|

市场调查报告书

商品编码

1689828

生物基聚丙烯:市场占有率分析、产业趋势与成长预测(2025-2030)Bio-based Polypropylene - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

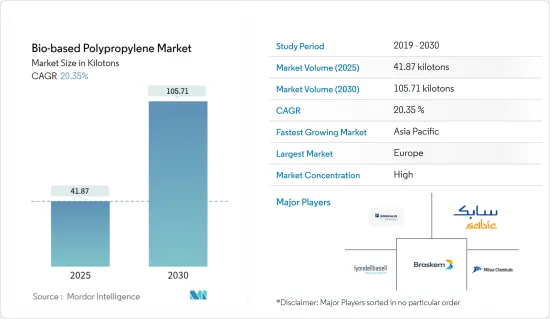

预计 2025 年生物基聚丙烯市场规模为 41.87 千吨,2030 年将达到 105.71 千吨,预测期间(2025-2030 年)的复合年增长率为 20.35%。

由于原料短缺和需求减少,COVID-19 的影响是负面的。不过,疫情过后纺织业的激增推动了生物基聚丙烯的消费。

关键亮点

- 推动市场发展的关键因素是人们对使用传统塑胶的环境问题的日益关注,以及以可再生材料取代化石原料的动力日益增强。

- 另一方面,生物基原材料的高成本阻碍了市场成长。

- 政府加强激励力以促进生物基材料的使用,预计将为市场提供新的机会。

- 由于德国和法国的需求激增,预计欧洲将主导市场。

生物基聚丙烯的市场趋势

射出成型应用需求不断成长

- 生物基聚丙烯因其高熔点、优异的疲劳性能、耐热性、耐化学性和环保性而被用于包装、汽车、电子和医疗行业的各种射出成型应用。

- 生物基聚丙烯的需求正在稳步增长,用于包装应用,包括有特殊要求的产品,如有机食品、奢侈品和品牌产品。

- 此外,在与技术创新、资源效率和气候变迁相关的各种政策的推动下,世界各国政府都在推广生质塑胶包装。

- 最近的一项消费者调查发现,永续性是全球 60% 消费者的宝贵购买标准,而美国的排名略高于全球平均水平,为 61%。

- 此外,中国深度参与塑胶的大规模生产,并从贸易出口中获得收入。这为各包装公司提供了庞大的生产能力。根据ITC统计,2021年中国塑胶及模塑製品出口额约1,310.7亿美元,较前一年(2020年)的约963.8亿美元成长36%。

- 预计2021年全球生质塑胶产能将成长16%,达到240万吨。 2021年生物分解性生质塑胶的总产能将达160万吨。

- 根据米德尔哈尼斯射出成型专家 SFA Packaging 介绍,大多数食品都采用聚丙烯射出成型包装。

- 出于对环境问题的考虑,越来越多的消费者和製造商青睐环保包装,推动了生物基聚丙烯市场的需求。

欧洲主导市场

- 欧洲是生物基聚丙烯产业的重要基地,占约50%的市场占有率。欧洲在该产业的研发水准位居世界前列。

- 大多数欧洲国家对可分解塑胶(包括生物基聚丙烯)的使用有严格的政府规定。政府正在不断提倡使用环保产品。

- 生物基聚丙烯主要用于包装产业。欧洲是包装产业的主要消费国之一,推动各个包装领域的发展。

- 德国是欧洲最大的塑胶消费国。包装产业中塑胶的使用量不断增加,推动了塑胶的需求。 2021年,德国包装产业的收益为296亿欧元(345.5亿美元)。这一数字较前一年的 263 亿欧元(307 亿美元)有所下降。

- 此外,德国政府正在推广包装产业使用生物基和再生材料。例如,德国联邦参议院核准了一项新的包装方法,以促进包装废弃物的回收。这对生质塑胶产业来说是一个重要的讯号,因为生物基材料和再生材料首次被认为是使包装更加永续并减少对有限化石资源的依赖的同等可行的解决方案。

- 此外,电子商务领域的普及和不断增长的零售市场为该地区的生物基聚丙烯市场提供了巨大的成长机会。

- 2021 年,德国 B2C 电子商务领域的销售额约为 867 亿欧元(1,010 亿美元)。自新冠肺炎疫情在全球蔓延以来,网路购物呈现成长态势。在电子商务领域,德国在2021年排名第六,落后中国、美国、英国、日本和韩国。尤其是行动商务正变得越来越重要。目前,全球有72.6亿人使用智慧型手机,预计2026年这数字将达到75亿人。

