|

市场调查报告书

商品编码

1687833

印刷基板(PCB) 产业:市场占有率分析、产业趋势与统计、成长预测(2024-2029 年)Printed Circuit Board (PCB) Industry - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

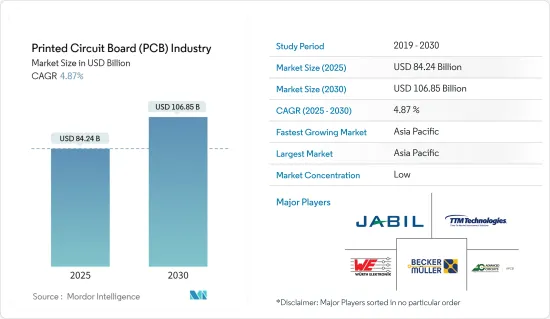

印刷基板(PCB) 市场规模预计在 2024 年将达到 803.3 亿美元,预计到 2029 年将达到 965.7 亿美元,在预测期内(2024-2029 年)的复合年增长率为 4.87%。

主要亮点

- 由于廉价智慧型手机产量的增加,预计行动电话PCB产量将会增加。据日本电产株式会社称,儘管智慧型手机销量正在下滑,但全球每年的出货量仍有13亿部。这些趋势为 PCB 带来了巨大的机会,因为它们是连接和支援各种电子元件(如微处理器、记忆体晶片、感测器和其他积体电路)的关键行动电话元件。

- 虽然消费性 PCB 并不是新鲜事物,但 PCB 在电子产品中的应用及其製造所使用的材料已经发展了一段时间。鑑于小型化的趋势,这是尤其不可避免的。此外,现代电子设备和电脑应用需要具有高导热性的 PCB 来散发产生的热量。由于使用的电器产品种类繁多,因此对各种 PCB 的需求也很大。例如,智慧型手錶所需的 PCB 与电脑不同。

- PCB 体积小、重量轻,非常适合可携式电子设备。 PCB 组装产业的成长和效率源自于消费性电子设备高度依赖精心设计和组装的印刷电路基板。高效能基板的有效整合可以优化各种家用电子电器,使其无缝执行您的日常业务。由于 PCB 设计紧凑且能够容纳复杂电路,因此对于智慧型手机、电视、笔记型电脑和游戏机等各种消费性电子产品至关重要。

- 推动 PCB 市场成长的一个主要趋势是 5G 等先进技术的日益普及,这在很大程度上得到了各政府机构和私人组织不断增加的投资的支持。

- 例如,2024年3月,爱立信宣布将建立一个新的专门的营业单位,以推动美国联邦政府由5G主导的数位转型。这项声明是在 5G通讯日益重要的情况下发布的,因为它对美国国家和经济通讯至关重要,也是美国国防现代化计画的关键组成部分。

- 人们对印刷电路基板(PCB)等电子废弃物的担忧日益增加,这是一个必须解决的重大环境问题。 PCB 含有多种有害物质,包括铅、汞、镉和溴化阻燃剂。如果处理不当,这些物质会渗入土壤和水中,对人类健康和环境构成威胁。

- 不当处置 PCB,例如掩埋或焚烧,可能会造成严重的环境后果。当 PCB 被丢弃在垃圾掩埋场时,有害物质会渗入土壤并污染地下水。当 PCB 被焚烧时,有毒气体和微粒会被释放到大气中,造成空气污染。

- 此外,台湾在半导体产业的重要性日益提升,以及半导体製造设备多样化的重要性日益提高等因素,可能会影响未来 PCB 的供需结构。

印刷基板(PCB)市场趋势

消费性电子领域将成为最大的终端使用者产业

- 随着消费性电子产业对 PCB 的需求不断增长,政府已采取倡议传播有关 PCB 製造的意识并为学生提供必要的培训。

- 例如,2024 年 2 月,麻萨诸塞大学洛威尔分校宣布成立麻省电子製造业进化研究所 (MEME),以协助培训 PCB 设计和製造的学生和产业工作者。该计划将获得马萨诸塞州技能资本津贴金 50 万美元,用于购买设备。麻萨诸塞州劳动力技能内阁提供由州政府透过资本预算资助的津贴计画。

- PCB原型製作设施是现代技术的重要组成部分,使美国、印度和中国等国家的企业家能够创造出可在全球销售的尖端产品。

- 2023 年 3 月,印度最大的原型设计中心 T-Works 与高通合作建立了最先进的多层印刷基板(PCB) 製造厂。新工厂预计将支援多种产品的开发,包括医疗设备、电动车、家用电器和工业自动化产品。

