|

市场调查报告书

商品编码

1939743

欧洲合约物流:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Europe Contract Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

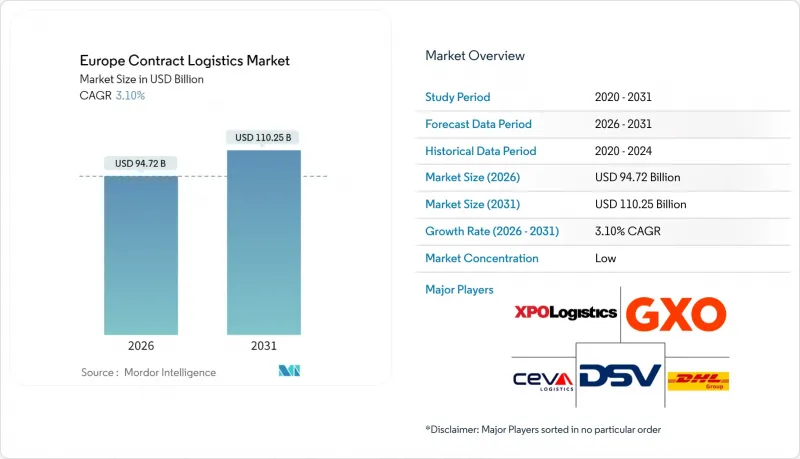

预计到 2026 年,欧洲合约物流市场规模将达到 947.2 亿美元,高于 2025 年的 918.7 亿美元,预计到 2031 年将达到 1,102.5 亿美元。

预计从 2026 年到 2031 年,其复合年增长率将达到 3.10%。

随着履约、供应链韧性增强和人工智慧驱动的最佳化等因素的出现,成熟的市场环境正稳步向加值解决方案转型,传统营运模式也随之改变。东欧近岸外包正在重塑贸易走廊,欧盟「Fit for 55」计画下的永续性目标正推动对低碳运输资产和绿色仓库的投资。 DSV对DB Schenker的重大收购所体现的加速整合表明,营运商正在寻求规模经济,以应对劳动力短缺、房地产价格上涨和监管日益复杂等问题。采用机器人技术、端到端视觉化平台和灵活仓库布局的营运商,最有可能抓住欧洲合约物流市场下一波外包需求的浪潮。

欧洲合约物流市场趋势与洞察

电子商务的快速成长推动了外包物流配送的履约

随着零售商转向轻资产模式,以灵活的仓储合约取代固定的房地产成本,第三方物流(3PL) 营运商正抓住日益增长的电商需求。对大型物流中心的需求不断增长,导致供应紧张,促使零售商签订长期租赁合同,并将日常营运外包给 3PL。为了在欧洲合约物流市场实现当日送达目标,供应商正在投资全通路分类、机器人拣选和与承运商无关的最后一公里配送网路。时尚和鞋类行业的高退货率增加了逆向物流的复杂性,整合退货处理已成为新契约的标配。先驱企业履约和退货处理整合到单一技术平台上的企业,正在获得更高的客户留存率和溢价。

加强后疫情时代供应链的韧性

疫情已将韧性从成本中心提升至董事会层面的优先事项,推动了欧洲各地供应商的双重采购、区域缓衝和多元化。将海运、陆运、铁路和空运资讯整合到单一仪錶板的多模态视觉化系统,已成为欧洲合约物流市场竞标的核心选择标准。客户优先考虑能够协调多个库存地点并在中断期间动态重新安排货物运输路线的第三方物流公司。在2024年至2025年间投资建设控制塔架构的供应商报告称,由于承运商寻求能够为其应急响应计划提供数据支持的合作伙伴,其中订单率有所提高。视觉化的重要性也延伸至环境、社会和治理(ESG)报告,即时碳排放追踪正日益成为服务水准协议中的重要内容。

司机和仓库工人短缺

欧洲正面临日益严重的驾驶人,国际道路运输联盟(IRU)警告称,到2026年,卡车司机缺口可能超过200万人。仓库工人离职率也加速上升,老员工退休速度远超新进员工入职速度。薪资上涨对欧洲合约物流市场的利润率带来压力,儘管营运商正透过提供入职奖金、灵活的工作安排和内部培训机构等方式来应对。自动化可以缓解部分压力,但前期投资和变革管理週期意味着较长的投资回报期。除非企业对其劳动力策略进行现代化改造,否则将面临服务中断和运能调整的风险,最终导致客户满意度下降。

