|

市场调查报告书

商品编码

1687928

低温运输包装:市场占有率分析、产业趋势与成长预测(2025-2030)Cold Chain Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

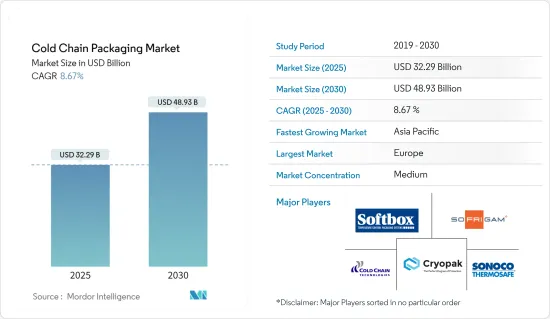

低温运输包装市场规模预计在 2025 年为 322.9 亿美元,预计到 2030 年将达到 489.3 亿美元,预测期内(2025-2030 年)的复合年增长率为 8.67%。

联合国粮食及农业组织估计,全球每年浪费13亿吨食物,每个国家、每个社会群体、每个供应链环节都有浪费。新冠疫情造成的粮食体係不稳定加剧了本已严重的损失。

关键亮点

- 各国政府对低温运输包装的采用,不仅反映了包装的重要性,也有助于扩大市场。例如,2022年6月有报告指出,低温运输、增值和保存基础设施计画(主要由印度政府资助)将由政府资助对低温运输(包括加工)的投资。

- 低温运输、加值和保鲜基础设施计划旨在为从农民到消费者提供无缝整合的低温运输和保鲜基础设施。该策略重点关注农场级低温运输基础设施建设,为计划规划提供了灵活性。此外,根据印度政府宣布的综合低温运输和增值基础设施计划,有兴趣的投资者可以根据政府预先设定的成本参数获得相当于计划成本35%至50%的津贴或补贴。

- 此外,鑑于电子商务的激增,隔热包装很可能在规模较小的电子商务和食品宅配业务(从餐套件到其他新鲜食品和饮料)中表现出色。装有生鲜产品和冷冻食品的多个包裹需要隔热包装,而疫情引发的行为变化意味着这些包裹将在外面放置一段时间。因此,预计疫情期间对低温运输包装解决方案的需求将大幅增加。

- 低温运输包装解决方案对于不断增长的全球生鲜产品贸易以及向世界提供食品和医疗用品至关重要。消费者对生鲜食品的需求不断增加、贸易自由化导致的国际贸易成长以及有组织的食品零售业的扩张是推动市场成长的一些因素。

- 日益严格的法规,例如《食品安全现代化法案》(食品储存的冷藏仓库要求)的有效实施,正在推动市场成长。此外,医疗设备和製药业等各种工业应用的需求不断增长也为全球低温运输包装市场做出了重大贡献。

- 然而,近期由于供需缺口扩大,聚苯乙烯价格波动,导致价格上涨,且这种趋势在预测期内可能会持续下去。此外,原料成本的上涨也推高了最终产品的总成本。

- 在新冠疫情爆发之前,低温运输解决方案的利用效率从来都不是首要任务。疫情期间,世界面临的最艰鉅的挑战之一是生产足够的疫苗,为每位公民接种,这是一项艰鉅的任务,以确保疫苗在不受损坏的情况下分发给公民。疫情带来的送货上门限制和其他限制措施迫使一些企业改变产业计画并引入宅配选项。此外,还需要高效率的低温运输物流解决方案。由于消费者意识的提高和维持基本品质标准的需要,需求进一步增加。

低温运输包装市场趋势

医药产业的成长将推动低温运输包装市场的扩张

- 根据 Almac Pharma Services 介绍,正在开发的生技药品管对温度的敏感性越来越高,导致原料药的冷冻储存(-40 至 -70°C)需求增加。该公司补充说,细胞和基因治疗产品的标籤、包装和分销通常需要在超低温(约 20 至 -80°C)下储存和处理产品,并且仅在使用前立即解冻产品。