- 在家电产业,企业正在开发穿戴式物联网设备,以减少用户对智慧型手机的依赖。这些设备包括智慧型手錶和恆温器等简单、实惠的小工具,以及先进的智慧家庭自动化应用程式、智慧服饰、手錶、可听设备和眼镜。这些设备正在改变人们工作、沟通和完成日常业务的方式。消费级物联网设备的使用和普及度已显着增长,随着人们对更实惠、更快、更强大、更安全的物联网设备的需求,这一趋势预计还将持续。爱立信预计,2027年智慧家电等近距离物联网设备数量将达到251.5亿台,可望推动市场成长。

- 此外,物联网的普及和对连网型设备的需求不断增长预计将推动市场的发展。 IoT Analytics 的最新报告《2023 年春季物联网状况》宣布,2022 年全球物联网连线数量将成长 18%,达到 143 亿个活跃物联网端点。

- 到 2023 年,全球连网物联网设备数量将成长 16%,达到 167 亿活跃终端。儘管2023年的成长率将略低于2022年,但预计物联网设备连接仍将持续成长多年。此外,亚太地区中国、泰国和越南居民的连网型设备拥有率已经很高。

预计亚太地区将出现显着成长

- 随着中国电子产业的快速发展,多家中国PCB厂商已成为全球PCB市场的主导企业,并正在抢占亚太地区的市场占有率。这些製造商提供广泛的服务和能力,包括 PCB 设计、製造和组装,具有竞争力的价格和快速的交货时间。这些製造商包括 JLCPCB、Graperain、Fulltronics、YMS PCB Assembly 和 Hitech Circuits。

- 目前中国当地约有2500家PCB製造商。中国PCB产业主要分布在珠三角、Delta、环渤海Delta,这些地区元件市场集中,交通运输条件、水力发电条件良好。

- 推动中国PCB市场成长的关键因素是整体成本的下降和营运效率的提高。第一,虽然中国人口红利即将结束,但人事费用仍低于日本、韩国、台湾地区,甚至低于欧美。第二,中国的环保、工会、福利等领域的成本相对较低。

- 而且,作为全球最大的製造业大国,我国PCB产业拥有从铜箔、玻璃纤维、树脂、覆铜板到PCB的完整产业链。 PCB接近最终产品,许多电子产品也在中国完成。

- 受惠于全球PCB产能转移到中国以及下游电子终端产品的蓬勃发展,中国PCB产业呈现快速发展态势。电子资讯产业是我国重大发展的战略性、基础性、先导性支柱产业。 PCB产业作为电子资讯产业发展的基石,已成为国家鼓励发展的计划之一。

- 此外,根据可靠产业机构的经验资料显示,台湾在全球PCB产值中持续占据主导地位,占有较大的市场占有率。值得注意的是,韩国PCB製造商已经超越日本PCB製造商,在区域范围内占据第三的位置。

印刷基板(PCB) 产业概况

印刷基板(PCB)市场高度分散,既有全球性参与者,也有中小型企业。市场的主要参与者包括 Jabil Inc.、Wurth Elektronik Group(Wurth Group)、TTM Technologies Inc.、Becker &Muller Schaltungsdruck Gmbh 和 Advanced Circuits Inc. 市场参与者正在采用伙伴关係和收购等策略来加强其产品供应并获得永续的竞争优势。

2024 年 4 月 - TTM Technologies Sdn Bhd 是一家射频 (RF) 组件和先进印刷电路基板等技术解决方案的全球製造商,该公司在马来西亚槟城开设了第一家製造工厂,投资额为 2 亿美元。据该公司介绍,新工厂将建在槟城科学园区内,并将拥有高度先进和自动化的 PCB 製造能力。

2023 年 11 月 - Jabil Inc. 在墨西哥奇瓦瓦州开设第三家生产工厂,标誌着其持续发展和对该地区承诺的一个里程碑。该工厂面积超过25万平方英尺。此次扩张对于支援能源、汽车和交通、医疗保健、数位印刷和零售业的客户至关重要。新工厂将提高业务效率和灵活性,增强我们提供高品质产品的能力。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买家的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争强度

- 产业价值链分析

- COVID-19 的副作用和其他宏观经济因素将如何影响市场

第五章 市场动态

- 市场驱动因素

- 对技术小型化的需求日益增加

- 终端用户产业需求不断成长

- 市场限制

- 对电子废弃物的担忧日益加剧

第六章 市场细分

- 依产品类型

- 标准多层 PCB

- 刚性 1-2 面 PCB

- HDI/微孔/积层

- 柔性 PCB

- 软硬复合板

- 其他的

- 按最终用户产业

- 工业电子

- 卫生保健

- 航太和国防

- 车

- 消费性电子产品

- 其他最终用户产业

- 按地区

- 北美洲

- 欧洲

- 亚洲

- 澳洲和纽西兰

- 拉丁美洲

- 中东和非洲

第七章 竞争格局

- 公司简介

- Jabil Inc.

