|

市场调查报告书

商品编码

1689762

包装印刷:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)Packaging Printing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

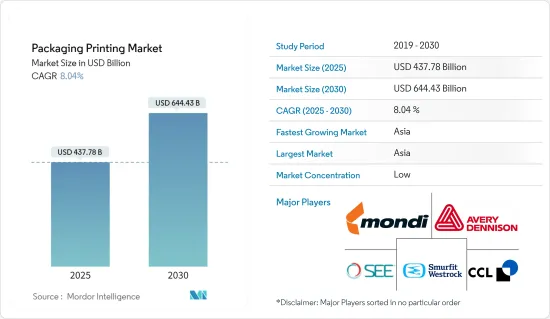

2025 年包装印刷市场规模预估为 4,377.8 亿美元,预计到 2030 年将达到 6,444.3 亿美元,预测期内(2025-2030 年)的复合年增长率为 8.04%。

主要亮点

- 由于对技术先进的包装和创新的包装解决方案的需求,包装印刷市场正在成长。品牌间激烈的竞争和消费者意识的增强推动了这种需求。食品、食品和饮料、化妆品行业等主要终端用户领域对创造性包装的需求日益增长,进一步推动了市场扩张。包装印刷产业正在快速发展,新的印刷技术和材料不断开发以满足不断变化的消费者偏好和永续性要求。

- 数位印刷技术越来越受欢迎,为品牌提供了灵活性和客製化选项。由于线上零售商希望改善客户的拆包体验,电子商务的成长为包装印刷商创造了新的机会。随着企业寻求在实体店和数位市场中使其产品脱颖而出,包装印刷在品牌传播和产品保护中发挥越来越重要的作用。

- 促销和行销印刷的需求不断增长,推动了印表机技术的创新。为了有效回应当前趋势,该公司正在开发新模式,专注于更快、更通用、更具成本效益的印刷解决方案,可以处理各种材料和格式。 2024 年 1 月,惠普公司宣布推出 HP Thermal InkjetTM 108mm 大量列印解决方案,利用 TIJ 4.0 印字头技术的进步。这款新型印表机旨在透过提高列印品质、加快速度和提高耐用性来满足包装行业的需求。此印表机设计用于处理大批量列印,同时保持包装和促销材料所需的精确度和色彩准确度。这些技术进步表明该行业对不断变化的市场需求的适应能力以及印刷品质在品牌表达和产品行销中日益增长的重要性。

- 多年来,包装产业的采用率持续成长。特别是在化妆品包装领域,创新解决方案取得了长足的进步。数位印刷使美容品牌能够创造客製化的 SKU 和限量版产品。品牌使用数位印刷来尝试图像和讯息,利用可以在数位印刷机上轻鬆调整的设计来瞄准不同的消费者群体。该方法已被证明在实施可变策略和进行市场测试方面是有效的。

- 数位印刷技术的快速进步正在改变标籤印刷市场并加速数位印刷标籤的采用。推动数位印刷标籤成长的关键因素是其灵活性、多功能性和高品质的图形输出。同时,柔版印刷方法的独特之处在于它能够在多种基材上进行印刷,包括金属薄膜、塑胶、赛珞玢、纸张和瓦楞表面。

- 柔版印刷可望在标籤印刷领域大幅扩张。最近的技术进步,包括先进的柔版印刷机、连续印刷解决方案、改进的软体整合和增强的耐用性,大大缩短了生产前置作业时间。例如,总部位于荷兰的药品标籤供应商Pharmalabel最近安装了Ink Manager软体和GSE ColorsatSwitch分配系统。这种整合提高了柔版印刷过程的效率和品管。

- 软质包装已成为行业主要供应商关注的核心,为全球差异化、收益成长和提高利润率提供了重大机会。例如,该领域的主要企业Amcor 约 70% 的收益来自软包装。这一高比例凸显了软包装在新兴市场和成熟西方经济体的潜力。

