|

市场调查报告书

商品编码

1689739

东南亚电池:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Southeast Asia Battery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

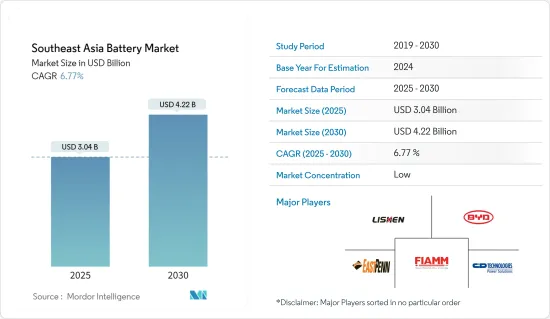

预计2025年东南亚电池市场规模为30.4亿美元,到2030年将达到42.2亿美元,预测期内(2025-2030年)的复合年增长率为6.77%。

儘管2020年新冠疫情对市场产生了负面影响,但目前已恢復至疫情前的水准。

主要亮点

- 从中期来看,汽车产业需求成长、锂离子电池价格下降以及将东南亚定位为资料中心枢纽的计画等因素预计将在预测期内推动市场发展。

- 儘管汽车、资料中心和通讯领域对电池的需求不断增长,但由于大多数国家依赖其他形式的能源储存,预计电池能源储存产业仍将保持低迷。这可能会在预测期内抑制能源储存领域电池市场的成长。

- 此外,预计在预测期内,将可再生能源纳入各国电网的计画将为锂离子电池製造商和供应商带来巨大的商机。

- 由于汽车、资料中心和其他终端用户领域的需求不断增加,预计泰国将在预测期内占据市场主导地位。

东南亚电池市场趋势

预计汽车产业将主导市场

- 以前仅使用内燃机车辆(ICE)。内燃机汽车使用铅酸电池,并且很可能继续使用而不需要进行大规模更换。

- 但现在,由于人们对环境问题的日益关注,科技正在转向电动车。电动车主要使用锂离子电池,这种电池能量密度高、自放电低,几乎不需要维护。

- 锂离子电池系统为插电式混合动力汽车和混合动力汽车车提供动力。锂离子电池具有高能量密度、快速充电能力和高放电功率,是唯一能够满足OEM对车辆续航里程和充电时间要求的技术。铅基牵引电池比能量低、重量大,在全混合动力汽车和电动车上使用不具竞争力。

- 此外,锂离子电池价格大幅下跌,导致其价值下降了 81.5%,从 2013 年的 668 美元/千瓦时跌至 2021 年的 123 美元/kWh。预计这一趋势将持续下去,使该地区更广泛的经济人群能够更负担得起电动车。

- 在混合动力汽车中,有多种电池技术可以以各种组合提供这些功能,但镍氢和锂离子电池由于其快速充电能力、良好的放电性能和持久的寿命,在高电压下更受青睐。

- 随着多个地区政府制定排放计划,预计预测期内电动车(EV)的区域份额将会增加。

- 因此,基于上述因素,预计预测期内汽车产业将主导东南亚电池市场。

泰国可望主导市场

- 泰国占据大部分市场份额。由于汽车、资料中心和通讯业的需求不断增加,预计这一趋势将在预测期内持续下去。

- 泰国的汽车产业具有巨大的投资潜力。该国是东南亚国家联盟主要汽车生产基地之一。五十年来,中国从一个汽车零件组装发展成为汽车製造和出口的顶级中心。

- 此外,预计该国的电动车领域将实现高速成长,尤其是插电式混合动力车 (PHEV) 和混合动力车 (HEV)。 2022年9月,比亚迪宣布计画在曼谷罗勇府兴建海外首个电动乘用车工厂。

- 国家电动车政策委员会 (NEVPC) 发布的蓝图显示,泰国到 2025 年将增加 10 万至 30 万辆汽车,到 2026 年最终将增加 40 万至 75 万辆汽车。

- 此外,2022 年 4 月,泰国政府同意资助生产为电动车 (EV)动力来源的锌离子电池。泰国将在当地建立电动车电池工厂,利用天然资源锌。

- 此外,泰国在资讯通信技术行业的发展方面取得了长足进步,迅速将该国从技术领域的二流参与者提升为地区领先者之一。过去十年,泰国的数位化足迹加速发展,并在劳动力教育和技能建设方面取得了长足的进步。

- 政府已在泰国4.0计划下规划了一个商业模组。该计划推动云端处理、互动媒体、巨量资料和物联网等新技术的使用。因此,该国对资料中心的需求很高,预计预测期内对资料中心电池的需求将增加。

