|

市场调查报告书

商品编码

1689924

复合半导体:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Compound Semiconductor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

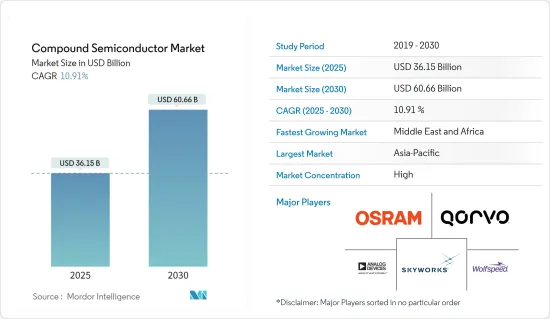

复合半导体市场规模预计在 2025 年为 361.5 亿美元,预计到 2030 年将达到 606.6 亿美元,预测期内(2025-2030 年)的复合年增长率为 10.91%。

新冠疫情导致化合物半导体製造业多种产品停产。此外,世界各地政府的封锁进一步沉重打击了各行各业,扰乱了全球的供应链和製造业运作。包括工厂作业在内的大多数製造业务都受到严重影响,导致生产率下降。

主要亮点

- 复合半导体由元素週期表中不同或相同族的两种或多种元素所构成。化合物半导体采用多种沉积技术製造,包括化学气相沉积和原子层沉积。具有耐高温和耐热性、提高的频率、对磁的高灵敏度、高速运转和光电特性等独特性能是推动需求的一些主要优势。此外,随着化合物半导体製造成本的下降,其在电子和行动装置中的应用正在扩大。

- 化合物半导体能够以通用照明(LED)、雷射和光纤接收器的形式发射和感应光,这进一步推动了需求。随着LED製造和安装成本的下降,其在照明灯具中的应用正在各个领域不断扩大。随着特大城市专注于投资基础设施以满足不断增长的人口的需求,政府正在帮助客户安装节能照明设备以降低电力消耗成本。

- 例如,在疫情期间,EESL(能源效率服务有限公司)庆祝了为期一年的政府计划「Unnat Jyoti 计画(UJALA)」的完成。该专案以LED照明取代了1060多万盏路灯,减少了2000万吨的碳排放和电费。这些倡议将进一步促进市场发展。

- 2020年,台积电约31%的零件来自中国大陆,2021年这一比例将上升至31%。

- 根据美国能源局(DOE)的数据,LED照明比传统白炽灯泡消费量约75-80%,比卤素灯泡节能约65%。商业建筑需要长时间照明,例如长时间工作、仓库和製造设施的安全保障以及其他用途。因此,改用 LED 照明每年可节省数百万美元。例如,美国能源回收公司(美国 能源回收) 的客户可以透过以现代 LED 照明取代旧照明系统来节省约 20-55% 的水电费。因此,向 LED 的采用转变正在推动市场成长。

- 智慧型手机是化合物半导体的主要消费者。近年来,智慧型手机市场竞争愈发激烈。预计行动电话使用量的增加将进一步推动全球市场的发展。例如,根据爱立信2022年行动报告,预计到2027年底全球5G用户将达到44亿,占所有行动电话用户的48%。

- 物联网应用正在兴起,预计将推动复合半导体的销售。此外,随着5G网路的发展,无线通讯领域也有望实现成长。随着消费者升级手机和设备,5G 网路也显示出良好的前景,刺激了全球对复合半导体的采用。

- 化合物半导体产业被认为是最复杂的产业之一,因为它面临的环境充满挑战,包括动荡的电子市场和不可预测的需求,以及製造和各种产品涉及的 500 多个製程步骤。

复合半导体市场趋势

预测期内光电子技术将显着成长

- 调查涵盖的光电子产品包括光电二极体、光电电晶体、频谱仪、太阳能板和其他光电子元件,但不包括LED产品。

- 基于 GaN 的电晶体正在开闢新的可能性,特别是在光电子领域,因为它们比基于 SiC 的电晶体更快、更有效率。 GaN的电子迁移率是硅的1000倍,即使在高温下也能相对稳定地运作。