- 人工智慧、RFID 技术和资料分析的进步正在推动包装行业个人化服务的增强。这些技术使公司能够收集和分析消费者资料,从而促进客製化包装设计和体验的创造。数位印刷的整合使得即使是大订单也可以实现卓越的印刷定制,使品牌能够为每件商品生产具有独特设计、可变资料或单独讯息的包装。这种个人化可以提高消费者参与度和品牌忠诚度。然而,实施这些先进封装技术以及大规模生产客製化封装的成本仍然是一个巨大的挑战,因为需要在设备、软体和熟练人力方面进行大量的投资。

包装印刷市场趋势

食品和饮料行业预计将占据主要市场占有率

- 近年来,由于全球食品和饮料消费量的增加,包装产业发生了重大变化。这种演变与消费者偏好的变化、技术进步和对永续性的日益关注密切相关。消费者越来越寻求方便、环保的包装解决方案,以维持食品品质并延长保质期。同时,印刷技术的进步使得包装材料上的设计更加精緻、引人注目。

- 在美国,食品和饮料的年度零售额正在大幅成长,这与全球趋势一致。 2020 年销售额将达 8,500 亿美元,到 2023 年将增至 9,853 亿美元。这一增长不仅反映了人口的增长,也反映了随着包装食品和方便食品的兴起而改变的饮食习惯。电子商务和食品宅配服务的扩张进一步增加了对创新包装解决方案的需求。

- 食品和饮料行业的成长产生了对包装多样化印刷格式的需求,尤其是在行业内部。例如,数位印刷因其能够小批量生产高品质、客製化包装而变得流行。柔版印刷仍然是大规模生产的首选,而凹版印刷则适用于设计精良的高檔包装。出于对环境问题的考虑,该行业也在探索更永续的印刷选择,例如水性和紫外线固化油墨。

- 预计食品和饮料产品需求的增加将推动食品和饮料印刷市场的成长。随着消费者对更多样化和更具视觉吸引力的产品的需求,该领域的公司正在转向创新的包装和印刷解决方案,以区分他们的产品并增强其货架吸引力。作为回应,食品和饮料印刷行业正在适应市场需求,并透过在包装印刷中采用新技术和永续实践来满足这些不断变化的需求。

- 食品和非食品产品种类的日益增加以及对食品和饮料产品的需求不断增长,推动着包装印刷品质的大幅提升。这一趋势是由对标籤和包装的需求所驱动,这些标籤和包装需要能够承受恶劣条件(包括冰冻温度)并保持耐用。标籤的防水印刷已变得至关重要,特别是对于可能暴露在潮湿或冰中的产品,例如瓶装饮料。

- 由于消费者对包装产品的偏好不断提高,食品包装上的印刷需求也日益增加。这一趋势是由饮食习惯的改变和生活方式的演变所驱动,可能会对市场产生重大影响。由于印刷包装具有高阻隔性、延长保质期和消费者安全性等特点,预计人均可支配收入的提高和人口的扩大将推动产品需求。在食品包装材料上印刷既可以传递讯息,又可以达到行销的目的。各种包装材料都可以直接印刷,包括塑胶、纸张、纸板和软木。

- 食品包装产业正在不断发展以满足消费者对透明度和品质的需求。包装上印刷的营养资讯正在提高人们的意识,而对天然、少加工食品的追求正在推动包装设计的创新。食品包装有多种用途:保护、方便、控制份量。永续包装解决方案解决食品废弃物和安全问题。

- 监管机构要求详细的标籤,强调高品质印刷的重要性。例如,印度食品安全和标准局(FSSAI)要求提供有关食品袋的全面资讯。製造商优先采取严格控制措施来保护消费者,并遵守管理食品包装各个方面(包括标籤)的综合法规。对食品包装的透明度、品质和安全性的关注反映了该行业对不断变化的消费者偏好和监管要求的反应。