细分市场分析

2025年,运输服务在欧洲合约物流市场占有率中占比达到60.35%,主要由公路、铁路、航空和海运驱动,为洲际贸易提供支援。然而,仓储和配送业预计将以3.92%的复合年增长率(CAGR)实现最快成长,直至2031年,因为托运人将库存布局置于单纯的运输速度之上。儘管运输业在欧洲合约物流市场仍保持强劲势头,但价值正向整合货运、仓储和轻型製造业务的打包服务转移。预计2024年铁路货运量将下降0.7%,凸显了这种运输方式的局限性,而欧盟的目标是将其市场份额增加一倍。虽然道路运输仍然是门到门运输的主流方式,但承运商网路正在引入数位化货运平台以实现动态路线规划。航空货运专注于高价值和时效性货物,而短途海运则将地中海和波罗的海门户与多式联运网路连接起来。

仓储和配送领域也出现了类似的趋势。对人口密集区附近大型枢纽的需求与土地稀缺和严格的规划法规相衝突,推高了黄金地段物业的租金。营运商正利用高层自动化、夹层机器人和暗库配置来控製成本,并将每平方公尺的容量提高三倍。低温运输,尤其是对药品和生鲜食品的运输,进一步提高了准入的技术门槛。因此,合约中现在规定了除托盘移动之外的其他绩效指标,例如拣货准确率、逆向物流週期和微型仓配处理速度。欧洲合约物流市场的结构旨在奖励那些能够将房地产专业知识与先进程式工程相结合的公司。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 电子商务的快速成长正在推动外包履约。

- 加强后疫情时代供应链韧性的措施

- 东欧製造业近岸外包

- 利用人工智慧进行仓库和路线优化

- 欧盟「Fit for 55」脱碳奖励

- 由于退货,对整合逆向物流的需求增加。

- 市场限制

- 司机和仓库工人短缺

- 分散的竞争性定价压力

- 符合ESG标准的仓库房地产成本飙升

- 复杂的多国海关和增值税合规

- 价值/供应链分析

- 监管环境

- 技术展望

- 波特五力模型

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 激烈的竞争

- 电子商务(国内和跨境)洞察

- 售后服务/逆向物流洞察

- 英国脱欧的影响

- 新冠疫情与地缘政治事件的影响

第五章 市场规模与成长预测

- 按服务类型

- 运输

- 道路运输

- 铁路

- 航空

- 海上运输

- 仓储/配送

- 附加价值服务(组装、贴标、套件包装)

- 运输

- 按合约期限

- 1-3年

- 3年或以上

- 按最终用户行业划分

- 製造业和汽车业

- 食品/饮料

- 零售与电子商务

- 医疗和药品

- 化学品

- 其他行业

- 按国家/地区

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 荷兰

- 波兰

- 比利时

- 瑞典

- 其他欧洲地区

第六章 竞争情势

- 市场集中度

- 策略性倡议(併购、合资、创新)

- 市占率分析

- 公司简介

- Deutsche Post DHL Group

- DSV

- GXO Logistics

- XPO Logistics

- CEVA Logistics

- Geodis

- Kuehne+Nagel

- Rhenus Logistics

- ID Logistics

- Hellmann Worldwide Logistics

- DACHSER

- United Parcel Service(UPS SCS)

- Neovia Logistics

- FIEGE Logistik Stiftung & Co. KG

- Savino Del Bene

- Rohlig Logistics

- BLG Logistics Group

- Groupe BBL

- Raben Group

- Noerpel Group

第七章 市场机会与未来展望

第八章附录

- 各行业对GDP的贡献

- 资金流分析

- 贸易统计

- 主要进出口路线

The Europe Contract Logistics Market size in 2026 is estimated at USD 94.72 billion, growing from 2025 value of USD 91.87 billion with 2031 projections showing USD 110.25 billion, growing at 3.10% CAGR over 2026-2031.

The mature landscape is steadily pivoting toward value-added solutions as e-commerce fulfillment, supply-chain resilience, and AI-enabled optimization transform traditional operating models. Nearshoring into Eastern Europe is redrawing trade corridors, while sustainability targets under the EU Fit for 55 package amplify investment in low-carbon transport assets and green warehousing. Intensifying consolidation-exemplified by DSV's recent mega-acquisition of DB Schenker-shows providers chasing economies of scale to blunt labor shortages, real-estate inflation, and regulatory complexity. Providers that embed robotics, end-to-end visibility platforms, and flexible warehousing footprints are best placed to capture the next wave of outsourced demand across the Europe contract logistics market.

Europe Contract Logistics Market Trends and Insights

E-commerce Boom Accelerates Outsourced Fulfillment

Third-party logistics (3PL) operators are capturing rising e-commerce volumes as retailers shift toward asset-light models that trade fixed real-estate costs for flexible warehousing contracts. Demand for XXL distribution centers has tightened availability, prompting retailers to secure long leases while outsourcing day-to-day operations to 3PLs. Providers are investing in omnichannel sortation, robotic picking, and carrier-agnostic last-mile networks to achieve same-day delivery targets across the Europe contract logistics market. High return rates in fashion and footwear elevate reverse-logistics complexity, making integrated returns processing a standard feature of new contracts. Early movers that bundle fulfillment and returns under one technology stack enhance customer stickiness and unlock premium pricing.