- Wurth elektronik group(Wurth group)

- TTM Technologies Inc.

- Becker & Muller Schaltungsdruck Gmbh

- Advanced Circuits Inc.

- Sumitomo Electric Industries Ltd(Sumitomo Corporation)

- Murrietta Circuits

- Unimicron Technology Corporation

- Tripod Technology Corporation

- AT&S Austria Technologie & Systemtechnik AG

- Nippon Mektron Ltd(nok Group)

- Zhen Ding Technology Holding Limited

第 8 章供应商市场占有率

第九章投资分析

第十章:未来市场展望

The PCB Market size is estimated at USD 80.33 billion in 2024, and is expected to reach USD 96.57 billion by 2029, growing at a CAGR of 4.87% during the forecast period (2024-2029).

Key Highlights

- Increased production of budget smartphones means that phone PCB production is expected to increase. According to Nidec, despite the downfall, 1.3 billion smartphones are shipped annually worldwide. These trends largely represent real opportunities for the PCB, as it is a vital mobile phone component that connects and supports various electronic components such as microprocessors, memory chips, sensors, and other integrated circuits.

- While consumer PCBs are certainly nothing new, the applications for PCBs for electronics and the materials used to make them have evolved over some time. This is inevitable, especially on account of the growing trend of miniaturization. Moreover, modern electronics and computer applications require PCBs with high thermal conductivity so that the heat generated can be dissipated. Different PCBs are needed for the many kinds of appliances in use. For example, the PCB needed to power a smartwatch is different from the PCB required for a computer.

- PCBs are highly suitable for portable consumer electronics due to their small size and lightweight characteristics. The growth and efficiency of the PCB assembly industry can be attributed to the significant reliance of consumer electronic products on well-designed and assembled printed circuit boards. By incorporating high-performance PCBs effectively, various consumer electronic devices can be optimized to carry out everyday tasks seamlessly. The indispensability of PCBs extends to a wide range of consumer electronics, such as smartphones, televisions, laptops, and gaming consoles, owing to their compact design and capability to accommodate intricate circuitry.

- One major trend driving the growth of the PCB market is the increasing adoption of advanced technologies such as 5G, which is significantly favored by growing investment from various government and private organizations.

- For instance, in March 2024, Ericsson announced the establishment of a dedicated entity for delivering a new dedicated entity to deliver 5G-driven digital transformation across the federal United States Government. This announcement was made taking the rising importance of 5G communication into consideration, as it is vital for US national and economic security and a key component of US defense modernization programs.

- The growing concerns regarding electronic waste, like printed circuit boards (PCBs), are a significant environmental issue that needs to be addressed. PCBs contain various hazardous materials, including lead, mercury, cadmium, and brominated flame retardants. When improperly disposed of, these substances can leach into the soil and water, posing a threat to human health and the environment.

- Improper disposal of PCBs, such as landfilling or incineration, can have serious environmental consequences. When PCBs end up in landfills, hazardous materials can seep into the soil and contaminate groundwater. Incineration of PCBs can release toxic gases and particles into the air, contributing to air pollution.

- Furthermore, factors such as the growing importance of Taiwan in the semiconductor industry and the increasing importance of diversifying semiconductor manufacturing facilities are likely to shape the supply and demand structure of PCBs in the future.

PCB Market Trends

Consumer Electronics Segment to be the Largest End-user Industry

- Owing to the growing demand for PCBs in the consumer electronics industry, the government is taking initiatives to spread awareness and provide essential training to students for PCB manufacturing.

- For instance, in February 2024, UMass Lowell announced the establishment of the Massachusetts Electronics Manufacturing Evolution (MEME) laboratory to help train students and industry workers in designing and fabricating PCBs. The project is supported with a USD 500,000 Massachusetts Skills Capital Grant for purchasing equipment for the facility. The Massachusetts Workforce Skills Cabinet offers the grant program, which is funded by the state through its capital budget.