- 光电子领域的最新进展,例如等离子体奈米结构、钙钛矿晶体管、光学活性量子点、微灯泡、低成本 3D 成像、雷射驱动 3D 显示技术和雷射 Li-Fi,有望带来光电子元件动态应用的量子转变。

- 此外,2022年6月,美国(中佛罗里达大学)和韩国的研究人员开发了一种多波长光电子突触,可在同一装置中侦测、储存和处理光学资料。由此产生的 InSensor 人工视觉系统显着提高了处理效率和影像辨识准确性,可用于机器人、自动驾驶汽车、机器视觉等领域。就像人眼中视网膜透过视神经中的突触传输光学资料一样,光电突触使得在同一装置中整合光学资料感知、记忆和处理成为可能。

- 此外,横河电机于2022年8月推出了两款新型频谱仪(OSA),以满足市场对可测量宽波长范围的仪器的需求,以满足独特的光学产品扩展和製造需求。横河马达的AQ6375E和AQ6376E是唯一覆盖2μm以上SWIR(短波红外线)和3μm以上MWIR(中波红外线)的基于光栅的OSA,具有先进的光学性能。

- 为了满足客户的多样化需求,公司正在扩大产品系列。例如,2022 年 4 月,专门製造各种光电设备的亿光电科技 (Everlight Line) 在其产品组合中推出了一系列新产品,包括光电二极体和光电电晶体。这些产品由第三方经销商Transfer Multisort Elektronik (TME) 提供。

- 对可再生能源日益增长的需求进一步推动了市场的发展。根据IRENA预测,印度的太阳能发电能力将在2022年达到峰值,超过62.8吉瓦,与前一年同期比较成长21.5%。

中东和非洲经济强劲成长

- 沙乌地阿拉伯、埃及和阿拉伯联合大公国等中东和非洲主要国家拥有该地区最广泛的可再生能源项目。复合半导体装置在控制再生能源来源的产生和将其连接到网路方面发挥关键作用。

- 此外,半导体产业在中东和非洲地区逐渐获得发展动力,创造了丰富的市场成长机会。例如,2022年3月,阿卜杜勒阿齐兹国王科技城(KACST)宣布启动沙乌地阿拉伯首个半导体计划,旨在支援电子晶片设计和在地化领域的研发和专家资格认证。

- 此外,5G 在中东和北非地区正在大力扩张。海湾国家在 5G 发展方面处于主导,各国政府和当局允许通讯业者进入许可权5G 发射频段,让他们能够建造世界上第一个也是最快的 5G 网路。据 GSMA 称,中东和北非 (MENA) 地区的多元化经济将从 5G 中受益匪浅,预计到 2030 年中频段将增加超过 160 亿美元的新 GDP(占该地区 GDP 的 0.35%)。

- 此外,2022年3月,南非跨国行动电信业者MTN宣布将在该国最大的省份北开普省和司法中心Free State投资超过4,225万美元用于网路建设和5G推广。这些倡议将促进这些地区的整体半导体产业发展,为市场成长创造积极的前景。

- 此外,杜拜预计将投入数百万迪拉姆作为奖励,到 2030 年让 42,000 辆电动车上路。通用汽车预计,随着雪佛兰电动车的推出,其在中东和非洲的销量将会成长。作为「智慧杜拜」计画的一部分,杜拜的电动车绿色充电站数量可能会增加一倍,该计画旨在使杜拜成为世界上最具创新性和最幸福的城市。杜拜电力和水务局宣布将在杜拜全境安装 100 个电动车绿色充电站,这是其绿色充电器计画第二阶段的一部分。

- 据气候现实计画称,世界上最大的聚光型太阳光电发电厂最近在杜拜附近竣工,预计将产生 1,000 兆瓦的电力。杜拜的目标是到2050年75%的能源来自清洁能源来源,2030年的能源结构目标是25%的能源来自太阳能。这些努力正在推动该地区的市场发展。

