|

市场调查报告书

商品编码

1687988

硬质塑胶包装:市场占有率分析、产业趋势与统计、成长预测(2025-2030)Rigid Plastic Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

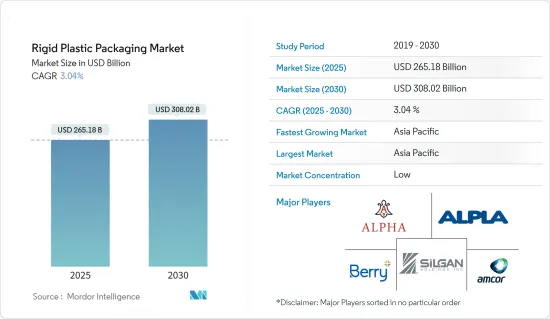

2025 年硬质塑胶包装市场规模估计为 2,651.8 亿美元,预计到 2030 年将达到 3,080.2 亿美元,预测期内(2025-2030 年)的复合年增长率为 3.04%。

硬质塑胶包装是全球包装产业新时代的核心,其多功能性正迅速成为许多包装产品产业的基础。塑胶是世界上最突出的包装材料之一。其重量轻、成本低的特性使其立即受到所有最终用户的欢迎。

关键亮点

- 永续性正在成为硬质塑胶包装产业的首要任务。最终用户和监管机构要求更永续的解决方案,包括再生材料、减少塑胶消费量和环保选择。

- 硬包装的可回收性明显高于软包装。主要原因是硬质包装通常是单一聚合物的整体结构,这使得它比软包装中通常使用的整体多层结构更容易回收。

- 随着环保意识的增强,製造商越来越意识到环保产品的重要性。因此,人们对传统合成产品的清洁替代品的偏好预计将推动对Oxo生物分解性塑胶的需求。

- 硬质塑胶因其可回收和可持续的特性,目前是世界上最值得信赖的包装材料之一。在过去的几十年里,它影响了当前的生产趋势,提供了卓越的品质、耐用性和永续性。食品和饮料、化妆品、製药、工业和汽车等终端用户领域对硬质塑胶包装解决方案的需求正在增长。

- 由于人们对环境问题的担忧日益加剧,预计市场将面临监管标准的动态变化所带来的重大挑战。世界各国政府正在回应公众对塑胶包装废弃物尤其是塑胶包装废弃物的担忧,并实施法规以尽量减少环境废弃物并改善废弃物管理流程。

- 与塑胶使用相关的环境问题日益严重是塑胶包装替代品市场成长的主要原因。与硬质包装解决方案相比,软质塑胶包装具有更广泛的应用,因此成为包装製造商高度青睐的替代方案。此外,软包装所需的材料较少,产品与包装的比例比硬包装高得多。

硬质塑胶包装市场趋势

聚对苯二甲酸乙二酯(PET)显着成长

- PET 塑胶瓶已成为笨重且易碎的玻璃瓶的广泛替代品,因为它们为矿泉水和其他饮料提供了可重复使用的包装,并且使运输过程更加经济。 PET 的高透明度和天然的二氧化碳阻隔性能使其用途广泛,易于吹製成瓶并形成其他形状。可以透过着色剂、紫外线防护剂、氧气阻隔剂/清除剂和其他添加剂来改善 PET 的性能,从而使品牌能够开发出适合其特定需求的瓶子。

- 在硬质包装产业,PET 可用于生产微波食品托盘和软性饮料、水、果汁、运动饮料、啤酒、漱口水、番茄酱、沙拉酱和食品罐的塑胶瓶。居家医疗、饮料和个人护理等各个终端用户行业对宝特瓶的需求正在增长。成长的动力来自于消费者的偏好以及宝特瓶的特性,例如重量轻、可回收性高。

- 一些跨国公司越来越意识到将 PET 回收製成饮料容器等食品级产品的迫切性。这推动了 PET 需求的成长。例如,可口可乐计划在2030年在其包装中使用50%的再生PET。联合利华、欧莱雅和宝洁等大公司已宣布大幅增加包装中消费后再生(PCR)树脂的使用量,使其翻一番,其中PET是首选树脂类型。例如,联合利华承诺在2025年实现100%的塑胶包装可重复使用或回收。

- 市场供应商正致力于提高 PET 一次性包装的可回收性,以符合法规要求并创建闭合迴路回收週期。对回收材料的日益重视预计将为 PET 一次性包装提供成长前景。

- 例如,2023 年 10 月,可口可乐印度公司在全国多个市场为其旗舰品牌可口可乐推出了 250 毫升和 750 毫升包装尺寸的全再生宝特瓶。该公司的策略包括在市场上促销低价包装以吸引更多消费者,并帮助消费者选择小包装以抵消高通膨的影响。