Post-COVID Supply-Chain Resilience Initiatives

The pandemic reframed resilience from a cost center to a board-level priority, driving dual-sourcing, regional buffers, and supplier diversification across Europe. Multimodal visibility systems that consolidate ocean, road, rail, and air events into a single dashboard are now core selection criteria when tendering for Europe contract logistics market contracts. Customers prioritize 3PLs capable of orchestrating parallel inventory locations and dynamically rerouting freight during disruption. Providers that invested in control-tower architectures in 2024-2025 report win-rate uplifts as shippers seek data-rich partners able to evidence contingency playbooks. The visibility imperative extends to ESG reporting, with real-time carbon tracking increasingly written into service-level agreements.

Driver & Warehouse-Labor Shortages

Europe faces a looming shortfall of professional truck drivers, with the International Road Transport Union warning that vacancies could top 2 million by 2026. Warehouse attrition has accelerated as aging workforces retire faster than recruits enter the sector. Operators respond through signing bonuses, flexible schedules, and in-house training academies, but wage inflation squeezes margins in the Europe contract logistics market. Automation offsets some pressure, yet up-front capex and change-management cycles lengthen payback periods. Service disruptions and capacity rationing risk eroding customer satisfaction unless workforce strategies are modernized.

Other drivers and restraints analyzed in the detailed report include:

- Eastern Europe Near-Shoring of Manufacturing

- AI-Driven Warehouse & Route Optimization

- Fragmented Competitive Pricing Pressure

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Transportation services captured 60.35% of the Europe contract logistics market share in 2025 as road, rail, air, and sea movements underpin continental trade. Yet Warehousing & Distribution is growing fastest at 3.92% CAGR to 2031 as shippers prioritize inventory positioning over pure transit speed. The Europe contract logistics market size allocated to Transportation remains healthy, but value is shifting toward integrated bundles that combine freight, storage, and light manufacturing tasks. Rail freight slipped 0.7% in 2024, underscoring modal constraints despite EU ambitions to double its share. Road continues to dominate door-to-door flows, although carrier networks now embed digital freight platforms for dynamic routing. Air freight retains a niche, serving high-value or time-critical goods, while short-sea lanes link Mediterranean and Baltic gateways into wider multimodal offerings.

A parallel narrative unfolds in Warehousing & Distribution. Demand for XXL hubs near population centers collides with scarce land and stricter zoning, inflating prime rents. Operators mitigate costs by adopting high-bay automation, mezzanine robotics, and dark-store configurations that triple throughput per square meter. Cold-chain extensions support pharmaceuticals and fresh food, deepening technical barriers to entry. Consequently, contracts now stipulate performance metrics beyond pallet moves, tracking pick accuracy, reverse-logistics cycles, and micro-fulfillment turnaround. The Europe contract logistics market thus rewards firms able to marry real-estate acumen with advanced process engineering.

The Europe Contract Logistics Market Report is Segmented by Service Type (Transportation, Warehousing & Distribution, and Value-Added Services), Contract Duration (1-3 Years and Above 3 Years), End-User Industry (Manufacturing & Automotive, Retail & E-Commerce, Healthcare & Pharmaceuticals, and More), Country (Germany, United Kingdom, France, Italy, Spain, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Deutsche Post DHL Group

- DSV

- GXO Logistics

- XPO Logistics

- CEVA Logistics

- Geodis

- Kuehne + Nagel

- Rhenus Logistics

- ID Logistics

- Hellmann Worldwide Logistics

- DACHSER

- United Parcel Service (UPS SCS)

- Neovia Logistics

- FIEGE Logistik Stiftung & Co. KG

- Savino Del Bene

- Rohlig Logistics

- BLG Logistics Group

- Groupe BBL

- Raben Group

- Noerpel Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 E-commerce boom accelerates outsourced fulfilment

- 4.2.2 Post-COVID supply-chain resilience initiatives

- 4.2.3 Eastern-Europe near-shoring of manufacturing

- 4.2.4 AI-driven warehouse & route optimisation

- 4.2.5 EU "Fit-for-55" decarbonisation incentives

- 4.2.6 Integrated reverse-logistics demand from returns

- 4.3 Market Restraints

- 4.3.1 Driver & warehouse-labour shortages

- 4.3.2 Fragmented competitive pricing pressure

- 4.3.3 Surging ESG-compliant warehouse real-estate costs

- 4.3.4 Complex multi-country customs / VAT compliance

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power - Buyers

- 4.7.3 Bargaining Power - Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Rivalry

