|

市场调查报告书

商品编码

1687400

医疗保健领域的半导体应用:市场占有率分析、行业趋势和成长预测(2025-2030 年)Semiconductor Applications in Healthcare - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

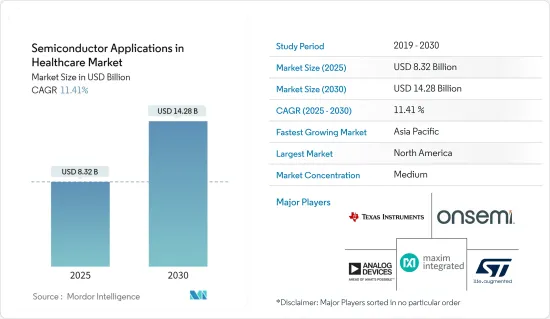

医疗保健市场中的半导体应用规模预计在 2025 年为 83.2 亿美元,预计到 2030 年将达到 142.8 亿美元,预测期内(2025-2030 年)的复合年增长率为 11.41%。

医疗保健行业使用的大部分设备都依赖半导体製造技术。感测器、积体电路 (IC)、分离式元件、记忆体和电源管理元件等半导体元件正在推动医学成像、临床诊断和治疗以及携带式和家庭医疗保健等领域的各种应用。

主要亮点

- 市场正在见证医疗设备的多种发展,对先进半导体的需求预计将上升。可携式透析设备一直是市场驱动力,疫情过后,百特等供应商生产的机器已获得美国食品药物管理局(FDA)批准,可直接连接患者的处方笺和治疗资料电子健康记录。这些发展正在推动对先进半导体的需求。

- 远距病人监护设备的使用不断增加、先进的诊断和治疗方法以及非传染性疾病的高发性等因素预计也将推动医疗保健市场半导体的成长。例如,美国癌症协会预测,2024年美国将诊断出234,580例新发生肺癌和支气管癌病例。据报道,其中佛罗里达州的数量最多。有多种治疗方案可供选择,但现代冷冻手术技术可以实现完全康復。

- 此外,儘管癌症预防和治疗不断取得进展,但癌症负担仍在增加,根据国际癌症研究机构的《世界癌症报告》,预计2018年至2040年间全球癌症病例数将增加50%。 IARC 在 2000 年发现 1,010 万例新发癌症病例,2018 年发现 1,810 万例,并预测到 2040 年这一数字将上升到每年 2,700 万例。

- 大量医疗保健专业人员和医院仍在使用各种需要达到当前技术标准的传统硬件,并且无法升级到更新的技术。此外,全球二手医疗技术市场庞大,对此类设备的更大可用性和资金筹措需求阻碍了新技术的发展和采用。

- 俄乌战争正在影响半导体供应链。俄罗斯和乌克兰是生产半导体和电子元件及一系列设备的重要原料供应国。衝突可能扰乱供应链,造成原材料短缺和价格上涨,影响製造商并导致最终用户成本上升。

- 此外,根据乌克兰投资局的数据,铜价在 2022 年 3 月初上涨至 10,845 美元/吨,但 2023 年有所回落。俄罗斯与乌克兰之间的战争、能源成本的上升以及欧洲更严格的排放标准被认为是铜短缺持续的主要原因。

医疗保健领域半导体应用的市场趋势

医疗图像成为成长最快的应用

- 医疗图像领域包括电脑断层扫描、磁振造影、X射线成像和正电子发射断层扫描,医疗图像用于诊断各种疾病,包括癌症和慢性病。

- 随着技术进步和医疗保健领域的日益普及,医疗辐射设备和技术取得了许多进步。

- 介入性X射线成像在过去几年中取得的关键进展之一是专注于核心和支援技术,以便在不增加辐射剂量的情况下提供高品质、高解析度的影像。这是西门子的 Artis Q、飞利浦的 ClarityIQ 和 Q.zen 技术、通用电气医疗的影像引导系统 (IGS) 和东芝的 Infinix Elite 产品线等技术进步的关键驱动力。这些正在推动对先进半导体的需求。

- 由于对诊断放射学的关注度不断提高以及慢性病负担的不断加重,医疗设备业每年进行的影像和诊断测试数量不断增加。

- 根据联合国世界人口展望报告,65岁及以上人口数量正稳定增加。预计到2050年,全世界老年人口(60岁以上)数量将增加至20亿,其中80%将生活在中低收入国家。因此,老年人口的增加以及整形外科和心血管手术数量的增加预计将进一步推动医学影像在医疗保健应用中的应用。