- 根据美国塑胶工业协会(PLASTICS)硬质塑胶包装小组(RPPG)的数据,塑胶占全球包装产业的三分之一,其中很大一部分是硬质塑胶包装。此外,根据经合组织的报告,预计2019年至2060年间全球塑胶使用量将成长168%,到2060年将达到12亿吨,这进一步推动了市场研究。

亚太地区占很大市场占有率

- 中国的宝特瓶和其他硬包装的回收率大幅提高。目前正在推行多种策略来解决循环经济问题,包括使用替代材料、投资开发生物基塑胶以及设计包装以形成循环循环。

- 中国在2021-2025年五年规划中表示,将提高塑胶回收和焚烧能力,推广「绿色」塑胶产品,并打击包装和农业中塑胶的滥用。新的五年计画还要求鼓励商店和宅配业者减少「不合理」的塑胶包装,到2025年将都市区垃圾焚烧率从去年的每天58万吨提高到大约80万吨。预计此类发展将增加国内对可回收硬质塑胶包装的需求。

- 人口成长、劳动人数增加以及忙碌的生活方式等关键因素正在推动该行业的发展。最终用户领域的预期成长正在推动硬质塑胶包装产业的需求。

- 为了减少塑胶对环境的影响,印度也注重塑胶产品的再利用和回收,其中饮料业的公司已经合作推动回收。

- 例如,2024 年 1 月,可口可乐印度公司和 Reliance Retail 宣布启动一项名为「Bhool Na Jana, Plastic Bottle Lautana」的可持续发展倡议,重点是透过孟买 Reliance Retail 商店的反向自动贩卖机 (RVM) 和收集箱收集消费后 PET。该先导计画旨在创建循环经济,符合印度政府的「清洁印度」计划,将在孟买和德里的 36 家 Reliance Retail 商店(包括 Smart Bazaar 和 Sahakari Bhandar)启动,併计划到 2025 年扩展到印度各地的 200 家商店。

- 日本漫长的海岸线对日本经济成长产生了重大影响。战略定位,有利于贸易和海上活动,使日本成为世界主要贸易国之一。

硬质塑胶包装市场概况

硬质塑胶包装行业的特点是分散,主要企业包括 Amcor PLC、Berry Global Inc.、Sealed Air Corporation 和 Greif Inc.,以及许多其他製造商。儘管进入门槛很高,但在工业、食品和饮料强劲需求的推动下,区域包装公司正在意识到进入硬质包装领域的价值。市场领导者正在利用竞争策略,专注于收购、合作、强大的研发和尖端创新。

- 2024 年 3 月 - Mauser Packaging Solutions 和 Rikutec Packaging 建立独家伙伴关係关係,共同推动永续 IBC 解决方案的发展。两家公司将生产和销售专门满足高纯度需求的顶级多向包装。此次合作将推出最先进的、可重复使用的重型 1,000 公升 IBC,并透过 Rikutec 的创新产品增强 Mauser 的产品组合。

- 2024 年 1 月 – ALPLA 收购波多黎各的 Fortiflex。两家公司一直合作为加勒比海和中美洲市场生产包装产品。透过收购 Fortiflex,ALPLA 旨在加强其 2023 年成立的工业部门,该部门专门从事大容量包装解决方案,并扩大提案。 2023年,ALPLA和Fortiflex均在哥斯大黎加建立了一条新的桶生产线。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概览

- 产业价值链分析

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买家/消费者的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

第五章市场动态

- 市场驱动因素

- 新法规预计将增加对氧化可分解塑胶的需求

- 终端用户产业对硬质塑胶包装解决方案的需求不断增长

- 市场问题

- 塑胶业严格立法

- 与软质塑胶包装的竞争

第六章市场区隔

- 依产品类型

- 瓶子和罐子

- 托盘和容器

- 瓶盖和瓶塞

- 中型散装容器(IBC)

- 鼓

- 调色盘

- 其他的

- 按材质

- 聚乙烯(PE)

- 聚对苯二甲酸乙二醇酯(PET)

- 聚丙烯(PP)

- 聚苯乙烯(ps)和发泡聚苯乙烯(EPS)

- 聚氯乙烯(PVC)

- 其他硬质塑胶包装材料

- 按最终用户

- 食物

- 饮料

- 医疗保健

- 化妆品和个人护理

- 工业的

- 建筑与施工

- 汽车

- 其他的

- 按地区

- 北美洲

- 美国

- 加拿大

- 欧洲

- 法国

- 德国

- 义大利

- 英国

- 西班牙

- 波兰

- 亚洲

- 中国

- 印度

- 日本

- 泰国

- 澳洲

- 拉丁美洲

- 巴西

- 阿根廷

- 墨西哥

- 中东和非洲

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 南非

- 北美洲

第七章竞争格局

- 公司简介

- Amcor Group GmbH

- Alpha Packaging Inc.