亚洲可望成为成长最快的市场

- 亚洲包装印刷市场规模庞大,涵盖多个行业的广泛印刷技术和应用。中国、印度、日本和韩国等国家对包装解决方案的需求很高。多个行业正在推动这一需求,包括食品和饮料、家电和其他行业。

- 在中国,电子商务的快速成长刺激了对创新包装解决方案的需求,尤其是瓦楞纸箱和软包装。印度蓬勃发展的中产阶级和不断加快的都市化推动了包装食品和个人保健产品的激增,从而促进了包装印刷行业的发展。日本以其先进的包装技术而闻名,在奢侈品和电子产品的高品质包装印刷领域继续保持领先地位。韩国蓬勃发展的电子产业正在推动对专业包装印刷服务的需求。

- 该地区也正在向永续包装解决方案转变,许多公司采用环保材料和印刷工艺。这一趋势在新加坡和台湾尤为明显,那里的环境问题开始影响消费者的选择和企业政策。

- 有几个因素推动了这项需求。快速的都市化和不断变化的消费者生活方式正在推动对包装商品的需求。这些国家的中阶人口不断成长,推动了包装产品的消费成长。此外,该地区电子商务的成长也加速了对创新和永续包装解决方案的需求。

- 该地区的包装印刷市场正与全球趋势保持同步,尤其是永续和智慧包装技术。主要倡议包括采用生物分解性材料、齐心协力减少塑胶使用量以及整合二维码和无线射频识别标籤以增强可追溯性并提高消费者意识。此外,企业正在投资先进的包装技术来提高包装品质和效率,并且也更加重视使用环保油墨和被覆剂。

- 在印度,包装印刷对食品和饮料、製药、化妆品、电子和汽车行业等多个领域都至关重要。包装上数位资料印刷的应用正在迅速增加,尤其是在食品和饮料领域。这一趋势主要由传达基本细节的需求所驱动,例如最佳食用日期、成分和营养资讯。反映这一成长,印度包装食品市值预计将从 2020 年的 4,377 万美元飙升至 2026 年的 7,021 万美元。包装食品市场的强劲扩张刺激了对各种包装印刷技术的需求增加。

- 不断增长的消费者支出和对耐用品的需求正在推动亚洲包装的进步。加工食品消费量的增加和新的包装印刷技术进一步推动了市场的成长。製药业和便捷包装的需求也是主要贡献者。亚洲对标准产品的需求不断增长,推动了中小型工业的发展,增强了数位印刷包装市场的发展。

- 包装产业对研发的投入推动了全球市场的扩张和印表机的创新。 2024年2月,Canon针对亚太市场宣布推出三款全新IMAGE PROGRAF GP系列印表机(GP-526S/546S/566S),采用环保瓦楞纸箱包装。 GP546S型号减少了89.5%的发泡聚苯乙烯包装,最大限度地减少了废弃物并促进了环境的永续性。

包装印刷业概况

由于 Mondi PLC、Ahlstrom-Munksjo Oyj、Autajon CS、Huhtamaki Flexible Packaging(Huhtamaki Oyj)和 Avery Dennison Corporation 等主要企业的存在,包装印刷市场的竞争格局较为分散。我们不断创新产品的能力使我们比其他公司拥有竞争优势。透过策略伙伴关係、研发和併购,这些公司在市场上占据了更大的份额。

- 2024 年 7 月 - DS Smith 是全球着名的永续纤维包装解决方案提供商,在其位于西班牙 Torrelavit 的工厂安装了 Nozomi 14000 AQ单一途径水性数位喷墨印表机,走在创新的前沿。 Nozomi 14000 AQ 印表机由 Electronics for Imaging 公司开发,能够使用环保的水性油墨进行高解析度列印。这款先进的印表机可以将您的设计直接列印到瓦楞纸板上,消除了平版印刷层压等传统方法带来的浪费。

