件。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概览

- 产业吸引力-波特五力分析

- 买家的议价能力

- 消费者议价能力

- 新进入者的威胁

- 竞争对手之间的竞争

- 替代品的威胁

- 价值链/供应链分析

- 评估宏观经济因素对产业的影响

第五章市场动态

- 市场驱动因素

- 资料中心采用蒸发冷却器

- 对经济高效的冷却解决方案的需求

- 市场限制

- 对外部气候的依赖

第六章市场区隔

- 按冷却方式

- 直接冷却

- 间接

- 两阶段

- 按应用

- 住宅

- 工业的

- 商业的

- 对于牲畜

- 其他的

- 按国家

- 美国

- 加拿大

第七章竞争格局

- 公司简介

- Condair Group AG

- Baltimore Aircoil Company Inc.(BAC)

- Munters Group AB

- Colt Group

- Phoenix Manufacturing Inc.

- Delta Cooling Towers Inc.

- SPX Cooling Technologies

- Bonaire Group(Celi Group)

第八章投资分析

第九章市场趋势与未来机会

The NA Evaporative Cooling Market size is estimated at USD 1.85 billion in 2025, and is expected to reach USD 2.41 billion by 2030, at a CAGR of 5.38% during the forecast period (2025-2030).

Key Highlights

- North American region has been witnessing a surge in the overall number of initiatives for sustainable energy management. Hence, traditional air conditioning is not a feasible option. This crucial factor is boosting the popularity of evaporative cooling, which is becoming the most effective option for cooling large open spaces or areas.

- Various government standards have been implemented within the region, especially in the United States, for efficient energy utilization across commercial and industrial sectors with evaporative cooling techniques. Therefore, Natural Resources Canada is considering a rise in the minimum energy performance standards (MEPS) for evaporative-cooled products to align with the MEPS in the United States for those classes of products. As evaporative cooling utilizes a natural process, namely reducing air temperature by evaporating water on it, they are the preferred alternative over traditional cooling technologies.

- Evaporative coolers offer several key benefits to end users, including cost-effectiveness, energy savings, low maintenance, and operational requirements, besides being multifunctional (can be used in an open environment for cooling, air purification, and ventilation). Thus, owing to favorable regulations for sustainable energy across the region, advancements in technologies and their benefits compared to traditional cooling techniques are significantly driving the market studied.

- The other significant driver for the United States is the rise in the adoption of evaporative coolers in data centers. The demand for data centers is increasing at a rapid pace in the country, with the adoption of digital content, Big Data, and e-commerce. Keeping these facilities constantly functional is mandatory, especially for multinational companies operating in this space. In addition to reliability, the industry is seeking various energy-efficient solutions that have the potential to lower operational costs and reduce carbon emissions from data center operations.

- However, the dependency of evaporative cooling technologies on the external climate could be a major point of concern that can overall limit the growth of the market.

- The sudden COVID-19 pandemic outbreak caused the adoption of strict lockdown laws across several nations, which has mainly led to the temporary closure of many manufacturing facilities and fluctuations in demand for evaporative cooling systems. During the post-COVID-19 scenario, the market is expected to witness ample opportunities for growth throughout the forecast period significantly, especially due to the rise in the demand for the data center within the region.

North America Evaporative Cooling Market Trends

Commercial Sector is Expected to Register a Significant Growth

- Commercial establishments are greatly required to maintain optimal climatic conditions, especially to protect the health and well-being of clients and employees. Commercial entities, such as hospitals, movie theaters, airports, hotels, and malls, among others, generally employ both air conditioners and evaporative coolers depending upon the ventilation and cooling requirements of an enclosure.

- Moreover, evaporative air coolers are majorly used in commercial establishments' facilities as alternatives to air conditioners. Apart from this, the market is anticipated to be driven by the growing adoption of small to medium enterprises instead of air conditioners, as the cost of air conditioning setup can be significantly high.

- Due to the recent surge in demand for data center operations, it has become imperative for HVAC companies to provide cost and energy-efficient solutions for data centers. Data center solution providers are mostly on the lookout for reliable solutions that are able to cut down overall emissions, thereby driving the market's growth considerably.

- A normal data center usually requires about 0.5 to 50MW of cooling capacity, and due to recent changes in ASHRAE guidelines, the permissible operating temperature has been increased to 27°C. This has been a significant driver for the overall demand for evaporative air coolers in data centers. Additionally, these products do not make utilization of any refrigerants or CFCs, which could further minimize the overall carbon footprint for the end-user applications.

- As per US Census Bureau, the value of commercial construction that has been put in place reached a landmark of around USD 115 billion this year. Warehouses and private offices were the most common type of commercial construction started in the United States. In contrast, the total count was around USD 94.55 billion last year, indicating significant growth in the commercial construction sector. This rise in the commercial construction sector within the region is likely to drive the market's growth exponentially.

Direct Cooling is Expected to Hold Major Share

- Direct evaporative air cooling is the oldest, simplest, and most widely used type of evaporative cooling. The fan in the system pulls hot air through a dampened sponge-like pad and distributes the resulting cool air to the interior space either directly or through ducts. Warm, dry air is converted to cool, moist air as the heat in the air evaporates the water.

- Direct evaporative cooling systems are mainly suitable for applications with large heat-load removal needs and those open to using outside air to accomplish this. The major areas of their applications include residential sectors, commercial kitchens, and warehouses where comfort requirements are more relaxed. Hence, the system requirement depends on the end users and the specified operational performance requirements.

