|

市场调查报告书

商品编码

1687992

仓储服务:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Warehousing and Storage Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

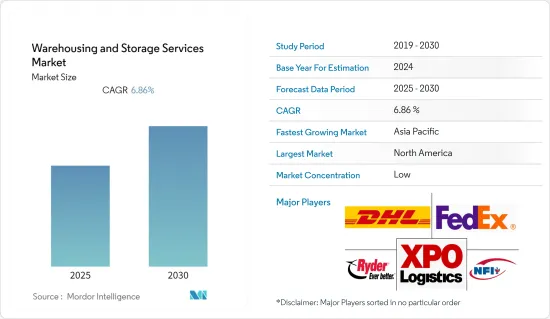

预计仓储和储存服务市场在预测期内的复合年增长率将达到 6.86%。

工业部门的成长、对製成品、加工和冷冻食品的需求不断增加以及电子商务产业的扩张是推动仓储和储存服务需求的一些主要因素。

关键亮点

- 仓储和存储服务描述的是其他企业或组织的财产的存储,例如零件、设备、车辆、成品和生鲜产品。全通路模式需求的不断增长预计将推动市场的发展。儘管消费者已经接受了网上购物的趋势,但线下商店仍然占据着相当大的市场占有率,并且正在扩大仓储市场,特别是在家具等大宗商品领域。

- 随着供应链重组以满足比以往任何时候都更快的需求,仓库也越来越多地整合物流,而物流服务在这过程中发挥关键作用。此外,随着全球趋势进一步扩大,全球营运的行业的很大一部分库存经常从海外交付到仓库,透过供应链运输成品,这也推动了对仓储服务的需求。

- 需求的成长和储存新型产品的要求对仓储服务供应商的复杂性产生了重大影响,他们现在开始寻找可以帮助降低复杂性并为他们提供更好地管理设施的工具的创新技术。例如,仓储系统就是这样一种解决方案,它提供了公司整个库存和供应链履约业务的可视性,从配送中心到商店货架。

- 此外,仓储服务供应商还专注于优化食材、处理和拣选流程,以进一步缩短交货时间,同时确保交货品质。这些趋势正在推动新仓库建设和管理技术的发展。此外,为了与全球参与企业竞争,许多供应商在其仓储业务中采用了 GPS、RFID、VoIP 设备、数位语音和影像技术等新技术。

- 然而,仓储服务提供者面临的主要挑战之一是建立仓库和引进先进技术所需的高额投资。此外,中小企业缺乏意识和全球通用标准也对市场成长构成挑战。

- 受新冠疫情影响,许多仓库比以往任何时候都更加运作,主要经营食品、药品和日用品。亚马逊、Aldi、Asda 和 Lidl 均表示需要扩大产能并僱用更多仓库员工。虽然某些行业,特别是工业和製造业的需求减少,尤其是在初始阶段,但预计未来几年市场将逐步復苏。

冷藏冷冻仓库市场趋势

冷藏仓库和仓储产业强劲成长

- 冷藏仓库和储存设施处理需要在冷藏控制室储存的产品。它也是低温储存和保存易腐烂产品的地方。大多数冷藏库或冷藏仓库的设计都具有能够将物品保存在最佳条件下的特性。冷藏和仓储行业的机构提供回火、冷冻和气调储藏等服务。

- 冷藏仓储和储存市场呈现正面成长趋势,主要集中在製药和食品饮料领域。护理品质委员会建议将胰岛素、抗生素液体、注射、眼药水和一些药膏储存在 20°C 至 80°C 之间,以保持其有效性。根据美国人口普查局的数据,2021 年有 1.1745 亿美国使用眼药水或洗眼液。预计到 2023 年这一数字将上升到 1.1849 亿。液体药物需求的成长,尤其是在大流行之后,预计将对市场成长产生积极影响。

- 在运输和储存对温度敏感的产品时,冷藏保管是供应链管理 (SCM) 的重要组成部分。此外,北美自由贸易协定(北美自由贸易组织(NAFTA) )等双边自由贸易协定正在创造新的机会,允许美国供应商扩大生鲜食品贸易,同时最大限度地降低进口关税。此类贸易协定有利于市场成长。

- 考虑到对冷藏的需求不断增长,市场上的供应商不断致力于扩大其足迹。例如,根据国际冷藏仓库协会(IARW)的统计,Lineage 物流是北美最大的冷藏物流供应商,拥有42,526,060立方公尺的控温空间。