- 因此,基于上述因素,预计泰国将在预测期内主导东南亚电池市场。

东南亚电池产业概况

东南亚电池市场较为分散,主要企业包括天津力神电池股份有限公司、FIAMM Energy Technology SpA、比亚迪、C&D Technologies Inc. 和 East Penn Manufacturing Co. Inc.(排名不分先后)。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究范围

- 市场定义

- 调查前提

第 2 章执行摘要

第三章调查方法

第四章 市场概况

- 介绍

- 2028 年市场规模与需求预测

- 最新趋势和发展

- 政府法规和政策

- 市场动态

- 驱动程式

- 限制因素

- 供应链分析

- 波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争强度

第五章 市场区隔

- 依电池类型

- 铅酸电池

- 锂离子电池

- 其他电池类型

- 按最终用户

- 车

- 资料中心

- 通讯

- 能源储存

- 其他最终用户

- 按地区

- 印尼

- 马来西亚

- 菲律宾

- 新加坡

- 泰国

- 越南

- 缅甸

- 其他东南亚地区

第六章 竞争格局

- 併购、合资、合作、协议

- 主要企业策略

- 公司简介

- BYD Co. Ltd.

- C&D Technologies Inc.

- East Penn Manufacturing Co. Inc.

- Tianjin Lishen Battery Joint-Stock Co. Ltd.

- Exide Industries Ltd.

- FIAMM Energy Technology SpA

- GS Yuasa Corporation

- LG Chem Ltd.

- Panasonic Corporation

- Saft Groupe SA

- Samsung SDI Co. Ltd.

- Clarios

- Tesla Inc.

- Leoch International Technology Limited

第七章 市场机会与未来趋势

The Southeast Asia Battery Market size is estimated at USD 3.04 billion in 2025, and is expected to reach USD 4.22 billion by 2030, at a CAGR of 6.77% during the forecast period (2025-2030).

Though COVID-19 negatively impacted the market in 2020, it has reached pre-pandemic levels.

Key Highlights

- Over the medium term, factors such as growing demand from the automotive sector, declining lithium-ion battery prices, and plans to make Southeast Asia a data center hub are expected to drive the market during the forecast period.

- Despite the growing demand for batteries in the automotive, data centers, and telecommunications sectors, the battery energy storage segment is expected to witness stagnant growth, as most countries depend on other energy storage alternatives. This, in turn, is likely to restrain the growth of the battery market in the energy storage segment during the forecast period.

- Moreover, plans to integrate renewable energy with the national grids in respective countries are expected to create significant opportunities for lithium-ion battery manufacturers and suppliers during the forecast period.

- Thailand is expected to dominate the market during the forecast period due to the increasing demand from the automotive, data center, and other end-user sectors.

Southeast Asia Battery Market Trends

Automotive Sector is Expected to Dominate the Market

- Vehicles with internal combustion engines (ICE) were the only types used earlier. ICE vehicles have been using lead-acid batteries, which may continue with no significant replacement available.

- However, nowadays, technology has been shifting toward electric vehicles due to rising concerns about the environment. In EVs, mostly lithium-ion batteries are used, as they provide high energy density, have low self-discharge, and require little maintenance.

- Lithium-ion battery systems propel plug-in hybrid and electric vehicles. Due to their high energy density, fast recharge capability, and high discharge power, lithium-ion batteries are the only available technology that meets the OEM requirements for vehicles' driving range and charging time. Lead-based traction batteries are not competitive for use in full-hybrid electric cars or electric vehicles because of their lower specific energy and higher weight.

- Moreover, the exponential decline in lithium-ion batteries' prices reduced their value by 81.5% from USD 668/kWh in 2013 to USD 123/kWh in 2021. The trend is likely to continue in the future, making EVs affordable to a broader range of economic groups in the region.

- For hybrid vehicles, several battery technologies can provide these functions in different combinations, with nickel-metal hydride and lithium-ion batteries preferred at higher voltages due to their fast recharge capability, good discharge performance, and lifetime endurance.

- Several regional governments developed plans to reduce emissions, which are expected to increase the region's share of electric vehicles (EV) during the forecast period.

- Therefore, owing to the abovementioned factors, the automotive sector is expected to dominate the Southeast Asian battery market during the forecast period.

Thailand is Expected to Dominate the Market

- Thailand accounts for the majority share of the market. This trend is expected to continue during the forecast period, owing to the increasing demand from the automotive, data center, and telecom sectors.

- Thailand provides great investment potential for the automotive sector. The country has a leading automotive production base in the Association of Southeast Asian Nations. The country has developed from an assembler of auto components into a top automotive manufacturing and export hub in over 50 years.

- Moreover, the country is expected to witness high growth in the EV segment, particularly in plug-in hybrid electric vehicles (PHEVs) and hybrid electric vehicles (HEVs). In September 2022, BYD Co. announced plans to build its first overseas electric passenger car plant in Rayong, Bangkok.