- Moreover, Direct evaporative cooling (DEC) is typically the most energy-efficient method to cool a data center, as the outside air is directly cooled through evaporation and is then used to moderate the internal climate. Hence, the rise in the overall count of regional data centers is expected to amplify the market's growth exponentially.

- As per Cloudscene, as of January 2022, the total count of data centers in the United States was 2,701 data centers whereas Germany ranked second with an overall count of 487 data centers. The United Kingdom ranked third among countries in terms of the total number of data centers, with 456, while China recorded 443. This possession of a significant number of data centers in the United States is expected to amplify the market's growth throughout the forecast period.

- For instance, In July 2022, ST Engineering declared the launch of its new Airbitat DC Cooling System, thereby marking its entry into the data center cooling market. The Airbitat DC Cooling System, an innovation by its Urban Environment Solutions (UES) business, delivers powerful pre-cooling for tropical data centers, achieving annual net energy savings of more than 20% over conventional chiller systems alone.

North America Evaporative Cooling Industry Overview

The North American evaporative cooling market is semi-consolidated. The market is competitive and consists of various major global players. Based on market share, few of the major players currently dominate the market. These significant players with prominent shares in the market are focusing on expanding their customer base across foreign countries. These companies leverage strategic collaborative initiatives to maximize their market share and increase profitability.

- November 2023: Metso announced the launch of its enhanced evaporative cooling tower. This innovative solution efficiently cools hot furnace off-gases through evaporation. The tower, typically used in conjunction with a hot electrostatic precipitator or bag filter, effectively lowers the gas temperature from approximately 600-700°C to about 200-350°C. It is important to note that the tower operates dryly, meaning all added water evaporates. The rapid evaporation of small droplets in the tower significantly reduces the required retention time and length, ensuring complete evaporation.

- March 2023: Air2O, a Phoenix-based manufacturer of evaporated cooling systems, has received a generous investment of USD 14.1 million from EREN Groupe. This investment will be utilized to enhance our supply chain logistics, operations, and workforce. We are proud to announce that our innovative solutions have proven to achieve a PUE of lower than 1.1 in Data Centers. Furthermore, we have successfully developed and patented intelligent control systems that adapt to changing external and internal climate conditions across various applications.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Buyers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Intensity of Competitive Rivalry

- 4.2.5 Threat of Substitutes

- 4.3 Value Chain / Supply Chain Analysis

- 4.4 Assessment of Impact of Macro-economic Factors on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Adoption of Evaporative Coolers in Data Centers

- 5.1.2 Demand for Cost-effective Cooling Solution

- 5.2 Market Restraints

- 5.2.1 Dpendency on External Climate

6 MARKET SEGMENTATION

- 6.1 By Cooling

- 6.1.1 Direct

- 6.1.2 Indirect

- 6.1.3 Two-Stage

- 6.2 By Application

- 6.2.1 Residential

- 6.2.2 Industrial

- 6.2.3 Commercial

- 6.2.4 Confinement Farming

- 6.2.5 Other Applications

- 6.3 By Country

- 6.3.1 United States

- 6.3.2 Canada

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Condair Group AG

- 7.1.2 Baltimore Aircoil Company Inc. (BAC)

- 7.1.3 Munters Group AB

- 7.1.4 Colt Group

- 7.1.5 Phoenix Manufacturing Inc.

- 7.1.6 Delta Cooling Towers Inc.

- 7.1.7 SPX Cooling Technologies

- 7.1.8 Bonaire Group (Celi Group)

8 INVESTMENT ANALYSIS

9 MARKET TRENDS AND FUTURE OPPORTUNITIES

蒸发冷却市场规模、份额、趋势和预测:按冷却方式、销售管道、应用和地区划分,2026-2034年

蒸发冷却市场规模、份额、趋势和预测:按冷却方式、销售管道、应用和地区划分,2026-2034年 蒸发冷却市场:按产品类型、最终用户、分销管道和应用分類的全球市场预测,2026-2032年高压雾化加湿系统市场依产品类型、最终用途产业、应用及通路划分,全球预测(2026-2032)

蒸发冷却市场:按产品类型、最终用户、分销管道和应用分類的全球市场预测,2026-2032年高压雾化加湿系统市场依产品类型、最终用途产业、应用及通路划分,全球预测(2026-2032) 2026年全球蒸发冷却市场报告

2026年全球蒸发冷却市场报告 蒸发冷却市场规模、份额和成长分析(按冷却类型、最终用途、容量范围、部署类型和地区划分)-2026-2033年产业预测

蒸发冷却市场规模、份额和成长分析(按冷却类型、最终用途、容量范围、部署类型和地区划分)-2026-2033年产业预测 被动辐射冷却膜:全球市场份额和排名、总收入和需求预测(2025-2031 年)

被动辐射冷却膜:全球市场份额和排名、总收入和需求预测(2025-2031 年) 蒸发冷却市场 - 全球产业规模、份额、趋势、机会和预测,按冷却类型、应用、配销通路、地区和竞争进行细分,2020-2030 年预测

蒸发冷却市场 - 全球产业规模、份额、趋势、机会和预测,按冷却类型、应用、配销通路、地区和竞争进行细分,2020-2030 年预测 全球被动辐射冷却薄膜市场考察,预测至 2031 年

全球被动辐射冷却薄膜市场考察,预测至 2031 年 蒸发冷却:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)

蒸发冷却:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年) 蒸发冷却全球市场 2024-2028

蒸发冷却全球市场 2024-2028