预计北美将占很大份额

- 有几个因素推动着北美仓储物流市场的发展。随着经销商和零售商对储存原材料和成品的物流需求不断增加,製造商越来越多地将仓储服务外包,以专注于扩大生产和业务。此外,业务效率的提高和成本的节约正在促使托运人将物流业务委託给仓储服务供应商。

- 亚马逊和沃尔玛等零售和电子商务巨头的存在极大地促进了该地区对仓储和储存服务的需求。据沃尔玛称,截至 2022 年,该公司使用 31 个纯电子商务履约中心和 4,700 家位于 90%美国人口 10 英里范围内的商店来配送线上订单。

- 根据对美国亚马逊卖家的调查,卖家在上游仓储配送业务面临的三大痛点为收费系统复杂、仓储成本高、仓储容量不足。为了应对这些挑战,供应商越来越注重製定新的商务策略来吸引更多的客户。例如,亚马逊于 2022 年 9 月宣布了一项新服务,该服务将允许卖家使用新建的专用设施进行大量库存储存和自动配送。

- 由于製造业、零售业和製药业的显着成长,美国市场显示出潜在的成长。根据美国商务部的数据,到 2021 年,美国仓储业的销售额将增加至 5,049 万美元。随着供应商继续专注于扩大其设施,预计这一趋势将会成长。

- 此外,北美是快速采用新技术的地区,因此预计新仓储和储存技术的采用率将保持在高位。此外,所需的基础设施、不断增强的意识和熟练劳动力的可用性也是支持这一趋势的其他重要因素。

仓储服务业概况

仓储和储存服务市场竞争激烈,主要是因为存在多个参与企业。由于进入门槛相对较低,预计竞争将会加剧。长期伙伴关係、合併、收购以及对仓库软体的大量投资是公司在日益激烈的竞争中保持生存所采用的主要成长策略。市场的主要企业包括 DHL International Gmbh、XPO Logistics Inc. 和 FedEx Corp。

- 2022 年 9 月 - 领先的合约物流供应商 GXO Logistics Inc. 与拜耳合作开设了新的仓库设施。 GXO 将在内布拉斯加州科尔尼开设一个占地 350,000 平方英尺的新工厂,并将透过其共用空间物流网络 GXO Direct 为拜耳作物科学部门管理仓库支持,包括所有入站和出站业务。

- 2022 年 5 月—温控物流中心开发商和营运商 Vertical Cold Storage 从 US Cold Storage 手中收购了位于佛罗里达州、内布拉斯加州和北卡罗来纳州的三个公共冷藏仓库。该公司进行这些收购是为了支持其不断扩大的蛋白质业务,其中包括家禽、肉类、家禽和鱼贝类。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概览

- 产业价值链分析

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争强度

- COVID-19 市场影响

第五章市场动态

- 市场驱动因素

- 全通路分销日益普及

- 电子商务产业的成长

- 市场限制

- 投资和维护成本高

第六章市场区隔

- 按类型

- 普通仓库和仓储

- 冷藏仓库

- 农产品仓储

- 拥有者

- 个人仓库

- 公共仓库

- 保税仓库

- 按最终用户产业

- 製造业

- 消费品

- 饮食

- 零售

- 医疗保健

- 其他的

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

第七章竞争格局

- 公司简介

- DHL International GmbH

- XPO Logistics Inc.

- Ryder System Inc.

- NFI Industries Inc.

- AmeriCold Logistics LLC

- FedEx Corp

- Lineage Logistics Holding LLC

- NF Global Logistics Ltd

- APM Terminals BV

- DSV Panalpina AS

- Kane Is Able Inc.

- MSC-Mediterranean Shipping Agency AG

第八章投资分析

第九章:未来市场展望

The Warehousing and Storage Services Market is expected to register a CAGR of 6.86% during the forecast period.

The growth of the industrial sector, increasing demand for manufactured products, processed and frozen food products, and the expansion of the e-commerce industry are among the significant factors driving the demand for warehousing and storage services.

Key Highlights

- Warehousing and storage services provide storage for another company or organization's property, including parts, equipment, vehicles, products, and perishable goods. The increasing demand for an omnichannel model is expected to drive the market. Although customers embrace the online buying trend, offline stores still hold a significant market share, especially in the big-ticket products segment, such as furniture, which expands the warehouse and storage market.

- With supply chains being reconfigured to meet demand faster than ever, warehouses are increasingly integrating logistics, as logistics services play a crucial role in this process. Additionally, with the globalization trend further expanding its scope, a significant portion of the inventory of industries that operate globally is delivered frequently from abroad to a warehouse to transfer finished goods through the supply chain, which in turn is also driving the demand for warehouse and storage services.