化合物半导体产业概况

复合半导体市场竞争激烈,主要由博通、Skyworks Solutions、Cree、Qorvo、Analog Devices、OSRAM、GaN Systems、Skyworks Solution 和英飞凌科技等大公司主导。由于拥有较大的市场占有率,这些大公司正致力于扩大海外基本客群。这些公司正在利用战略合作计划来增加市场占有率和盈利。然而,随着技术进步和产品创新,中小企业正在透过赢得独特的合约和探索新市场来扩大市场。

- 2022年6月,ams OSRAM宣布台湾Ledtech公司已采用OSLON UV 3636 UV-C LED用于其新型智慧空气清净机BioLED的杀菌功能。 BioLED 的 OSLON UV 3636 LED 的辐照率为 3.6mJ/cm2,能够灭活高达 99.99% 的病毒,包括 SARS-CoV-2。

- 2022年5月,Qorvo宣布推出新一代1200V SiCFET。新型 UF4C/SC 系列 1200V Gen 4 SiCFET(来自最近收购的 UnitedSiC)专为电动汽车车载充电器、工业电池充电器、工业电源、DC/DC 太阳能逆变器、焊接机、不断电系统和感应加热应用中的 800V 总线架构而设计。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概览

- 产业价值链分析

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买家的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 评估宏观经济趋势对市场的影响

第五章市场动态

- 市场驱动因素

- 电子和行动装置需求不断成长

- 提高工业自动化

- 市场挑战

- 原料和製造成本高

第六章市场区隔

- 按类型

- 砷化镓(GaAs)

- 氮化镓(GaN)

- 磷化镓(GaP)

- 碳化硅(SiC)

- 其他的

- 按产品

- LED

- RF

- 光电子

- 电力电子

- 其他的

- 按应用

- 通讯

- 资讯和通讯技术

- 国防与航太

- 家电

- 卫生保健

- 车

- 其他的

- 按地区

- 北美洲

- 美国

- 加拿大

- 欧洲

- 德国

- 法国

- 义大利

- 其他欧洲国家

- 亚太地区

- 中国

- 日本

- 印度

- 其他亚太地区

- 拉丁美洲

- 中东和非洲

- 北美洲

第七章竞争格局

- 公司简介

- Skyworks Solutions INC.

- Wolfspeed Inc.

- Qorvo Inc.

- Analog Devices Inc.

- OSRAM GmbH(ams-OSRAM AG)

- GaN Systems Inc.

- Infineon Technologies AG

- NXP Semiconductors NV

- Advanced Wireless Semiconductor Company

- STMicroelectronics NV

- Texas Instruments Inc.

- Microsemi Corporation(Microchip Technology Inc.)

- WIN Semiconductors Corp.

- ON Semiconductor Corp.(Semiconductor Components Industries Llc)

- Mitsubishi Electric Corporation

第八章投资分析

第九章:市场的未来

The Compound Semiconductor Market size is estimated at USD 36.15 billion in 2025, and is expected to reach USD 60.66 billion by 2030, at a CAGR of 10.91% during the forecast period (2025-2030).

The COVID-19 pandemic halted the manufacturing of several products in the compound semiconductor production industry owing to continued lockdown in critical global regions. In addition, country-wise lockdowns inflicted by governments across the globe further resulted in sectors taking a hit and disrupting supply chains and manufacturing operations worldwide. Most manufacturing operations, including the factory floor work, were significantly affected, resulting in decreased productivity.

Key Highlights

- Compound semiconductors are made from two or more elements of the different or same group of the periodic table. These are manufactured by using various types of deposition techniques, such as chemical vapor deposition, atomic layer deposition, and others. They possess unique properties like high temperature and heat resistance, enhanced frequency, high sensitivity to magnetism, and faster operation and optoelectronic features are some of the key advantages boosting their demand. Moreover, the decrease in the manufacturing cost of compound semiconductors has increased their application in electronic and mobile devices.

- The ability of compound semiconductors to emit and sense light in the form of general lighting (LEDs) and lasers and receivers for fiber optics is further driving the demand. The decrease in manufacturing and installation cost of LEDs has increased its application in lamps and fixtures across all sectors. Mega-cities concentrate on investing in infrastructure development to meet the needs of the growing population, and governments are helping customers to install energy-efficient lighting sources to reduce their electricity consumption costs.