- The PCB prototyping facility is a crucial component of modern technology, enabling entrepreneurs from countries such as the United States of America, India, and China to create cutting-edge products that can be launched globally.

- In March 2023, T-Works, India's largest prototype center, partnered with Qualcomm to establish a state-of-the-art multilayer Printed Circuit Board (PCB) fabrication facility. This new facility is anticipated to support the development of a wide range of products, including medical devices, electric vehicles, consumer electronics, industrial automation products, and more.

- Companies are developing wearable IoT devices in the consumer electronics industry to reduce users' reliance on smartphones. These devices can vary from primary and affordable gadgets like smartwatches and thermostats to advanced smart home automation applications, smart clothing, watches, hearables, and glasses. The way users work, communicate, and perform their daily tasks is being transformed by these devices. The usage and popularity of consumer IoT devices have grown significantly, and this trend is expected to continue as long as people demand IoT devices that are more affordable, faster, capable, powerful, and safer. According to Ericsson, short-range IoT devices like smart home appliances are expected to reach 25,150 million by 2027, which is expected to drive the market's growth.

- Furthermore, the rising IoT deployments and increasing demand for connected devices are expected to drive the market. The latest IoT Analytics "State of IoT-Spring 2023" report presents that the number of global IoT connections grew by 18% in 2022 to 14.3 billion active IoT endpoints.

- In 2023, the global number of connected IoT devices grew by 16% to 16.7 billion active endpoints. While 2023 growth was slightly lower than in 2022, IoT device connections are expected to continue to grow for many years. In addition, ownership of connected devices in the Asia-Pacific region is already high among those living in China, Thailand, and Vietnam.

Asia Pacific Region is Expected to Witness Significant Growth

- With the rapid development of China's electronics industry, many Chinese PCB manufacturers have emerged as leading players in the global PCB market, capturing a market share in the Asia-Pacific region. These manufacturers offer a wide range of services and capabilities, including PCB design, fabrication, and assembly, with competitive pricing and fast turnaround times. They include JLCPCB, Graperain, Fulltronics, YMS PCB Assembly, and Hitech Circuits.

- At present, there are about 2,500 PCB manufacturers in mainland China. The PCB industry in China is mainly distributed in the Pearl River Delta, the Yangtze River Delta, and the Bohai Rim, where they centralize the large component markets, good transportation conditions, and water and electricity conditions.

- Major reasons driving the growth of the PCB market in the Chinese region include lower overall cost and higher management efficiency. First, although China's demographic dividend is ending, labor costs are still lower than those of Japan, South Korea, and Taiwan and even lower than those of Europe and the United States. Second, China's environmental protection, trade unions, and welfare sectors are relatively low-cost.

- In addition, as the world's largest manufacturing country, China's PCB industry has a complete industrial chain from copper foil, glass fiber, resin, copper-clad laminates, and PCBs. PCB is close to the final products, and a great number of electronics are also finished in China.

- Benefiting from the transfer of global PCB production capacity to China and the vigorous development of downstream electronic terminal products, China's PCB industry shows a rapid development trend. The electronic information industry is a strategic, essential, and leading pillar industry for China's key development. The PCB industry, as the cornerstone of the development of the electronic information industry, has become one of the projects encouraged by China.

- Furthermore, empirical data from reputable industry associations underscores Taiwan's continued dominance in global PCB production values, with a major market share. Notably, South Korean PCB manufacturers have surpassed their Japanese counterparts, securing the third position on a regional scale.

PCB Industry Overview

The PCB market is highly fragmented due to the presence of both global players and small and medium-sized enterprises. Some of the major players in the market are Jabil Inc., Wurth Elektronik Group (Wurth group), TTM Technologies Inc., Becker & Muller Schaltungsdruck Gmbh, and Advanced Circuits Inc. Players in the market are adopting strategies such as partnerships and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

April 2024 - TTM Technologies Inc., a global manufacturer of technology solutions such as radio frequency ("RF") components and advanced printed circuit boards, opened its first manufacturing plant in Penang, Malaysia, with an investment of USD 200 million. According to the company, the new facility is built in Penang Science Park and has highly advanced and automated PCB manufacturing capabilities.