- The growth in demand and requirement to store new product types have significantly impacted the complexity of the warehouse service providers, who now have started to look for innovative technologies that can help them reduce the complexity and provide them with tools to manage the facility better. For instance, Warehouse Management System is one such solution that offers visibility into a business' entire inventory and works supply chain fulfillment operations from the distribution center to the store shelf.

- Furthermore, warehousing/storage service providers are also focusing on optimizing their batching, handling, and picking processes to enhance delivery times further while ensuring the quality of delivery. Such trends facilitate the development of new warehouse construction and management techniques. Additionally, to compete with global players, many vendors are adopting emerging technologies, such as GPS, RFID, VoIP devices, digital voice, and imaging technology for warehouse operations.

- However, the higher investment required to set up warehouses and adopt advanced technologies is among the significant challenges warehouse/storage service providers face. Furthermore, a lack of awareness among SMEs and common global standards also challenges the market's growth.

- COVID-19 resulted in many warehouses running busier than ever, mainly catering to food products, pharmaceuticals, and essential household goods. Amazon, Aldi, Asda, and Lidl have all reported a need to increase their capacities and hire an additional warehouse workforce. Although in some sectors, especially in the industrial and manufacturing domain, the demand declined, especially during the initial phase, the market is expected to recover gradually in the coming years.

Warehousing and Storage Market Trends

The Refrigerated Warehousing and Storage Segment to Grow Significantly

- The refrigerated warehousing and storage facilities deal with products that require refrigerated and controlled rooms for storage. It also refers to where perishable products are stored or kept at low temperatures. Most of these cold storage rooms or refrigerated warehouses are designed with properties that can keep the items within optimum conditions. Establishments in the refrigerated warehousing and storage industry provide services, such as tempering, blast freezing, and modified atmosphere storage services.

- Refrigerated warehousing and storage are showing positive trends toward market growth, mainly in the pharma and food and beverage sectors. The Care Quality Commission recommends that insulins, antibiotic liquids, injections, eye drops, and some creams must be stored between 20C and 80C to maintain the effectiveness of the medicines. According to the U.S. Census Bureau, 117.45 million Americans used eye drops and eyewash in 2021. This figure is projected to increase to 118 .49 million in 2023. The increasing demand for liquid pharmaceutical products, especially after the pandemic, is expected to impact the market's growth positively.

- Refrigerated storage is integral to Supply Chain Management (SCM) when transporting and storing temperature-sensitive products. New opportunities are also being created by bilateral free trade agreements, such as the North America Free Trade Agreement (NAFTA), which allows vendors in the United States to increase the trading of perishable food products with minimal import duties. Such trade agreements favor the market's growth.

- Considering the growing demand for cold storage warehouses, the vendors operating in the market continuously focus on expanding their footprint. For instance, according to the International Association of Refrigerated Warehouses (IARW), Lineage Logistics was the most extensive refrigerated warehousing and logistics provider in the North American region, with 42,526.06 thousand cubic meters of temperature-controlled space.

North America is Expected to Hold a Major Share

- Several factors also drive the warehousing and storage market in the North American region. An increase in logistics needs for storing raw materials and finished goods for distributors and retailers has been growing as manufacturing companies increasingly outsource warehousing services to focus on productional and operational expansions. Additionally, enhanced operational efficiency and cost savings encourage shippers to outsource the logistics portion of their activities to warehouse service providers.

- The presence of retail and e-commerce giants, such as Amazon and Walmart contributes significantly to the region's demand for warehouse and storage services. According to Walmart, as of 2022, the company uses 31 dedicated e-commerce fulfillment centers and 4,700 stores within 10 miles of 90% of the U.S. population to fulfill online orders.

- According to a survey of U.S. Amazon sellers, the three most significant pain points for sellers in upstream warehousing and distribution operations were complicated fee structures, high prices for storage, and insufficient storage capacity. To address these challenges, vendors are increasingly focusing on developing new business strategies to attract more customers. For instance, in September 2022, Amazon announced new services to enable sellers to use new, purpose-built facilities for bulk inventory storage and automated distribution.

- With significant growth in the manufacturing, retail, and pharma units, the market shows potential growth in the United States. According to the U.S. Department of Commerce, the U.S. warehousing and storage industry's revenue increased to USD 50.49 million in 2021. With vendors continuously focusing on expanding their facilities, such trends are only expected to grow further.