- 预计这些因素将在未来几年推动欧洲生物基聚丙烯市场的发展。

生物基聚丙烯产业概况

生物基聚丙烯市场部分整合,大型企业占相当大的份额。参与市场的公司(不分先后顺序)包括北欧化工公司、巴西石化公司、三井化学公司、沙乌地基础工业公司和利安德巴塞尔工业控股公司。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 调查前提条件

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场动态

- 驱动程式

- 人们对使用传统塑胶的环境问题的担忧日益加剧

- 越来越多用可再生原料取代化石原料

- 限制因素

- 生物基原料高成本

- 其他限制因素

- 产业价值链分析

- 波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章市场区隔

- 应用

- 射出成型

- 纺织品

- 电影

- 其他的

- 地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 其他欧洲国家

- 其他的

- 亚太地区

第六章 竞争格局

- 併购、合资、合作与协议

- 市场占有率(%)**/排名分析

- 主要企业策略

- 公司简介

- Biobent Management Services Inc.

- Borealis AG

- Borouge

- Braskem

- FKuR

- INEOS

- INTER Ikea SYSTEMS BV

- LyondellBasell Industries Holdings BV

- Mitsui Chemicals Inc.

- SABIC

第七章 市场机会与未来趋势

- 增加政府奖励措施以促进生物基材料的使用

- 其他机会

The Bio-based Polypropylene Market size is estimated at 41.87 kilotons in 2025, and is expected to reach 105.71 kilotons by 2030, at a CAGR of 20.35% during the forecast period (2025-2030).

The impact of COVID-19 was negative due to the raw materials shortage and declined demand for the product. However, an upsurge in the textile industry propelled bio-based polypropylene consumption after the pandemic.

Key Highlights

- The major factors driving the market are the rising environmental concerns regarding using conventional plastics and the increasing replacement of fossil-based feedstock with renewable materials.

- On the flip side, the high cost of bio-based materials is hindering the market's growth.

- Increasing incentives by the government promoting bio-based materials use is expected to provide new opportunities for the market.

- Europe is estimated to dominate the market studied owing to the surging demand in Germany and France.

Bio-based Polypropylene Market Trends

Growing Demand from Injection Molding Application

- Due to its high melting point, good fatigue properties, heat and chemical resistivity, and eco-friendly nature, bio-based polypropylene is used in various injection molding applications in packaging, automotive, electronics, and medical industries.

- The demand for bio-based polypropylene in packaging applications, such as wrapping organic food and premium and branded products with particular requirements, is rising steadily.

- Moreover, governments worldwide are promoting bioplastic packaging in the context of various policies for innovation, resource efficiency, and climate change.

- According to a recent consumer study, sustainability is a valuable purchase criterion for 60% of consumers globally, with the US boasting a percentage a little above the global average at 61%.

- Furthermore, China is significantly involved in producing high amounts of plastics, generating revenues from trade exports. It is, thereby, creating significant production capacities for various packaging companies. According to ITC, in 2021, China exported plastics and articles valued at about USD 131.07 billion, a 36% rise in exports from the previous year (2020), valued at around USD 96.38 billion.

- The global production capacity of bioplastics increased by 16% in 2021 to 2.4 million metric tons. Biodegradable bioplastics accounted for 1.6 million metric tons of the total capacity in 2021.

- According to the injection mold specialist SFA Packaging from Middelharnis, most foods come in injection mold packaging made of polypropylene.

- Due to environmental concerns, more consumers and manufacturers are preferring eco-friendly packaging options, boosting the demand for the bio-based polypropylene market.

Europe to Dominate the Market

- Europe is a significant hub for the bio-based polypropylene industry, with about 50% of the market share. It ranks high in R&D in this industry.

- Government regulations in most European countries regarding using bio-degradable plastics, including bio-based polypropylene, are stringent. The government is continuously pushing the usage of eco-friendly products.

- Bio-based polypropylenes are majorly used in the packaging industry. Europe is one of the leading consumers in the packaging industry and is developing various packaging segments.

- Germany is the largest plastic consumer in Europe. The increasing plastic usage in the packaging industry propelled the plastic demand. In 2021, the packaging industry in Germany generated EUR 29.6 billion (USD 34.55 billion) in revenue. It decreased compared to the previous year to EUR 26.3 billion (USD 30.70 billion).

- Moreover, the German government is promoting bio-based and recycled materials used in the packaging industry. For instance, Germany's Bundesrat, the upper house of parliament, approved a new packaging law to boost the recycling of packaging waste. It is an important signal for the bioplastics industry as, for the first time, bio-based and recycled materials are recognized as equally viable solutions to make packaging more sustainable and reduce our dependency on finite fossil resources.

- Additionally, the popularity of the e-commerce segment and the growing retail market gave a vast growth opportunity to the bio-based polypropylene market in the region through the years.