- 2023 年 9 月,利乐与 Flow Beverage Corp. 建立了第一个自订印刷伙伴关係。此举是在利乐的客自订印刷解决方案在超过 1 亿个包装上成功检验之后采取的。新的解决方案旨在透过为消费者提供灵活性和个人化选项来扩大商业和行销机会。

- 2023 年 6 月,Constantia Flexibles 宣布完成对波兰包装公司 Drukpol Flexo 的收购。 Drukpol Flexo 是食品、家居、个人护理和医药 (HPP) 市场的包装解决方案提供商,其印刷和转换能力受到本地和国际客户的一致好评。

- 2023 年 4 月 Sealed Air 与 Koenig & Bauer 签署了一份不具约束力的意向书,以扩大他们在数位印刷机领域的策略伙伴关係。此次合作旨在透过利用先进的数位印刷技术、设备和服务来提高包装设计能力。 SEE 和 Koenig & Bauer 的创新加速了数位印刷材料的交货,并使品牌所有者能够透过更有效的包装吸引消费者。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买家的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争强度

- 产业生态系统分析

第五章 市场动态

- 市场驱动因素

- RFID 和数位印刷需求

- 数位印刷和永续包装印刷的需求不断增加

- 市场限制

- 高资本投入

- 包装印刷法规

第六章 市场细分

- 依印刷技术

- 平张胶印

- 凹版印刷

- 柔版印刷

- 数位印刷

- 网版印刷

- 按油墨类型

- 溶剂型墨水

- UV 固化墨水

- 水性油墨

- 按包装类型

- 标籤

- 塑胶

- 玻璃

- 金属

- 纸和纸板

- 按应用

- 化妆品和家居护理

- 饮食

- 药品

- 其他用途

- 按地区

- 北美洲

- 美国

- 加拿大

- 欧洲

- 英国

- 法国

- 德国

- 亚洲

- 中国

- 日本

- 印度

- 澳洲和纽西兰

- 拉丁美洲

- 巴西

- 墨西哥

- 哥伦比亚

- 中东和非洲

- 阿拉伯聯合大公国

- 南非

- 沙乌地阿拉伯

- 北美洲

第七章 竞争格局

- 公司简介

- Mondi PLC

- Ahlstrom-Munksjo Oyj

- Autajon CS

- Huhtamaki Oyj

- Avery Dennison Corporation

- CCL Industries Inc.

- Clondalkin Group Holdings BV

- Constantia Flexibles Group GmbH

- Tetra Pak

- Smurfit WestRock

- DS Smith PLC

- Georgia-Pacific LLC

- International Paper Company

- Sealed Air Corporation

- Stora Enso Oyj

- Sonoco Products Company

- Mayr-Melnhof Karton AG

- Trustpack UAB

- Duncan Printing Group

第八章投资分析

第九章:市场的未来

The Packaging Printing Market size is estimated at USD 437.78 billion in 2025, and is expected to reach USD 644.43 billion by 2030, at a CAGR of 8.04% during the forecast period (2025-2030).

Key Highlights

- The Packaging Printing Market is experiencing growth driven by technological advancements and the demand for innovative packaging solutions. This demand is fueled by intense competition among brands and increased consumer awareness. The growing need for creative packaging in crucial end-user segments, including the food, beverage, and cosmetics industries, further supports the market expansion. The packaging printing industry is rapidly evolving, with new printing techniques and materials being developed to meet changing consumer preferences and sustainability requirements.

- Digital printing technologies are gaining prominence, providing enhanced flexibility and customization options for brands. The growth of e-commerce has created new opportunities for packaging printers, as online retailers aim to improve customers' unboxing experience. As companies seek to differentiate their products in physical stores and digital marketplaces, packaging printing plays an increasingly vital role in brand communication and product protection.

