|

市场调查报告书

商品编码

1687731

相机模组-市场占有率分析、产业趋势与统计、成长预测(2025-2030)Camera Module - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

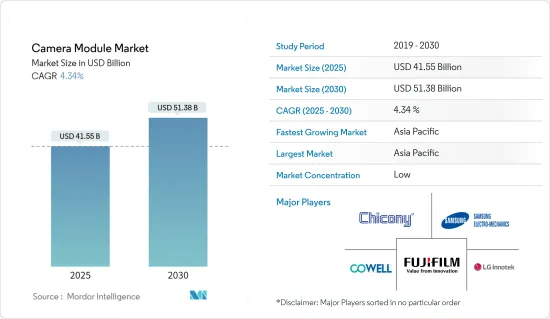

预计 2025 年相机模组市场规模为 415.5 亿美元,到 2030 年将达到 513.8 亿美元,预测期内(2025-2030 年)的复合年增长率为 4.34%。就出货量而言,预计将从 2025 年的 80.8 亿台成长到 2030 年的 109.2 亿台,预测期间(2025-2030 年)的复合年增长率为 6.20%。

相机模组市场:全面分析

关键亮点

- ADAS(高级驾驶辅助系统)激增:相机模组市场正在经历显着增长,这主要是由于汽车对 ADAS(高级驾驶辅助系统)的需求不断增加。前置摄影机系统在 ADAS 中发挥关键作用,为车道维持辅助、自动紧急煞车和主动车距控制巡航系统等安全功能提供先进的感测能力。对 ADAS 的日益依赖正在推动工业公司大力投资研发 (R&D) 和合作伙伴关係。例如,赛灵思公司和 Motovis 合作将赛灵思汽车 Zynq系统晶片平台与 Motovis 的卷积类神经网路IP 集成,以实现透过前置摄影机系统进行车辆感知和控制。

- 舜宇光学科技与 Valens Semiconductor 合作,将 MIPI A-PHY 相容晶片组整合到下一代 ADAS相机模组中。

- 麦格纳国际推出了环景显示摄影和电控系统,让3D环景显示技术更容易被消费者所接受。

- Foresight Autonomous Holdings 与日本一级供应商签署了联合概念验证协议,以提高 ADAS 效能。

- 保全摄影机的普及率不断提高:住宅和商业场所中保全摄影机的使用日益增多也是推动相机模组市场发展的主要因素。这种需求是在犯罪和恐怖主义威胁不断增加以及基于物联网的安全系统的采用的背景下产生的。例如,美国安装的监视器数量从 2018 年的 7,000 万个跃升至 2021 年的 8,500 万个,增幅达 21%。同样,预计到 2024 年,英国的安全系统服务收入将从 2019 年的 13.519 亿美元增至 15.9884 亿美元。

- 在韩国,公共CCTV安装数量增加了200%,到2021年达到1,458,465台。

- 作为智慧城市计画的一部分,古尔冈城市发展局计划在 200 个地点安装 1,000 个监视器。

- 为因应不断上升的暴力犯罪率,蒙特娄警方安装了九个额外的监视器。

- 技术进步推动创新相机模组市场正在经历快速的技术进步,尤其是在行动摄影领域。随着欧菲光等厂商推出超薄潜望镜镜头模组,潜望镜模组已成为旗舰智慧型手机的标准配备。此外,晶圆级玻璃 (WLG) + 塑胶镜头也越来越受欢迎,例如小米的 Redmi K40 游戏版就采用了混合 WLG相机镜头。

- Oppo 推出了一款连续光学变焦镜头,其影像品质比传统远摄感测器更好。

- 苹果公司已获得潜望镜相机系统的专利,该系统使用棱镜、镜头阵列和影像感测器。

- Vision Components 推出了一种用于医疗技术应用的新型 MIPI相机模组,具有高解析度和快速影格速率。

- 市场机会与未来成长:由于智慧型手机、汽车和医疗设备等应用的进步,微型相机模组市场可望大幅成长。据爱立信称,全球智慧型手机市场正在扩大,预计全球智慧型手机用户数量将从 2021 年的 6.259 兆增长到 2027 年的 7.69 兆。汽车领域也正在见证后置相机和 ADAS 前置相机的普及率不断提高,创造了巨大的机会。