- 在医疗领域,牙科应用需要更小、更短的扫描。据李施德林专业口腔护理公司称,口腔疾病是全球最严重的健康问题,影响39亿人。因此,牙科领域对X光成像的主要需求预计将增加,从而推动所调查市场对各种半导体的需求。

- 此外,一些公司已经推出了与X光影像分析软体相关的产品,从而对该领域的成长产生了积极影响。例如,2024 年 1 月,Carestream Health 推出了 DXR-Excel Plus。 DXR-Excel Plus 是一种二合一系统,适用于透视和一般 X 光检查,可轻鬆为各种检查提供即时影像,同时提供有助于改善使用者、病患和管理员体验的功能。

亚太地区可望成为成长最快的市场

- 预计预测期内亚太地区将经历健康扩张。关键成长要素包括增加对研究和研发中心的投资、政府计划以及促进 IT 和医疗设备及器械市场的政策。此外,该地区也是全球最大的半导体市场。这是由于中国、日本、印度、台湾、韩国和新加坡等国所致。这些国家正在为医疗保健产业的发展做出贡献。

- 在日本,企业正在投资医疗保健领域,以打造具有前瞻性的业务并实现永续成长。例如,FUJIFILM Holdings推出了新的中期经营计划“VISION2023”,涵盖从2022年3月结束的财年(2021财年)到2023财年的三年时间。根据“VISION2023”,该公司将在三年内共投资8.491兆日元,以加速业务成长,主要在医疗保健和高性能材料业务方面。医疗保健业务将扩大为销售额和营业利润最大的业务领域,并建立实现永续成长的稳健业务基础。

- 此外,中国国务院于2014年发布的《国家积体电路产业发展指南》提出了2030年在半导体产业各个领域成为世界领导者的目标。此外,「中国製造2025」倡议也强调了半导体製造对中国未来经济和社会的重要性。此外,该国在医疗保健领域的支出为 5,740 亿美元。

- 此外,韩国是受调查市场中领先的消费者、投资者和创新者之一。韩国在半导体产业和医疗设备製造业的强大地位有助于增强该国在全球半导体医疗保健市场的地位。政府在发展国内市场方面也发挥关键作用,主要是为了推动经济发展。

- 此外,该国正在利用製药业的人工智慧进一步扩大其市场。据政府称,韩国人工智慧主导的药物开发市场预计每年增长 40%,到 2024 年达到 39 亿美元。

医疗保健市场中的半导体应用概述

预计预测期内医疗保健半导体市场将以中等速度成长。德州仪器公司、安森美半导体公司、美国模拟装置公司、美信整合产品公司和意法半导体等市场竞争对手正在采取联盟和收购等策略来加强其产品组合併获得永续的竞争优势。

- 2023 年 11 月,Miller 宣布了收购 Sentron 的策略计划,Sentron 是一家压力和 pH 感测器的全整合製造商,旨在透过压力感测器技术增强医学理解并实现科学发现。

- 2023 年 11 月杜邦 Livo Healthcare 宣布与意法半导体合作,将意法半导体的多功能微型感测器和控制电子设备融入杜邦的柔性贴片设计中,开发用于远端生物讯号监测的新型智慧穿戴装置概念。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买家的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 产业价值链分析

- 评估主要宏观趋势的市场影响

第五章 市场动态

- 市场驱动因素

- 连网医疗连网型设备的成长

- 医疗保健需要先进的半导体技术

- 市场限制

- 现有硬体的更新和最终产品设备成本的上升

第六章 市场细分

- 按应用

- 医学影像

- 消费医疗电子产品

- 诊断性病患监测和治疗

- 医疗设备

- 按组件

- 积体电路

- 模拟

- 逻辑

- 记忆

- 微型组件

- 光电子

- 感应器

- 分立元件

- 积体电路

- 按地区

- 北美洲

- 欧洲

- 亚洲

- 澳洲和纽西兰

- 拉丁美洲

- 中东和非洲

第七章 竞争格局

- 公司简介

- Texas Instruments Incorporated

- ON Semiconductor Corporation

- Analog Devices Inc.

- Maxim Integrated Products Inc.

- STMicroelectronics

- NXP Semiconductors NV

- Broadcom Inc.