- For instance, during the pandemic, EESL (Energy Efficiency Services Limited) celebrated the completion of its one-year governmental project called the Unnat Jyoti Program (UJALA). Under this program, it substituted more than 10.6 million street light bulbs with LED lights to reduce the carbon dioxide footprint by 20 million tons and the electricity cost. Such initiatives further boost the market studied.

- In 2020, the Taiwan Semiconductor Manufacturing Company (TSMC) sourced about 31% of spare parts locally in China, which increased to 31% in 2021.

- According to the US Department of Energy (DOE), LED lights use about 75-80% less energy than traditional incandescent light bulbs and about 65% less energy than halogen bulbs. Commercial enterprises need lighting for an extended period, whether for long working hours, safety and security in a warehouse or manufacturing facility, or other uses. Thus, switching to LED lights can save millions of dollars annually. For example, US Energy Recovery clients can save about 20-55% on their electric utility bills by swapping out old lighting systems for state-of-the-art LED lighting. Therefore, the shift toward LED adoption is driving the growth of the market studied.

- The smartphone is the major consumer of compound semiconductors. The smartphone market has been very competitive in recent years. The increasing usage of mobile phones is further anticipated to drive the global market. For instance, according to the Ericsson Mobility Report, 2022, by the end of 2027, there will be 4.4 billion 5G subscriptions globally, accounting for 48% of all mobile subscriptions.

- The Internet of Things applications are increasing, which is expected to boost the sales of compound semiconductors. Moreover, the wireless communications sector is expected to grow with the growth in 5G networks. Fifth-generation networks also indicate the likelihood of consumers upgrading their mobile handsets or devices to drive global compound semiconductor adoption.

- The compound semiconductor industry is considered one of the most complex industries, not only due to the more than 500 processing steps involved in the manufacturing and various products but also due to the harsh environment it faces, e.g., the volatile electronic market and the unpredictable demand.

Compound Semiconductor Market Trends

Optoelectronics to Have a Significant Growth During the Forecast Period

- Optoelectronic products covered under the study scope include photodiodes, phototransistors, optical spectrum analyzers, solar panels, and other optoelectronic devices, excluding LED products.

- GaN-based transistors are discovering new ways, particularly in optoelectronics, compared to SiC-based, as they are faster and more efficient. GaN has 1,000 times the electron mobility of silicon, along with relatively stable operability at higher temperatures.

- Recent advancements in the field of optoelectronics, such as plasmonic nanostructures, perovskite transistors, optically active quantum dots, microscopic light bulbs, low-cost 3D imaging, laser-powered 3D display technology, and Laser Li-Fi, are expected to cause a quantum shift in the dynamic applicability areas of optoelectronic apparatus.

- Further, in June 2022, a multiwavelength optoelectronic synapse that enables optical data detection, storage, and processing in the same device was created by researchers in the United States (University of Central Florida) and South Korea. The resultant in-sensor artificial visual system, which significantly improves processing effectiveness and picture identification precision, might use robotics, self-driving cars, and machine vision. Like the human eye, where the retina, through the synapse of the optic nerve, carries optical data, optoelectronic synapse allows optical data sensing, memory, and processing to be integrated into the same device.

- Additionally, in August 2022, Yokogawa launched two new optical spectrum analyzers (OSAs) to fulfill the market demand for an instrument capable of measuring a wide range of wavelengths to meet unique optical product expansion and manufacturing needs. The Yokogawa AQ6375E and AQ6376E are the only grating-based OSAs covering SWIR (Short-Wavelength InfraRed) over 2 μm and MWIR (Mid-Wavelength InfraRed) over 3 μm, with advanced optical performance.

- To meet the various needs of the customers, the firms are expanding their product portfolio. For instance, in April 2022, the Everlight line specializes in manufacturing different optoelectronic devices, introduced a wide range of new products in its portfolio, including photodiodes and phototransistors. These products are offered by third-distributor Transfer Multisort Elektronik (TME).