- 对 360 度视角、车舱监控和电子后视镜应用的需求正在推动每辆车的平均摄影机数量增加。

- OmniVision 和 Valens Semiconductor 合作开发了适用于汽车应用的符合 MIPI A-PHY 标准的摄影机解决方案。

- 医疗产业也从中受益,OmniVision 推出了用于内视镜检查的最小的医疗级 CMOS 影像感测器。

相机模组市场趋势

影像感测器部分占据主导地位

- 细分市场概述:影像感测器细分市场占据相机模组市场的大部分,占2021年市场总收入的50.16%。作为最大的组件细分市场,影像感测器在各行业的相机模组中发挥着至关重要的作用。

- 市场规模与成长:到 2027 年,影像感测器部分预计将达到 300.8 亿美元,2022 年至 2027 年的年复合成长率(CAGR)为 6.71%。这一增长反映了影像感测器在相机模组生态系统中持续的重要性。

- 技术进步:对更高解析度和更佳低照度性能的需求正在推动影像感测器的技术进步。佳能开发的单光子Avalanche二极体 (SPAD) 感测器就是一个例子,能够在低照度条件下实现高品质的捕捉。

- 竞争格局:索尼集团等主要企业之间的激烈竞争推动着科技不断创新。索尼透过策略伙伴关係以及为智慧型手机、汽车和新兴技术开发先进感测器,继续保持市场领先地位。

- 工业应用:影像感测器的采用范围正在超越传统的相机应用,特别是在汽车领域,ADAS 和自动驾驶汽车需要高品质的感测器。 OmniVision 和 Valens Semiconductor 合作开发汽车级摄影机解决方案,彰显汽车领域日益增长的重要性。

亚太地区是相机模组市场成长的中心

- 区域优势:亚太地区是相机模组市场规模最大、成长最快的地区,预计到 2027 年将达到 389.4 亿美元,复合年增长率为 10.77%。

市场驱动因素

- 製造地:该地区的电子和半导体製造能力(主要在中国、韩国和台湾)正在推动相机模组的生产。

- 智慧型手机的普及:印度和中国等人口大国智慧型手机的快速普及推动了对相机模组的需求,据报道,到 2021 年,中国的行动网路用户将超过 10 亿。

- 汽车领域的成长:日本、韩国和中国等汽车市场的成长正在加速对ADAS和相机模组的需求。

- 政府倡议:「印度製造」计画等支持措施正在吸引对相机模组製造的投资。

- 工业发展:主要企业正在该地区大力投资。为了满足印度的製造目标,三星已将其工厂从中国迁至印度,而 OPPO 则建立了一座每三秒钟就能生产一部智慧型手机的工厂。

- 技术创新:欧菲光集团等亚太公司处于技术创新的前沿,并正在建立研究机构以在全球市场上保持竞争力。

相机模组市场概览

相机模组市场高度整合,LG Innotek、舜宇光学、欧菲光等全球领先公司在 2021 年占据了 75% 的市场占有率。 Luxvisions、Chicony 和 Mcnex 等较小的参与企业总合占据剩余市场占有率的 34.6%。

创新与垂直整合:市场领导非常重视研发和垂直整合。例如,LG Innotek每年将销售额的5%以上投入研发,并计画投资10.7亿美元提升产能。舜宇光学透过收购富士天津并建立自己的精密光学公司,加强了垂直整合。

未来成功策略:为了保持竞争力,公司必须投资于技术进步、策略伙伴关係和市场多样化。舜宇光学科技已与Valens Semiconductor合作开发支援ADAS的相机模组。此外,随着公司专注于汽车和物联网等新兴领域,他们需要优化製造流程以满足对小型化、高性能相机模组日益增长的需求。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概览

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买家的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争强度

- 产业价值链分析

- COVID-19 工业影响评估

- 价格趋势分析

- 超轻巧相机模组的动态

- 不同应用的相机模组尺寸的演变

- 各厂商提供的解析度和产品映射

- 分辨率与成本分析

第五章市场动态

- 市场驱动因素

- 汽车ADAS(高级驾驶辅助系统)市场驱动力不断增加

- 家庭和商业场所保全摄影机的使用增加

- 市场限制

- 复杂的製造和供应链挑战

- 科技发展趋势

- 透过组件实现技术进步

- 每款最终产品的平均相机数量-智慧型手机与微型汽车

汽车和行动电话相机的演变

第六章市场区隔

- 按组件

- 影像感测器

- 镜片

- 相机模组组装

- VCM供应商(AF和OIS)

- 按应用

- 移动的

- 家用电子电器(不包括手机)

- 车

- 医疗保健

- 安全功能

- 工业的

- 按地区

- 北美洲

- 欧洲

- 亚洲

- 澳洲和纽西兰

- 拉丁美洲

- 中东和非洲

7.供应商市场占有率分析

- 相机模组供应商市场占有率

- 影像感测器(CIS)供应商排名

- 镜头组供应商排名

第八章竞争格局

- 公司简介

- Chicony Electronics Co. Ltd

- Cowell E Holdings Inc.