- Berry Global Inc.

- Alpla Group

- Silgan Holdings Inc.

- Sealed Air Corporation

- Plastipak Holding Inc.

- Sonoco Products Company

- Resilux NV

- Graham Packaging Company Inc.

- Greif Inc.

- Mauser Packaging Solutions(Bway Holding Corporation)

- Pact Group Holdings Ltd

- Gerresheimer AG

第八章投资分析

第九章 市场机会与未来趋势

The Rigid Plastic Packaging Market size is estimated at USD 265.18 billion in 2025, and is expected to reach USD 308.02 billion by 2030, at a CAGR of 3.04% during the forecast period (2025-2030).

Rigid plastic packaging is at the centre of a new era in the global packaging industry, and its versatile usage is becoming the foundation for many industries that package their products. Plastic is one of the most prominent packaging materials in the world. Its lightweight and low-cost nature instantly made it prominent among all end-users.

Key Highlights

- Sustainability is becoming a top priority for the rigid plastics packaging industry. End users and regulators demand more sustainable solutions, such as recycled materials, reduced plastic consumption, and eco-friendly options.

- The recyclability of rigid packaging is significantly higher than that of flexible packaging. The main reason is that rigid packaging typically has a mono-polymer monolithic structure, which is much easier to recycle than the monolithic multi-layer structures commonly used in flexible packaging.

- With rising environmental concerns, manufacturers have ever-grown awareness about the importance of environmentally friendly products. As a result, the preference for clean substitutes from conventional synthetic products is expected to drive the demand for oxo-biodegradable plastics.

- Rigid plastic is presently one of the world's most trusted packaging materials due to its recyclable and sustainable characteristics. Over the past few decades, it has continued influencing current production trends, providing superior quality, durability, and sustainability. The demand for rigid plastic packaging solutions has been experiencing growth across end-user sectors such as food, beverage, cosmetics, pharmaceuticals, industrial, automotive, etc.

- The market is expected to be significantly challenged due to dynamic changes in regulatory standards, primarily due to increasing environmental concerns. Governments worldwide are responding to public concerns regarding plastic packaging waste, especially plastic packaging waste, and implementing regulations to minimize environmental waste and improve waste management processes.

- Growing environmental concerns associated with plastic usage are a primary reason for the growth of alternatives for plastic packaging in the market. Flexible plastic packaging is highly preferred as an alternative by packaging manufacturers due to its wide applications in replacing rigid packaging solutions. Furthermore, flexible packaging requires less material, resulting in a significantly higher product-to-package ratio than its rigid counterparts.

Rigid Plastic Packaging Market Trends

Polyethylene Terephthalate (PET) to Register Significant Growth

- Plastic bottles made from PET are widely replacing heavy and fragile glass bottles since they offer reusable packaging for mineral water and other beverages, allowing a more economical transportation process. With its clarity and natural CO2 barrier properties, PET has wide applications and is easily blown into a bottle or molded into any other shape. PET properties can be improved with colorants, UV blockers, oxygen barriers/scavengers, and other additives to develop a bottle to match a brand's specific needs.

- In the rigid packaging industry, PET manufactures microwavable food trays and plastic bottles for soft drinks, water, juices, sports drinks, beer, mouthwash, ketchup, salad dressings, and food jars. There is a growing demand for PET bottles from various end-user industries, such as home care, beverages, and personal care. The growth is driven by consumer preference and its properties, such as being lightweight and having a high recycling rate.

- Several global companies increasingly recognize the urgency of recycling PET into food-grade products, such as beverage containers. This can drive the growth of the demand for PET. For instance, the Coca-Cola Company intends to use 50% recycled PET in its containers by 2030. Major companies, such as Unilever, L'Oreal, and P&G, announced a significant increase, thereby doubling the usage of post-consumer recycled (PCR) resins in their packaging, for which PET was a desirable resin type. For instance, Unilever is committed to making 100% of its plastic packaging reusable or recyclable by 2025.

- Market vendors are focusing on increasing the recyclability of PET single-use packaging to adhere to the regulations and create a closed-loop recycling cycle. The increasing emphasis on recycling these materials is expected to provide growth prospects for PET single-use packaging.