- 大多数高价值医药产品透过低温运输运送至世界各地的分销网络。因此,药品的成长可望推动低温运输包装市场的发展。根据国际贸易中心的数据,当年英国对欧盟的药品出口额在英国成员国中最高,达近24.3亿英镑。大量的出口量显示可以选择低温运输包装,让包装要求适应温度、运输方式等动态条件。

- 此外,医疗产业对冷藏药品的需求持续成长直接影响低温运输包装市场。从区域来看,低温运输包装市场以欧洲和北美为主。这是因为欧洲和北美国家生物製药进出口量较大。这些地区在改善医药运输和仓储方面也取得了创新。

- 此外,政府关于低温运输包装材料使用的法规也对市场产生了影响。人们也强烈要求采用更永续的设计,包括再利用计划,以减少碳足迹。不断变化的法规和标准也推动了人们对温控包装的兴趣。例如,ISTA(国际安全运输协会)的温度曲线在过去五年内发生了变化。预计此类变化将对市场产生影响。

欧洲占最大市场占有率

- 欧洲占据低温运输包装市场的大部分份额。由于医疗保健产业对冷藏药品的需求持续增加,预计预测期内市场将大幅成长。

- 为了保持竞争优势,许多公司都集中投资和研发力量,创造创新的低温运输包装技术。例如,2022年5月,Essentra Packaging与AMD合作开发了新一代TTI(时间温度指示器),这是一项针对製药业的智慧包装技术。两家英国公司之间的合作旨在结合 AMD 和 Essentra Packaging 的优势,提供高度相关且可提高病患安全性的未来包装解决方案。

- 此外,欧洲公司正在透过实施低温运输解决方案在增强药品包装和储存方面取得进展。例如,2022年7月,Sharp Corporation位于荷兰海伦芬的工厂扩大了医疗服务范围。Sharp Corporation是合约包装和临床供应服务领域的杰出参与企业。为了适应开放和随机临床测试,增加了标籤和二次包装服务,增强了现有的临床储存和分发能力。初步包装和标籤已经完成。夏普目前可从该设施提供全方位的临床服务,包括-80°C 至 -80°C 的二次包装、2°C 至 8°C 的储存以及作为临床测试材料的 QP 放行的干冰储存。该网站的客户可以获得有关在欧洲发布和分发物品的监管问题的帮助。

- 此外,由于欧洲製药和生命科学公司数量的不断增加,许多欧洲公司也在扩大其国际影响力。例如,2022年2月,德国邮政敦豪集团旗下物流公司DHL供应链的生命科学与医疗保健(LSHC)部门宣布,今年将投资超过4亿美元,将其医药和医疗设备分销网络的覆盖范围扩大27%,即约300万亿平方英尺。新大楼将拥有完整的许可证、满足药品储存需求的温控空间以及能够处理包装和受控运输的整合解决方案。

低温运输包装产业概况

低温运输包装市场细分程度适中,少数公司占相当大的份额。主要参与企业包括 Cold chain Technologies、Sonoco Thermosafe、Sofrigram、Softbox Systems、Cryopak、Sealed Air Corporation、DGP Intelsius LLC. 和 Amcor Plc。

- 2022 年 3 月 - Cold Chain Technologies, LLC 宣布收购 Packaging Technology Group, LLC,后者是生命科学领域环保、可回收热感包装解决方案的知名供应商。该协议将使包装技术集团公司扩大对关键永续技术的投资,并为全球客户提供更广泛的创新解决方案。

- 2021 年 12 月 - 环保冷藏包製造商 Recycold Cool Solutions BV 已被 Ranpak Holdings Corp. 收购。与传统冷藏包不同,Recycold Cool Packs 由可安全排水的植物来源凝胶製成,并已添加到 Ranpak 不断增长的低温运输包装解决方案系列中。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概览

- 产业价值链分析

- 产业吸引力-波特五力分析

- 新进入者的威胁

- 买家的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

- 市场驱动因素

- 製药和医疗产业成长带来的市场復苏

- 消费者对生鲜食品的需求不断增加

- 市场限制

- 关于使用低碳材料的政府法规

- 原料成本上涨

- COVID-19 市场影响评估

第五章市场区隔

- 按产品

- 保温容器

- 冷媒

- 温度监控

- 按最终用户应用程式

- 食物

- 乳製品

- 製药

- 其他的

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 其他的

第六章 竞争格局

- 公司简介

- Pelican BioThermal LLC

- Sonoco Thermosafe

- Cold Chain Technologies Inc.