- Fujifilm Corporation

- LG Innotek Co. Ltd

- Samsung Electro-Mechanics Co. Ltd

- Primax Electronics Ltd

- LuxVisions Innovation Limited(Lite-On Technology Corporation)

- Sharp Corporation

- Sony Group Corporation

- STMicroelectronics NV

- Sunny Optical Technology(Group)Company Limited

- AMS OSRM AG

- On Semiconductor(Semiconductor Components Industries LLC)

- OFILM Group Co. Ltd

- OmniVision Technologies Inc.

第九章投资分析

第十章市场机会与未来成长

The Camera Module Market size is estimated at USD 41.55 billion in 2025, and is expected to reach USD 51.38 billion by 2030, at a CAGR of 4.34% during the forecast period (2025-2030). In terms of shipment volume, the market is expected to grow from 8.08 billion units in 2025 to 10.92 billion units by 2030, at a CAGR of 6.20% during the forecast period (2025-2030).

Camera Module Market: A Comprehensive Analysis

Key Highlights

- Surge in Advanced Driver Assistance Systems: The camera module market is experiencing significant growth, primarily due to the rising demand for Advanced Driver Assistance Systems (ADAS) in vehicles. Forward camera systems play a crucial role in ADAS by providing advanced sensing capabilities for safety features like lane-keeping assistance, automatic emergency braking, and adaptive cruise control. The increasing reliance on ADAS is prompting industry players to invest heavily in research and development (R&D) and collaborations. For example, Xilinx Inc. and Motovis collaborated to integrate the Xilinx Automotive Zynq system-on-chip platform with Motovis' convolutional neural network IP for vehicle perception and control through forward camera systems.

- Sunny Optical Technology and Valens Semiconductor partnered to incorporate MIPI A-PHY-compliant chipsets into next-generation camera modules for ADAS applications.

- Magna International launched surround-view cameras and electronic control units, making 3D surround-view technology more accessible to consumers.

- Foresight Autonomous Holdings signed a joint proof of concept with a Japanese Tier One supplier to enhance ADAS performance.

- Rising Security Camera Adoption: The growing use of security cameras in both residential and commercial settings is another major factor driving the camera module market. This demand is fueled by the increasing threat of crime and terrorism, coupled with the adoption of IoT-based security systems. For example, the number of installed surveillance cameras in the U.S. surged by 21%, from 70 million in 2018 to 85 million in 2021. Similarly, security system services in the U.K. are projected to generate USD 1,598.84 million in revenue by 2024, up from USD 1,351.9 million in 2019.

- South Korea saw a 200% increase in public CCTV installations, reaching 1,458,465 cameras in 2021.

- Gurugram Metropolitan Development Authority plans to install 1,000 surveillance cameras across 200 locations as part of its smart city initiative.

- Montreal police installed nine additional security cameras in response to rising violent crime rates.

- Technological Advancements Driving Innovation: The camera module market is experiencing rapid technological advancements, especially in mobile photography. Periscope modules have become standard features in flagship smartphones, with manufacturers like O-Film unveiling ultra-thin periscope lens modules. Additionally, Wafer Level Glass (WLG) + Plastic lenses are gaining traction, as seen in Xiaomi's Redmi K40 Gaming Edition, which incorporates a hybrid WLG camera lens.

- Oppo launched a continuous optical zoom lens offering superior image quality over conventional telephoto sensors.

- Apple was granted a patent for a periscope camera system using prisms, a lens array, and an image sensor.

- Vision Components introduced new MIPI camera modules for medical technology applications, featuring high image resolutions and fast frame rates.