- The growing demand for promotional and marketing printing is driving innovation in printer technology. Companies are developing new models to address current trends efficiently, focusing on faster, more versatile, cost-effective printing solutions capable of handling diverse materials and formats. In January 2024, HP Inc. introduced its HP Thermal InkjetTM 108mm bulk printing solution, leveraging advancements in TIJ 4.0 printhead technology. This new printer model aims to meet the packaging industry's requirements by offering enhanced print quality, increased speed, and improved durability. It is designed for high-volume printing tasks and maintains precision and color accuracy, essential for packaging and promotional materials. These technological advancements demonstrate the industry's adaptation to evolving market demands and the increasing significance of print quality in brand representation and product marketing.

- The packaging industry has been experiencing consistent year-on-year growth in adoption. The cosmetics packaging sector, in particular, has made significant advancements in innovative solutions. Digital printing has enabled beauty brands to create customized SKUs and exclusive limited-edition products. Brands are using digital printing to experiment with imagery and messaging, targeting various consumer segments with easily adjustable designs on digital presses. This method has proven effective for implementing variable strategies and conducting market tests.

- The swift advancement of digital print technology has transformed the label printing market and accelerated the adoption of digital print labels. Key factors propelling the growth of digital print labels include their flexibility, versatility, and high-quality graphic output. Concurrently, the flexographic method distinguishes itself through its ability to print on a wide array of materials, such as metallic films, plastics, cellophane, paper, and corrugated surfaces.

- Flexographic printing is set for significant expansion in the label printing sector. Recent technological advancements, including sophisticated flexographic printers, continuous printing solutions, improved software integrations, and enhanced durability, have markedly reduced production lead times. For instance, Pharmalabel, a Netherlands-based pharmaceutical label supplier, recently implemented a GSE ColorsatSwitch dispensing system with ink manager software. This integration has boosted both efficiency and quality control in its flexographic printing processes.

- Flexible packaging has become a central focus for major vendors in the industry, offering significant opportunities for differentiation, revenue growth, and profit enhancement globally. For example, Amcor, a leading company in the sector, derives approximately 70% of its revenue from flexible packaging. This high percentage highlights the potential of flexible packaging in both emerging markets and established Western economies.

- Artificial intelligence, RFID technology, and data analytics advancements have enhanced personalized offerings in the packaging industry. These technologies enable companies to gather and analyze consumer data, facilitating the creation of tailored packaging designs and experiences. Digital printing integration allows for superior print customization in large-volume orders, enabling brands to produce packaging with unique designs, variable data, or individualized messages for each item. This personalization can increase consumer engagement and brand loyalty. However, the cost factor remains a significant challenge, as implementing these advanced technologies and producing customized packaging at scale requires substantial investment in equipment, software, and skilled personnel.

Packaging Printing Market Trends

Food and Beverage Sector is Expected to Hold Significant Market Share

- The packaging industry has undergone substantial changes in recent years, driven by the global increase in food and beverage consumption. This evolution is closely tied to shifting consumer preferences, technological progress, and growing sustainability concerns. Consumers increasingly demand convenient, eco-friendly packaging solutions that preserve food quality and extend shelf life. Simultaneously, advancements in printing technologies have enabled more sophisticated and eye-catching designs on packaging materials.

- In the United States, annual retail food and drink sales have risen significantly, mirroring global trends. Sales reached USD 850 billion in 2020 and increased to USD 985.30 billion in 2023. This growth reflects not only population increases but also changes in eating habits, with a rise in packaged and convenience foods. The expansion of e-commerce and food delivery services has further fueled the demand for innovative packaging solutions.

- This growth in the food and beverage sector has created a demand for diverse printing formats in packaging, particularly within the industry. Digital printing, for instance, has gained popularity due to its ability to produce high-quality, customized packaging in smaller quantities. Flexographic printing remains a staple for large-scale production, while gravure printing is favored for premium packaging with intricate designs. The industry also explores sustainable printing options, such as water-based and UV-curable inks to align with environmental concerns.