- ams Osram

- Vishay Intertechnology Inc.

- Renesas Electronics Corporation

第八章投资分析

第九章:市场的未来

The Semiconductor Applications in Healthcare Market size is estimated at USD 8.32 billion in 2025, and is expected to reach USD 14.28 billion by 2030, at a CAGR of 11.41% during the forecast period (2025-2030).

Many devices used in the healthcare industry rely on semiconductor manufacturing technology. Semiconductor components, such as sensors, integrated circuits (ICs), discrete devices, and memory power management devices, are driving various applications in fields, including medical imaging, clinical diagnostics and therapy, and portable and home healthcare.

Key Highlights

- The market is witnessing various developments in medical devices that are expected to increase the need for advanced semiconductors. Portable dialysis machines are gaining market traction, and vendors like Baxter have received FDA clearance post-pandemic that is designed to directly connect electronic medical records for patients' prescriptions and treatment data. Such developments are driving the need for advanced semiconductors.

- Factors like increasing use of remote patient monitoring devices, development in diagnostic and treatment modalities, and high incidence of non-communicable diseases are also expected to drive the growth of the semiconductor in the healthcare market. For instance, the American Cancer Society predicts that there will be 234,580 new cases of lung and bronchus cancer diagnosed in the United States overall in 2024. The state of Florida is reported to have the most significant number of these instances. Even though there are multiple treatment options, modern cryosurgery technology gives a complete cure.

- Furthermore, according to the IARC's World Cancer Report, despite constant progress in cancer prevention and treatment, the global cancer burden is still growing as the number of new cases is anticipated to increase by 50% between 2018 and 2040. IARC detected 10.1 million new cancer cases in 2000 and 18.1 million in 2018, and the number is projected to increase to 27 million new cancer cases per year by 2040.

- A significant number of healthcare professionals and hospitals still use various legacy hardware that need to be in line with current technological standards and are incapable of upgrading to new tech. In addition to this, there is a huge market for pre-owned medical technology worldwide, owing to the need for more availability and funding for such devices, which is hampering the growth and adoption of new technology.

- The Russia-Ukraine War is impacting the supply chain of semiconductors. Being a significant supplier of raw materials for producing semiconductors and electronic components, including various equipment. The dispute has disrupted the supply chain, causing shortages and price increases for these materials, impacting manufacturers and potentially leading to higher costs for end users.

- Further, according to UkraineInvest, copper prices escalated to USD 10,845/mt in early March 2022; however, it eased somewhat in 2023. The war between Russia and Ukraine, high energy costs, and stricter emissions standards in Europe have been noted as the primary reasons for the continued shortage of copper.

Semiconductor Applications in Healthcare Market Trends

Medical Imaging to be the Fastest-growing Application

- The medical imaging segment consists of computed tomography, magnetic resonance imaging, X-ray, and positron emission tomography that find applications in diagnosing various diseases, such as cancer and chronic diseases, via medical imaging.

- With the advancements in technology and the increasing adoption of technology in the healthcare sector, many advances were seen in medical radiation regarding equipment and techniques.

- Over the past few years, one of the significant advancements in interventional X-ray has been an increased focus on core and supporting technologies to provide high-quality, high-resolution images without a corresponding increase in radiation dose. This has been a critical driver behind technological advancements, such as Siemens' Artis Q, Philips' ClarityIQ and Q.zen technology, GE Healthcare's image-guided systems (IGS), and Toshiba's Infinix Elite product line. These have been driving the demand for advanced semiconductors.

- Owing to the increasing focus on radiological diagnostic tests and the rising burden of chronic diseases, the medical devices industry is witnessing growth in yearly imaging and diagnostic tests performed.

- According to the United Nations World Population Prospects, the number of people aged 65 years and over is steadily increasing. The number of older people (60 years and older) around the world is estimated to increase to 2 billion by 2050, of which 80% will live in low-income and middle-income countries. Therefore, the growing elderly population and increasing number of orthopedic and cardiovascular procedures are likely to further promote the adoption of medical imaging in healthcare applications.

- In the medical sector, dental applications require smaller and shorter scans. According to the Listerine Professional, oral conditions are the most faced health issues affecting 3.9 billion people globally. Therefore, in the dental sector, the primary demand for X-ray imaging is expected to increase and drive the demand for various semiconductors in the market studied.