- For instance, in October 2023, Coca-Cola India introduced fully recycled PET bottles in pack sizes of 250 ml and 750 ml for its flagship Coca-Cola brand across multiple markets in the country. The company's strategy includes promoting low-priced packs in the market to attract more consumers and assist shoppers in selecting smaller packs to counteract the impact of high inflation.

- According to the Plastics Industry Association (PLASTICS)'s Rigid Plastic Packaging Group (RPPG), plastics account for one-third of the global packaging industry, and much of this plastic packaging is rigid. In addition, as stated by an OECD report, plastics use worldwide is expected to grow by 168 per cent from 2019 to 2060, reaching 1.2 billion metric tonnes by 2060, driving the market studied.

Asia-Pacific Holds Significant Market Share

- China is witnessing significant recycling rates in plastic bottles and other rigid packaging options. Multiple strategies are being advanced to address the issue of a circular economy, including substituting for alternative materials, investments toward the development of bio-based plastics, and designing packaging to make the circular loop.

- In a 2021-2025 "five-year plan," China announced it would improve its plastic recycling and incineration capacities, promote "green" plastic products, and combat the misuse of plastic in packaging and agriculture. The new five-year plan would push merchants and delivery companies to reduce "unreasonable" plastic wrapping and increase garbage incineration rates in cities to about 800,000 tons per day by 2025, up from 580,000 tons last year. Such developments are expected to increase the country's demand for recyclable rigid plastic packaging.

- Significant factors like the growing population drive the industry, increasing working individuals, and hanging lifestyles with busy schedules. Growth prospects of end-user segments are leading to a rise in the need for the rigid plastic packaging industry.

- India is also focused on reusing and recycling plastic products as part of lowering the environmental impact of plastics, and as part of this, companies operating in the beverage industry are partnering to promote recycling.

- For instance, in January 2024, Coca-Cola India and Reliance Retail announced the launch of a sustainability initiative titled 'Bhool Na Jana, Plastic Bottle Lautana,' focused on post-consumer PET collection at Reliance Retail stores in Mumbai via Reverse Vending Machines (RVMs) and collection bins. With an idea for a circular economy, this pilot project, aligned with the Government's Swachh Bharat Mission, has begun in 36 Reliance Retail stores, including Smart Bazaar and Sahakari Bhandar stores in Mumbai and Delhi, and will extend to 200 stores across India by 2025 with a target of collecting 5,00,000 PET bottles annually in the pilot phase.

- Japan's long coastline has significantly impacted the country's economic growth. The country's strategic location along essential sea routes has made it easier to trade and conduct maritime activities, which has helped Japan to become one of the top trading countries in the world.

Rigid Plastic Packaging Market Overview

The rigid plastic packaging industry is characterized by fragmentation, featuring prominent players like Amcor PLC, Berry Global Inc., Sealed Air Corporation, and Greif Inc., alongside numerous other manufacturers. Despite high entry barriers for newcomers, regional packaging firms are increasingly recognizing the value of entering the rigid packaging domain, driven by robust demand from sectors such as industrial, food, and beverages. Major players in the market are leveraging competitive strategies, focusing on acquisitions, partnerships, robust R&D, and cutting-edge technological innovations.

- March 2024 - Mauser Packaging Solutions and Rikutec Packaging have forged an exclusive partnership, aligning with the global push for sustainable IBC solutions. Together, they're set to produce and promote top-tier multiway packaging, specifically designed for high-purity needs. This collaboration will see the introduction of a state-of-the-art, reusable, and heavy-duty 1,000-litre IBC, enhancing Mauser's product lineup with Rikutec's innovative offerings.

- January 2024 - ALPLA has acquired Fortiflex, a company based in Puerto Rico. The two firms have collaborated to manufacture packaging products catering to the Caribbean and Central American markets. With the acquisition of Fortiflex, ALPLA aims to bolster its industrial division, which focuses on large-volume packaging solutions established in 2023, and broaden its offerings as a comprehensive provider for its customers. In 2023, both ALPLA and Fortiflex set up a new production line for buckets in Costa Rica.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitutes

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Demand for Oxo-Degradable Plastics is Expected to Increase with New Regulations

- 5.1.2 Increasing Rigid Plastic Packaging Solution Demand Across the End-user Industry

- 5.2 Market Challenges

- 5.2.1 Stringent Laws and Regulations Pertaining to Plastic Industries

- 5.2.2 Competition from Flexible Plastic Packaging

6 MARKET SEGMENTATION

- 6.1 By Product Type

- 6.1.1 Bottles and Jars

- 6.1.2 Trays and Containers

- 6.1.3 Caps and Closures

- 6.1.4 Intermediate Bulk Containers (IBCs)