- The increasing demand for food and beverage products is expected to drive growth in the food and beverage printing market. As consumers seek more diverse and visually appealing products, companies in this sector are increasingly utilizing innovative packaging and printing solutions to differentiate their offerings and enhance shelf appeal. In response, the printing industry within the food and beverage sector is adapting to meet these evolving needs by incorporating new technologies and sustainable practices in packaging printing, aligning with market demands.

- The growing variety of food and non-food products and increased demand for food and beverages has led to a significant trend in quality printing for packaging. This trend is driven by the need for labels and packaging that can withstand extreme conditions, such as freezing temperatures, and maintain durability. Water-resistant printing for labels has become essential, particularly for products like bottled beverages that may be exposed to moisture or ice.

- The demand for printing in food packaging is increasing due to rising consumer preferences for packaged products. This trend is driven by changing eating habits and evolving lifestyles, which may significantly impact the market. The growth in per capita disposable income and expanding population are expected to boost product demand, owing to the high barrier properties, extended shelf life, and consumer safety offered by printed packaging. Printing on food packaging materials serves both informational and marketing purposes. Various packaging materials, including plastics, paper, cardboard, and cork, can be directly printed.

- The food packaging industry is evolving to meet consumer demands for transparency and quality. Nutritional information printed on packaging enhances awareness, while the trend toward natural, minimally processed foods drives innovation in packaging design. Food packaging serves multiple purposes, including protection, convenience, and portion control. Sustainable packaging solutions address food waste and safety concerns.

- Regulatory bodies mandate detailed labeling, emphasizing the importance of high-quality printing. For instance, the Food Safety and Standards Authority of India (FSSAI) requires comprehensive information on food pouches. Manufacturers prioritize strict controls to protect consumers, adhering to comprehensive legislation governing all aspects of food packaging, including labels. This focus on transparency, quality, and safety in food packaging reflects the industry's response to changing consumer preferences and regulatory requirements.

Asia is Expected to be the Fastest-growing Market

- The packaging printing market in Asia is substantial, incorporating various printing technologies and applications across multiple industries. Countries like China, India, Japan, and South Korea have experienced significant demand for packaging solutions. Multiple sectors drive this demand, including food and beverages, consumer electronics, and other industries.

- In China, the rapid growth of e-commerce has fueled the need for innovative packaging solutions, particularly in corrugated boxes and flexible packaging. India's burgeoning middle class and increasing urbanization have led to a surge in packaged food and personal care products, boosting the packaging printing sector. Japan, known for its advanced technology, continues to lead in high-quality packaging printing for premium products and electronics. South Korea's robust electronics industry drives demand for specialized packaging printing services.

- The region has also shifted toward sustainable packaging solutions, with many companies adopting eco-friendly materials and printing processes. This trend is particularly evident in Singapore and Taiwan, where environmental concerns increasingly influence consumer choices and corporate policies.

- Multiple factors drive this demand. Rapid urbanization and evolving consumer lifestyles have increased the need for packaged goods. The expanding middle-class population in these countries has contributed to higher consumption of packaged products. Furthermore, the growth of e-commerce in the region has accelerated the demand for innovative and sustainable packaging solutions.

- The packaging printing market in the region is aligning with global trends, notably in sustainable and intelligent packaging technologies. Key initiatives include adopting biodegradable materials, a concerted effort to reduce plastic usage, and integrating QR codes and RFID tags to enhance traceability and boost consumer engagement. Additionally, companies are investing in advanced printing techniques to improve packaging quality and efficiency, and there is a growing focus on using eco-friendly inks and coatings.

- Packaging printing is pivotal in India across multiple sectors, including food and beverage, pharmaceuticals, cosmetics, electronics, and the automobile industry. Notably, the food and beverage sector has seen a surge in adopting digital data printing on packages. This trend is primarily driven by the need to communicate essential details like shelf-life, ingredients, and nutritional information. Reflecting this growth, the market value of packaged food in India jumped from USD 43.77 million in 2020 and is projected to reach USD 70.21 million by 2026. Such robust expansion in the packed food market is fueling rising demand for varied printing techniques in packaging.