- Furthermore, several companies are launching products associated with X-ray image analysis software to positively impact the segment's growth. For example, in January 2024, Carestream Health launched the DXR-Excel Plus, which is a two-in-one system for both fluoroscopy and general radiology that facilitates real-time images for a wide range of exams while providing features that help create an enhanced experience for users, patients, and administrators.

Asia-Pacific is Expected to be the Fastest-growing Market

- Asia-Pacific is expected to expand healthy during the forecast period. Key growth factors include increased investment in research and innovation centers, government programs, and policies to promote the IT and healthcare equipment and devices market. Additionally, the region is also the world's largest semiconductor market. This is due to countries like China, Japan, India, Taiwan, South Korea, and Singapore. These countries contribute to the growth of the healthcare segment.

- In Japan, companies invest in healthcare to build advanced businesses and achieve sustainable growth. For instance, FUJIFILM Holdings Corporation launched a new medium-term management plan, VISION2023, covering three years from the fiscal year ending March 2022 (FY2021) to FY2023. Over three years, VISION2023 foresees investments totaling USD 8.491 trillion to accelerate business growth, focusing on healthcare and highly functional materials businesses. The healthcare business will be expanded to the most considerable revenue and operating income segment to build a robust business foundation that enables sustainable growth.

- Moreover, China's State Council's 2014 National Integrated Circuit Industry Development Guidelines set the goal of becoming a world leader in all areas of the semiconductor industry by 2030. Furthermore, the Made in China 2025 initiative emphasizes semiconductor manufacturing as crucial to China's future economy and society. In addition, the country spent USD 574 billion on the healthcare sector.

- Additionally, South Korea is one of the major consumers, investors, and innovators in the market studied. South Korea's strong presence in the semiconductor industry and medical device manufacturing is helping the country strengthen its presence in the global semiconductor healthcare market. The government also plays a significant role in developing the domestic market, mainly to drive its economy.

- Moreover, the country utilizes AI in its pharmaceutical industry, further expanding the market. According to the government, South Korea's AI-driven drug development market is expected to grow by 40% annually and reach USD 3.9 billion in 2024.

Semiconductor Applications in Healthcare Market Overview

The semiconductor in the healthcare market is expected to grow moderately during the forecast period. The major players in the market, like Texas Instruments Incorporated, On Semiconductor Corporation, Analog Devices Inc., Maxim Integrated Products Inc., and STMicroelectronics, are adopting strategies such as partnerships and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

- November 2023: Miller announced its strategic plan to acquire Sentron, which is a fully integrated pressure and pH sensor manufacturing company for advancing medical understanding and enabling scientific discoveries through pressure sensor technology.

- November 2023: DuPont Liveo Healthcare announced its collaboration with STMicroelectronics to develop a new smart wearable device concept for remote biosignal monitoring, which employs multifunctional microsensors and control electronics from ST embedded in a flexible patch design from DuPont.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of the Impact of Key Macro Trends on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growth of Connected Devices in Medicines

- 5.1.2 Need for Advanced Semiconductor Technology for Better Medical Care

- 5.2 Market Restraints

- 5.2.1 Revamp of the Existing Hardware and High Equipment Cost of the End-use Product

6 MARKET SEGMENTATION

- 6.1 By Application

- 6.1.1 Medical Imaging

- 6.1.2 Consumer Medical Electronics

- 6.1.3 Diagnostic Patient Monitoring and Therapy

- 6.1.4 Medical Instruments

- 6.2 By Component

- 6.2.1 Integrated Circuits

- 6.2.1.1 Analog

- 6.2.1.2 Logic

- 6.2.1.3 Memory

- 6.2.1.4 Micro Components

- 6.2.2 Optoelectronics

- 6.2.3 Sensors

- 6.2.4 Discrete Components

- 6.2.1 Integrated Circuits

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia

- 6.3.4 Australia and New Zealand

- 6.3.5 Latin America

- 6.3.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Texas Instruments Incorporated

- 7.1.2 ON Semiconductor Corporation

- 7.1.3 Analog Devices Inc.

- 7.1.4 Maxim Integrated Products Inc.

- 7.1.5 STMicroelectronics

- 7.1.6 NXP Semiconductors NV

- 7.1.7 Broadcom Inc.

- 7.1.8 ams Osram

- 7.1.9 Vishay Intertechnology Inc.

- 7.1.10 Renesas Electronics Corporation