- Cryopak Industries Inc.

- Sofrigam Company

- Intelsius(A DGP Company)

- Coolpac

- Softbox Systems Ltd.

- Clip-Lok SimPak

- Chill-Pak.com.

第七章投资分析

第八章:市场的未来

The Cold Chain Packaging Market size is estimated at USD 32.29 billion in 2025, and is expected to reach USD 48.93 billion by 2030, at a CAGR of 8.67% during the forecast period (2025-2030).

The Food and Agriculture Organization estimates that 1.3 billion metric tonnes of food are wasted worldwide each year, accounting for contributions from every country, every societal group, and every step in the supply chain. The instability in the food system brought on by the COVID-19 epidemic made an already terrible loss even more painful.

Key Highlights

- The adoption of cold chain packaging by various governments not only demonstrates the importance of the packaging but also aids in market expansion. For instance, in June 2022, the "Scheme of Cold Chain, Value Addition and Preservation Infrastructure" plan, which is largely funded by the Indian government, reported that the government provides funding for investments in the cold chain, including processing.

- The Scheme of Cold Chain, Value Addition, and Preservation Infrastructure aims to provide seamless, integrated cold chain and preservation infrastructure facilities from the farm gate to the consumer. With a focus on developing farm-level cold chain infrastructure, the strategy offers project planning flexibility. Additionally, an interested investor may receive a grant or subsidy of 35% to 50% of the project cost based on previously established cost parameters by the government under the scheme for integrated cold chain and value addition infrastructure released by the Government of India.

- Further, considering the spike in e-commerce, insulated packaging is expected to see strong sales with smaller e-commerce and food delivery formats across meal kits and other perishable food and beverage items. As multiple packages containing fresh and frozen items require good insulation, the pandemic-led behavioral change has led to packages being left outdoors for some time. Hence, the pandemic is further expected to witness a significant increase in the demand for cold chain packaging solutions.

- Cold chain packaging solutions are essential to the growth of the global trade in perishable products and the worldwide availability of food and health supplies. The rise in consumer demand for perishable food items, growth of international trade due to trade liberalization, and expansion of the organized food retail industry are some of the factors driving the growth of the market.

- Increasing stringent regulations, such as the effective implementation of the Food Safety Modernization Act (cold storage warehouse requirement to preserve food), drive the market's growth. Additionally, the rising demand from various industrial applications, such as the medical devices and pharmaceutical industries, are significant contributors to the global cold chain packaging market.

- However, in recent times, instability in polystyrene prices, due to the increased gap between demand and supply, has led to a price surge, which is likely to continue during the forecast period. Moreover, the escalated cost of raw materials is boosting the overall cost of the final product.

- Efficiency in using cold chain solutions was never a top priority before COVID-19. While during the pandemic, one of the most difficult challenges facing the globe was to produce enough vaccines to immunize every citizen, which was a huge undertaking to ensure that vaccines were distributed to citizens without spoiling them. Due to lockdowns and other limitations brought on by the outbreak, some businesses were forced to alter their business plans and implement home delivery options. Additionally, this called for efficient cold chain logistics solutions. Demand increased even more due to growing consumer awareness and the necessity of upholding essential quality standards.

Cold Chain Packaging Market Trends

Growth in Pharmaceutical Sector to Augment the Cold Chain Packaging Market

- According to Almac Pharma Services, the pipeline of biological drugs in development is becoming more temperature-sensitive, resulting in an increase in the storage of bulk drug substances at frozen temperatures (-40 to -70 °C). The company adds that labeling, packing, and distributing cell and gene therapy products often requires products to be stored and processed at ultra-low temperatures (-20 to -80 °C), with the products only being defrosted immediately before use.