- 4.8 E-commerce (Domestic & Cross-border) Insights

- 4.9 After-sales / Reverse-logistics Insights

- 4.10 Brexit Implications

- 4.11 Impact of COVID-19 & Geo-Political Events

5 Market Size & Growth Forecasts

- 5.1 By Service Type

- 5.1.1 Transportation

- 5.1.1.1 Road

- 5.1.1.2 Rail

- 5.1.1.3 Air

- 5.1.1.4 Sea

- 5.1.2 Warehousing & Distribution

- 5.1.3 Value-added Services (Assembly, Labelling, Kitting)

- 5.1.1 Transportation

- 5.2 By Contract Duration

- 5.2.1 1 - 3 Years

- 5.2.2 Above 3 years

- 5.3 By End-user Industry

- 5.3.1 Manufacturing & Automotive

- 5.3.2 Food & Beverage

- 5.3.3 Retail & E-commerce

- 5.3.4 Healthcare & Pharmaceuticals

- 5.3.5 Chemicals

- 5.3.6 Other Industries

- 5.4 By Country

- 5.4.1 Germany

- 5.4.2 United Kingdom

- 5.4.3 France

- 5.4.4 Italy

- 5.4.5 Spain

- 5.4.6 Netherlands

- 5.4.7 Poland

- 5.4.8 Belgium

- 5.4.9 Sweden

- 5.4.10 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, JV, Innovation)

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.4.1 Deutsche Post DHL Group

- 6.4.2 DSV

- 6.4.3 GXO Logistics

- 6.4.4 XPO Logistics

- 6.4.5 CEVA Logistics

- 6.4.6 Geodis

- 6.4.7 Kuehne + Nagel

- 6.4.8 Rhenus Logistics

- 6.4.9 ID Logistics

- 6.4.10 Hellmann Worldwide Logistics

- 6.4.11 DACHSER

- 6.4.12 United Parcel Service (UPS SCS)

- 6.4.13 Neovia Logistics

- 6.4.14 FIEGE Logistik Stiftung & Co. KG

- 6.4.15 Savino Del Bene

- 6.4.16 Rohlig Logistics

- 6.4.17 BLG Logistics Group

- 6.4.18 Groupe BBL

- 6.4.19 Raben Group

- 6.4.20 Noerpel Group

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

8 Appendix

- 8.1 GDP Contribution by Industry

- 8.2 Capital-flow Insights

- 8.3 External-trade Statistics

- 8.4 Key Import / Export Corridors

亚太地区合约物流:市场占有率分析、产业趋势与统计、成长预测(2026-2031)北美合约物流:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

亚太地区合约物流:市场占有率分析、产业趋势与统计、成长预测(2026-2031)北美合约物流:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 日本合约物流市场报告(按类型(内部物流、外部物流)、最终用户(汽车、消费品和零售、能源、高科技和医疗保健、工业和航太、技术及其他)和地区划分,2026-2034 年)

日本合约物流市场报告(按类型(内部物流、外部物流)、最终用户(汽车、消费品和零售、能源、高科技和医疗保健、工业和航太、技术及其他)和地区划分,2026-2034 年) 合约物流市场规模及预测 2021 - 2031、全球及地区份额、趋势及成长机会分析报告涵盖范围:按类型、服务类型、最终用户及地理划分

合约物流市场规模及预测 2021 - 2031、全球及地区份额、趋势及成长机会分析报告涵盖范围:按类型、服务类型、最终用户及地理划分 美国合约物流市场:依服务、类型、产业、运输方式、地区、机会及预测,2018-2032

美国合约物流市场:依服务、类型、产业、运输方式、地区、机会及预测,2018-2032 合约物流的全球市场(2025年)

合约物流的全球市场(2025年) 合约物流市场-全球产业规模、份额、趋势、机会和预测(按类型、按服务、按应用、按地区、按竞争划分,2020-2030 年预测)

合约物流市场-全球产业规模、份额、趋势、机会和预测(按类型、按服务、按应用、按地区、按竞争划分,2020-2030 年预测) 合约物流市场规模、份额、趋势分析报告:按服务、类型、运输方式、产业、地区和细分市场预测,2025 年至 2030 年英国合约物流:市场占有率分析、产业趋势与成长预测(2025-2030 年)印度合约物流市场评估:依服务、类型、行业、运输方式、地区、机会、预测(2018-2032年)

合约物流市场规模、份额、趋势分析报告:按服务、类型、运输方式、产业、地区和细分市场预测,2025 年至 2030 年英国合约物流:市场占有率分析、产业趋势与成长预测(2025-2030 年)印度合约物流市场评估:依服务、类型、行业、运输方式、地区、机会、预测(2018-2032年)