- Market Opportunities and Future Growth: The compact camera module market is on the verge of substantial growth, driven by advancements across applications like smartphones, automotive, and healthcare. The global smartphone market is expanding, with worldwide smartphone subscriptions expected to grow from 6,259 billion in 2021 to 7,690 billion by 2027, according to Ericsson. The automotive sector also presents significant opportunities, particularly with the rising adoption of rear cameras and ADAS forward cameras.

- The average number of cameras per car is increasing, driven by the demand for 360-degree views, cabin monitoring, and e-mirror applications.

- OmniVision and Valens Semiconductor collaborated to develop a MIPI A-PHY-compliant camera solution for automotive applications.

- The healthcare industry is also benefiting, with OmniVision launching its smallest medical CMOS image sensor for endoscopy procedures.

Camera Module Market Trends

Image Sensor Segment Dominating the Component Landscape

- Segment Overview: The image sensor segment commands a significant portion of the camera module market, contributing to 50.16% of the total market revenue in 2021. As the largest component segment, image sensors play a vital role in camera modules across various industries.

- Market Size and Growth: By 2027, the image sensor segment is projected to reach USD 30.08 billion, with a compound annual growth rate (CAGR) of 6.71% from 2022 to 2027. This growth reflects the continued importance of image sensors in the camera module ecosystem.

- Technological Advancements: The demand for higher resolution and better low-light performance is driving technological evolution in image sensors. Canon's development of a single-photon avalanche diode (SPAD) sensor exemplifies this, allowing high-quality image capture in low-light conditions.

- Competitive Landscape: Intense competition among key players like Sony Group Corporation drives continuous innovation. Sony remains a market leader through strategic partnerships and the development of advanced sensors for smartphones, automotive, and emerging technologies.

- Industry Applications: The adoption of image sensors is expanding beyond traditional camera uses, particularly in the automotive sector, where ADAS and autonomous vehicles require high-quality sensors. OmniVision and Valens Semiconductor collaborated to develop automotive-grade camera solutions, illustrating the automotive sector's growing significance.

Asia-Pacific The Epicenter of Camera Module Market Growth

- Regional Dominance: The Asia-Pacific region is the fastest-growing and largest segment of the camera module market, expected to reach USD 38.94 billion by 2027 with a CAGR of 10.77%.

Market Drivers:

- Manufacturing Hub: The region's electronics and semiconductor manufacturing capabilities, particularly in China, South Korea, and Taiwan, drive camera module production.

- Smartphone Penetration: Rapid smartphone adoption in populous countries like India and China is fueling demand for camera modules, with China reporting over 1 billion mobile internet users in 2021.

- Automotive Sector Growth: The growing automotive markets in countries like Japan, South Korea, and China are accelerating demand for ADAS and camera modules.

- Government Initiatives: Supportive policies like India's "Make in India" initiative are attracting investments in camera module manufacturing.

- Industry Developments: Key players are investing heavily in the region. Samsung shifted its factory from China to India, aligning with the country's manufacturing goals, while OPPO established a plant capable of producing one smartphone every three seconds.

- Technological Innovation: Asia-Pacific companies like OFILM Group Co. Ltd are at the forefront of innovation, establishing research institutes to maintain a competitive edge in the global market.

Camera Module Market Overview

The camera module market is highly consolidated, with leading global players such as LG Innotek, Sunny Optical, and O-Film commanding a 75% market share in 2021. Smaller players like Luxvisions, Chicony, and Mcnex collectively account for 34.6% of the remaining market share.

Innovation and Vertical Integration: Market leaders emphasize R&D and vertical integration. For instance, LG Innotek invests over 5% of its annual revenue in R&D and plans to increase production capacity with a USD 1.07 billion investment. Sunny Optical has bolstered its vertical integration by acquiring Fuji Tianjin and establishing its own precision optics company.

Strategies for Future Success: Companies must invest in technological advancements, strategic partnerships, and market diversification to remain competitive. Sunny Optical's partnership with Valens Semiconductor to develop ADAS-compliant camera modules exemplifies this. Moreover, companies should focus on emerging sectors like automotive and IoT, while optimizing manufacturing processes to meet growing demand for miniaturized, high-performance camera modules.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of Impact of COVID-19 on the Industry

- 4.5 Price Trend Analysis

- 4.6 Ultra Small Camera Module Dynamics

- 4.6.1 Evolution of Camera Module Size Across Various Applications

- 4.6.2 Product Mapping with Resolutions Offered by Various Vendors

- 4.6.3 Resolution Vs. Cost Analysis

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increased Market Demand for Advanced Driver Assistance Systems in Vehicles