- The high-value pharmaceutical products are mostly shipped via the cold chain across the entire distribution network worldwide. Thus, pharmaceutical growth is anticipated to propel the cold chain packaging market. According to International Trade Center, the value of exports of pharmaceutical products from the United Kingdom to the European Union show that in that year, Belgium was the EU member with the largest export value of such British goods, amounting to almost 2.43 billion British pounds. The significant export value represents that the packaging conditions may choose cold chain packaging to adapt to dynamic conditions such as temperature, mode of transportation,etc.

- Moreover, the cold chain packaging market is directly influenced by the continuous growth in demand for cold storage medicinal products used in the healthcare industry. Regionally, the cold chain packaging market is dominated by Europe and North America region. This is due to the high number of biopharmaceuticals imports & exports in the countries in Europe and North America. These regions are also the innovators for the improvement in shipping and warehousing of pharmaceutical products.

- Further, the market is witnessing an effect due to government regulations regarding the use of materials in cold chain packaging. There is also a strong demand for more sustainable designs, including re-use programs, to reduce the carbon footprint. The interest in temperature-controlled packaging is also impacted by changing regulations and standards. For instance, ISTA's (International Safe Transit Association) temperature profiles were altered within the past five years. Such changes are anticipated to affect the market.

Europe to Hold the Largest Market Share

- Europe occupies the major share in the cold chain packaging market. The market is expected to grow significantly in the forecast period owing to continuous growth in demand for cold storage medicinal products used in the healthcare industry.

- Many companies have focused on investments and research and development activities on creating innovative cold chain packaging technologies to stay ahead of the competition. For instance, in May 2022, Essentra Packaging collaborated with AMD to create a new generation of Time Temperature Indicators (TTIs), a smart packaging technology for the pharmaceutical industry. The collaboration by the United Kingdom-based companies aims to provide future packaging solutions that are relevant and improve patient safety by combining the strengths of AMD and Essentra Packaging.

- Additionally, European businesses are creating advancements in enhancing pharmaceutical packaging and storage by implementing cold chain solutions. For instance, in July 2022, the Netherlands' Sharp plant in Heerenveen increased the range of healthcare service offerings. Sharp is a prominent player in contract packaging and clinical supply services. Labeling and secondary packaging services have been added to the site to accommodate open and randomized clinical trials, enhancing the clinical storage and distribution capabilities already there. Already finished are the initial packaging and labeling procedures. Sharp can now provide a full range of clinical services out of the facility, including secondary packaging between temperatures of -80°C and -80°C, storage between 2 and 8°C, and on dry ice as QP release for clinical trial materials. The website's customers can get help with regulatory issues to release and distribute items in Europe.

- Furthermore, many European-based businesses are engaged in corporate growth to broaden their reach internationally due to the growing number of pharmaceutical and life sciences enterprises across the continent. For instance, in February 2022, the life sciences and healthcare (LSHC) sector of the Deutsche Post DHL Group's logistics company, DHL Supply Chain, announced that it would invest more than USD 400 million this year to expand its pharmaceutical and medical device distribution network footprint by 27 percent or nearly 3 million additional square feet. The new buildings will have complete licensing, temperature-controlled space that satisfies pharmaceutical storage needs, and integrated solutions that can handle the packing and managed transportation.

Cold Chain Packaging Industry Overview

The cold chain packaging market is moderately fragmented due to a few players having a significant share in the market. Some of the major players are Cold chain Technologies, Sonoco Thermosafe, Sofrigram, Softbox Systems, Cryopak, Sealed Air Corporation, DGP Intelsius LLC., Amcor Plc, among others.