- 6.1.5 Drums

- 6.1.6 Pallets

- 6.1.7 Other Product Types

- 6.2 By Material

- 6.2.1 Polyethylene (PE)

- 6.2.2 Polyethylene Terephthalate (PET)

- 6.2.3 Polypropylene (PP)

- 6.2.4 Polystyrene (ps) and Expanded Polystyrene (EPS)

- 6.2.5 Polyvinyl Chloride (PVC)

- 6.2.6 Other Rigid Plastic Packaging Materials

- 6.3 By End User

- 6.3.1 Food

- 6.3.2 Beverage

- 6.3.3 Healthcare

- 6.3.4 Cosmetics and Personal Care

- 6.3.5 Industrial

- 6.3.6 Building and Construction

- 6.3.7 Automotive

- 6.3.8 Other End User Industries

- 6.4 By Geography

- 6.4.1 North America

- 6.4.1.1 United States

- 6.4.1.2 Canada

- 6.4.2 Europe

- 6.4.2.1 France

- 6.4.2.2 Germany

- 6.4.2.3 Italy

- 6.4.2.4 United Kingdom

- 6.4.2.5 Spain

- 6.4.2.6 Poland

- 6.4.3 Asia

- 6.4.3.1 China

- 6.4.3.2 India

- 6.4.3.3 Japan

- 6.4.3.4 Thailand

- 6.4.3.5 Australia

- 6.4.4 Latin America

- 6.4.4.1 Brazil

- 6.4.4.2 Argentina

- 6.4.4.3 Mexico

- 6.4.5 Middle East and Africa

- 6.4.5.1 United Arab Emirates

- 6.4.5.2 Saudi Arabia

- 6.4.5.3 South Africa

- 6.4.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Amcor Group GmbH

- 7.1.2 Alpha Packaging Inc.

- 7.1.3 Berry Global Inc.

- 7.1.4 Alpla Group

- 7.1.5 Silgan Holdings Inc.

- 7.1.6 Sealed Air Corporation

- 7.1.7 Plastipak Holding Inc.

- 7.1.8 Sonoco Products Company

- 7.1.9 Resilux NV

- 7.1.10 Graham Packaging Company Inc.

- 7.1.11 Greif Inc.

- 7.1.12 Mauser Packaging Solutions (Bway Holding Corporation)

- 7.1.13 Pact Group Holdings Ltd

- 7.1.14 Gerresheimer AG

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

硬质塑胶包装市场,全球预测:材料类型、产品类型、最终用途产业和製造流程 - 全球预测 2025-2032

硬质塑胶包装市场,全球预测:材料类型、产品类型、最终用途产业和製造流程 - 全球预测 2025-2032 2025年硬质塑胶包装全球市场报告

2025年硬质塑胶包装全球市场报告 全球硬质塑胶包装市场研究报告-产业分析、规模、份额、成长、趋势及2025年至2033年预测

全球硬质塑胶包装市场研究报告-产业分析、规模、份额、成长、趋势及2025年至2033年预测 硬质塑胶包装的印度市场:类别,各流程,各产品,各终端用户产业,各地区,机会,预测,2019年~2033年

硬质塑胶包装的印度市场:类别,各流程,各产品,各终端用户产业,各地区,机会,预测,2019年~2033年 硬质塑胶包装的未来(~2030年)

硬质塑胶包装的未来(~2030年) 2025 年至 2033 年硬质塑胶包装市场规模、份额、趋势及预测(依产品、材料、生产流程、最终用途产业及地区)

2025 年至 2033 年硬质塑胶包装市场规模、份额、趋势及预测(依产品、材料、生产流程、最终用途产业及地区) 硬质塑胶包装市场规模、份额、趋势分析报告:按材料、生产过程流程、产品、应用、地区、细分市场预测,2025-2030 年

硬质塑胶包装市场规模、份额、趋势分析报告:按材料、生产过程流程、产品、应用、地区、细分市场预测,2025-2030 年 硬质塑胶包装市场(2025-2029)

硬质塑胶包装市场(2025-2029) 2032 年硬质塑胶包装市场预测:按包装类型、材料类型、技术、应用、最终用户和地区进行的全球分析

2032 年硬质塑胶包装市场预测:按包装类型、材料类型、技术、应用、最终用户和地区进行的全球分析 印尼硬质塑胶包装:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)

印尼硬质塑胶包装:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)