November 2023 - Jabil Inc. opened its third production facility in Chihuahua, Mexico, marking a milestone in its continued growth and commitment to the region. The plant spans more than 250,000 square feet. This expansion will be critical in supporting customers across the energy, automotive and transportation, healthcare, digital print, and retail industries. This new facility will enhance operational efficiency, flexibility, and the ability to deliver high-quality products.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Impact of COVID-19 Aftereffects and Other Macroeconomic Factors on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rising Demand for Miniaturization of Technology

- 5.1.2 Increasing Demand from End-user Industries

- 5.2 Market Restraints

- 5.2.1 Growing Concern Regarding Electronic Waste

6 MARKET SEGMENTATION

- 6.1 By Product Type

- 6.1.1 Standard Multilayer PCBs

- 6.1.2 Rigid 1-2 Sided PCBs

- 6.1.3 HDI/Micro-via/Build-up

- 6.1.4 Flexible PCBs

- 6.1.5 Rigid-flex PCBs

- 6.1.6 Others

- 6.2 By End-user Industry

- 6.2.1 Industrial Electronics

- 6.2.2 Healthcare

- 6.2.3 Aerospace and Defense

- 6.2.4 Automotive

- 6.2.5 Consumer Electronics

- 6.2.6 Other End-user Industries

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia

- 6.3.4 Australia and New Zealand

- 6.3.5 Latin America

- 6.3.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Jabil Inc.

- 7.1.2 Wurth elektronik group (Wurth group)

- 7.1.3 TTM Technologies Inc.

- 7.1.4 Becker & Muller Schaltungsdruck Gmbh

- 7.1.5 Advanced Circuits Inc.

- 7.1.6 Sumitomo Electric Industries Ltd (Sumitomo Corporation)

- 7.1.7 Murrietta Circuits

- 7.1.8 Unimicron Technology Corporation

- 7.1.9 Tripod Technology Corporation

- 7.1.10 AT&S Austria Technologie & Systemtechnik AG

- 7.1.11 Nippon Mektron Ltd (nok Group)

- 7.1.12 Zhen Ding Technology Holding Limited

8 VENDOR MARKET SHARE

9 INVESTMENT ANALYSIS

10 FUTURE OUTLOOK OF THE MARKET

印刷基板(PCB) 市场预测:至 2034 年-按类型、基板型、应用和地区分類的全球分析

印刷基板(PCB) 市场预测:至 2034 年-按类型、基板型、应用和地区分類的全球分析 5G印刷基板市场:按基板类型、基板材料、层数和应用划分-全球预测,2026-2032年光学模组印刷电路基板技术市场:依技术类型、材料类型、层数、频率范围及最终用途划分-2026年至2032年全球预测

5G印刷基板市场:按基板类型、基板材料、层数和应用划分-全球预测,2026-2032年光学模组印刷电路基板技术市场:依技术类型、材料类型、层数、频率范围及最终用途划分-2026年至2032年全球预测 高密度互连(HDI)印刷基板市场规模、份额、趋势和预测:按HDI层数、最终用途行业和地区划分,2026-2034年PCB切割机市场按操作模式、机器类型、电源、刀片类型和最终用途产业划分-全球预测,2026-2032年PCB隔离器市场按类型、技术、厚度、应用和最终用户划分,全球预测(2026-2032年)FR-4 刚性印刷电路基板市场:表面处理、基板、铜箔重量、层数和应用,全球预测,2026-2032 年铜基印刷基板市场(依产品类型、技术、应用、基板和铜箔重量划分)-全球预测,2026-2032年铜芯电路基板市场:依应用、结构、材料和製程划分,全球预测(2026-2032年)

高密度互连(HDI)印刷基板市场规模、份额、趋势和预测:按HDI层数、最终用途行业和地区划分,2026-2034年PCB切割机市场按操作模式、机器类型、电源、刀片类型和最终用途产业划分-全球预测,2026-2032年PCB隔离器市场按类型、技术、厚度、应用和最终用户划分,全球预测(2026-2032年)FR-4 刚性印刷电路基板市场:表面处理、基板、铜箔重量、层数和应用,全球预测,2026-2032 年铜基印刷基板市场(依产品类型、技术、应用、基板和铜箔重量划分)-全球预测,2026-2032年铜芯电路基板市场:依应用、结构、材料和製程划分,全球预测(2026-2032年) 印刷基板市场分析及预测(至2035年):依类型、产品、技术、组件、应用、材料类型、製程、最终用户、功能及安装类型划分

印刷基板市场分析及预测(至2035年):依类型、产品、技术、组件、应用、材料类型、製程、最终用户、功能及安装类型划分