- March 2022 - The acquisition of Packaging Technology Group, LLC, a prominent supplier of environmentally friendly, curbside-recyclable thermal packaging solutions for the life sciences sector, was announced by Cold Chain Technologies, LLC. Through this agreement, the Packaging Technology Group Company will be able to make more investments in vital sustainable technologies and provide its customers worldwide with a wider range of innovative solutions.

- December 2021 - Recycold Cool Solutions BV, a producer of eco-friendly cool packs, has been acquired by Ranpak Holdings Corp. Recycold Cool Packs, which are constructed from a drain-safe, plant-based gel, unlike conventional cool packs, have been added to increase the variety of Ranpak's Cold Chain packaging solutions.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitutes

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Market Drivers

- 4.4.1 Growth in Pharmaceutical and Healthcare Sector to Boost the Market

- 4.4.2 Increasing Consumer Demand for Perishable Food

- 4.5 Market Restraints

- 4.5.1 Government Regulations Regarding the Use of Materials with Low Carbon

- 4.5.2 Rising Cost of Raw Material

- 4.6 Assessment of Impact of COVID-19 on the Market

5 MARKET SEGMENTATION

- 5.1 By Product

- 5.1.1 Insulated Containers

- 5.1.2 Refrigerants

- 5.1.3 Temperature Monitoring

- 5.2 By End User Applications

- 5.2.1 Food

- 5.2.2 Dairy

- 5.2.3 Pharmaceutical

- 5.2.4 Other End-user Applications

- 5.3 Geography

- 5.3.1 North America

- 5.3.2 Europe

- 5.3.3 Asia Pacific

- 5.3.4 Rest of the World

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Pelican BioThermal LLC

- 6.1.2 Sonoco Thermosafe

- 6.1.3 Cold Chain Technologies Inc.

- 6.1.4 Cryopak Industries Inc.

- 6.1.5 Sofrigam Company

- 6.1.6 Intelsius (A DGP Company)

- 6.1.7 Coolpac

- 6.1.8 Softbox Systems Ltd.

- 6.1.9 Clip-Lok SimPak

- 6.1.10 Chill-Pak.com.

7 INVESTMENT ANALYSIS

8 FUTURE OF THE MARKET

2032 年低温运输包装市场预测:按产品类型、包装系统、材料类型、可用性、温度要求、最终用户和地区进行的全球分析

2032 年低温运输包装市场预测:按产品类型、包装系统、材料类型、可用性、温度要求、最终用户和地区进行的全球分析 2025年低温运输包装全球市场报告2025年医药低温运输包装全球市场报告

2025年低温运输包装全球市场报告2025年医药低温运输包装全球市场报告 全球医药冷链包装市场研究报告-产业分析、规模、份额、成长、趋势及2025年至2033年预测低温运输包装冷媒市场预测(至 2032 年):按类型、包装类型、应用、最终用户和地区进行的全球分析

全球医药冷链包装市场研究报告-产业分析、规模、份额、成长、趋势及2025年至2033年预测低温运输包装冷媒市场预测(至 2032 年):按类型、包装类型、应用、最终用户和地区进行的全球分析 2025 年至 2033 年冷链包装市场规模、份额、趋势及预测(按产品、最终用户和地区)

2025 年至 2033 年冷链包装市场规模、份额、趋势及预测(按产品、最终用户和地区) 美国医药低温运输包装市场规模、份额、趋势分析报告:按包装类型、基材、温度要求、产品、组件、应用、细分预测,2025-2030 年医药冷链包装市场机会、成长动力、产业趋势分析及2025-2034年预测

美国医药低温运输包装市场规模、份额、趋势分析报告:按包装类型、基材、温度要求、产品、组件、应用、细分预测,2025-2030 年医药冷链包装市场机会、成长动力、产业趋势分析及2025-2034年预测 低温运输包装市场规模、份额、成长分析(按产品、材料类型、应用和地区)-2025-2032 年产业预测低温运输包装市场:按产品类型、应用和地区

低温运输包装市场规模、份额、成长分析(按产品、材料类型、应用和地区)-2025-2032 年产业预测低温运输包装市场:按产品类型、应用和地区