- 5.1.2 Increased Use of Security Cameras in Households and Commercial Establishments

- 5.2 Market Restraints

- 5.2.1 Complicated Manufacturing and Supply Chain Challenges

- 5.3 Technology Evolution Trends

- 5.3.1 Component-wise Technological Advancements

- 5.3.2 Average Number of Cameras Per End-product - Smartphones Vs. Light

Vehicles / Camera Evolution in a Mobile Phone

6 MARKET SEGMENTATION

- 6.1 By Component

- 6.1.1 Image Sensor

- 6.1.2 Lens

- 6.1.3 Camera Module Assembly

- 6.1.4 VCM Suppliers (AF & OIS)

- 6.2 By Application

- 6.2.1 Mobile

- 6.2.2 Consumer Electronics (Excl. Mobile)

- 6.2.3 Automotive

- 6.2.4 Healthcare

- 6.2.5 Security

- 6.2.6 Industrial

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia

- 6.3.4 Australia and New Zealand

- 6.3.5 Latin America

- 6.3.6 Middle East and Africa

7 VENDOR MARKET SHARE ANALYSIS

- 7.1 Camera Module Vendor Market Share

- 7.2 Image Sensor (CIS) Vendor Ranking

- 7.3 Lens Set Vendor Ranking

8 COMPETITIVE LANDSCAPE

- 8.1 Company Profiles

- 8.1.1 Chicony Electronics Co. Ltd

- 8.1.2 Cowell E Holdings Inc.

- 8.1.3 Fujifilm Corporation

- 8.1.4 LG Innotek Co. Ltd

- 8.1.5 Samsung Electro-Mechanics Co. Ltd

- 8.1.6 Primax Electronics Ltd

- 8.1.7 LuxVisions Innovation Limited (Lite-On Technology Corporation)

- 8.1.8 Sharp Corporation

- 8.1.9 Sony Group Corporation

- 8.1.10 STMicroelectronics NV

- 8.1.11 Sunny Optical Technology (Group) Company Limited

- 8.1.12 AMS OSRM AG

- 8.1.13 On Semiconductor (Semiconductor Components Industries LLC)

- 8.1.14 OFILM Group Co. Ltd

- 8.1.15 OmniVision Technologies Inc.

9 INVESTMENT ANALYSIS

10 MARKET OPPORTUNITIES AND FUTURE GROWTH

汽车分割画面相机模组市场:按应用程式、销售管道、车辆类型、影像技术、安装方式和价格分布范围划分-全球预测,2025-2032年相机模组市场按类型、组件、解析度、焦点类型、应用和最终用户划分—2025-2032 年全球预测

汽车分割画面相机模组市场:按应用程式、销售管道、车辆类型、影像技术、安装方式和价格分布范围划分-全球预测,2025-2032年相机模组市场按类型、组件、解析度、焦点类型、应用和最终用户划分—2025-2032 年全球预测 2025年全球相机模组市场报告

2025年全球相机模组市场报告 小型车载相机模组的全球市场

小型车载相机模组的全球市场 2025 年至 2033 年相机模组市场报告(按组件、焦点类型、介面、像素、製程、应用和地区)

2025 年至 2033 年相机模组市场报告(按组件、焦点类型、介面、像素、製程、应用和地区) 相机模组市场按产品类型、应用和地区划分全球汽车分割视角相机模组市场相机模组市场规模、份额、趋势分析报告:按组件、焦点、像素、最终用途、细分市场预测,2025-2030 年

相机模组市场按产品类型、应用和地区划分全球汽车分割视角相机模组市场相机模组市场规模、份额、趋势分析报告:按组件、焦点、像素、最终用途、细分市场预测,2025-2030 年 相机模组市场 - 全球产业规模、份额、趋势、机会和预测,按产品类型、按地区和竞争划分,2019-2029 年

相机模组市场 - 全球产业规模、份额、趋势、机会和预测,按产品类型、按地区和竞争划分,2019-2029 年 全球相机模组市场规模研究,按製程(板载相机模组、倒装晶片相机模组)、组件、介面、像素、应用和区域预测 2022-2032 年。

全球相机模组市场规模研究,按製程(板载相机模组、倒装晶片相机模组)、组件、介面、像素、应用和区域预测 2022-2032 年。