- Growing demands for renewable energy are further driving the studied Market. According to IRENA, the solar photovoltaic energy capability in the South Asian country of India peaked at over 62.8 gigawatts in 2022, up 21.5% from the previous year.

Middle East and Africa to Witness Significant Growth

- Prominent countries across the Middle East and Africa, such as Saudi Arabia, Egypt, and the United Arab Emirates, have some of the region's most extensive renewable energy programs. Compound semiconductor devices play a significant role in controlling the generation and link to the network of renewable energy sources.

- Moreover, the semiconductor industry is slowly gaining momentum in the Middle East and Africa, creating considerable market growth opportunities. For instance, in March 2022, the King AbdulazizCity for Science and Technology (KACST) announced the launch of the Saudi Semiconductor Program, the first of its kind in the province, which is desired to support the research, development, and qualification of professionals in the field of designing and localizing electronic chips.

- Furthermore, in the Middle East & North Africa, 5G is expanding significantly. The Gulf nations have taken the lead in developing 5G, and their governments and authorities have given mobile carriers access to the 5G launch spectrum so they may build some of the world's first and fastest 5G networks. According to GSMA, the diversified economies of the Middle East and North Africa (MENA) will significantly benefit from 5G, with the mid-band estimated to provide USD16 billion more in new GDP in 2030, or 0.35% of the region's GDP.

- In addition, in March 2022, MTN, a multinational mobile telecommunications firm based in South Africa, said it would invest more than USD 42.25 million in network development and a 5G push in the nation's largest province, the Northern Cape, and its judicial center, the Free State. Such initiatives to boost the overall semiconductor industry in these regions create a positive outlook for the growth of the studied market.

- Further, Dubai is expected to spend millions of Dirhams on incentives to have 42,000 EVs on its streets by 2030. General Motors expects to boost sales in the Middle East & Africa with the launch of its Chevrolet EV. The number of EV Green Charger stations in Dubai may be doubled as part of the 'Smart Dubai' initiative, which seeks to make Dubai the world's most innovative and happiest city. The Dubai Electricity and Water Authority announced the fulfillment of the second phase of its 'Green Charger' ambition, which contained the installation of additional 100 EV Green Charger stations across Dubai.

- According to the Climate Reality Project, the world's most extensive concentrated solar plant is due to be completed recently near Dubai, and it is expected to have a capacity of 1,000 MW. Dubai aims to produce 75% of its energy from clean sources by 2050, and its target energy mix for 2030 is 25% solar. These initiatives are driving the studied market in the region.

Compound Semiconductor Industry Overview

The Compound Semiconductor Market is highly competitive and is dominated by several major players like Broadcom, Skyworks Solutions, Cree, Qorvo, Analog Devices, OSRAM, GaN Systems, Skyworks Solution, and Infineon Technologies. These prominent players with a significant market share focus on extending their customer base across foreign nations. These companies leverage strategic cooperative initiatives to increase their market share and profitability. However, with technological advancements and product innovations, mid-size to smaller companies are growing their market by securing unique contracts and tapping new markets.

- June 2022 - ams OSRAM announced that Taiwan-based Ledtech had chosen OSLON UV 3636 UV-C LEDs for a sanitization function in its newBioLED intelligent air purifier. The BioLED's OSLON UV 3636 LEDs can inactivate up to 99.99% of viruses, including SARS-CoV-2, at a dosing rate of 3.6mJ/cm2.

- May 2022 - Qorvo introduced a new generation of 1200V SiCFETs. The new UF4C/SC series of 1200V Gen 4 SiCFETs (from recently acquired UnitedSiC) are designed for 800V bus architectures in onboard chargers for electric vehicles, industrial battery chargers, industrial power supplies, DC/DC solar inverters, welding machines, uninterruptible power supplies, and induction heating applications.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitutes

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Assessment of Impact of Macroeconomic Trends on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rise in Demand for Electronic and Mobile Devices

- 5.1.2 Increase in Industrial Automation

- 5.2 Market Challenges

- 5.2.1 High Raw Material and Fabrication Costs

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Gallium Arsenide (GaAs)

- 6.1.2 Gallium Nitride (GaN)