- Rising consumer spending and demand for durable goods drive packaging advancements in Asia. They increased processed food consumption and emerging packaging printing technologies further fuel market growth. The pharmaceutical sector and demand for convenient packaging also contribute significantly. The rise in demand for standard products in Asia boosts small and medium-scale industries, enhancing the digital printing packaging market.

- Investments in packaging industry R&D drive global market expansion and printer innovation. In February 2024, Canon introduced three new images PROGRAF GP Series printers (GP-526S/546S/566S) for the Asia-Pacific market, packaged in eco-friendly cardboard boxes. The GP546S model reduced polystyrene foam packaging by 89.5%, minimizing waste and promoting environmental sustainability.

Packaging Printing Industry Overview

The competitive rivalry in the packaging printing market is fragmented owing to the presence of some key players, such as Mondi PLC, Ahlstrom-Munksjo Oyj, Autajon CS, Huhtamaki Flexible Packaging (Huhtamaki Oyj), and Avery Dennison Corporation, among others. Their ability to continually innovate their offerings has allowed them to gain a competitive advantage over others. Through strategic partnerships, R&D, and mergers and acquisitions, the players have achieved a more significant footprint in the market.

- July 2024: DS Smith, a prominent global provider of sustainable fiber-based packaging solutions, spearheads innovation by installing a Nozomi 14000 AQ single-pass, water-based digital inkjet printer at its Torrelavit facility in Spain. Developed by Electronics for Imaging, the Nozomi 14000 AQ printer offers high-resolution printing using eco-friendly water-based ink. This advanced printer applies designs directly onto corrugated cardboard, eliminating the waste typically associated with traditional methods like lithographic lamination.

- September 2023: Tetra Pak has launched its first Custom Printing partnership with Flow Beverage Corp. This initiative follows the successful validation of Tetra Pak's Custom Printing solution, which has been applied to over 100 million packages. The new offering aims to expand business and marketing opportunities by providing consumers with increased flexibility and personalization options.

- June 2023: Constantia Flexibles has announced the completion of its acquisition of Drukpol Flexo, an established packaging company in Poland. Drukpol Flexo, a packaging solutions provider for food and household, personal care, and pharmaceutical (HPP) markets, has built a reputation among local and international customers for its printing and converting capabilities.

- April 2023: Sealed Air and Koenig & Bauer AG have signed a non-binding letter of intent to broaden their strategic alliance in digital printing machines. This collaboration seeks to elevate packaging design capabilities by pioneering advanced digital printing technologies, equipment, and services. The innovations from SEE and Koenig & Bauer promise to expedite the delivery of digitally printed materials, allowing brand owners to engage consumers more effectively through enhanced packaging.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definitions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHT

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Ecosystem Analysis

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Demand for the Use of RFIDs and Digital Printing