- Under the National Electric Vehicle Policy Committee (NEVPC) roadmap, Thailand is expected to add between 100,000 and 300,000 vehicles by 2025 and finally between 400,000 and 750,000 vehicles by 2026.

- Further, in April 2022, the Thai government agreed to fund the manufacturing of zinc-ion batteries to power electric vehicles (EVs). Thailand will develop a local EV battery plant worth using zinc as a natural resource.

- Furthermore, Thailand has made great progress in growing its ICT sector, moving quickly from being a secondary player in the world of technology to one of the regional leaders. Over the past decade, the digital share in Thailand has been closing at an ever-increasing speed, with the country making significant gains in labor force education and skills building.

- The government planned its business module under Thailand's 4.0 Program. This program helps increase the use of new technologies such as cloud computing, interactive media, big data, and the internet of things. Hence, the country is expected to have a high demand for data centers, which is expected to increase the demand for batteries in its data centers during the forecast period.

- Therefore, owing to the abovementioned factors, Thailand is expected to dominate the Southeast Asian battery market during the forecast period.

Southeast Asia Battery Industry Overview

The Southeast Asian battery market is partially fragmented due to the presence of key players, including (in no particular order) Tianjin Lishen Battery Joint-Stock Co. Ltd., FIAMM Energy Technology SpA, BYD Co. Ltd., C&D Technologies Inc., and East Penn Manufacturing Co. Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD billion, till 2028

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.2 Restraints

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Battery Type

- 5.1.1 Lead-acid Battery

- 5.1.2 Lithium-ion Battery

- 5.1.3 Other Battery Types

- 5.2 By End-User

- 5.2.1 Automotive

- 5.2.2 Data Centers

- 5.2.3 Telecommunication

- 5.2.4 Energy Storage

- 5.2.5 Other End-Users

- 5.3 By Geography

- 5.3.1 Indonesia

- 5.3.2 Malaysia

- 5.3.3 Philippines

- 5.3.4 Singapore

- 5.3.5 Thailand

- 5.3.6 Vietnam

- 5.3.7 Myanmar

- 5.3.8 Rest of Southeast Asia

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 BYD Co. Ltd.

- 6.3.2 C&D Technologies Inc.

- 6.3.3 East Penn Manufacturing Co. Inc.

- 6.3.4 Tianjin Lishen Battery Joint-Stock Co. Ltd.

- 6.3.5 Exide Industries Ltd.

- 6.3.6 FIAMM Energy Technology SpA

- 6.3.7 GS Yuasa Corporation

- 6.3.8 LG Chem Ltd.

- 6.3.9 Panasonic Corporation

- 6.3.10 Saft Groupe SA

- 6.3.11 Samsung SDI Co. Ltd.

- 6.3.12 Clarios

- 6.3.13 Tesla Inc.

- 6.3.14 Leoch International Technology Limited

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

电池结构件市场-全球产业规模、份额、趋势、机会与预测(细分、按类型、按应用、按电池类型、按地区、按竞争,2020-2030 年预测)矿山机械电池市场-全球产业规模、份额、趋势、机会及预测(按类型、产能、应用、地区和竞争,2020-2030 年)

电池结构件市场-全球产业规模、份额、趋势、机会与预测(细分、按类型、按应用、按电池类型、按地区、按竞争,2020-2030 年预测)矿山机械电池市场-全球产业规模、份额、趋势、机会及预测(按类型、产能、应用、地区和竞争,2020-2030 年) 亚太钠离子电池(SIB)市场:应用、产品与国家分析与预测(2025-2035)

亚太钠离子电池(SIB)市场:应用、产品与国家分析与预测(2025-2035) 欧洲钠离子电池市场按应用、产品类型、外形规格、系统/电池组级电压和地区分類的分析与预测(2025-2035)

欧洲钠离子电池市场按应用、产品类型、外形规格、系统/电池组级电压和地区分類的分析与预测(2025-2035) 2025年全球盐水电池市场报告2025年钠离子电池全球市场报告

2025年全球盐水电池市场报告2025年钠离子电池全球市场报告 氧化银电池市场类型、电压、容量、电池尺寸、销售管道和应用—2025-2030 年全球预测

氧化银电池市场类型、电压、容量、电池尺寸、销售管道和应用—2025-2030 年全球预测 全球电子设备电池市场

全球电子设备电池市场 全球量子电池市场:2025年至2030年预测

全球量子电池市场:2025年至2030年预测 全球钠离子电池市场:应用、产品与地区的分析与预测(2025-2035)

全球钠离子电池市场:应用、产品与地区的分析与预测(2025-2035)