- 6.1.3 Gallium Phosphide (GaP)

- 6.1.4 Silicon Carbide (SiC)

- 6.1.5 Others

- 6.2 By Product

- 6.2.1 LED

- 6.2.2 RF

- 6.2.3 Optoelectronics

- 6.2.4 Power Electronics

- 6.2.5 Other Products

- 6.3 By Application

- 6.3.1 Telecommunications

- 6.3.2 Information & Communication Technology

- 6.3.3 Defense & Aerospace

- 6.3.4 Consumer Electronics

- 6.3.5 Healthcare

- 6.3.6 Automotive

- 6.3.7 Other Applications

- 6.4 By Geography

- 6.4.1 North America

- 6.4.1.1 United States

- 6.4.1.2 Canada

- 6.4.2 Europe

- 6.4.2.1 Germany

- 6.4.2.2 France

- 6.4.2.3 Italy

- 6.4.2.4 Rest of Europe

- 6.4.3 Asia Pacific

- 6.4.3.1 China

- 6.4.3.2 Japan

- 6.4.3.3 India

- 6.4.3.4 Rest of the Asia Pacific

- 6.4.4 Latin America

- 6.4.5 Middle East and Africa

- 6.4.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Skyworks Solutions INC.

- 7.1.2 Wolfspeed Inc.

- 7.1.3 Qorvo Inc.

- 7.1.4 Analog Devices Inc.

- 7.1.5 OSRAM GmbH (ams-OSRAM AG)

- 7.1.6 GaN Systems Inc.

- 7.1.7 Infineon Technologies AG

- 7.1.8 NXP Semiconductors NV

- 7.1.9 Advanced Wireless Semiconductor Company

- 7.1.10 STMicroelectronics N.V.

- 7.1.11 Texas Instruments Inc.

- 7.1.12 Microsemi Corporation (Microchip Technology Inc.)

- 7.1.13 WIN Semiconductors Corp.

- 7.1.14 ON Semiconductor Corp. (Semiconductor Components Industries Llc)

- 7.1.15 Mitsubishi Electric Corporation

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

化合物半导体市场机会、成长要素、产业趋势分析及2026-2035年预测。

化合物半导体市场机会、成长要素、产业趋势分析及2026-2035年预测。 系统半导体市场:2026年至2032年全球预测(依产品类型、材料类型、技术、外形规格、连接方式、应用和最终用途产业划分)

系统半导体市场:2026年至2032年全球预测(依产品类型、材料类型、技术、外形规格、连接方式、应用和最终用途产业划分) 2026年全球化合物半导体市场报告2026年全球磷化铟化合物半导体市场报告

2026年全球化合物半导体市场报告2026年全球磷化铟化合物半导体市场报告 全球化合物半导体市场:市场规模、占有率、成长率、产业分析、依类型、应用和地区划分的分析以及未来预测(2026-2034)按设备类型、产品材料、基板和最终用途分類的水平式低压化学气相沉积市场-2026-2032年全球预测

全球化合物半导体市场:市场规模、占有率、成长率、产业分析、依类型、应用和地区划分的分析以及未来预测(2026-2034)按设备类型、产品材料、基板和最终用途分類的水平式低压化学气相沉积市场-2026-2032年全球预测 化合物半导体市场规模、份额及成长分析(按产品、应用、类型及地区划分)-2026-2033年产业预测

化合物半导体市场规模、份额及成长分析(按产品、应用、类型及地区划分)-2026-2033年产业预测 化合物半导体材料市场规模、份额及成长分析(按产品、材料、应用及地区划分)-2026-2033年产业预测

化合物半导体材料市场规模、份额及成长分析(按产品、材料、应用及地区划分)-2026-2033年产业预测 复合半导体材料市场预测至2032年:依产品形态、材料类型、加工服务、应用、最终用户和地区的全球分析化合物半导体市场规模:依板材类型、材料、车辆类型、区域范围和预测

复合半导体材料市场预测至2032年:依产品形态、材料类型、加工服务、应用、最终用户和地区的全球分析化合物半导体市场规模:依板材类型、材料、车辆类型、区域范围和预测