- 5.1.2 Growing Demand for Digital and Sustainable Packaging Printing

- 5.2 Market Restraints

- 5.2.1 High Capital Investments

- 5.2.2 Packaging and Printing Regulations

6 MARKET SEGMENTATION

- 6.1 By Printing Technology

- 6.1.1 Offset Lithography

- 6.1.2 Rotogravure

- 6.1.3 Flexography

- 6.1.4 Digital Printing

- 6.1.5 Screen Printing

- 6.2 By Ink Type

- 6.2.1 Solvent-based Ink

- 6.2.2 UV-curable Ink

- 6.2.3 Aqueous Ink

- 6.3 By Packaging Type

- 6.3.1 Label

- 6.3.2 Plastic

- 6.3.3 Glass

- 6.3.4 Metal

- 6.3.5 Paper and Paperboard

- 6.4 By Application

- 6.4.1 Cosmetic and Homecare

- 6.4.2 Food and Beverage

- 6.4.3 Pharmaceutical

- 6.4.4 Other Applications

- 6.5 By Geography

- 6.5.1 North America

- 6.5.1.1 United States

- 6.5.1.2 Canada

- 6.5.2 Europe

- 6.5.2.1 United kingdom

- 6.5.2.2 France

- 6.5.2.3 Germany

- 6.5.3 Asia

- 6.5.3.1 China

- 6.5.3.2 Japan

- 6.5.3.3 India

- 6.5.3.4 Australia and New Zealand

- 6.5.4 Latin America

- 6.5.4.1 Brazil

- 6.5.4.2 Mexico

- 6.5.4.3 Columbia

- 6.5.5 Middle East and Africa

- 6.5.5.1 United Arab Emirates

- 6.5.5.2 South Africa

- 6.5.5.3 Saudi Arabia

- 6.5.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Mondi PLC

- 7.1.2 Ahlstrom-Munksjo Oyj

- 7.1.3 Autajon CS

- 7.1.4 Huhtamaki Oyj

- 7.1.5 Avery Dennison Corporation

- 7.1.6 CCL Industries Inc.

- 7.1.7 Clondalkin Group Holdings BV

- 7.1.8 Constantia Flexibles Group GmbH

- 7.1.9 Tetra Pak

- 7.1.10 Smurfit WestRock

- 7.1.11 DS Smith PLC

- 7.1.12 Georgia-Pacific LLC

- 7.1.13 International Paper Company

- 7.1.14 Sealed Air Corporation

- 7.1.15 Stora Enso Oyj

- 7.1.16 Sonoco Products Company

- 7.1.17 Mayr-Melnhof Karton AG

- 7.1.18 Trustpack UAB

- 7.1.19 Duncan Printing Group

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

包装印刷市场规模、份额及成长分析(按包装类型、印刷技术、印刷油墨、应用和地区划分)-2026-2033年产业预测

包装印刷市场规模、份额及成长分析(按包装类型、印刷技术、印刷油墨、应用和地区划分)-2026-2033年产业预测 包装油墨和涂料市场规模、份额和成长分析(按类型、技术、应用和地区划分)-2026-2033年产业预测

包装油墨和涂料市场规模、份额和成长分析(按类型、技术、应用和地区划分)-2026-2033年产业预测 包装印刷市场规模、占有率、成长及全球产业分析:按类型、应用和地区划分的洞察与预测(2024-2032 年)3D列印包装市场规模、占有率、成长及全球产业分析:按类型、应用和地区划分的洞察与预测(2024-2032)

包装印刷市场规模、占有率、成长及全球产业分析:按类型、应用和地区划分的洞察与预测(2024-2032 年)3D列印包装市场规模、占有率、成长及全球产业分析:按类型、应用和地区划分的洞察与预测(2024-2032) 包装印刷市场(按基材类型、包装类型、印刷类型和最终用途划分)—全球预测,2025-2032 年

包装印刷市场(按基材类型、包装类型、印刷类型和最终用途划分)—全球预测,2025-2032 年 2025年全球包装印刷市场报告

2025年全球包装印刷市场报告 硬质塑胶包装油墨和涂料市场-全球产业规模、份额、趋势、机会和预测(按产品类型、最终用户、地区和竞争细分,2020-2030 年)

硬质塑胶包装油墨和涂料市场-全球产业规模、份额、趋势、机会和预测(按产品类型、最终用户、地区和竞争细分,2020-2030 年) 2025-2029年全球包装油墨和被覆剂市场2025年全球包装油墨和被覆剂市场报告全球包装印刷市场研究报告-产业分析、规模、份额、成长、趋势与预测 2025 年至 2033 年

2025-2029年全球包装油墨和被覆剂市场2025年全球包装油墨和被覆剂市场报告全球包装印刷市场研究报告-产业分析、规模、份额、成长、趋势与预测 2025 年至 2033 年