- In 2021, the B2C e-commerce sector in Germany generated around EUR 86.7 billion (USD 101 billion). Online shopping is on the rise after COVID-19 spread across the globe. In the e-commerce sector, Germany was in sixth place after China, the United States, Great Britain, Japan, and South Korea, in 2021. In particular, mobile commerce is becoming increasingly important. Currently, 7.26 billion people use smartphones, and this is estimated to reach 7.5 billion by 2026.

- The abovementioned factors are expected to drive the market for bio-based polypropylene in Europe in the coming years.

Bio-based Polypropylene Industry Overview

The bio-based polypropylene market is partially consolidated, with the major players dominating a significant portion. Some companies operating in the market (in no particular order) are Borealis AG, Braskem, Mitsui Chemicals Inc., SABIC, and LyondellBasell Industries Holdings BV.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Rising Environmental Concerns Regarding the Usage of Conventional Plastics

- 4.1.2 Increasing Replacement of Fossil-based Feedstock with Renewable Materials

- 4.2 Restraints

- 4.2.1 High Cost of Bio-based Materials

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Application

- 5.1.1 Injection Molding

- 5.1.2 Textiles

- 5.1.3 Films

- 5.1.4 Other Applications

- 5.2 Geography

- 5.2.1 Asia-Pacific

- 5.2.1.1 China

- 5.2.1.2 India

- 5.2.1.3 Japan

- 5.2.1.4 South Korea

- 5.2.1.5 Rest of Asia-Pacific

- 5.2.2 North America

- 5.2.2.1 United States

- 5.2.2.2 Canada

- 5.2.2.3 Mexico

- 5.2.3 Europe

- 5.2.3.1 Germany

- 5.2.3.2 United Kingdom

- 5.2.3.3 France

- 5.2.3.4 Italy

- 5.2.3.5 Rest of Europe

- 5.2.4 Rest of the World

- 5.2.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share(%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Biobent Management Services Inc.

- 6.4.2 Borealis AG

- 6.4.3 Borouge

- 6.4.4 Braskem

- 6.4.5 FKuR

- 6.4.6 INEOS

- 6.4.7 INTER Ikea SYSTEMS BV

- 6.4.8 LyondellBasell Industries Holdings BV

- 6.4.9 Mitsui Chemicals Inc.

- 6.4.10 SABIC

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Incentives by the Government Promoting the Usage of Bio-based Materials

- 7.2 Other Opportunities

生物基聚丙烯医疗设备市场-全球产业规模、份额、趋势、机会和预测:按应用、地区和竞争格局划分,2021-2031年

生物基聚丙烯医疗设备市场-全球产业规模、份额、趋势、机会和预测:按应用、地区和竞争格局划分,2021-2031年 聚四亚甲基醚二醇市场:市场机会、成长驱动因素、产业趋势分析及预测(2026-2035)

聚四亚甲基醚二醇市场:市场机会、成长驱动因素、产业趋势分析及预测(2026-2035) 生物基聚丙烯市场规模、份额和趋势分析报告:按应用、地区和细分市场预测(2026-2033 年)

生物基聚丙烯市场规模、份额和趋势分析报告:按应用、地区和细分市场预测(2026-2033 年) 生物基聚丙烯市场规模、份额和成长分析(按原料、製造流程、挤出类型、应用和地区划分)-2026-2033年产业预测

生物基聚丙烯市场规模、份额和成长分析(按原料、製造流程、挤出类型、应用和地区划分)-2026-2033年产业预测 全球医疗设备生物基聚丙烯市场全球合成与生物基聚丙烯市场

全球医疗设备生物基聚丙烯市场全球合成与生物基聚丙烯市场 聚四亚甲基醚二醇市场评估:各用途,各终端用户产业,各地区,机会及预测,2018~2032年

聚四亚甲基醚二醇市场评估:各用途,各终端用户产业,各地区,机会及预测,2018~2032年 生物基聚丙烯市场按来源、应用、最终用途产业和地区划分 - 预测至 2029 年

生物基聚丙烯市场按来源、应用、最终用途产业和地区划分 - 预测至 2029 年 聚四亚甲基醚二醇 (PTMEG):市场占有率分析、产业趋势与统计、2025-2030 年成长预测

聚四亚甲基醚二醇 (PTMEG):市场占有率分析、产业趋势与统计、2025-2030 年成长预测 医疗设备生物为基础聚丙烯的全球市场:市场规模·占有率·趋势,产业分析 (各用途·各终端用户·材料类别·各生产方法·各变性方法·各地区),未来预测 (2025年~2034年)

医疗设备生物为基础聚丙烯的全球市场:市场规模·占有率·趋势,产业分析 (各用途·各终端用户·材料类别·各生产方法·各变性方法·各地区),未来预测 (2025年~2034年)