- Furthermore, the adoption rate of new warehouse and storage technologies is expected to remain high in the North American region as the region is among the early adopters of new technologies. Additionally, the required infrastructure heightened awareness, and availability of a skilled workforce are other significant factors supporting such trends.

Warehousing and Storage Industry Overview

The warehousing and storage services market is competitive, mainly because of the presence of several players. The competition is expected to intensify because of the relatively low entry barriers. Long-term partnerships, mergers, acquisitions, and high investments in warehouse management software are the prime growth strategies adopted by companies to sustain the growing competition. Some major players operating in the market include DHL International Gmbh, XPO Logistics Inc., and FedEx Corp, among others.

- September 2022 - GXO Logistics Inc., a leading pure-play contract logistics provider, opened a new warehouse facility with Bayer. GXO will manage warehouse support, including all shipping and receiving activities, for Bayer's Crop Science division through its shared-space distribution network GXO Direct at the new 350,000-square-foot facility in Kearney, Nebraska.

- May 2022 - Vertical Cold Storage, a developer, and operator of temperature-controlled distribution centers acquired three public refrigerated warehouses in Florida, Nebraska, and North Carolina from US Cold Storage. The company made these acquisitions to support its expanding protein business, including poultry, meat, poultry, and seafood.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rising Popularity of Omnichannel Distribution

- 5.1.2 Growth in the E-commerce Industry

- 5.2 Market Restraints

- 5.2.1 High Investment and Maintenance Costs

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 General Warehousing and Storage

- 6.1.2 Refrigerated Warehousing and Storage

- 6.1.3 Farm Product Warehousing and Storage

- 6.2 By Ownership

- 6.2.1 Private Warehouses

- 6.2.2 Public Warehouses

- 6.2.3 Bonded Warehouses

- 6.3 By End-user Industry

- 6.3.1 Manufacturing

- 6.3.2 Consumer Goods

- 6.3.3 Food and Beverage

- 6.3.4 Retail

- 6.3.5 Healthcare

- 6.3.6 Other End-user Industries

- 6.4 By Geography

- 6.4.1 North America

- 6.4.2 Europe

- 6.4.3 Asia-Pacific

- 6.4.4 Latin America

- 6.4.5 Middle East & Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 DHL International GmbH

- 7.1.2 XPO Logistics Inc.

- 7.1.3 Ryder System Inc.

- 7.1.4 NFI Industries Inc.

- 7.1.5 AmeriCold Logistics LLC

- 7.1.6 FedEx Corp

- 7.1.7 Lineage Logistics Holding LLC

- 7.1.8 NF Global Logistics Ltd

- 7.1.9 APM Terminals BV

- 7.1.10 DSV Panalpina AS

- 7.1.11 Kane Is Able Inc.

- 7.1.12 MSC - Mediterranean Shipping Agency AG

8 INVESTMENT ANALYSIS

9 FUTURE OUTLOOK OF THE MARKET

居家养老住房解决方案市场-全球产业规模、份额、趋势、机会和预测,按住房模式、年龄层(活跃老年人、中老年人、高龄老年人)、地点、地区和竞争情况细分,2020-2030 年预测

居家养老住房解决方案市场-全球产业规模、份额、趋势、机会和预测,按住房模式、年龄层(活跃老年人、中老年人、高龄老年人)、地点、地区和竞争情况细分,2020-2030 年预测 2025年全球医药仓储市场报告2025年全球行销研究与分析服务市场报告

2025年全球医药仓储市场报告2025年全球行销研究与分析服务市场报告 仓库模拟市场,按类型、按部署、按行业垂直、按国家和地区 - 2025 年至 2032 年全球行业分析、市场规模、市场份额和预测

仓库模拟市场,按类型、按部署、按行业垂直、按国家和地区 - 2025 年至 2032 年全球行业分析、市场规模、市场份额和预测 智慧仓库市场(按产品、技术、最终用户、应用、部署模式和组织规模)—2025-2030 年全球预测

智慧仓库市场(按产品、技术、最终用户、应用、部署模式和组织规模)—2025-2030 年全球预测 全球仓库租借市场

全球仓库租借市场 仓库和仓储熏蒸市场 - 预测 2025-2030全球按需仓储市场2025年仓储全球市场报告2025年全球威士忌仓储市场报告

仓库和仓储熏蒸市场 - 预测 2025-2030全球按需仓储市场2025年仓储全球市场报告2025年全球威士忌仓储市场报告